Asset Securitization Theory And Practice Joseph C Huauth

Asset Securitization Theory And Practice Joseph C Huauth

Asset Securitization Theory And Practice Joseph C Huauth

Asset Securitization Theory And Practice Joseph C Huauth

Asset Securitization Theory And Practice Joseph C Huauth

1.

Asset Securitization TheoryAnd Practice Joseph

C Huauth download

https://ebookbell.com/product/asset-securitization-theory-and-

practice-joseph-c-huauth-4299514

Explore and download more ebooks at ebookbell.com

2.

Here are somerecommended products that we believe you will be

interested in. You can click the link to download.

Securitization Economics Deconstructing The Economic Foundations Of

Asset Securitization 1st Ed Laurent Gauthier

https://ebookbell.com/product/securitization-economics-deconstructing-

the-economic-foundations-of-asset-securitization-1st-ed-laurent-

gauthier-22503906

Structured Finance Leveraged Buyouts Project Finance Asset Finance And

Securitization Charleshenri Larreur

https://ebookbell.com/product/structured-finance-leveraged-buyouts-

project-finance-asset-finance-and-securitization-charleshenri-

larreur-46639502

Structured Finance Lbos Project Finance Asset Finance And

Securitization Charleshenri Larreur

https://ebookbell.com/product/structured-finance-lbos-project-finance-

asset-finance-and-securitization-charleshenri-larreur-23279920

Structured Finance Lbos Project Finance Asset Finance And

Securitization Charleshenri Larreur Larreur

https://ebookbell.com/product/structured-finance-lbos-project-finance-

asset-finance-and-securitization-charleshenri-larreur-larreur-30357396

3.

Structured Finance LbosProject Finance Asset Finance And

Securitization Charleshenri Larreur

https://ebookbell.com/product/structured-finance-lbos-project-finance-

asset-finance-and-securitization-charleshenri-larreur-30357400

The Securitization Markets Handbook Structures And Dynamics Of

Mortgage And Assetbacked Securities Charles A Stone Anne Zissu

https://ebookbell.com/product/the-securitization-markets-handbook-

structures-and-dynamics-of-mortgage-and-assetbacked-securities-

charles-a-stone-anne-zissu-4700956

The Securitization Markets Handbook Structures And Dynamics Of

Mortgage And Assetbacked Securities 2nd Edition 2nd Charles Austin

Stone Phd

https://ebookbell.com/product/the-securitization-markets-handbook-

structures-and-dynamics-of-mortgage-and-assetbacked-securities-2nd-

edition-2nd-charles-austin-stone-phd-45037546

The Mechanics Of Securitization A Practical Guide To Structuring And

Closing Assetbacked Security Transactions 1st Edition Moorad Choudhry

https://ebookbell.com/product/the-mechanics-of-securitization-a-

practical-guide-to-structuring-and-closing-assetbacked-security-

transactions-1st-edition-moorad-choudhry-4682424

Asset Allocation From Theory To Practice And Beyond Wiley Finance 1st

Edition Mark P Kritzman

https://ebookbell.com/product/asset-allocation-from-theory-to-

practice-and-beyond-wiley-finance-1st-edition-mark-p-kritzman-46538470

Copyright # 2011John Wiley & Sons (Asia) Pte. Ltd.

Published in 2011 by John Wiley & Sons (Asia) Pte. Ltd.

2 Clementi Loop, #02–01, Singapore 129809

All rights reserved.

No part of this publication may be reproduced, stored in a retrieval system, or transmitted in

any form or by any means, electronic, mechanical, photocopying, recording, scanning, or

otherwise, except as expressly permitted by law, without either the prior written permission of

the Publisher, or authorization through payment of the appropriate photocopy fee to the

Copyright Clearance Center. Requests for permission should be addressed to the Publisher,

John Wiley & Sons (Asia) Pte. Ltd., 2 Clementi Loop, #02–01, Singapore 129809,

tel: 65–6463–2400, fax: 65–6463–4605, e-mail: enquiry@wiley.com.

This publication is designed to provide accurate and authoritative information in regard to the

subject matter covered. It is sold with the understanding that the publisher is not engaged in

rendering professional services. If professional advice or other expert assistance is required, the

services of a competent professional person should be sought.

Neither the authors nor the publisher are liable for any actions prompted or caused by the

information presented in this book. Any views expressed herein are those of the authors and do

not represent the views of the organizations they work for.

Other Wiley Editorial Offices

John Wiley & Sons, 111 River Street, Hoboken, NJ 07030, USA

John Wiley & Sons, The Atrium, Southern Gate, Chichester, West Sussex, P019 8SQ,

United Kingdom

John Wiley & Sons (Canada) Ltd., 5353 Dundas Street West, Suite 400, Toronto, Ontario,

M9B 6HB, Canada

John Wiley & Sons Australia Ltd., 42 McDougall Street, Milton, Queensland 4064, Australia

Wiley-VCH, Boschstrasse 12, D-69469 Weinheim, Germany

Library of Congress Cataloging-in-Publication Data

ISBN 978–0–470–82603–4 (Hard cover)

ISBN 978–0–470–82898–4 (e-PDF)

ISBN 978–0–470–82897–7 (e-Mobi)

ISBN 978–0–470–82899–1 (e-Pub)

Typeset in 10/12pt, Sabon by Thomson Digital, India

Printed in Singapore by Toppan Security Printing Pte. Ltd.

10 9 8 7 6 5 4 3 2 1

8.

Contents

Preface xiii

Introduction xv

PARTONE

Basics of Asset Securitization 1

CHAPTER 1

Asset Securitization: Concept and Market Development 3

Basic Concept of Asset Securitization 3

Special Purpose Entity 5

Asset Sale versus Debt Financing 5

The Requirement of Servicing 7

Credit of the Underlying Assets 8

Need for Credit Enhancement 9

Development of the Asset Securitization Market in the

United States 10

CHAPTER 2

Originators and Investors of the Asset Securitization Market 19

Efficient Financing for Originators with Asset Securitization 19

Satisfying Varying Investor Demands with Asset Securitization 24

Cultivating Investors: Matching Products with Investment

Demands 25

The Importance of Understanding the Underlying Assets 25

Three Types of Investors 26

Yield-Oriented Investors 26

Credit-Oriented Investors 27

Maturity-Oriented Investors 27

v

9.

CHAPTER 3

Intermediary Participantsof the Asset Securitization Market 29

Attorneys 29

Accountants 31

Guarantors and Credit Enhancers 31

Self-Insurance 32

Bond Insurance 32

Corporate Parent Guarantee 32

Letter of Credit 33

GSE Credit Guarantee 33

Credit Rating Agencies 33

Investment Bankers 35

CHAPTER 4

Necessary Ingredients and Benefits of Asset Securitization 39

The Nine Necessary Ingredients 39

Sound Loan Origination Process 40

Complementary Legal Framework 40

High Integrity of Cash-Flow Analysis 40

Clearly Defined Accounting Rules 41

Prudent Risk Evaluation 42

Full-Fledged Investment Banking Services 42

Mature Government Debt Market 42

Active Secondary Market 43

Broad Investor Base 44

Benefits of Asset Securitization 45

Improvement in the Financial Operation for the Originator 45

Provision of Diversified Investment Products 45

Lowering the Borrowing Cost 46

PART TWO

Residential Mortgages and Securitization of Residential Mortgages 49

CHAPTER 5

Residential Mortgages 51

Description of a Residential Mortgage 51

Characteristics of a Fixed-Rate Mortgage 52

Amortizing a Mortgage 53

vi CONTENTS

10.

Comparison of TwoMortgages with Different Mortgage Rates 54

Alternative Mortgages 57

Adjustable-Rate Mortgages (ARMs) 57

Fifteen-Year Fixed-Rate Mortgages 60

Graduated-Payment Mortgages (GPMs) 61

Biweekly Mortgages 62

Balloon Mortgages 63

Second Mortgages 63

Home Equity Loans (Subprime Mortgages) 63

Hybrid Mortgages 64

Reverse Annuity Mortgages 65

CHAPTER 6

The Residential Mortgage Market 67

The Origination of a Residential Mortgage 67

Housing and Debt Ratios 68

Credit History 69

Property Appraisal 69

Down Payment 70

Mortgage Originators 71

Mortgage Servicers 72

Mortgage Insurers 72

FHA Mortgage Insurance 73

VA Loan Guarantee 73

Private Mortgage Insurance 73

The Development of the Residential Mortgage Market 74

CHAPTER 7

Residential Mortgage Pass-Through Securities 79

Mortgage Pass-Throughs 79

Ginnie Mae Mortgage Pass-Throughs 79

Concept and Terminology 82

Freddie Mac Participation Certificates 87

Fannie Mae Mortgage-Backed Securities 89

Private-Label Pass-Throughs 91

Subprime Mortgage-Backed Securities 92

Trading and Relative Value of Pass-Throughs 92

TBA Trade 93

Forward Settlement 93

Contents vii

11.

Specified Trades 93

Bid–OfferPrice Spreads 94

Benchmark Current-Coupon Yield Spreads 95

CHAPTER 8

Multiclass Mortgage Pass-Throughs 99

Prepayment of Mortgage Pass-Throughs 99

The Need for Multiclass Securities 100

Collateralized Mortgage Obligations 102

The Concept of Average Life 102

Real Estate Mortgage Investment Conduits 103

Issuance of Agency-Guaranteed Multiclass Securities 104

Variety of REMIC Classes 105

Planned Amortization Classes (PACs) 106

Floaters 106

Interest-Only and Principal-Only Securities (IOs and POs) 107

Z-Bonds 107

The Rise, Collapse, and Recovery of REMICs 108

The Rise of REMICs 108

The Collapse of REMICs 108

The Recovery of REMICs 109

Trading and Relative Value 111

CHAPTER 9

Private-Label Mortgage Pass-Throughs 115

The Growth of the Private-Label Pass-Through Market 115

A Typical Transaction 117

Characteristics of the Underlying Mortgages 119

Low Loan-to-Value Ratios 119

High Credit Quality of Borrowers 120

The Cash-Flow Structure—Mechanism of Credit

Enhancement 120

Senior/Subordinated Cash-Flow Structure 120

Bond Insurance 121

Pool Insurance and Corporate Guarantee 122

Letter of Credit 122

Credit Rating Criteria 122

Performance of Credit Ratings 124

viii CONTENTS

12.

Prepayment Pattern 126

Tradingand Relative Value 126

CHAPTER 10

Subprime Mortgage-Backed Securities 131

Evolution of the Subprime Mortgage Market 132

Features of Home Equity Loans 134

Two Types of HELs 134

Underwriting Criteria—Three Ratios 135

Credit Quality of Borrowers 136

Delinquencies and Defaults 136

Varying Characteristics of Pools of Subprime Mortgages 137

Examples of Transactions 142

An Early-Year Transaction: RASC 2003-KS4 143

Mixed Pools of Fixed- and Adjustable-Rate Mortgages 143

Mechanism of Credit Enhancement 143

Bond Insurance to Enhance Credit 145

Maturity Tranching to Capture Pricing Efficiency 145

A Later-Year Transaction: ABFC 2007-WMC1 146

Unique Prepayment Pattern 149

Performance of Credit Ratings 149

Trading and Relative Value 152

PART THREE

Securitization of Commercial Mortgages and Consumer Loans 155

CHAPTER 11

Commercial Mortgage-Backed Securities 157

The Growth of the CMBS Market 157

The Origination of a Commercial Mortgage 159

The Loan-to-Value Ratio 161

The Debt Service Coverage Ratio 161

Defaults and Losses of Commercial Mortgages 161

A Typical Transaction 164

Characteristics of Underlying Mortgages 165

Re-Underwriting Mortgages for Credit Ratings 167

Credit and Maturity Tranching 169

Contents ix

13.

Performance of CreditRatings 170

Trading and Relative Value 171

CHAPTER 12

Asset-Backed Securities 175

The Growth of the ABS Market 175

Credit Card ABS 176

Pattern of Cash Flow of the Underlying Collateral 176

Three Types of Issuers 177

Transaction Parameters 177

Investor Interest and Seller Interest 177

Revolving Period and Accumulation or Amortization Period 179

Portfolio Yield, Delinquency Rate, and Loss Rate 179

Payment Rate and Purchase Rate 180

Certificate Rate and Servicing Fee 180

Excess Spread 180

A Typical Transaction 181

Underlying Collateral 181

Credit Enhancement 182

Stress Test for Credit Ratings 183

Auto Loan ABS 184

Pattern of Cash Flow of the Underlying Collateral 184

Major Types of Issuers and Underlying Assets 184

A Typical Transaction 185

Cash Flow and Credit Enhancement 186

Prepayment 187

Performance of Credit Ratings 188

Trading and Relative Value 189

CHAPTER 13

Collateralized Debt Obligations 193

Basic Concept and Market Development of CDOs 194

CDOs Are Not Mutual Funds 195

Different Structural Types of CDOs 196

Cash Flow CDOs 196

Synthetic CDOs 197

Market Value CDOs and Hybrid CDOs 198

Motivations for Issuing CDOs 199

Arbitrage 199

x CONTENTS

14.

Capital Relief 199

RiskManagement 200

Facilitating the Growth of the Asset Securitization Market 200

Incentives for Investing in CDOs 200

Structuring and Credit Rating CDOs 201

A Simulation Model to Structure CDOs 203

Trading and Relative Value 205

PART FOUR

The Current Asset Securitization Market in the United States

and Asia-Pacific 209

CHAPTER 14

The Collapse and Recovery Prospects of the Asset Securitization Market 211

How the Market Collapsed 212

Sloppy Origination of the Underlying Assets 212

Overly Zealous Investment Banking 213

Complacent Credit Ratings 214

Irresponsible Investing Behavior 215

Prospects for Recovery 215

Underlying Asset Originators: Back to Basics 216

Investment Bankers: Reduce Leverage and Look

Out for Investors 217

Credit Rating Agencies: Strengthening Rating Criteria through

Research 217

Investors: Know What You Are Buying 218

CHAPTER 15

Asset Securitization in Asia-Pacific 221

Asset Securitization in Japan 221

Market Growth with Variety of Underlying Assets 221

Complementary Factors in Strong Growth 223

Asset Securitization in Australia 224

Rapid Growth with Focused Underlying Assets 224

Tapping the World Financial Markets for Funds 225

The Strong Base for the Australian RMBS 226

Different Patterns of Asset Securitization in Japan and Australia 226

Asset Securitization in Taiwan 226

Asset Securitization in China 229

Contents xi

15.

APPENDIX A

Analysis ofPrepayment and Prepayment Rate 233

Measurement of Prepayment Rate 233

Single Month Mortality (SMM) 233

Constant Prepayment Rate (CPR) 234

Public Securities Association Standard (PSA) 235

Two Fundamental Reasons for Prepayment 236

Refinancing 236

Housing Turnover 237

Home Sale 237

Default 238

Disaster 238

Death 238

APPENDIX B

Housing Price Appreciation and Mortgage Credit Performance 239

The Importance of Housing Price Appreciation 239

The National Experience 239

The California Experience 241

Credit Performance of Mortgages 241

Delinquencies and Defaults 241

The Standard Default Assumption 242

APPENDIX C

Fundamental Elements in Credit Ratings 245

Evaluating Credit Quality of the Underlying Assets 245

Reviewing Payment Structure and Cash-Flow Mechanics 247

Analyzing Legal and Regulatory Risks 247

Assessing Operational and Administrative Risks 248

Examining Third-Party Dependencies 248

APPENDIX D

The Collapse of the Asset Securitization Market 251

Index 255

xii CONTENTS

16.

Preface

This book, AssetSecuritization: Theory and Practice, is based on my

30 years of observations and work experience in the U.S. asset securitiza-

tion market. It is a celebration of this efficient financing method that has,

over the last four decades, benefited lenders, borrowers, and investors alike.

As a capstone for a career spent in some of the major investment banking

firms and a leading credit rating agency, this book is also written with an

unavoidable tinge of sadness. Powerhouses such as Salomon Brothers,

Bear Stearns, and Lehman Brothers, and venerable investment firms like

E. F. Hutton—places I admired or worked and honed my analytical skills

at as a young man—have been swept away by the change of times or mis-

management. And the asset securitization market was almost destroyed by

greed, abuse, and complacency. As a market practitioner who believes in

the power of asset securitization, and contributed in a small way to its suc-

cess, the events of the last three years have been painful to witness. How-

ever, ever the optimist, I am hopeful that the market will storm back bigger,

better, and stronger, to once again provide financing to consumers and busi-

nesses, creating wealth for our society.

This book could not have been published without the help of many of

my colleagues and friends. I would like to thank Rocco Sta. Maria, Head of

Sales and Client Services for Standard & Poor’s in Asia-Pacific, for putting

me in touch with John Wiley & Sons. I am grateful for the assistance

extended to me by my colleagues at Standard & Poor’s offices in Tokyo

(Yu-Tsung Chang), Melbourne (Vera Chaplin), Beijing (Li Jian), Hong

Kong (Frank Lu), and Taipei (Aaron Lai), who provided insights into the

development of the Japanese, Australian, Chinese, and Taiwanese asset

securitization markets. I would also like to express my gratitude to K. C.

Yu, Deputy CEO of SinoPac Holdings and Nick Ding of Standard & Poor’s

Beijing office, for providing me access to up-to-date market information.

Over the years, the excellent market commentaries of Citigroup Global

Markets, J. P. Morgan Securities, Merrill Lynch, Morgan Stanley, and UBS

Securities kept me abreast of the asset securitization market. I would also

like to thank many of my friends who helped me clarify and improve the

content of this book. Additionally, I greatly appreciate the assistance of

xiii

17.

Nick Melchior, SeniorPublishing Editor, John Wiley & Sons, without

whose encouragement and enthusiasm this book would not have been com-

pleted so expeditiously. Though I am solely responsible for the content

of this book, the skills and professionalism of my copy editor, Michael

Hanrahan, made the text eminently more readable. Finally, I wish to thank

my wife, Linda, and my children, Justin and Brian. Their love and support

made the writing of this book and, in fact, my whole professional journey

all the more rewarding and enjoyable.

Joseph Hu

November 2010

xiv PREFACE

18.

Introduction

In A Taleof Two Cities, Charles Dickens described the chaotic and brutal

period of the French Revolution as the best of times and the worst of

times. For the asset securitization market, one might similarly regard the

period after the subprime mortgage debacle that caused panic and tremen-

dous financial loss worldwide as the worst of times—the winter of hindsight

and reflection. Yet this period can also be viewed as the spring of hope and

rebirth, and as the best time to study the concept and practice of asset secu-

ritization, to once again make it a powerful financial engine that creates

wealth and prosperity.

Over the last 40 years, the asset securitization market has grown and

flourished to become the largest sector of the U.S. fixed-income securities

market. In the initial development of the asset securitization market in

1970, residential mortgages were the only type of securitized assets. Re-

markably, however, since the mid-1980s, many other types of financial

assets with a predictable future receivable cash flow began to be utilized as

the underlying asset for the issuance of asset-backed securities. These assets

include, but are not limited to, commercial mortgages, credit card receiv-

ables, auto loans, student loans, equipment leases, and small business loans.

By facilitating the funding of consumption and business activities, asset

securitization has contributed substantially to the steady growth of the U.S.

economy and the increase in the American standard of living. Asset securiti-

zation has been the living proof of the adage, ‘‘finance creates value.’’

Alas, asset securitization became the victim of its own success. With

the abundance of funds available to be invested, market participants

became overly creative with the underlying assets of their originations and

created a variety of new asset-backed securities. Throwing caution to the

wind, originations of residential mortgages—the securitization market’s

most prominent and best performing underlying assets—began to grossly

deviate from prudent underwriting guidelines. Driven by greed, more and

more of the low-credit-quality (subprime) mortgages were originated

and their inherent credit risks were consistently underestimated. When

incidences of delinquencies and defaults of these mortgages became abnor-

mally frequent, investors were alarmed and began to shy away from

xv

19.

subprime mortgage-backed securities.Like dominos, fear and panic quickly

spread to the mortgage-backed securities market and eventually put a stran-

gle hold on other sectors of the capital market as well.

A credit risk problem created a liquidity problem so severe that funding

became unavailable to consumption and business activities. Since late 2007,

the U.S. economy has experienced the worst contraction both in depth and

duration since the Great Depression. The rest of the world has been sim-

ilarly impacted with their economies languishing in a severe downturn. In

the initial panic, ‘‘asset securitization’’ became one of the most vilified and

demonized financial terms in the world. Critics questioned the justification

of such a market and there were doubts aplenty about whether the asset

securitization market would ever recover. It would seem that this is indeed

the worst time for asset securitization. Yet, the bottom of the market is the

perfect place and time to examine asset securitization anew—its successes

and failures—and plan for a future asset securitization market that is trans-

parent, self-disciplined, and rigorous in its regulation and supervision.

This book is intended for students and entry-level market professionals

alike who are interested in learning about asset securitization—its con-

cepts and practices. It is designed so that the readers will come away with a

fundamental but comprehensive understanding of the asset securitization

market. As such, the book aims to provide a review of the market’s develop-

ment, necessary framework, potential benefits, and detailed descriptions of

major asset securitization products.

Part 1 of the book, which consists of four chapters, will discuss the fun-

damental concepts, the funding efficiency, the market participants, and the

potential benefits of asset securitization. An analysis of mortgage finance

will be provided in Part 2, which consists of six chapters. They cover a vari-

ety of topics from the description of many different types of residential mort-

gages to the securitization of these mortgages, including the now infamous

subprime mortgages. Also included are important topics, such as prepay-

ments, cash-flow structure, maturity and credit tranching, and the trading

and relative value of the various mortgage-backed securities. The three chap-

ters in Part 3 will explain the other major asset securitization products, such

as commercial mortgage-backed securities, credit card receivable-backed

securities, auto loan-backed securities, and collateralized bond obligations.

Part 4 has two chapters: one reviews the collapse and the potential recovery

of the asset securitization market, and the other describes the asset securitiza-

tion efforts in Japan, Australia, Taiwan, and China.

Extensive tables and charts are presented to help illustrate a concept or

describe a product. Neither analytical discussions nor investment strategies

of the various asset-backed securities are included as they are not the focus

of this book.

xvi INTRODUCTION

20.

It is hopedthat, after reading this book, students of asset securitization

will gain new insight into and appreciation for the creative financial instru-

ments that make up this market. And be mindful of the critical lesson

learned that not all good things need come to an end, if prudence is always

the guiding principle of our behavior in the financial market.

Introduction xvii

Issuers of asset-backedsecurities are mostly originators of the assets

backing the securities. These assets can be a wide variety of residential or

commercial mortgages, consumer loans, commercial leases, or any financial

instruments that have predictable and stable receivable cash flows. In recent

years, there have been new and popular asset-backed securities that are sup-

ported by assets that are corporate bonds, commercial and industrial loans,

or even asset-backed securities themselves.

Since asset-backed securities are issued by lenders through the mechanism

of structuring future receivable cash flows of the underlying assets to finance

their funding needs, the securities are also called structured finance securities.

From an accounting point of view, the issuance of asset-backed securities is

considered an asset sale. This differs from the issuance of bonds, which is debt

financing by corporations, the various levels of government, or authorities.

Specifically, by issuing an asset-backed security to raise funds to finance

the origination of loans, the financing has the following five salient features:

& The asset-backed security is issued through a special purpose entity.

& The accounting treatment of issuing an asset-backed security is asset

sale rather than debt financing.

& An asset-backed security requires the servicing of the underlying assets

for the investor.

& The credit of the asset-backed security is derived primarily from the

credit of the underlying assets (the collateral).

& There is invariably a need of credit enhancement for the asset-backed

security.

At the outset, it is critical that several basic terms of asset securitization

are clarified to avoid possible confusion in future discussions. Throughout

this book, the presentation and the analysis, unless specifically noted, are

from the viewpoint of the lender, who is a loan originator. The originator

is the one who originates the loans that are pooled as the underlying assets

for the issuance of asset-backed securities in the asset securitization transac-

tion. Therefore, the term originator is synonymous with the term lender.

The two terms are used in the book interchangeably. Further, since asset

securitization is primarily enabling those originators to use their newly orig-

inated or existing loans to obtain funds, the loans are really their assets

(although from the point of view of the borrowers, they are debts). Thus,

the terms loans and assets in the context of structured finance are also syn-

onymous. They are interchangeable terms. The issuer of asset-backed secu-

rities is mostly an entity that is set up by the originator of the underlying

assets. So, while the originator and the issuer are legally two different enti-

ties, they are economically the same or very closely related business entities.

4 ASSET SECURITIZATION

24.

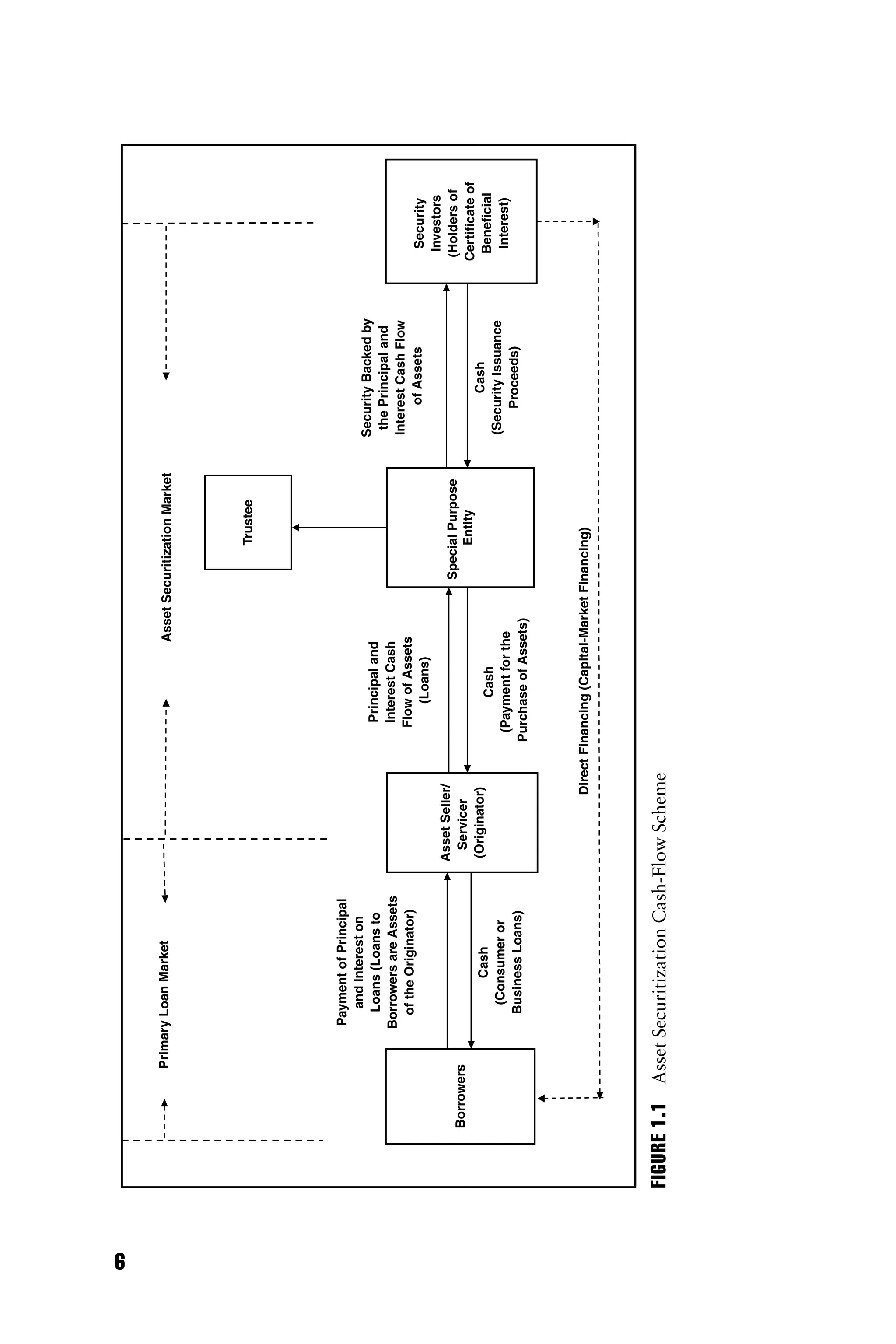

Special Purpose Entity

Aspecial purpose entity (SPE) is a unique feature of asset securitization.3

Alternatively, an SPE is also referred to as a special purpose vehicle (SPV)

or a special purpose trust (SPT). Basically, an SPE is a trust that is set up by

the originator for the purpose of purchasing the loans it originates and

issuing in the capital market a certificate of beneficial interest, for which the

cash flows are backed solely by the cash flow of loans purchased from

the originator (see Figure 1.1). Actually, the purchase of loans and the issu-

ance of the certificate of beneficial interest take place simultaneously. They

are two parts of a transaction. The SPE, on the one hand, raises the funds in

the capital market by issuing the asset-backed security; and on the other

hand, it uses the very issuance proceeds to pay for the purchase of the

underlying assets. The holder of the certificate of beneficial interest is gener-

ically called the investor of the asset-backed security.

From a balance-sheet point of view, the SPE has no assets other than

those purchased from the originator, and no liabilities other than those of

the asset-backed security it issues. With this special and strict asset–liability

structure, the cash flows of the assets are matched by those of the liabilities.

From the accounting and legal points of view, the SPE is considered

bankruptcy-remote. Asset securitization is also called structured finance,

because it is done through a special legal structure of the SPE and the inter-

est and principal payment of the security it issues is through the structuring

of the projected future receivable cash flows from the underlying assets.

Structured finance is a formal and generic term for asset securitization. The

term structured finance is often used to differentiate from corporate finance.

Colloquially, however, the term asset securitization is more often used to

describe precisely the process of pooling assets for the issuance of an asset-

backed security. To further simplify the description of asset securitization, it

sometimes is just called securitization.

Asset Sale versus Debt Financing

One great advantage of asset securitization is that it is an effective way of

managing the balance sheet by the originator through the selling of its

newly originated or existing loans to raise funds. This way of financing ena-

bles the originator to collect the present value, at the prevailing market

price, of the stream of the future receivable cash flows of their assets. Asset

securitization, therefore, is not a debt financing and the funding has no con-

sequence of expanding the issuer’s balance sheet. Further, by selling assets,

the originator does not rely on attracting deposits or borrowing from other

financial institutions to fund the origination of the assets, both of which will

Asset Securitization: Concept and Market Development 5

expand the liabilityside of the balance sheet. Actually, it can be said that

when a lender raises funds through asset securitization, the financing could

even have the effect of shrinking the lender’s balance sheet if it elects to use

the issuance proceeds to pay down liabilities (this being the case when the

lender sells existing loans on its portfolio). By contrast, a lender raising

funds through deposits, borrowing, issuing debt or equity securities to fund

the origination of loans would have the consequence of expanding its bal-

ance sheet.

The Requirement of Servicing

The function of servicing is unique for asset-backed securities because the

sole source of the interest and principal payments of the securities is sup-

ported entirely by the future cash flows of the underlying assets. The servic-

ing function is performed by a servicer, who often is the originator and also

the seller who sells the very assets to the SPE. Primarily, the servicer per-

forms the servicing function by collecting the interest and principal cash

flows generated from the underlying assets and then passing them, through

the SPE, to the investor (holder of certificate of beneficial interest). Other

important elements of the servicing function include working with delin-

quent borrowers, disposing of defaulted assets, and providing timely and

accurate cash-flow reports to investors.

In the early days of the legal structure of the SPE, which was a grantor

trust, the servicing function was passive in that the servicer was required not

to touch the cash flow generated from the underlying assets other than just

passing them on to the investor. This requirement was made necessary so

that the Internal Revenue Service would see through the SPE, not levying an

income tax at the SPE level on the interest cash flow generated from the

underlying assets. The income tax liability will fall on the investor, who is

the ultimate owner of the assets underlying the asset-backed securities. It

stands to reason that if the tax on interest income to the SPE were to be

levied while the interest income to the investor is also taxed, there would be

income taxes on two levels of the transaction. This double taxation would

completely nullify the economic benefits intended for securitization.

Under this passive management requirement, all the servicer was re-

quired to do was simply pass the cash flows onto the investor. The servicer

could not manage the cash flows to earn incremental yield for the trust by

reinvesting the interim cash flow (the cash flow the SPE owns temporarily

between the time it was collected by the servicer and the time it was distrib-

uted to the certificate holder). Nor was the servicer permitted to allocate the

principal cash flow of the underlying assets to satisfy the varying maturity

preferences of the different types of investors. Later on, new legislation

Asset Securitization: Concept and Market Development 7

27.

permitted active managementof the cash flow of the underlying assets. It

allowed the servicer to allocate the cash flow, without encountering tax

consequences, by prioritizing the principal payment of the underlying assets

to investors according to maturity and credit-risk preferences. Also, the

servicer was allowed to manage the interim cash flow to enhance the income

of the trust by purchasing short-term money market instruments with the

interim cash flow.

As will be explained in later chapters, the ability of the servicer to allo-

cate cash flows is critically important in the development of new types of

asset-backed securities. It allowed the innovative creation of maturity

tranching and credit tranching of the cash flows of the underlying assets.

Issuers were allowed to issue asset securitization securities in various matu-

rity classes and credit-risk classes.

In comparison with asset-backed securities, corporate or government

bonds do not need servicers. This is because the interest and principal pay-

ment of these obligations are paid out of the issuers’ earnings or tax reve-

nues. The cash flows of the liabilities are not matched by the cash flows of

any of their assets.

Credit of the Underlying Assets

Since the interest and principal cash flow of an asset-backed security come

solely from its underlying assets, the credit risk of the security is derived

primarily from the credit risk of the underlying assets. (As will be explained

in later chapters, the credit risk, or simply the credit, of a borrowing entity

or a debt instrument refers to the likelihood of the borrower defaulting on

its debt. The likelihood of default is assessed publicly by credit rating agen-

cies. According to credit rating agencies, the incidence of default is defined

as the borrower failing to make timely payment of interest and/or the repay-

ment of principal of the debt. A high credit rating, or a strong credit, would

mean a low probability of default. Conversely, a low credit rating, or a

weak credit, suggests a high probability of default.) More important, the

credit of the assets is highly dependent on economic conditions. In a pros-

perous economy, the underlying assets would perform strongly with less fre-

quent incidences of default. In a depressed economy, however, the

underlying asset would have a weak credit performance and the incidences

of default would become more frequent.

This feature contrasts sharply with the credit determinant of a debt ob-

ligation of a corporation or a government entity. The credit strength of a

corporate debt is first and foremost dependent on the management of the

corporation. A well-managed corporation is likely to have a stronger credit

because it is more likely to be financially healthy with a greater earning

8 ASSET SECURITIZATION

28.

potential. This wouldenable the corporation to service its debt in various

economic environments. Conversely, the credit of a poorly managed corpo-

ration is likely to be weaker. With the exception of the U.S. government,

whose debts are risk free, the credit of a state or local government is also

dependent on its ability to manage various expenditures in relation to tax

revenues under all economic conditions.

Need for Credit Enhancement

Credit risk of a security is an important investment consideration for inves-

tors. In order for an asset-backed security to attract certain investors, it has

to have a desirable credit rating. If the underlying assets cannot provide the

security with a desirable credit rating, then the security would require credit

enhancement as defined by the credit rating agencies. In this case, four ma-

jor sources of credit enhancement are available to strengthen the credit of

an asset-backed security. They are: (1) self-insurance, (2) corporate-parent

credit guarantee, (3) surety bond, and (4) letter of credit (detailed analysis

of credit enhancement will be provided in various later chapters when the

cash-flow structure of products is explained).

Credit enhancement through self-insurance can be in the form of senior/

subordination, over-collateralization, or interest spread. In senior/subordi-

nation, the cash flow of an asset-backed security is subdivided into two

classes: senior and subordinated classes. The principal cash flow of the sub-

ordinated class is structured to support (enhance) the credit of the principal

of the senior class. Under the senior/subordination structure, the investor of

the senior class of the security will be repaid before the investor of the sub-

ordinated class.

One simple example may be appropriate to explain the senior/subordi-

nate cash-flow credit enhancement. Consider a pool of assets that is

expected to experience a lifetime cumulative default rate (default frequency)

of 30 percent. After the default, the underlying assets may be liquidated to

recover 60 percent of the original loan amount. That is, the loss on the

defaulted assets is 40 percent (loss severity). For the life of the pool, the

cumulative loss therefore would be the product of default frequency and

loss severity; that is, 12 percent (30% 40% ¼ 12%). Based on these cash-

flow assumptions, it is possible to structure a senior/subordinate credit

enhancement with the senior class security being supported by the 88 per-

cent (1 – 12%) of the pool’s cash flow and the subordinate (junior) class

being supported by the first loss of 12 percent of the pool’s cash flow.

In an over-collateralization structure, the principal amount of the

underlying assets is greater than the principal amount of the asset-backed

security so that more principal protection can be provided by the excess

Asset Securitization: Concept and Market Development 9

29.

principal. For example,the underlying principal cash flow can be 110 percent

of that of the security. Thus, the additional 10 percent of over-collateralization

is behaving like a subordinate class that supports the principal of the senior

class. In addition to the principal, the interest can also be used in credit

enhancement. This is under the structure where the interest on the asset-

backed securities is set to be significantly less than that of the underlying

assets and the excess spread is used to support the credit of the asset-

backed securities. All these are viewed as self-insurance because the princi-

pal and/or the interest of the underlying assets are the sources of credit

enhancement.

Sometimes, it may be more economical to issue an asset-backed security

with the corporate-parent of the issuer providing the credit enhancement.

In this case, the credit strength of the security is equivalent to that of the

corporate parent. An alternative to a corporate-parent guarantee can be a

credit guarantee provided by a bond insurance company in the form of

surety bond. The bond insurance companies often have a very strong credit

so that the bond-insured structured security would also be highly rated. The

fourth alternative is credit enhancement via letter of credit from a commer-

cial bank with a strong credit. In this case, the credit of the asset-backed

security is the same as the credit of the commercial bank.

DEVELOPMENT OF THE ASSET SECURITIZATION

MARKET IN THE UNITED STATES

Asset securitization began in the United States in 1970, when residential mort-

gages were securitized by mortgage bankers with the issuance of mortgage-

backed securities. Over the last 40 years (1970 to 2009), more than $23 trillion

worth of principal amount of asset-backed securities has been issued with a

wide variety of underlying assets, ranging from residential mortgages to air-

plane leases to corporate bonds. As of year-end 2009, outstanding principal of

asset-backed securities approached $11 trillion.

Three major factors contributed to the rapid growth of the asset securi-

tization market. First, during the thrift crisis of the 1980s asset securitiza-

tion enabled thrifts to convert their holdings of residential and commercial

mortgages to mortgage-backed securities. It greatly increased the market-

ability of mortgages and expedited the resolution of failed thrifts. Second,

the coming of home-buying age in the late 1970s of the post–World War II

baby boomers created a strong demand for housing for nearly 20 years.

Securitization of residential mortgages facilitated the funding for the surge

of demographic demand for housing. Third, after the economic slowdown

in the early 1980s, consumption turned robust and persisted almost until

10 ASSET SECURITIZATION

30.

the severe recessionof 2008. Securitization of consumer loans, such as

credit cards and auto loans, provided needed financing for consumers.

This section will present a brief history of the development of the asset

securitization market in the United States. Detailed description of the

evolution of the major securitized products will be provided later in the

relevant chapters.

The earliest type of asset-backed security was Ginnie Maes. Actually,

during the 1970s, Ginnie Maes were not even thought of, in today’s sense,

as asset-backed securities. They were designed by the federal government

simply as a vehicle for mortgage bankers to raise funds in the capital market

to finance their originations of residential mortgages. It was natural that

mortgage bankers were the first originators to practice asset securitization

because they, unlike thrifts and banks, were non-depository lenders in that

they could not attract deposits as a source of funds. They could make loans

only with borrowed money and repay the borrowing after selling the newly

originated loans.

The issuance of Ginnie Maes efficiently facilitated the operation of

mortgage bankers by enabling them to borrow directly from the capital

market. The underlying mortgages backing Ginnie Maes were either in-

sured by the Federal Housing Administration (thus called FHA-insured

mortgages) or guaranteed by the Veterans Administration (now the Depart-

ment of Veterans Affairs, VA-guaranteed mortgages). Ginnie Maes were ac-

tually called mortgage pass-through securities (certificates of beneficial

interest) and the investors of Ginnie Maes owned the pro rata share of inter-

est in the pool of the mortgages backing Ginnie Maes. Because of the gov-

ernment insurance or guarantee, the credit of the underlying mortgages for

Ginnie Maes was enhanced to that of the U.S. government. (Here, the term

credit refers to the probability of the borrowers paying lenders the monthly

mortgage payment of interest and principal on time.) To further ensure the

acceptability of the pass-through securities among investors, the credit of

the securities was further enhanced by the guarantee of the Government

National Mortgage Association (GNMA, nowadays called Ginnie Mae).

The credit of GNMA in turn was backed by the full faith and credit of the

U.S. government. (Here, the credit refers to the probability of the issuer of

the pass-through security paying investors the monthly payment of interest

and principal on time.) In a sense, it can be said the Ginnie Maes are the

safest security because they carry a double credit guarantee from the U.S.

government.

In the early 1970s, there was another type of mortgage pass-through

security being issued in the marketplace. It was a participation certificate

called FHLMC PC (also a type of certificate of beneficial interest). This cer-

tificate was issued and guaranteed by the Federal Home Loan Mortgage

Asset Securitization: Concept and Market Development 11

31.

Corporation (FHLMC), nowa government-sponsored enterprise (GSE)

with a new official name of Freddie Mac.4

The reason this type of mortgage

pass-through was called a participation certificate was that the originator

who sold the mortgages to FHLMC was required to retain a 5 percent par-

ticipating interest in the pool of mortgages sold. One reason for the partici-

pating interest was to ensure that the originator, by retaining an interest and

therefore having a stake in the mortgage pool, would have a strong incen-

tive to maintain high underwriting standards of the mortgages. To differen-

tiate from Ginnie Maes, the underlying mortgages for FHLMC PCs were

conventional mortgages, meaning that they were not insured by FHA nor

guaranteed by VA. Generically, all mortgage pass-throughs are now termed

residential mortgage-backed securities (RMBS).

During the decade of the 1970s, the combined issuance volume of Gin-

nie Maes and FHLMC PCs was small; it never exceeded $30 billion annu-

ally. The pace of securitizing mortgages, however, accelerated dramatically

from 1981, when Freddie Mac and the Federal National Mortgage Associa-

tion (FNMA), another GSE now called Fannie Mae, became the guarantor

of RMBS. The sudden issuance surge of RMBS in the early 1980s was to

assist the thrifts that were in dire financial conditions to manage their bal-

ance sheets and improve earnings. The most critical financial problem of the

thrifts was their greatly mismatched assets and liabilities. They were hold-

ing long-term assets of mortgages (which were of mostly 30-year maturity)

with short-term liabilities of time deposits (which were of short maturities,

ranging from just a few months to mostly less than five years). In the early

1980s when interest rates were at a historical high with short-term interest

rates hovering significantly above long-term rates, thrifts were having great

difficulties rolling over their short-term debts. Worse, with the yields of

long-term asset substantially below those of market short-term rates, thrifts

were running huge negative cash flows, greatly depleting their capital

position.

The two GSEs initiated mortgage swap programs to facilitate the thrifts

to securitize their holdings of long-term residential mortgages. Through

the swap programs, the thrifts would sell their residential mortgages to the

GSEs and in return receive certificates of beneficial interest backed by

the very mortgages they sold. By doing the swap, thrifts would now own

more marketable and liquid RMBS rather than the illiquid residential mort-

gages. This would enable thrifts to more easily and quickly sell their RMBS

and pare down liabilities. The mortgage swap programs were also timely to

facilitate the financing for the demand for housing that was greatly strength-

ened in the late 1970s due to the coming of home-buying age of the post–

World War II baby boomers. This demand was temporarily suppressed by

the financial difficulties at thrifts and the historically high interest rates.

12 ASSET SECURITIZATION

32.

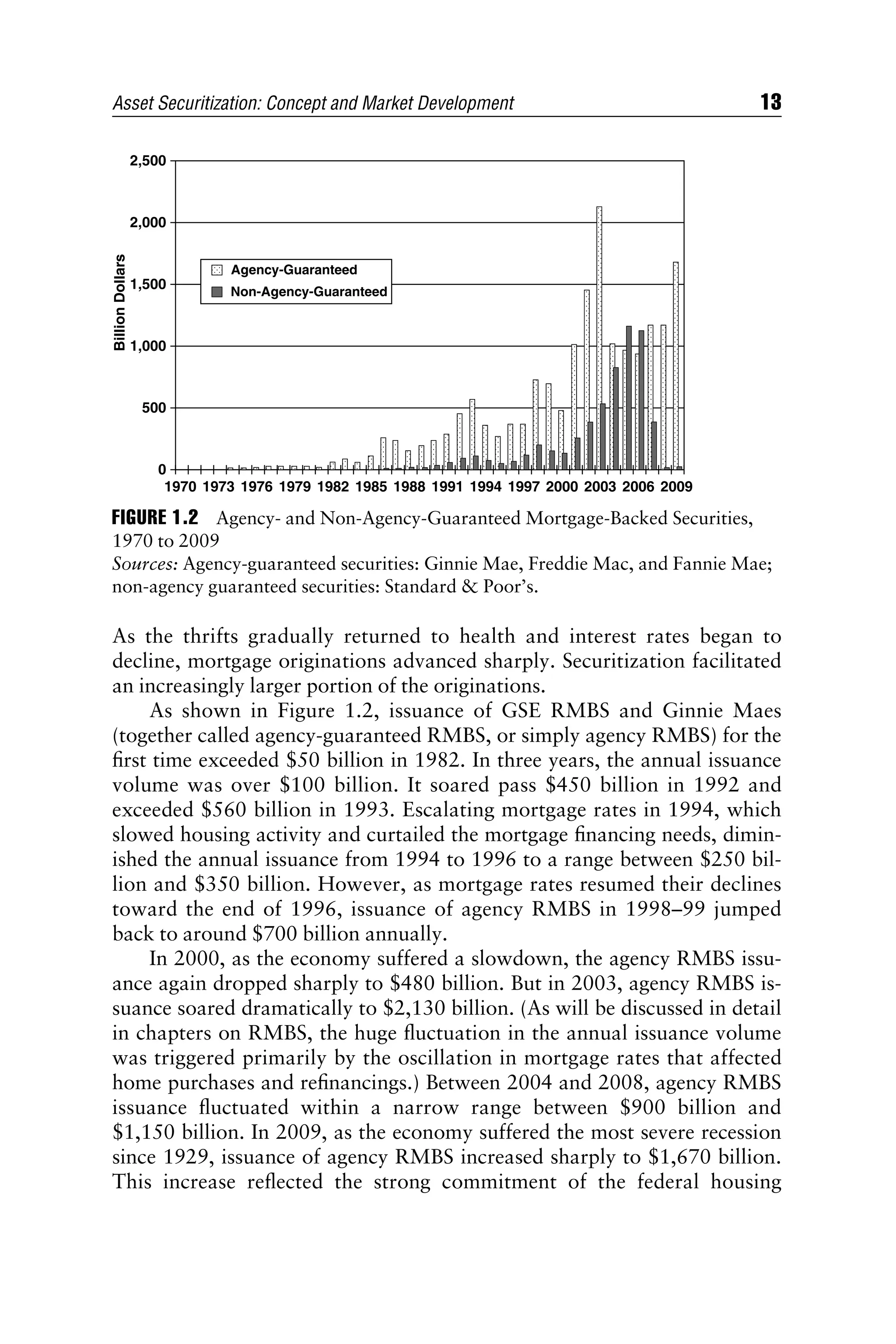

As the thriftsgradually returned to health and interest rates began to

decline, mortgage originations advanced sharply. Securitization facilitated

an increasingly larger portion of the originations.

As shown in Figure 1.2, issuance of GSE RMBS and Ginnie Maes

(together called agency-guaranteed RMBS, or simply agency RMBS) for the

first time exceeded $50 billion in 1982. In three years, the annual issuance

volume was over $100 billion. It soared pass $450 billion in 1992 and

exceeded $560 billion in 1993. Escalating mortgage rates in 1994, which

slowed housing activity and curtailed the mortgage financing needs, dimin-

ished the annual issuance from 1994 to 1996 to a range between $250 bil-

lion and $350 billion. However, as mortgage rates resumed their declines

toward the end of 1996, issuance of agency RMBS in 1998–99 jumped

back to around $700 billion annually.

In 2000, as the economy suffered a slowdown, the agency RMBS issu-

ance again dropped sharply to $480 billion. But in 2003, agency RMBS is-

suance soared dramatically to $2,130 billion. (As will be discussed in detail

in chapters on RMBS, the huge fluctuation in the annual issuance volume

was triggered primarily by the oscillation in mortgage rates that affected

home purchases and refinancings.) Between 2004 and 2008, agency RMBS

issuance fluctuated within a narrow range between $900 billion and

$1,150 billion. In 2009, as the economy suffered the most severe recession

since 1929, issuance of agency RMBS increased sharply to $1,670 billion.

This increase reflected the strong commitment of the federal housing

2,500

2,000

1,500

1,000

Billion

Dollars

500

0

1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009

Non-Agency-Guaranteed

Agency-Guaranteed

FIGURE 1.2 Agency- and Non-Agency-Guaranteed Mortgage-Backed Securities,

1970 to 2009

Sources: Agency-guaranteed securities: Ginnie Mae, Freddie Mac, and Fannie Mae;

non-agency guaranteed securities: Standard Poor’s.

Asset Securitization: Concept and Market Development 13

33.

agencies in supportingthe seriously weakened housing and mortgage fi-

nance markets.

As the agency RMBS grew rapidly over the past 20 years, RMBS issued

without the agency guarantee, called non-agency-guaranteed pass-throughs,

also developed with remarkable speed. In 1977, the first type of non-agency

pass-throughs, called private-label pass-throughs, were issued.5

The market

development in the next 13 years was rather slow, with the new issuance of

private-label pass-throughs between 1977 and 1989 totaling only $50 bil-

lion. Beginning in the 1990s, private-label pass-throughs started to grow

rapidly. By 1993, they registered a new issuance of over $100 billion. Be-

tween 1994 and 1996, due to escalating mortgage rates, private-label issu-

ance nearly halved to between $50 billion and $60 billion. However, it

resumed in 1997 with just under $120 billion offerings.

Beginning in the late 1980s, a new and more aggressive breed of mort-

gage finance began to catch fire in the mortgage securitization market. Bor-

rowers with a less pristine credit history had been granted loans to refinance

or purchase homes. The securitization of these new loans, generically called

subprime mortgages, became an increasingly important part of the non-

agency-guaranteed RMBS, sowing the seeds for the 2008 financial crisis. In

2003, out of the $535 billion new issuance of non-agency-guaranteed pass-

throughs, $215 billion were subprime mortgages. More significant, in 2005

and 2006, when non-agency RMBS issuance totaled around $1,150 billion

annually, over $500 billion belonged to subprime mortgages. As will be dis-

cussed later in more detail, the collapse of the mortgage-backed securities

market in 2008 was triggered by the rampant defaults of subprime mort-

gages, where the non-agency issuance plummeted to just $15 billion. The

non-agency market remained nonexistent in 2009 with the minuscule issu-

ance of under $30 billion.

The success of mortgage-backed securities was copied early on in many

other areas of consumer lending. In that respect, it was the mortgage swap

programs that revolutionized the thinking of asset securitization. No longer

was asset securitization practiced simply as an alternative method of raising

funds for mortgage bankers. It now had an additional, and more important,

benefit of balance-sheet management. Depository lenders, especially banks,

can now perform their intermediary function not just with deposits from

primarily consumers but also with funds from a great variety of institutional

investors in the capital market. More important, by securitizing their origi-

nations of consumer loans, banks can also strategically manage their assets

and liabilities with earnings and capital requirements.

Since the mid-1980s, commercial mortgages have also been pooled for

the issuance of commercial mortgage-backed securities (CMBS). Issuance of

CMBS in 1990 was merely $5 billion (see Figure 1.3). It exceeded

14 ASSET SECURITIZATION

34.

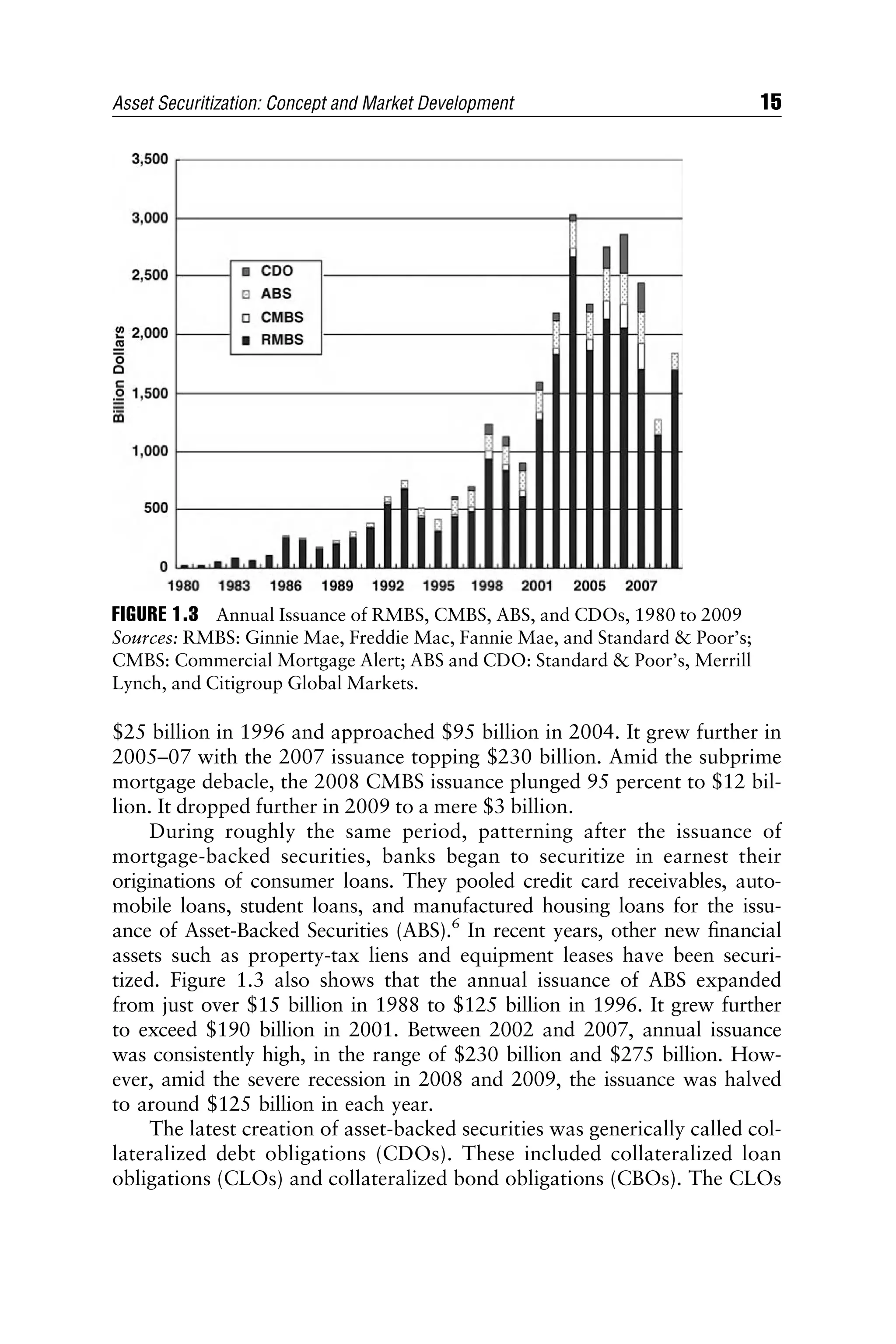

$25 billion in1996 and approached $95 billion in 2004. It grew further in

2005–07 with the 2007 issuance topping $230 billion. Amid the subprime

mortgage debacle, the 2008 CMBS issuance plunged 95 percent to $12 bil-

lion. It dropped further in 2009 to a mere $3 billion.

During roughly the same period, patterning after the issuance of

mortgage-backed securities, banks began to securitize in earnest their

originations of consumer loans. They pooled credit card receivables, auto-

mobile loans, student loans, and manufactured housing loans for the issu-

ance of Asset-Backed Securities (ABS).6

In recent years, other new financial

assets such as property-tax liens and equipment leases have been securi-

tized. Figure 1.3 also shows that the annual issuance of ABS expanded

from just over $15 billion in 1988 to $125 billion in 1996. It grew further

to exceed $190 billion in 2001. Between 2002 and 2007, annual issuance

was consistently high, in the range of $230 billion and $275 billion. How-

ever, amid the severe recession in 2008 and 2009, the issuance was halved

to around $125 billion in each year.

The latest creation of asset-backed securities was generically called col-

lateralized debt obligations (CDOs). These included collateralized loan

obligations (CLOs) and collateralized bond obligations (CBOs). The CLOs

FIGURE 1.3 Annual Issuance of RMBS, CMBS, ABS, and CDOs, 1980 to 2009

Sources: RMBS: Ginnie Mae, Freddie Mac, Fannie Mae, and Standard Poor’s;

CMBS: Commercial Mortgage Alert; ABS and CDO: Standard Poor’s, Merrill

Lynch, and Citigroup Global Markets.

Asset Securitization: Concept and Market Development 15

35.

were primarily issuedby banks by selling their holdings of commercial and

industrial (CI) loans. CBOs were mainly issued by bond or stock fund

managers, who issue these securities to raise funds to purchase more bonds

or stocks for their management. As mentioned earlier, CDOs are the new

and popular asset securitization securities, as their underlying assets are ac-

tually themselves securities which include asset securitization securities. In

1996, CDO issuance was around $20 billion. It quickly grew to $75 billion

in 1998. Between 1998 and 2004, issuance of CDOs hovered between

$50 billion and $70 billion. CDOs flourished in the banner years of 2005

and 2006 when they posted two consecutive years of record-breaking issu-

ance of around $150 billion and $340 billion respectively. In 2007, as the

situation of subprime mortgages got progressively worse, CDO issuance

dropped markedly by one-third to $250 billion. In 2008 and 2009, there

was virtually no issuance of CDOs.

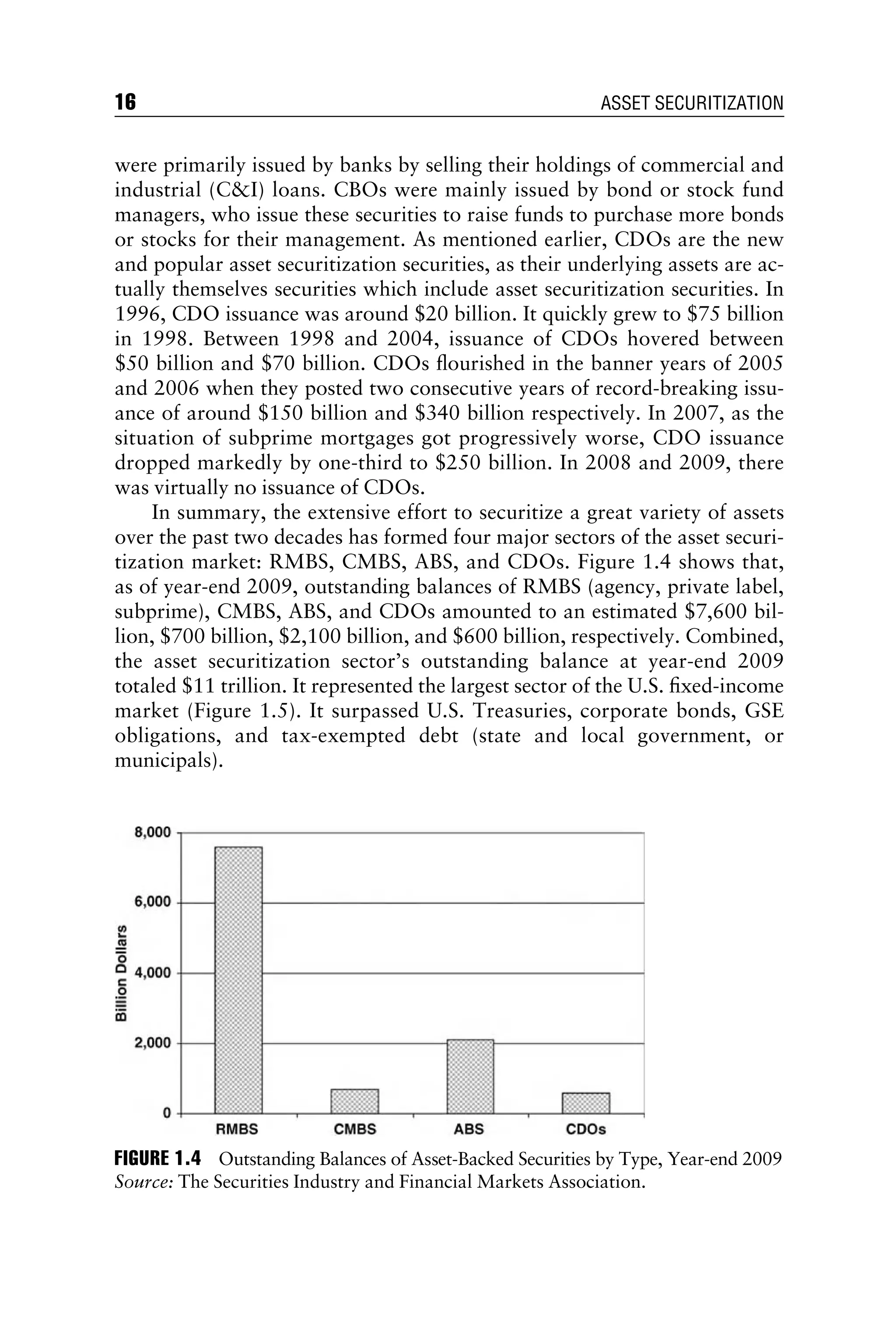

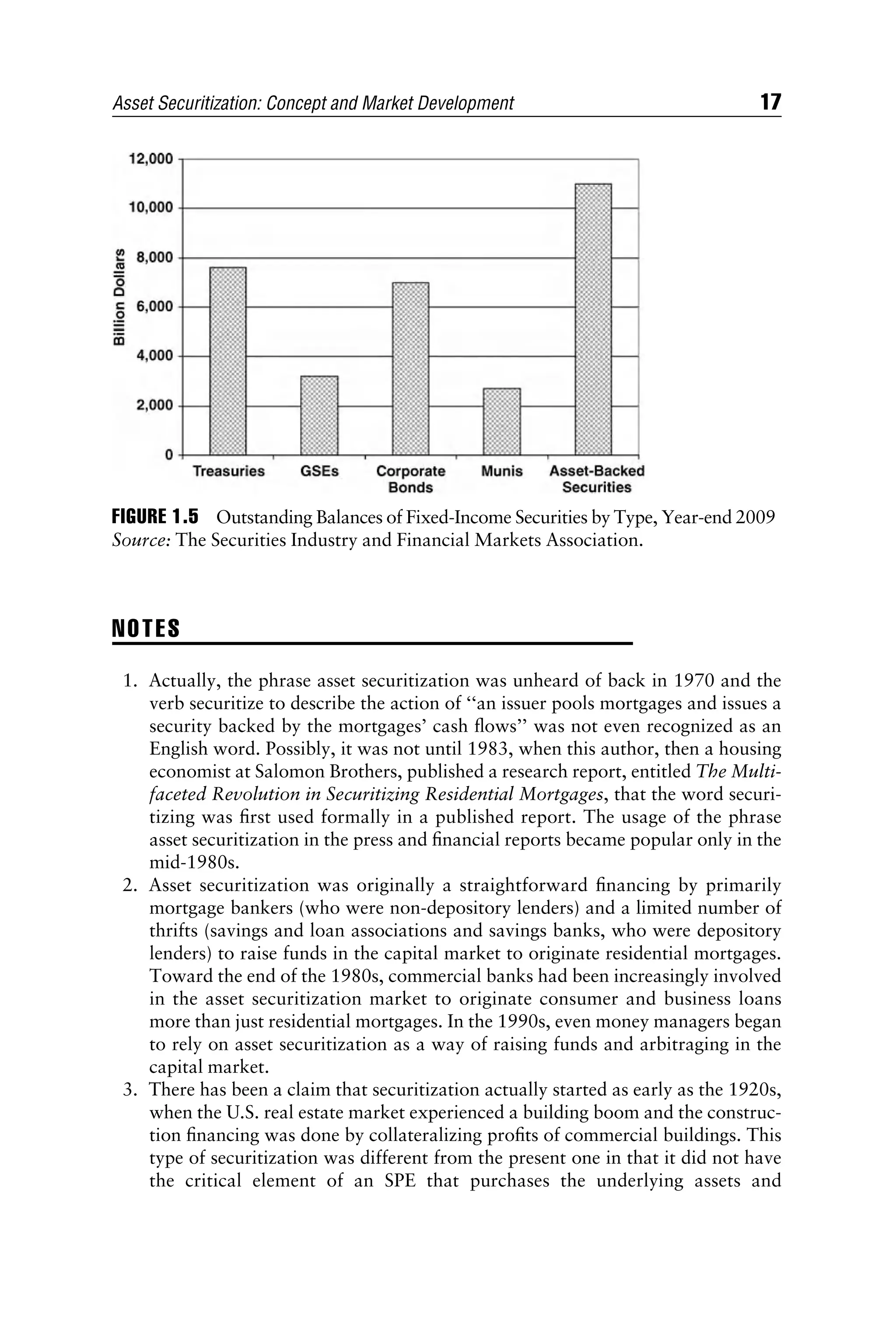

In summary, the extensive effort to securitize a great variety of assets

over the past two decades has formed four major sectors of the asset securi-

tization market: RMBS, CMBS, ABS, and CDOs. Figure 1.4 shows that,

as of year-end 2009, outstanding balances of RMBS (agency, private label,

subprime), CMBS, ABS, and CDOs amounted to an estimated $7,600 bil-

lion, $700 billion, $2,100 billion, and $600 billion, respectively. Combined,

the asset securitization sector’s outstanding balance at year-end 2009

totaled $11 trillion. It represented the largest sector of the U.S. fixed-income

market (Figure 1.5). It surpassed U.S. Treasuries, corporate bonds, GSE

obligations, and tax-exempted debt (state and local government, or

municipals).

FIGURE 1.4 Outstanding Balances of Asset-Backed Securities by Type, Year-end 2009

Source: The Securities Industry and Financial Markets Association.

16 ASSET SECURITIZATION

36.

NOTES

1. Actually, thephrase asset securitization was unheard of back in 1970 and the

verb securitize to describe the action of ‘‘an issuer pools mortgages and issues a

security backed by the mortgages’ cash flows’’ was not even recognized as an

English word. Possibly, it was not until 1983, when this author, then a housing

economist at Salomon Brothers, published a research report, entitled The Multi-

faceted Revolution in Securitizing Residential Mortgages, that the word securi-

tizing was first used formally in a published report. The usage of the phrase

asset securitization in the press and financial reports became popular only in the

mid-1980s.

2. Asset securitization was originally a straightforward financing by primarily

mortgage bankers (who were non-depository lenders) and a limited number of

thrifts (savings and loan associations and savings banks, who were depository

lenders) to raise funds in the capital market to originate residential mortgages.

Toward the end of the 1980s, commercial banks had been increasingly involved

in the asset securitization market to originate consumer and business loans

more than just residential mortgages. In the 1990s, even money managers began

to rely on asset securitization as a way of raising funds and arbitraging in the

capital market.

3. There has been a claim that securitization actually started as early as the 1920s,

when the U.S. real estate market experienced a building boom and the construc-

tion financing was done by collateralizing profits of commercial buildings. This

type of securitization was different from the present one in that it did not have

the critical element of an SPE that purchases the underlying assets and

FIGURE 1.5 Outstanding Balances of Fixed-Income Securities by Type, Year-end 2009

Source: The Securities Industry and Financial Markets Association.

Asset Securitization: Concept and Market Development 17

37.

simultaneously issues theasset-backed securities. See ‘‘In the Packaging of

Loans, A Bust with Precedent,’’ Floyd Norris, New York Times, January 28,

2010.

4. In the midst of the global financial crisis of 2008, both Freddie Mac and Fannie

Mae experienced tremendous financial difficulties with huge negative earnings

and severe shortages of capital. In September 2008, the U.S. government placed

the two GSEs into conservatorship run by the Federal Housing Finance Agency.

5. As will be elaborated on in later chapters, for this book non-agency pass-

throughs include private-label pass-throughs and subprime mortgage–backed

securities. Private-label pass-throughs were first issued in 1977 and subprime

mortgage-backed securities made their debut in the RMBS market in the late

1980s.

6. It should be noted here that as a general practice of market participants the

generic term of asset-backed securities refers to all structured finance securities

that are backed by any type of assets. A specific term, Asset-Backed Securities,

however, refers to only those securities backed by non-residential and non-

commercial mortgages, such as receivable cash flows of credit cards, auto loans,

student loans, manufactured housing loans, and small and medium enterprise

(SME) loans. Structured securities backed by residential mortgages are specifi-

cally called Residential Mortgage-Backed Securities (RMBS), and those backed

by commercial mortgages are termed Commercial Mortgage-Backed Securities

(CMBS).

18 ASSET SECURITIZATION

The remainder ofthis section uses simple numerical examples to

describe how an originator finances its loan originations through securi-

tization. By way of securitization, the originator is able to raise funds effi-

ciently. This efficiency is achieved by producing higher returns in the use of

capital with an effectively managed balance sheet. An effectively managed

balance sheet puts no undue pressure on capital adequacy and limits the

exposure of various risks on assets.

Consider, for example, an originator, Bank XYZ, that was not in the

business of originating residential mortgages in 2008, but plans to do so in

2009. (Residential mortgages are used in the hypothetical example because

they were the first to be securitized. Also, the example selects a bank, not a

mortgage banker, to show the economics of securitization because the latter

cannot attract deposits and has no choice but to sell to finance its loan origi-

nation.)2

As of December 31, 2008, Bank XYZ had a balance sheet as

shown in Table 2.1. For the purpose of illustration, the balance sheet is sim-

plified to have only a few assets and liabilities. Among the few assets, the

bank held consumer loans totaling $500,000 and a cash position of

$25,000. To finance its $525,000 worth of total assets, the bank relies on

the traditional funding source of deposits and debentures totaling

$483,000. There is, of course, an additional source of funds: the sharehold-

ers’ equity of $42,000. This equity amounts to 8 percent of the total assets.

For the 2009 operation, assume this bank decides to originate

$4,000,000 worth of residential mortgages and to fund the origination

entirely by attracting deposits. This is the traditional way of banks funding

loan originations. It is generally referred to as portfolio lending, in that the

originator books the newly originated loans as an addition to its portfolio.

In this case, assume further that the bank does not engage in any other lend-

ing activities during the year; the asset side of its balance sheet at the end of

2009 will have an additional item of $4,000,000 mortgages (Table 2.2).

This portfolio lending has the consequence of substantially expanding the

size of the bank’s total assets to $4,525,000. Similarly, the lending also in-

creases its liabilities to $4,163,000. To maintain the same assets-to-capital

ratio, the bank also manages to raise its capital by $320,000 to $362,000.

TABLE 2.1 Balance Sheet of Bank XYZ, as of December 31, 2008

Cash $ 25,000 Deposits $433,000

Consumer loans $500,000 Debentures $ 50,000

Capital $ 42,000

Total Assets $525,000 Total Liabilities and Capital $525,000

20 ASSET SECURITIZATION

40.

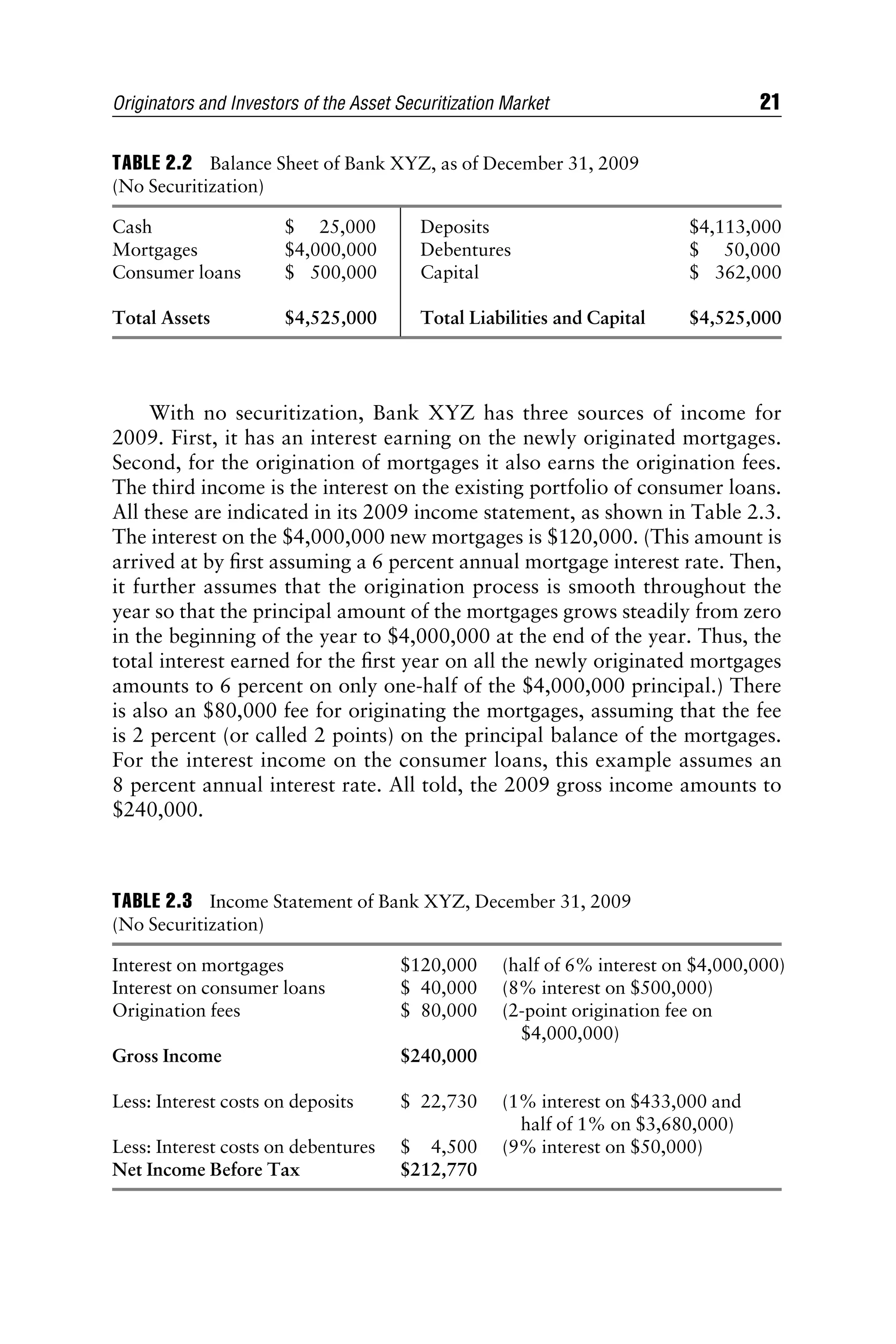

With no securitization,Bank XYZ has three sources of income for

2009. First, it has an interest earning on the newly originated mortgages.

Second, for the origination of mortgages it also earns the origination fees.

The third income is the interest on the existing portfolio of consumer loans.

All these are indicated in its 2009 income statement, as shown in Table 2.3.

The interest on the $4,000,000 new mortgages is $120,000. (This amount is

arrived at by first assuming a 6 percent annual mortgage interest rate. Then,

it further assumes that the origination process is smooth throughout the

year so that the principal amount of the mortgages grows steadily from zero

in the beginning of the year to $4,000,000 at the end of the year. Thus, the

total interest earned for the first year on all the newly originated mortgages

amounts to 6 percent on only one-half of the $4,000,000 principal.) There

is also an $80,000 fee for originating the mortgages, assuming that the fee

is 2 percent (or called 2 points) on the principal balance of the mortgages.

For the interest income on the consumer loans, this example assumes an

8 percent annual interest rate. All told, the 2009 gross income amounts to

$240,000.

TABLE 2.2 Balance Sheet of Bank XYZ, as of December 31, 2009

(No Securitization)

Cash $ 25,000 Deposits $4,113,000

Mortgages $4,000,000 Debentures $ 50,000

Consumer loans $ 500,000 Capital $ 362,000

Total Assets $4,525,000 Total Liabilities and Capital $4,525,000

TABLE 2.3 Income Statement of Bank XYZ, December 31, 2009

(No Securitization)

Interest on mortgages $120,000 (half of 6% interest on $4,000,000)

Interest on consumer loans $ 40,000 (8% interest on $500,000)

Origination fees $ 80,000 (2-point origination fee on

$4,000,000)

Gross Income $240,000

Less: Interest costs on deposits $ 22,730 (1% interest on $433,000 and

half of 1% on $3,680,000)

Less: Interest costs on debentures $ 4,500 (9% interest on $50,000)

Net Income Before Tax $212,770

Originators and Investors of the Asset Securitization Market 21

41.

Bank XYZ hastwo expenses (for simplicity, ignore operation expenses)

in 2009. The first expense is the $22,730 interest paid on deposits, assuming

an annual 1 percent interest on both the existing and the new deposits.

There is the interest expense of $4,330 on the existing deposits of

$433,000. For the funding of the $4,000,000 mortgage originations, the in-

terest cost on the corresponding new deposits $3,680,000 steadily acquired

throughout the year is $18,400 (for the same reasoning as calculating the

interest earned on the new mortgages). The second expense is the $4,500

interest paid on the debenture (assuming an annual interest rate of 9 per-

cent). To sum up, after netting out the two expenses, the bank has a before-

tax income of $212,770. This income represents a 4.7 percent return on

assets and 58.8 percent return on equity.

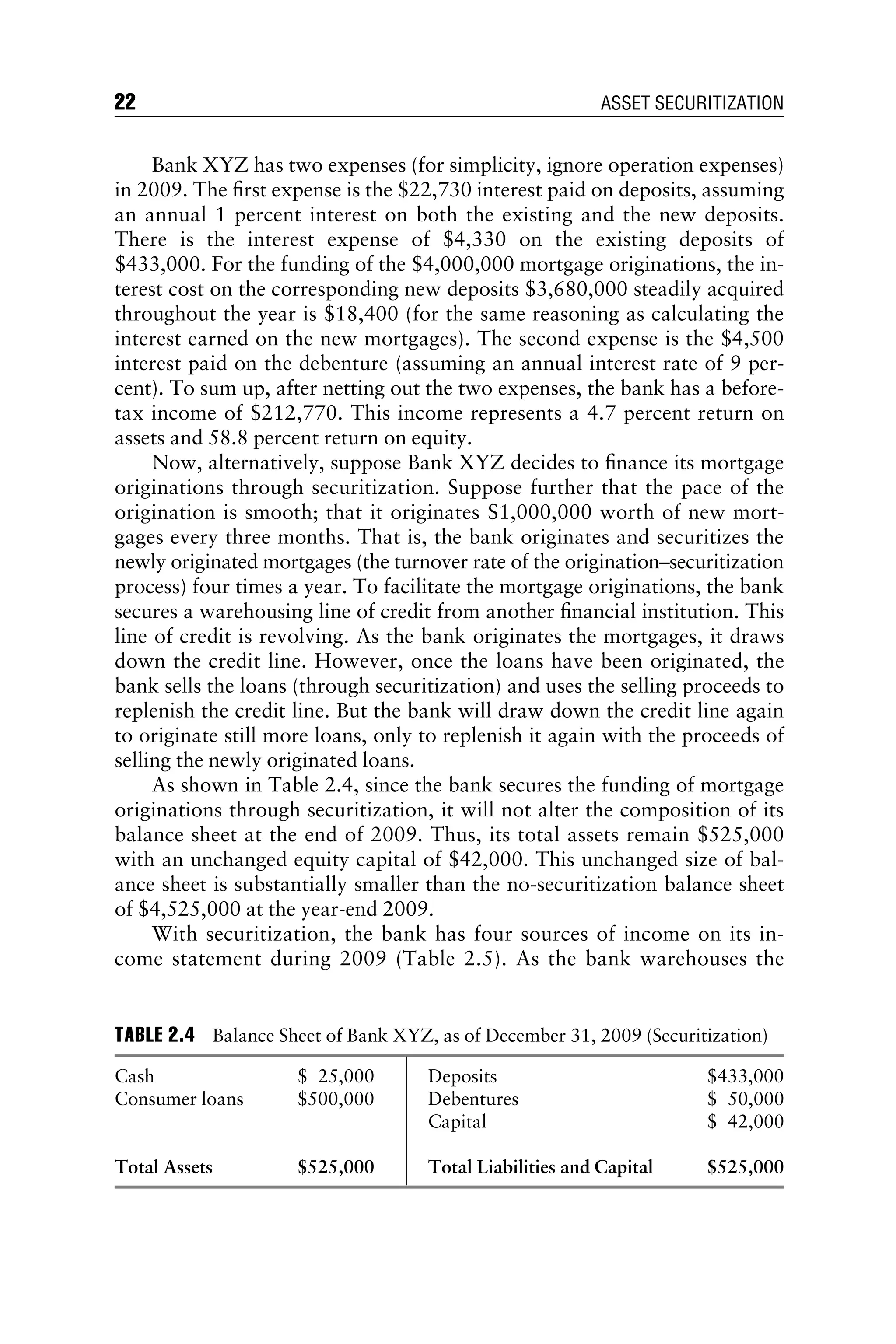

Now, alternatively, suppose Bank XYZ decides to finance its mortgage

originations through securitization. Suppose further that the pace of the

origination is smooth; that it originates $1,000,000 worth of new mort-

gages every three months. That is, the bank originates and securitizes the

newly originated mortgages (the turnover rate of the origination–securitization

process) four times a year. To facilitate the mortgage originations, the bank

secures a warehousing line of credit from another financial institution. This

line of credit is revolving. As the bank originates the mortgages, it draws

down the credit line. However, once the loans have been originated, the

bank sells the loans (through securitization) and uses the selling proceeds to

replenish the credit line. But the bank will draw down the credit line again

to originate still more loans, only to replenish it again with the proceeds of

selling the newly originated loans.

As shown in Table 2.4, since the bank secures the funding of mortgage

originations through securitization, it will not alter the composition of its

balance sheet at the end of 2009. Thus, its total assets remain $525,000

with an unchanged equity capital of $42,000. This unchanged size of bal-

ance sheet is substantially smaller than the no-securitization balance sheet

of $4,525,000 at the year-end 2009.

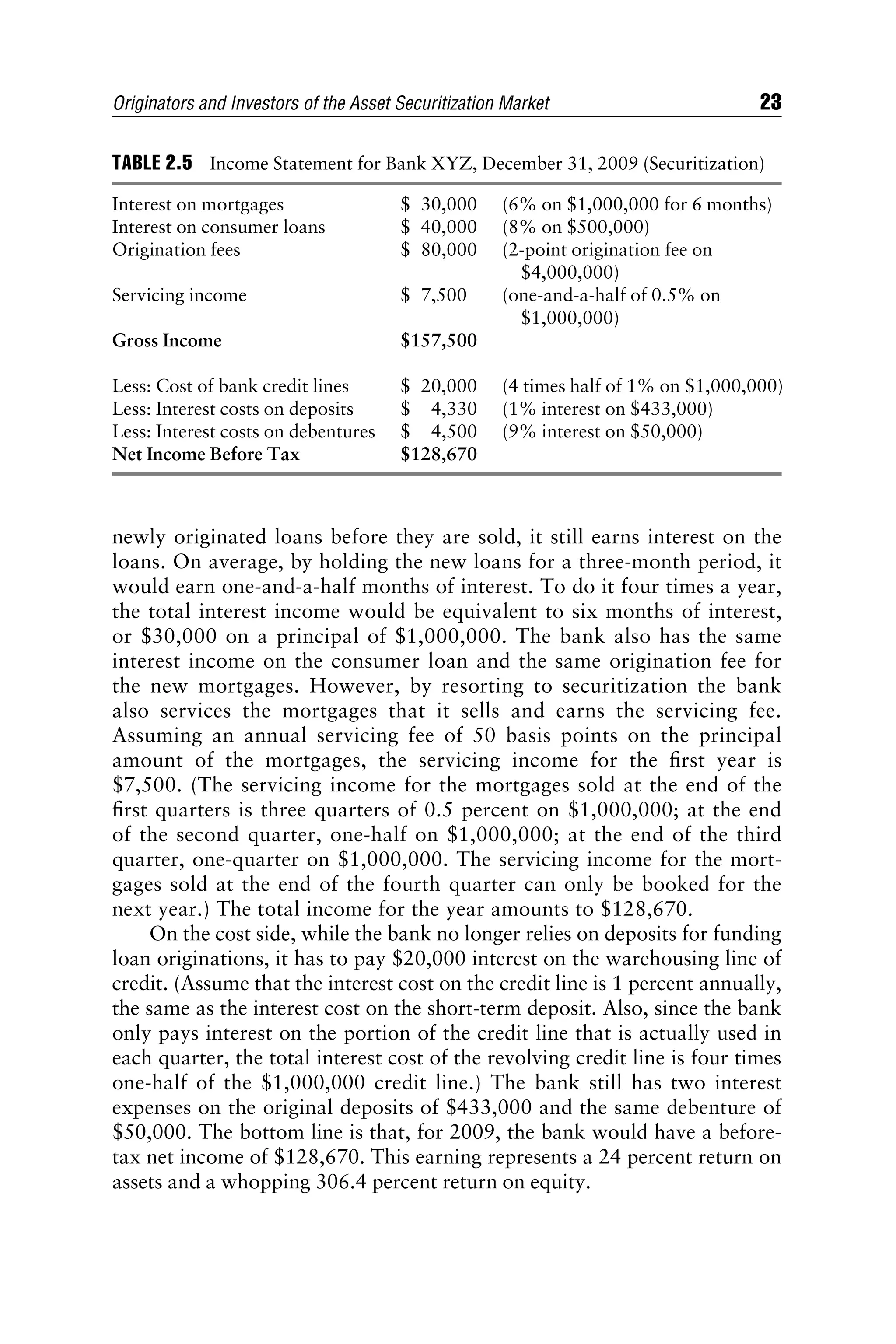

With securitization, the bank has four sources of income on its in-

come statement during 2009 (Table 2.5). As the bank warehouses the

TABLE 2.4 Balance Sheet of Bank XYZ, as of December 31, 2009 (Securitization)

Cash $ 25,000 Deposits $433,000

Consumer loans $500,000 Debentures $ 50,000

Capital $ 42,000

Total Assets $525,000 Total Liabilities and Capital $525,000

22 ASSET SECURITIZATION

42.

newly originated loansbefore they are sold, it still earns interest on the

loans. On average, by holding the new loans for a three-month period, it

would earn one-and-a-half months of interest. To do it four times a year,

the total interest income would be equivalent to six months of interest,

or $30,000 on a principal of $1,000,000. The bank also has the same

interest income on the consumer loan and the same origination fee for

the new mortgages. However, by resorting to securitization the bank

also services the mortgages that it sells and earns the servicing fee.

Assuming an annual servicing fee of 50 basis points on the principal

amount of the mortgages, the servicing income for the first year is

$7,500. (The servicing income for the mortgages sold at the end of the

first quarters is three quarters of 0.5 percent on $1,000,000; at the end

of the second quarter, one-half on $1,000,000; at the end of the third

quarter, one-quarter on $1,000,000. The servicing income for the mort-

gages sold at the end of the fourth quarter can only be booked for the

next year.) The total income for the year amounts to $128,670.

On the cost side, while the bank no longer relies on deposits for funding

loan originations, it has to pay $20,000 interest on the warehousing line of

credit. (Assume that the interest cost on the credit line is 1 percent annually,

the same as the interest cost on the short-term deposit. Also, since the bank

only pays interest on the portion of the credit line that is actually used in

each quarter, the total interest cost of the revolving credit line is four times

one-half of the $1,000,000 credit line.) The bank still has two interest

expenses on the original deposits of $433,000 and the same debenture of

$50,000. The bottom line is that, for 2009, the bank would have a before-

tax net income of $128,670. This earning represents a 24 percent return on

assets and a whopping 306.4 percent return on equity.

TABLE 2.5 Income Statement for Bank XYZ, December 31, 2009 (Securitization)

Interest on mortgages $ 30,000 (6% on $1,000,000 for 6 months)

Interest on consumer loans $ 40,000 (8% on $500,000)

Origination fees $ 80,000 (2-point origination fee on

$4,000,000)

Servicing income $ 7,500 (one-and-a-half of 0.5% on

$1,000,000)

Gross Income $157,500

Less: Cost of bank credit lines $ 20,000 (4 times half of 1% on $1,000,000)

Less: Interest costs on deposits $ 4,330 (1% interest on $433,000)

Less: Interest costs on debentures $ 4,500 (9% interest on $50,000)

Net Income Before Tax $128,670

Originators and Investors of the Asset Securitization Market 23

43.

While Bank XYZproduces much smaller earnings through securitiza-

tion than no securitization, it earns more dollar-for-dollar in terms of return

on assets (24.5 percent versus 4.7 percent) and return on equity (306.4 per-

cent versus 58.8 percent). There are also additional advantages that are not

evident in financial figures. First, since the balance sheet has not expanded,

the bank is under no pressure to raise new capital. Second, with securitiza-

tion, there is no maturity mismatch between assets and liabilities. With no

securitization, the bank runs a huge interest rate risk with the maturity of its

assets being much longer than that of liabilities. Third, in addition to the

interest rate risk, the no-securitization approach also adds substantial credit

risk to the bank’s balance sheet.

The simplified example demonstrates this: through securitization, the

bank is able to not only satisfy its financing needs, but also generate better

earnings with an efficiently managed balance sheet. By generating better

earnings, the bank can maintain a stronger capital position. By efficiently

managing the balance sheet, the bank can free up precious capital for other

lending and investment activities.

SATISFYING VARYING INVESTOR DEMANDS WITH

ASSET SECURITIZATION

One important reason why the U.S. asset securitization market could

achieve a remarkably long run of success was its ability to create investment

products that satisfy the varying investor demands. It can also be said that

the steady expansion of the investor base through the years has facilitated

the rapid growth of the asset securitization market. This expanded base

comprises a great variety of investors, ranging from short-term money mar-

ket investors, commercial bank portfolio managers, to long-term pension

fund managers. (It is important to note that investors in asset-backed securi-

ties are primarily institutional investors with very few individual investors.

To the extent that individual investors do get involved, they basically invest

through mutual fund managers.) Nowadays, virtually all types of fixed-

income investors own, to a varying degree, asset-backed securities with

underlying assets in the form of various consumer loans, commercial loans,

residential mortgages, and commercial mortgages.

The rapid expansion of asset-backed securities investors is not inciden-

tal. It took a great deal of research and marketing efforts on the part of issu-

ers, investment bankers, and rating agencies to cultivate and educate

investors on the investment features and credit performances of the asset-

backed securities. Investors, through the prices they are willing to pay, also

constantly provided feedback on the asset securitization products, which

24 ASSET SECURITIZATION

44.

drove improvement andinnovation of asset-backed securities. (As will be

presented in later chapters on various asset-backed securities, the prices

are actually expressed in yield spreads through secondary market trading.)

The remainder of this section explains how investors facilitated the growth

of asset-backed securities and how the facilitation in turn benefited inves-

tors by providing attractive returns for their investments.

Cultivating Investors: Matching Products

with Investment Demands

One of the most important goals of investing is to achieve the highest possi-

ble return given the risks of the investment. Since the cash flows of asset-

backed securities are derived solely from the underlying collateral, it is

critical that investors understand the investment characteristics of the

underlying assets. One example of this is RMBS. As will be discussed later

in detail in the RMBS chapters, residential mortgages are prepayable at par.

Thus, RMBS have a unique prepayment risk. When mortgage rates decline,

mortgagors (homeowners who borrow money from lenders to purchase

homes) tend to refinance their existing mortgages with new mortgages that

carry lower interest rates. As mortgagors refinance, the proceeds of pre-

payment would be returned at par to the RMBS investors.