The substantiveprocedures approach

This is also referred to as the vouching approach or

the direct verification approach.

In this approach, audit resources are targeted on

testing large volumes of transactions and account

balances without any particular focus on specified

areas of the financial statements.

4.

The balancesheet approach

In this approach, substantive procedures are focused on

balance sheet (statement of financial position) accounts,

with only very limited procedures being carried out on

income statement/profit and loss account items.

The justification for this approach is the notion that if

the relevant management assertions for all balance sheet

(statement of financial position) accounts are tested and

verified, then the profit/loss figure reported for the

accounting period will not be materially misstated.

5.

The systems-basedapproach

The approach whereby the auditor relies upon the entity’s

system of internal control

This approach requires auditors to assess the

effectiveness of the internal controls of an entity, and

then to direct substantive procedures primarily to those

areas where it is considered that systems objectives will

not be met.

Reduced testing is carried out in those areas where it is

considered systems objectives will be met.

6.

The risk-basedapproach

In this approach, audit resources are directed

towards those areas of the financial statements that

may contain misstatements (either by error or

omission) as a consequence of the risks faced by the

business.

ERCA is emphasizing the risk based approach.

7.

Risk based Audittests

Set audit objectives

- transaction related

- balance related

Asses and evaluate internal controls

Design and perform audit tests

8.

Analytical Procedures

Whatare analytical procedures?

Variation Analysis

Ratio Analysis

Trend Analysis

Why use analytical procedures?

Typically, analytical procedures are a quick way to point out

unusual trends or activity in account balances

8

04/26/2025

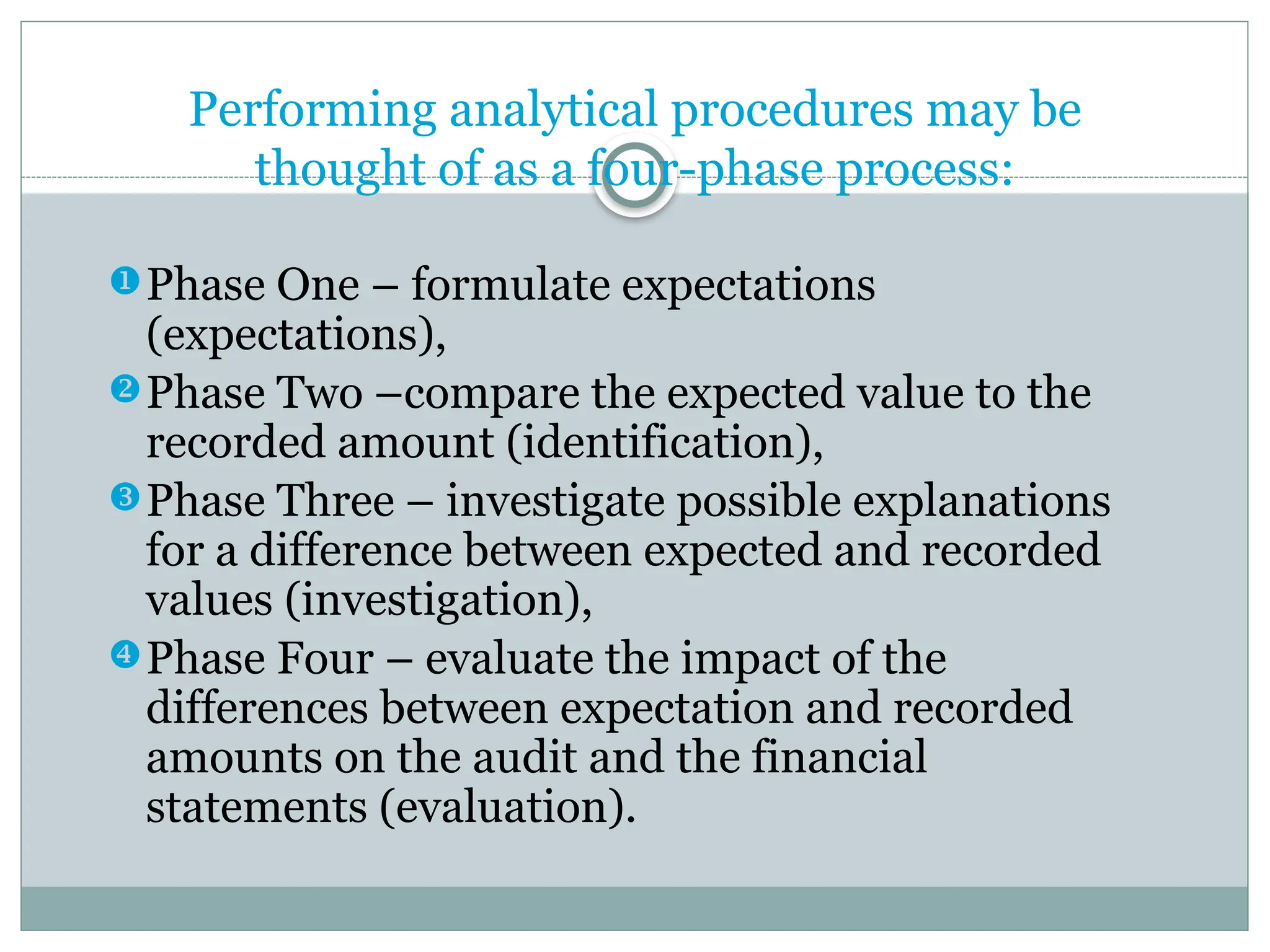

9.

Performing analytical proceduresmay be

thought of as a four-phase process:

Phase One – formulate expectations

(expectations),

Phase Two –compare the expected value to the

recorded amount (identification),

Phase Three – investigate possible explanations

for a difference between expected and recorded

values (investigation),

Phase Four – evaluate the impact of the

differences between expectation and recorded

amounts on the audit and the financial

statements (evaluation).

10.

04/26/2025

10

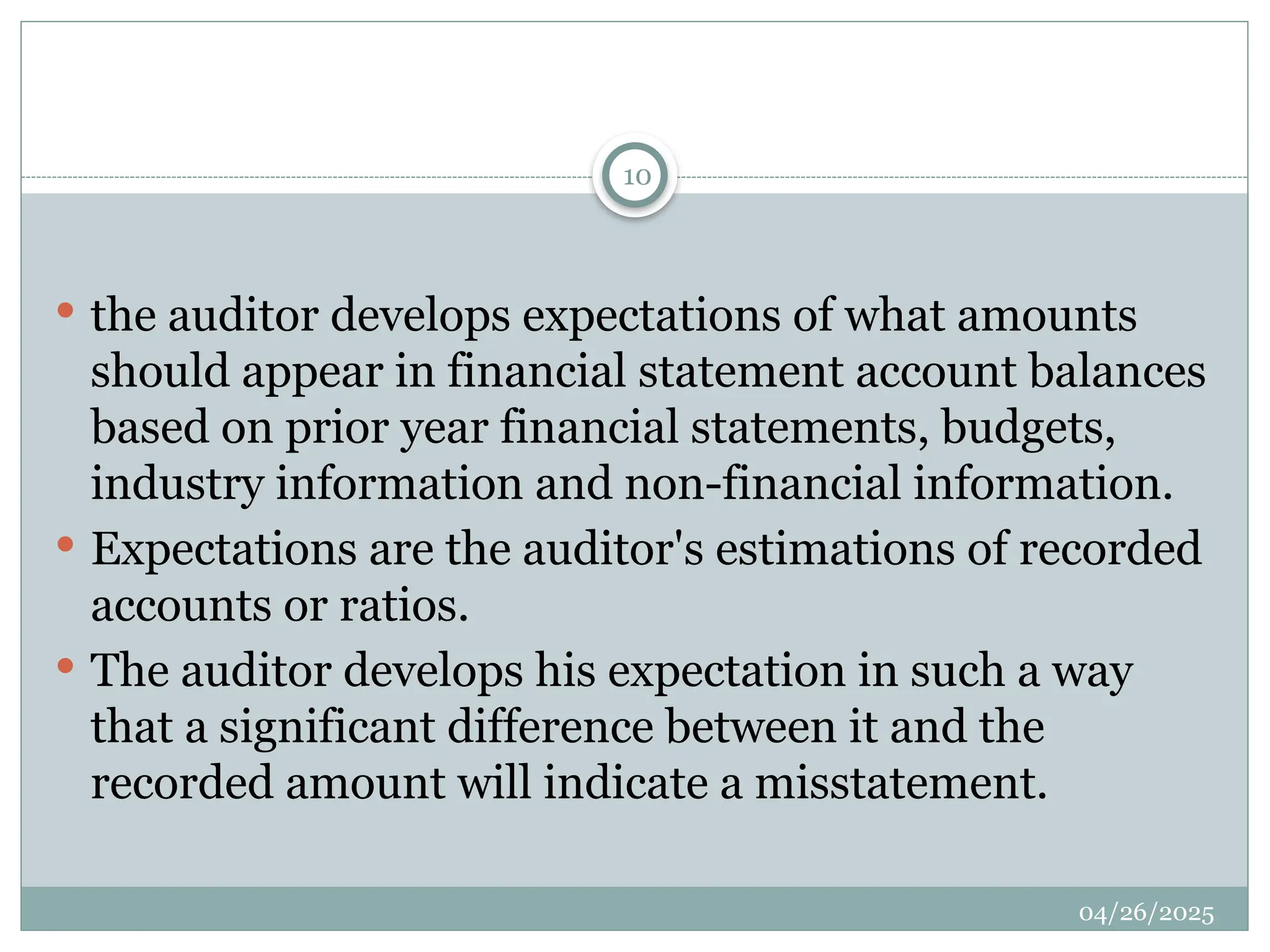

the auditordevelops expectations of what amounts

should appear in financial statement account balances

based on prior year financial statements, budgets,

industry information and non-financial information.

Expectations are the auditor's estimations of recorded

accounts or ratios.

The auditor develops his expectation in such a way

that a significant difference between it and the

recorded amount will indicate a misstatement.

11.

04/26/2025

11

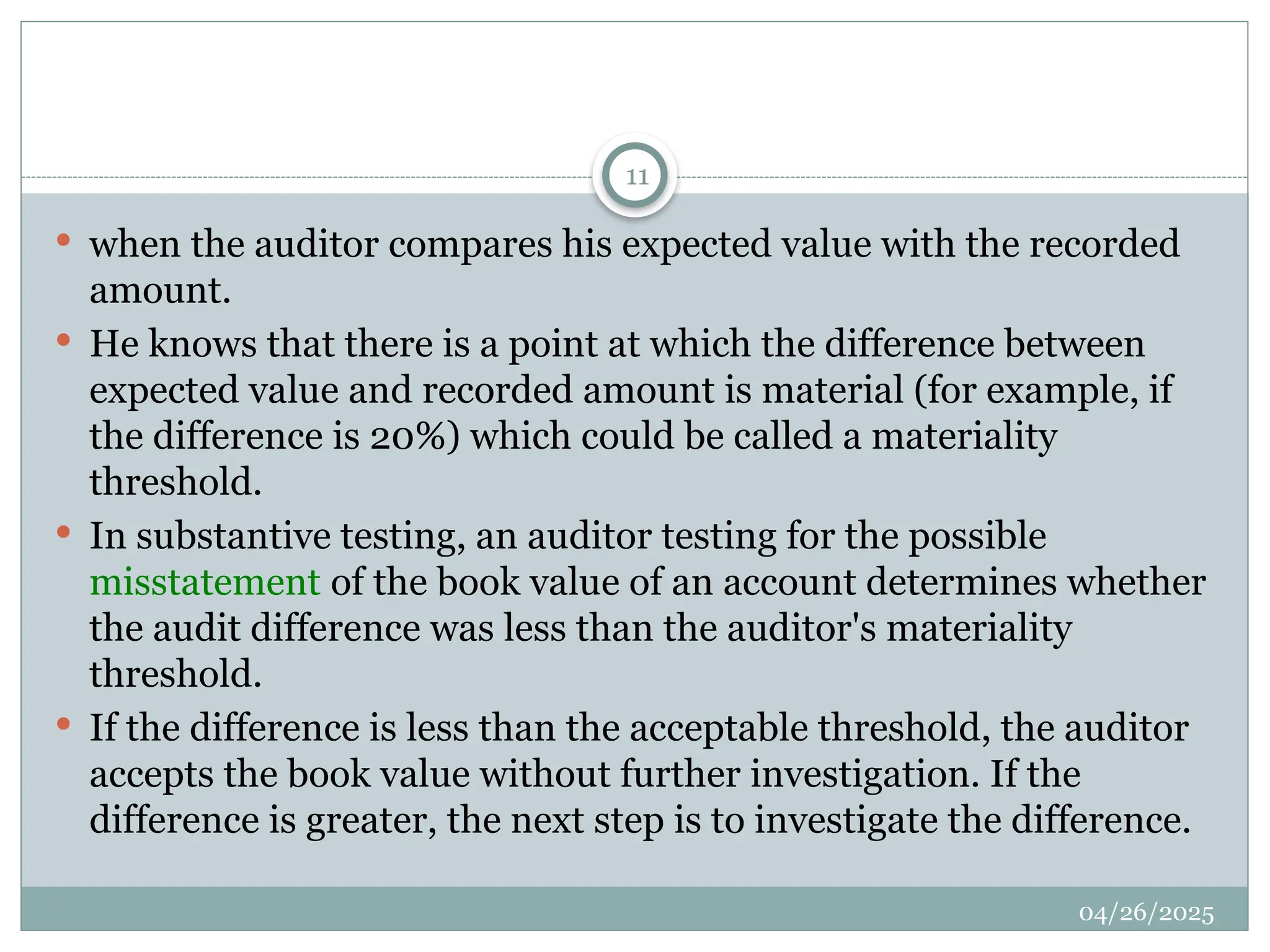

when theauditor compares his expected value with the recorded

amount.

He knows that there is a point at which the difference between

expected value and recorded amount is material (for example, if

the difference is 20%) which could be called a materiality

threshold.

In substantive testing, an auditor testing for the possible

misstatement of the book value of an account determines whether

the audit difference was less than the auditor's materiality

threshold.

If the difference is less than the acceptable threshold, the auditor

accepts the book value without further investigation. If the

difference is greater, the next step is to investigate the difference.

12.

04/26/2025

12

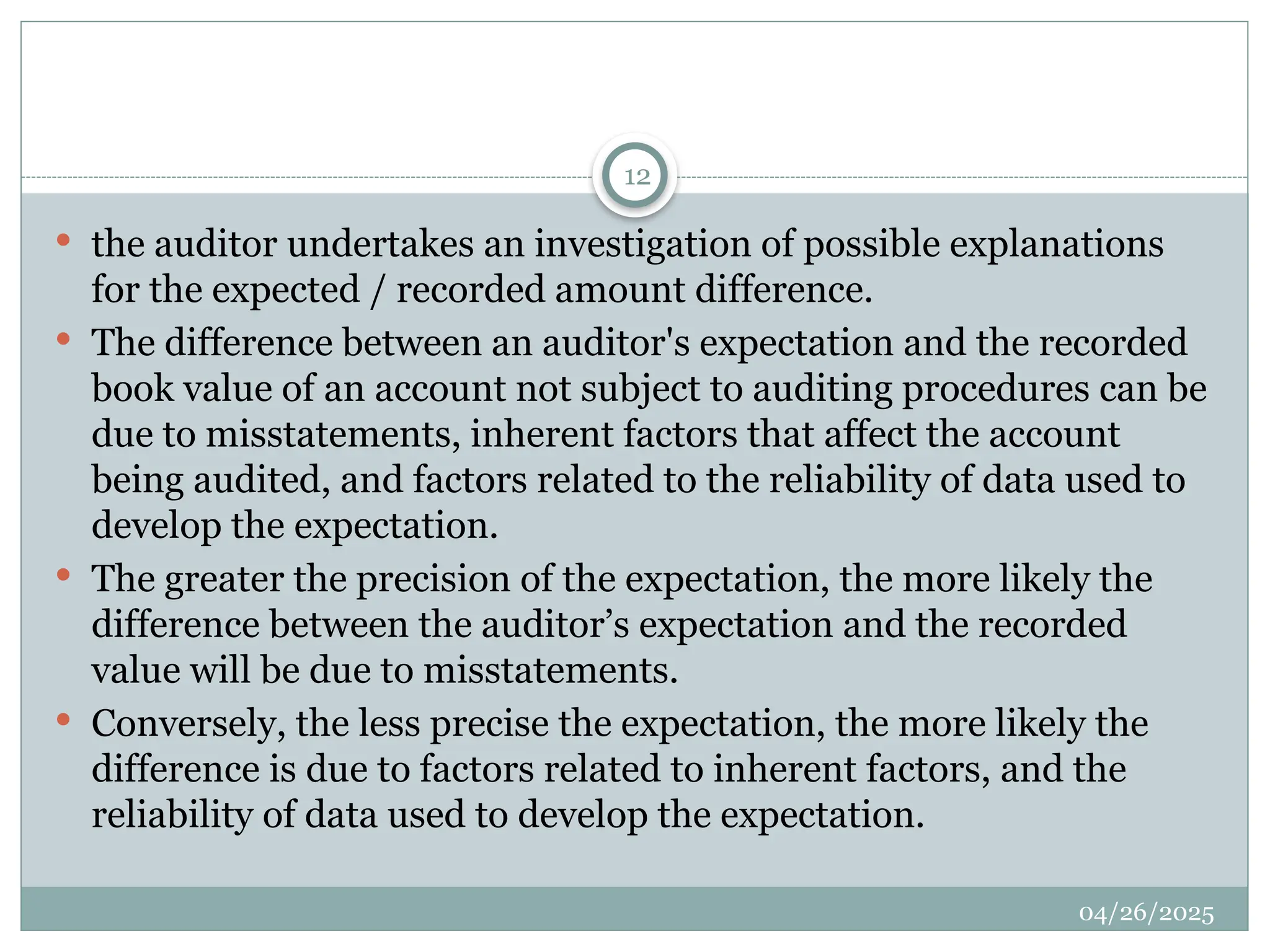

the auditorundertakes an investigation of possible explanations

for the expected / recorded amount difference.

The difference between an auditor's expectation and the recorded

book value of an account not subject to auditing procedures can be

due to misstatements, inherent factors that affect the account

being audited, and factors related to the reliability of data used to

develop the expectation.

The greater the precision of the expectation, the more likely the

difference between the auditor’s expectation and the recorded

value will be due to misstatements.

Conversely, the less precise the expectation, the more likely the

difference is due to factors related to inherent factors, and the

reliability of data used to develop the expectation.

13.

04/26/2025

13

Evaluate the impactof the differences between expectation and recorded

amounts on the audit and the financial statements (evaluation).

The final phase (phase four) of the analytical procedure process

involves evaluating the impact on the financial statements of the

difference between the auditor's expected value and the recorded

amount.

It is usually not practical to identify factors that explain the exact

amount of a difference investigated.

The auditor attempts to quantify that portion of the difference for

which plausible explanations can be obtained and, where appropriate,

corroborated.

If the amount that cannot be explained is sufficiently small, the

auditor may conclude there is no material misstatement.

14.

Analytical Procedures (cont)

Variation Analysis

Used to note unusual variations between certain related accounts or

to note variations between different time periods for one account

Also used to note variances between budgeted and actual amounts

What types of accounts are related?

Sales and A/R, COGS and Inventory, PP&E and Depreciation,

Gaming Revenues and Promotional Allowances, etc.

Why are the relationships important?

14

04/26/2025

15.

Analytical Procedures (cont)

Time Periods to Review

Balance Sheet accounts are typically reviewed month to month

or the most current month to the previous audited period,

which is typically year end.

Income Statement accounts are typically reviewed using the

same month or period of time from one year to the next,

especially in the hospitality industry. WHY?

These accounts are also compared against budgeted amounts.

15

04/26/2025

16.

Analytical Procedures (cont)

Ratio Analysis

Use of ratios to analyze

Types of ratios?

Current Ratio

Debt to Equity

Inventory Turnover

Gaming Specific Ratios

Hold %

RevPAR

Average Daily Rate

Occupancy %

Metrics against birr values (i.e. number of markers, fills per

ETB1,000 in drop)

16

04/26/2025

17.

Analytical Procedures (cont)

Trend Analysis

Review of trends in accounts. This is part of variation analysis.

Account balances climbing or declining at certain times of the

year.

Why would this happen?

Earnings Management

Bonuses

Proper Accounting

Other unusual items

17

04/26/2025

18.

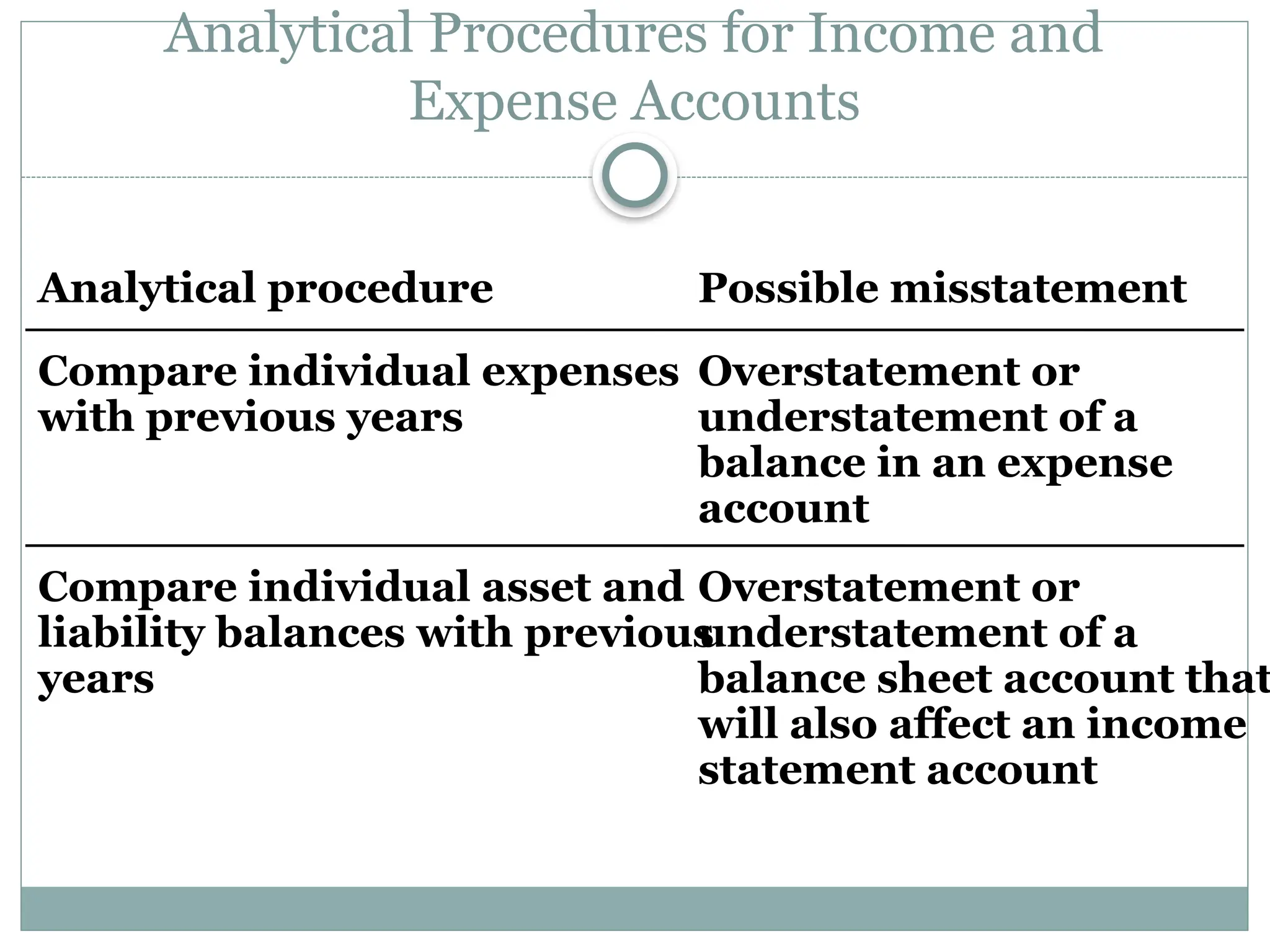

Analytical Procedures forIncome and

Expense Accounts

Compare individual asset and

liability balances with previous

years

Overstatement or

understatement of a

balance sheet account that

will also affect an income

statement account

Analytical procedure

Compare individual expenses

with previous years

Overstatement or

understatement of a

balance in an expense

account

Possible misstatement

19.

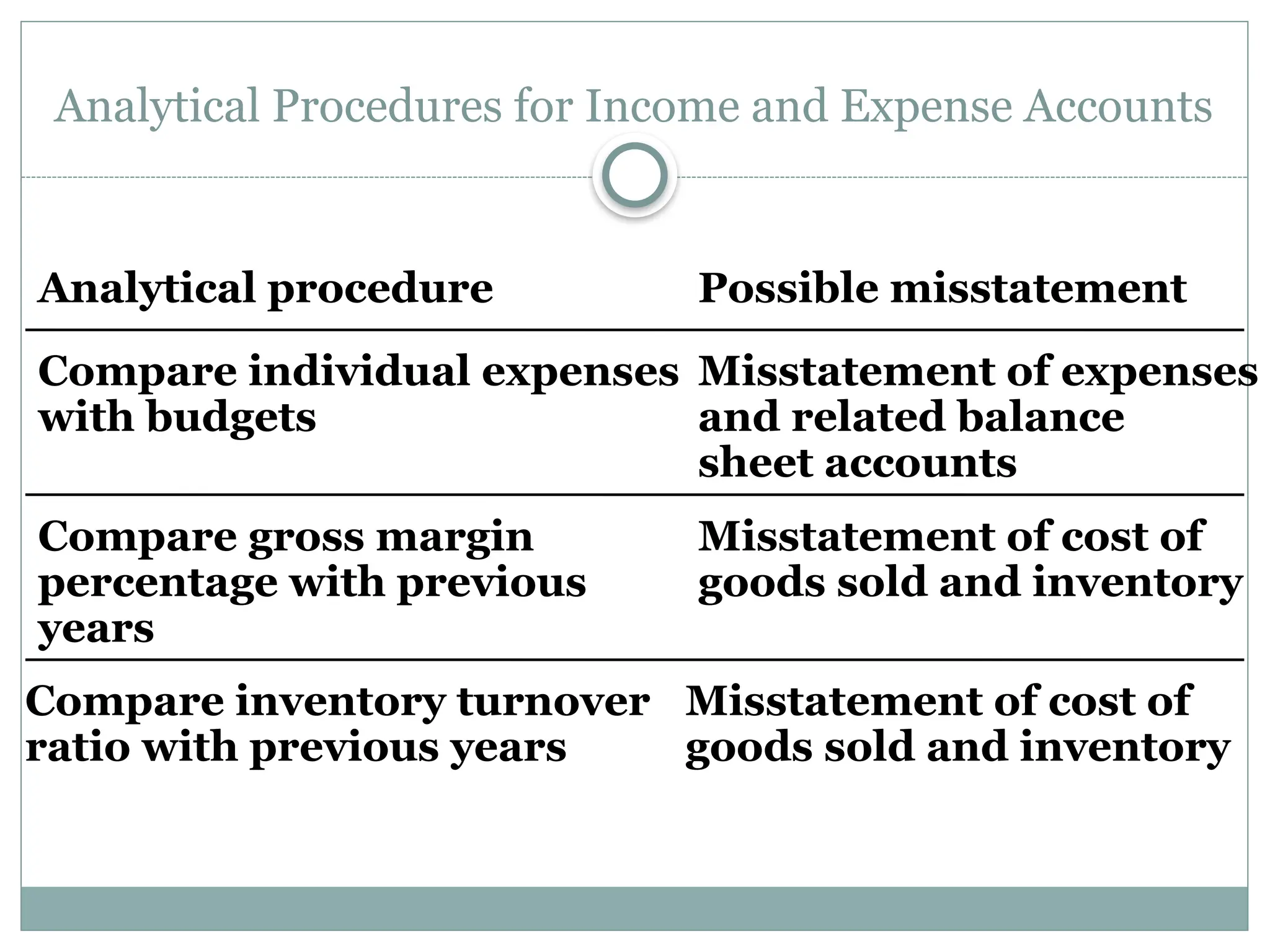

Analytical Procedures forIncome and Expense Accounts

Analytical procedure

Compare individual expenses

with budgets

Misstatement of expenses

and related balance

sheet accounts

Possible misstatement

Compare gross margin

percentage with previous

years

Misstatement of cost of

goods sold and inventory

Compare inventory turnover

ratio with previous years

Misstatement of cost of

goods sold and inventory

20.

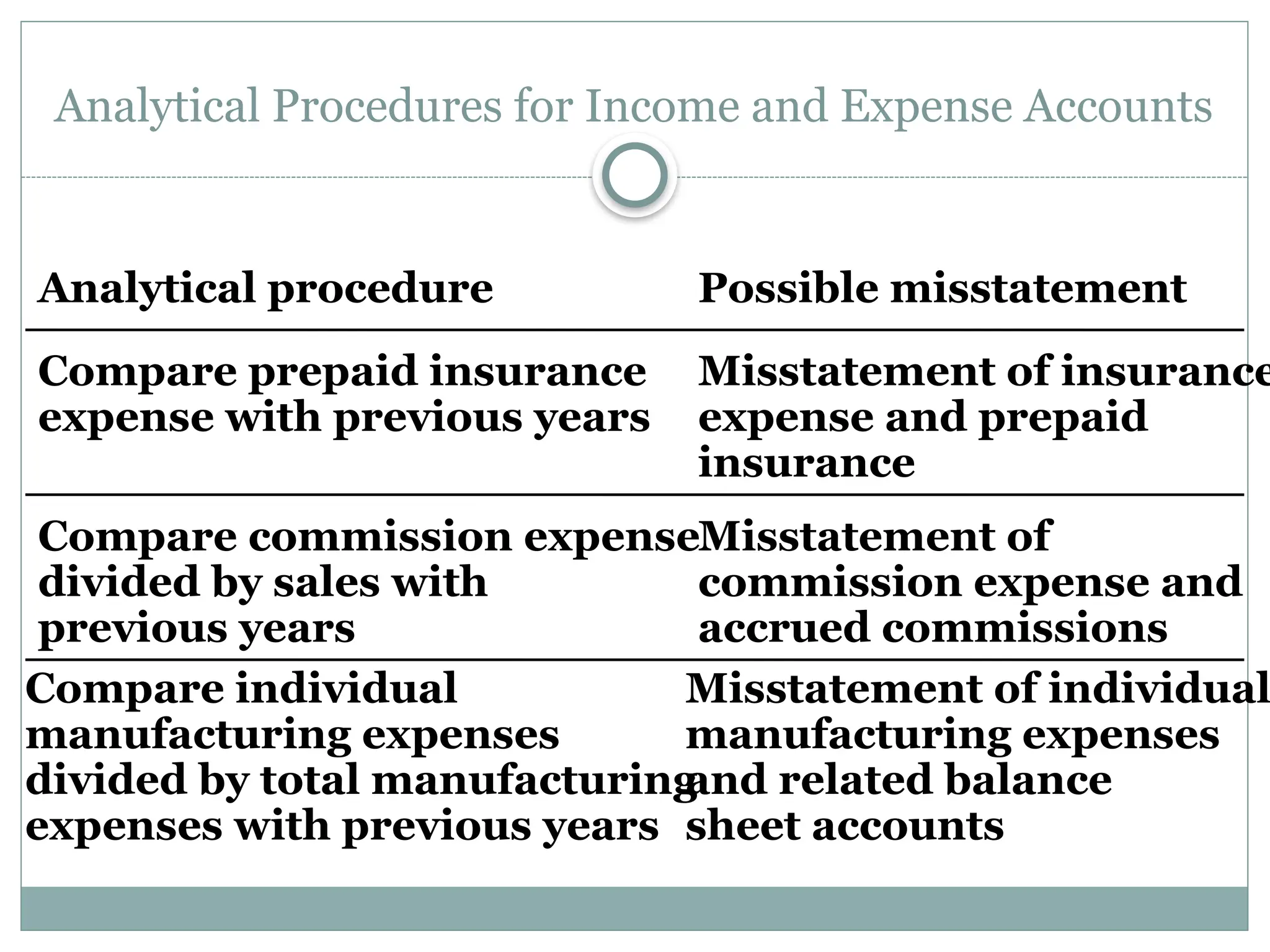

Analytical Procedures forIncome and Expense Accounts

Analytical procedure

Compare prepaid insurance

expense with previous years

Misstatement of insurance

expense and prepaid

insurance

Possible misstatement

Compare commission expense

divided by sales with

previous years

Misstatement of

commission expense and

accrued commissions

Compare individual

manufacturing expenses

divided by total manufacturing

expenses with previous years

Misstatement of individual

manufacturing expenses

and related balance

sheet accounts

21.

Tests of Controlsand Substantive

Test of Transactions

Both tests of controls and substantive

tests of transactions have the effect of

simultaneously verifying balance sheet

and income statement accounts.

22.

Assessing Control Riskfor Business Processes

If control risk is set at the maximum – the auditor does not rely on controls.

Instead extensive substantive procedures are used.

If a reliance strategy is followed – the auditor determines if controls may be

relied upon.

If controls are operating effectively – the auditor may reduce control risk below

the maximum.

22

04/26/2025

23.

Tests of Detailsof Account Balances – Expense Analysis

Expense account analysis:

Repairs and maintenance

Rent and lease

Legal expense

24.

Tests of Detailsof Account

Balances – Allocation

Several expense accounts result from the allocation

of accounting data rather than discrete transactions.

These include depreciation, depletion, and the

amortization of copyrights and catalog cost.

The allocation of manufacturing overhead between

inventory and cost of goods sold is an example of

a different type of allocation that affects expenses.

25.

Detail Audit Testing

Typically audit testing is done using samples or

scopes.

You also have to determine which accounts to test

and which specific items in that accounts also.

The detail testing is done in conjunction with

analytical procedures, observations, inquiries and

risk analysis to address all areas of concern.

25

04/26/2025

26.

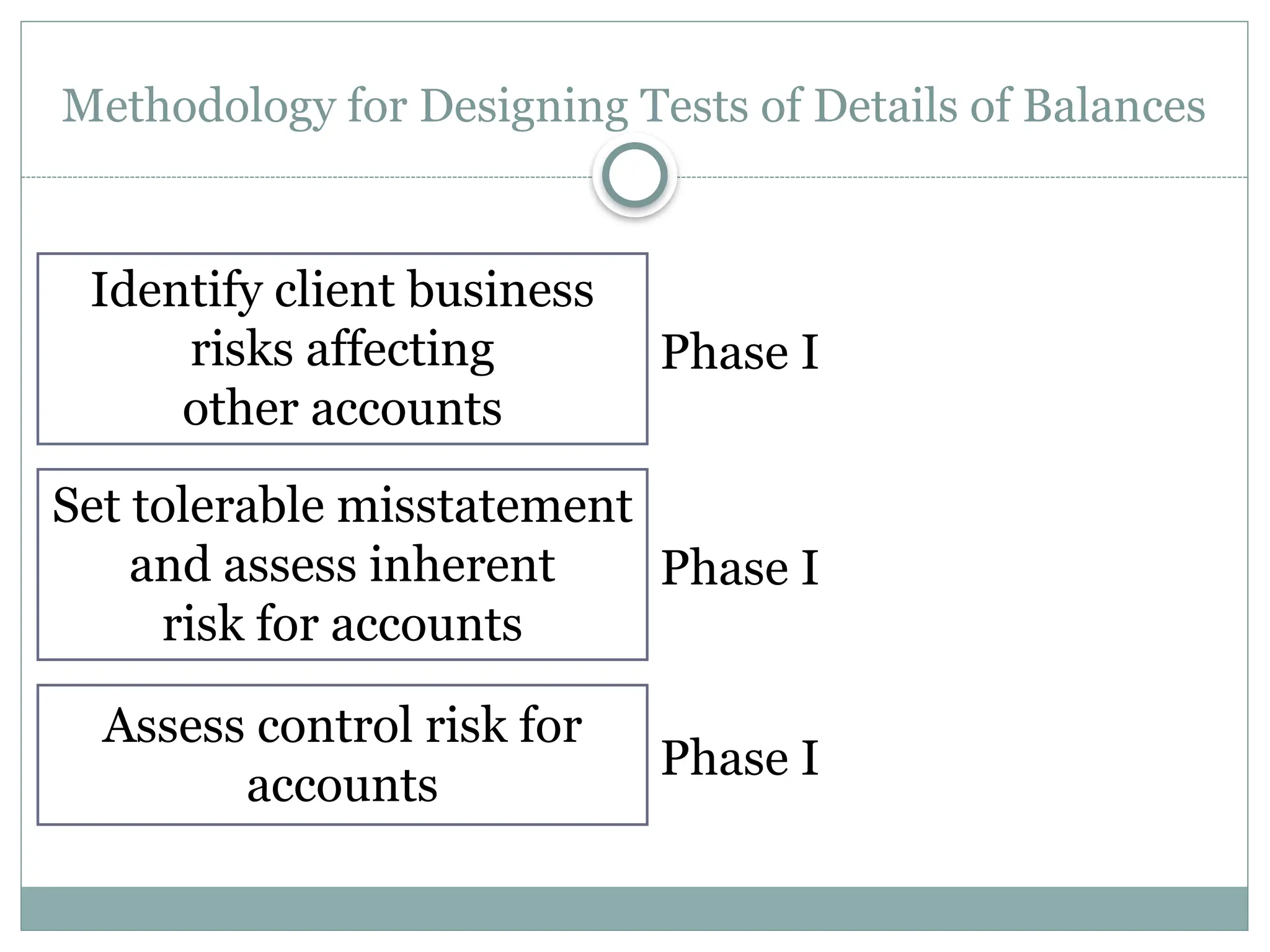

Identify client business

risksaffecting

other accounts

Methodology for Designing Tests of Details of Balances

Set tolerable misstatement

and assess inherent

risk for accounts

Assess control risk for

accounts

Phase I

Phase I

Phase I

27.

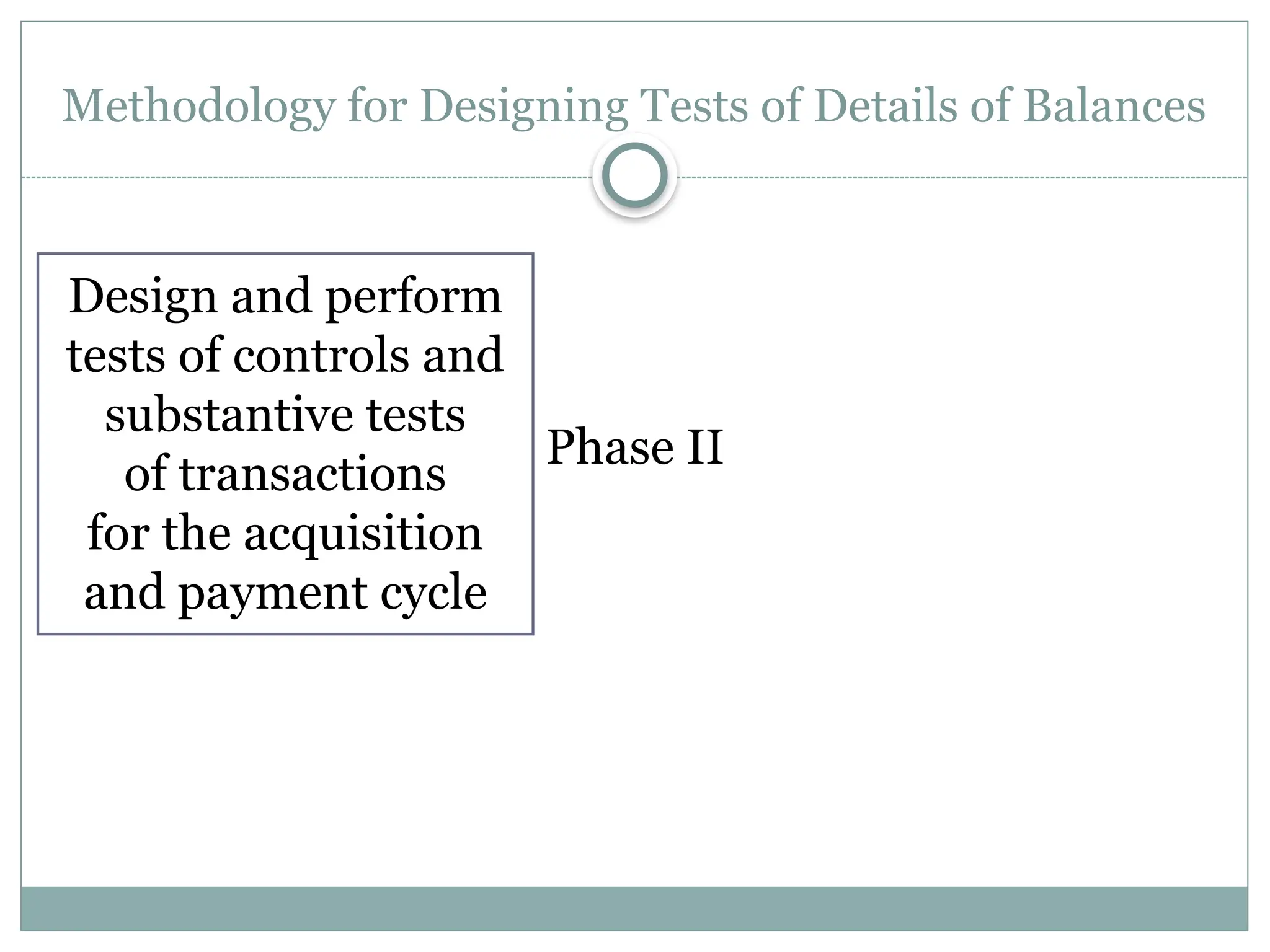

Methodology for DesigningTests of Details of Balances

Design and perform

tests of controls and

substantive tests

of transactions

for the acquisition

and payment cycle

Phase II

28.

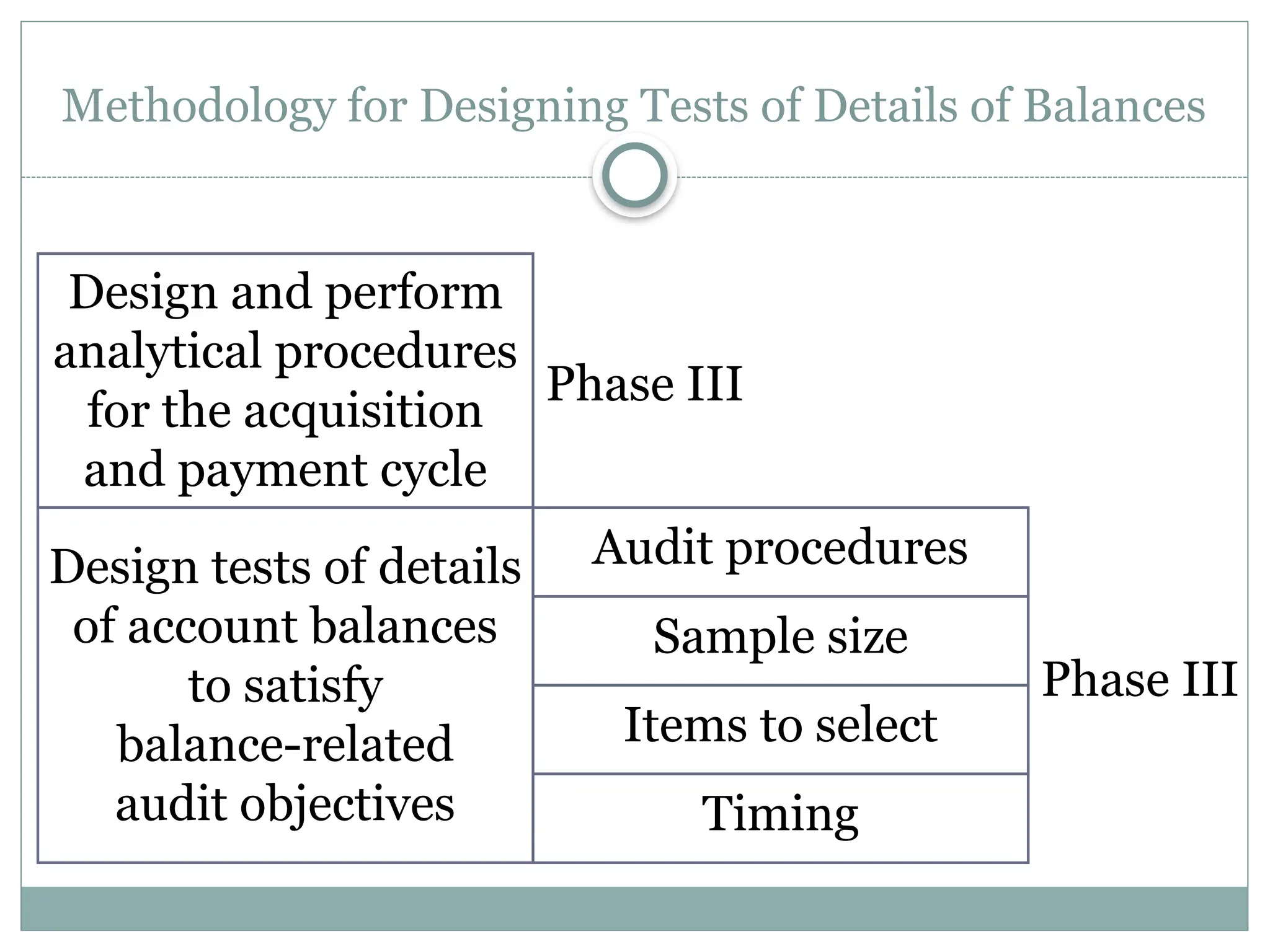

Timing

Items to select

Samplesize

Audit procedures

Methodology for Designing Tests of Details of Balances

Design and perform

analytical procedures

for the acquisition

and payment cycle

Design tests of details

of account balances

to satisfy

balance-related

audit objectives

Phase III

Phase III