Downloaded 238 times

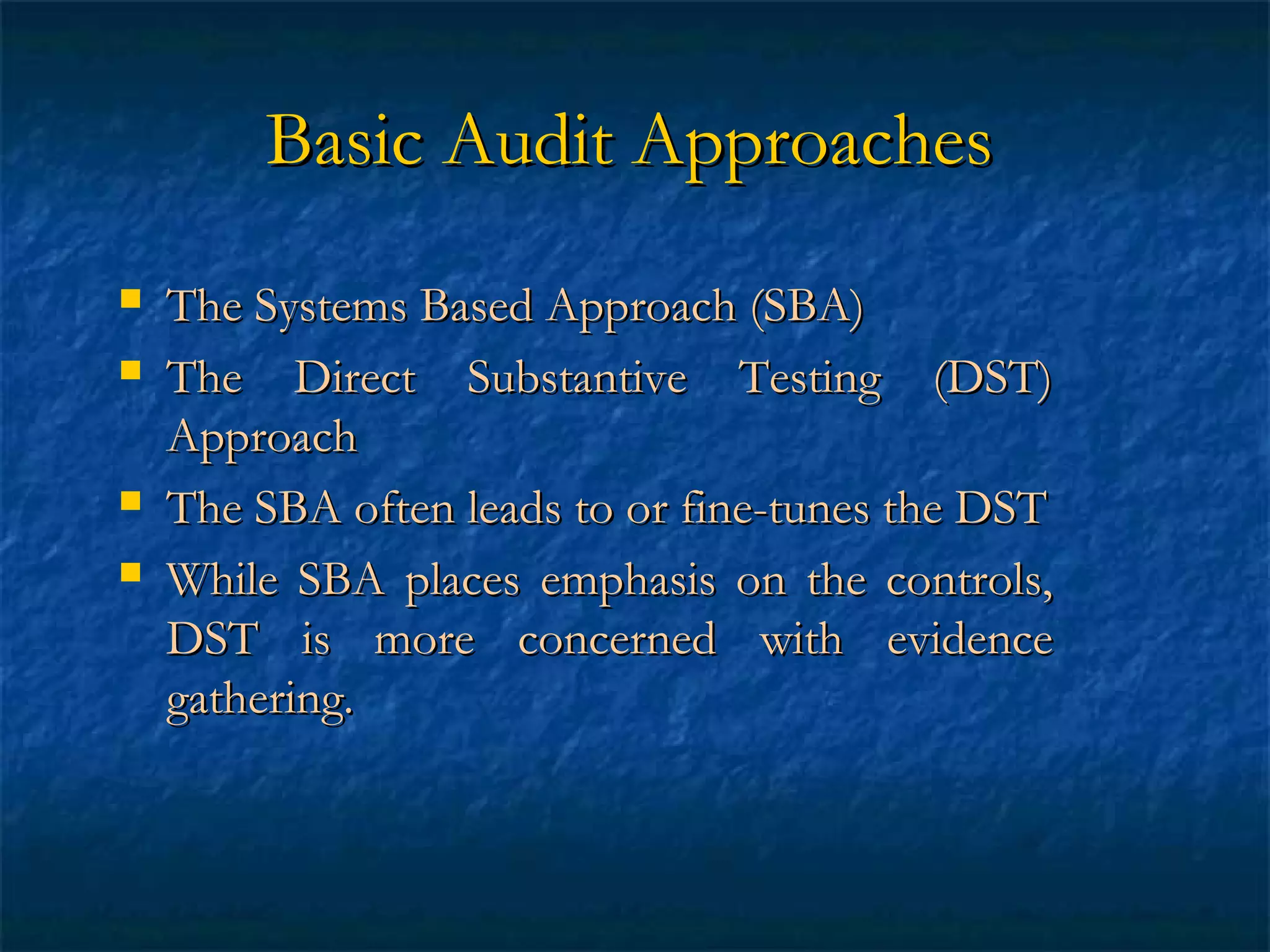

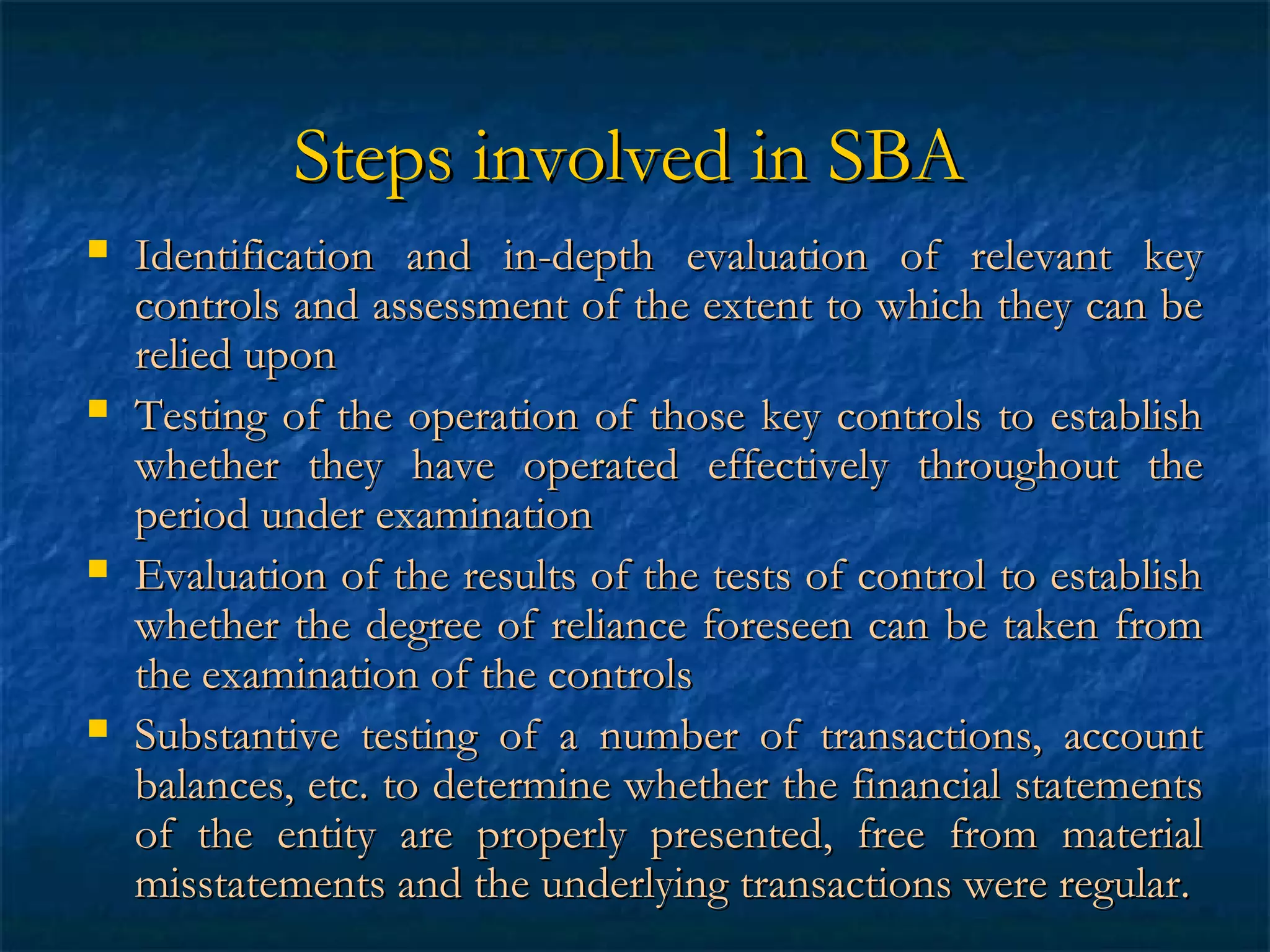

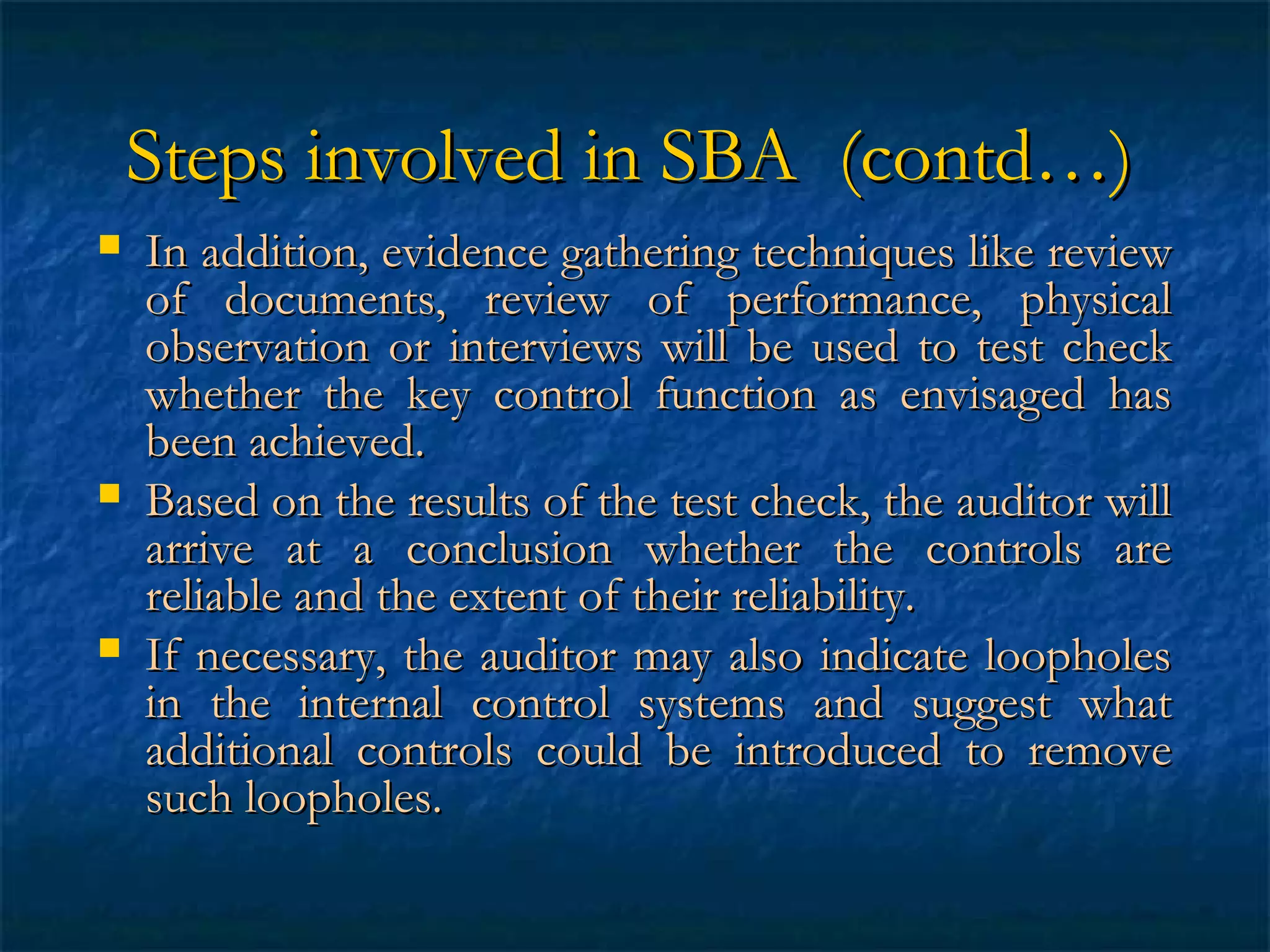

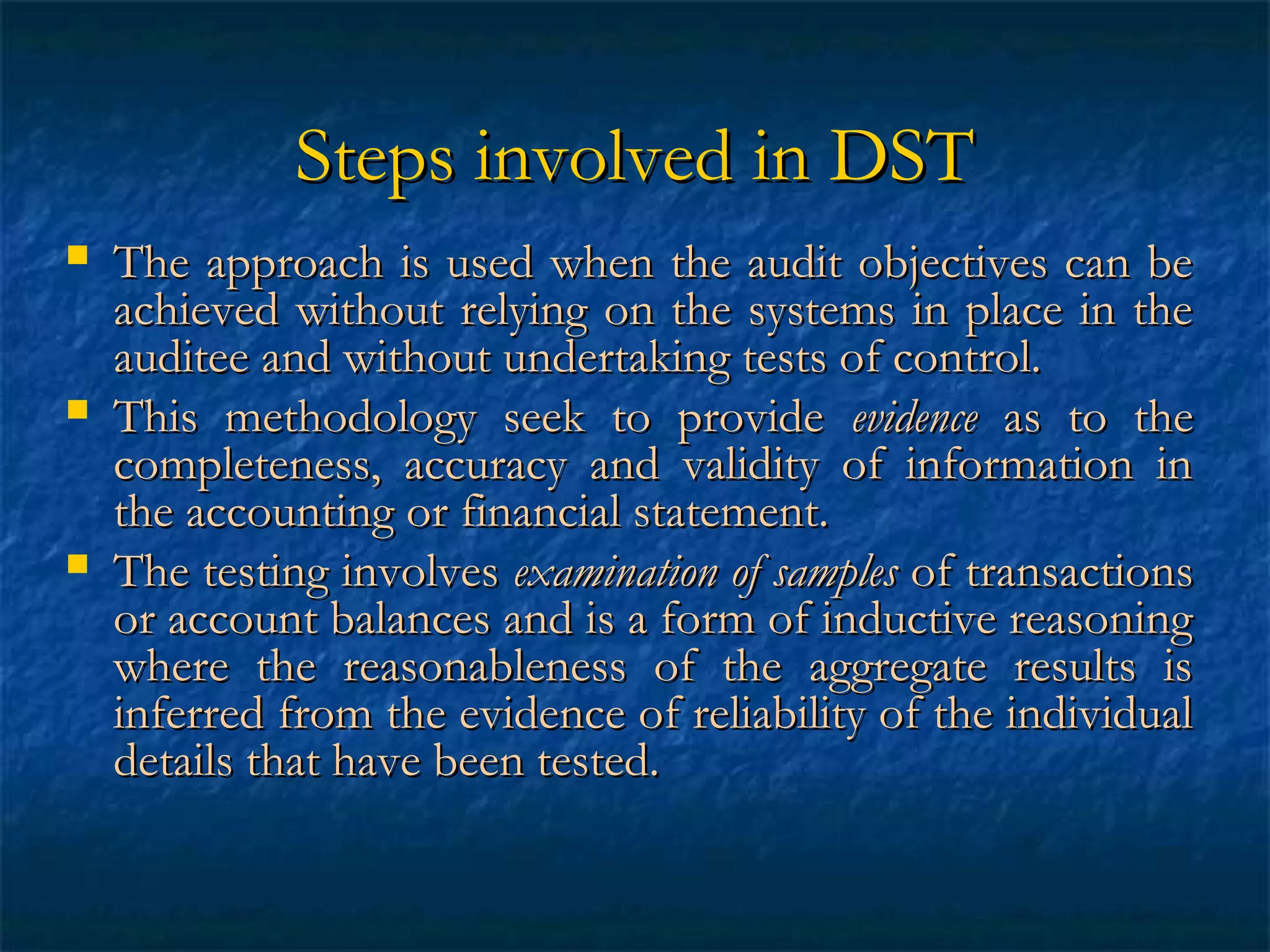

Analytical procedures and two basic audit approaches - systems based approach and direct substantive testing - are commonly used in audits. Analytical procedures involve analyzing financial ratios and trends to identify unexpected fluctuations. The systems based approach relies on evaluating internal controls, while direct substantive testing gathers evidence through examining transactions without relying on controls. Both approaches use procedures like analytical reviews, sampling, confirmations, and documentation to gather evidence and assess audit risk. The level of substantive testing required depends on the risks identified and whether controls can be relied upon.

![AUDIT REPORT [ AUDITING ]](https://cdn.slidesharecdn.com/ss_thumbnails/auditingtypesofauditreport-210303052610-thumbnail.jpg?width=640&height=640&fit=bounds)