Download to read offline

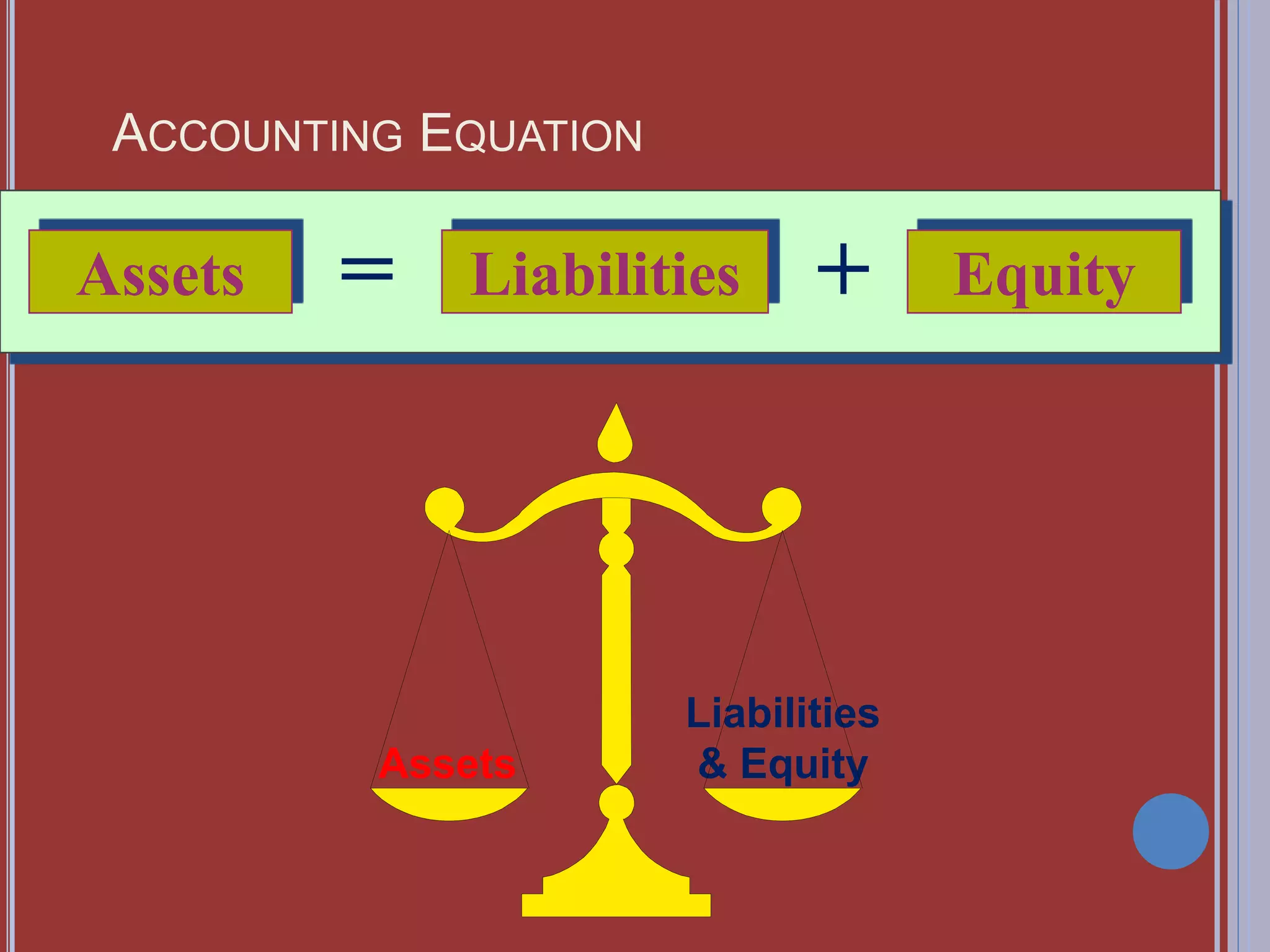

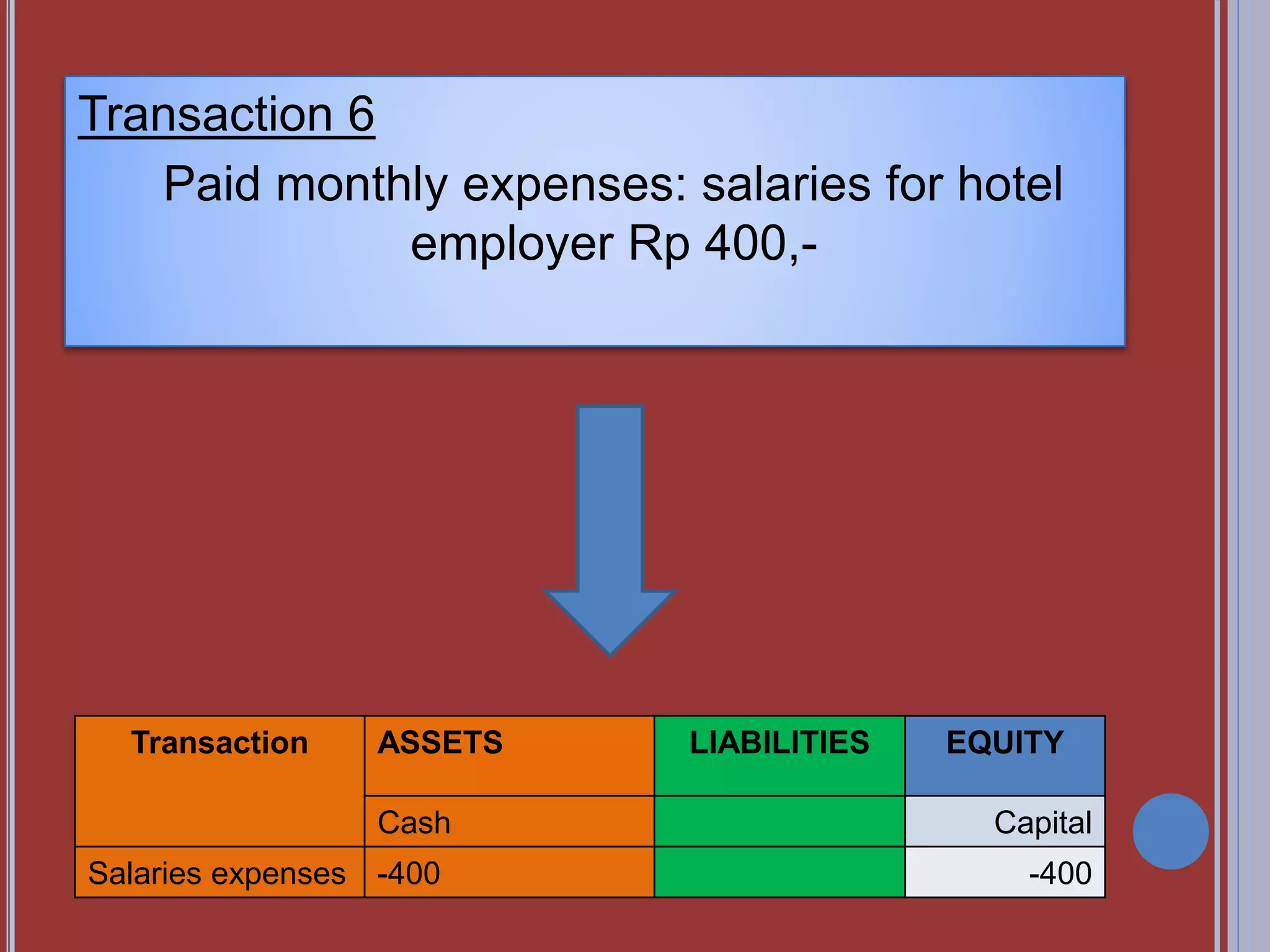

1. Akun (account) merujuk pada aset, hutang, pendapatan, beban, dan modal yang diwakili oleh masing-masing halaman buku besar, dimana perubahan nilainya dicatat secara kronologis dengan entry debit dan kredit. 2. Aset merujuk pada sumber daya atau hal-hal bernilai yang dimiliki perusahaan. Beberapa jenis aset antara lain: kas, piutang usaha, persediaan, perlengkapan, investasi, tanah, bangunan, peral

![1 book-keeping dr[1]. & cr.](https://cdn.slidesharecdn.com/ss_thumbnails/1-book-keepingdr1-cr-110822014205-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)