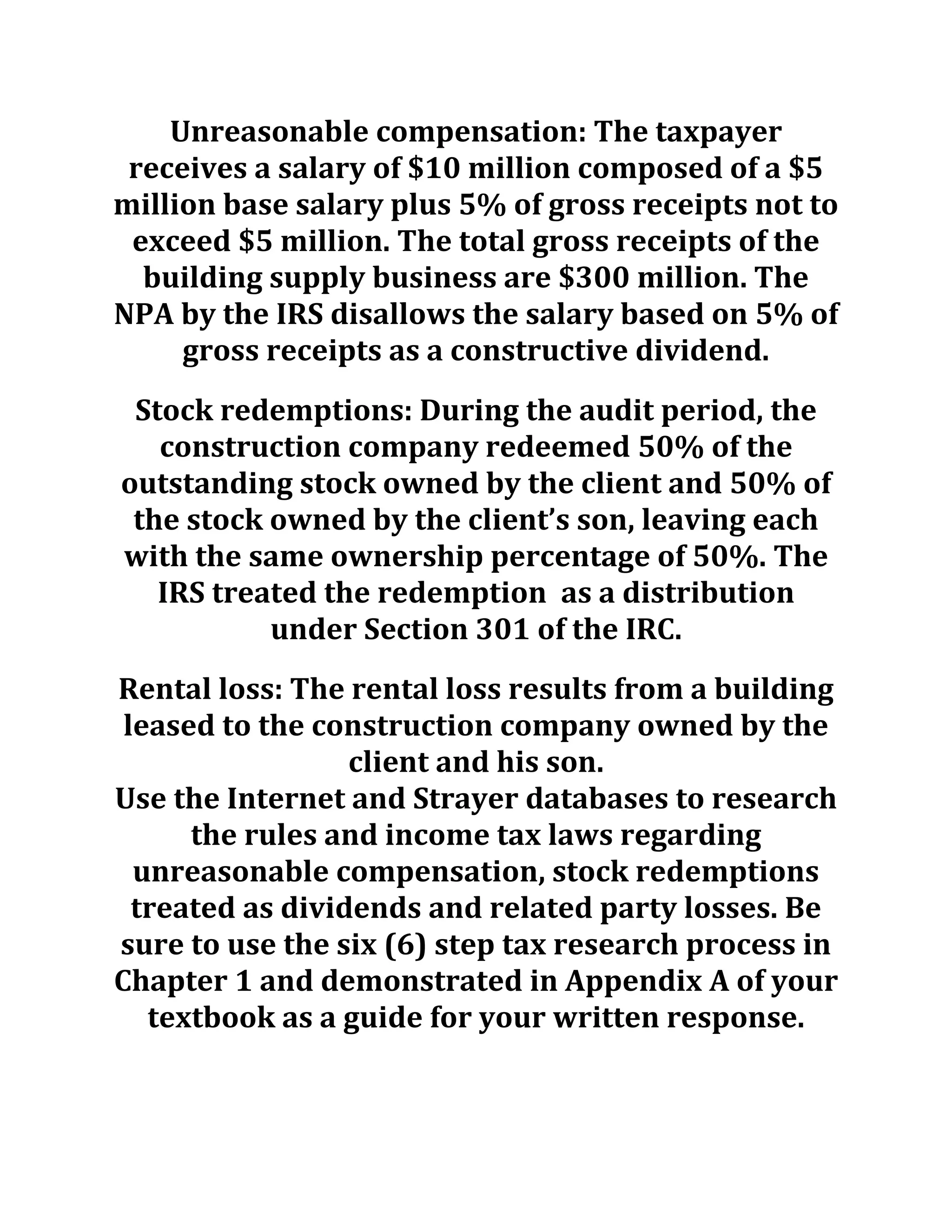

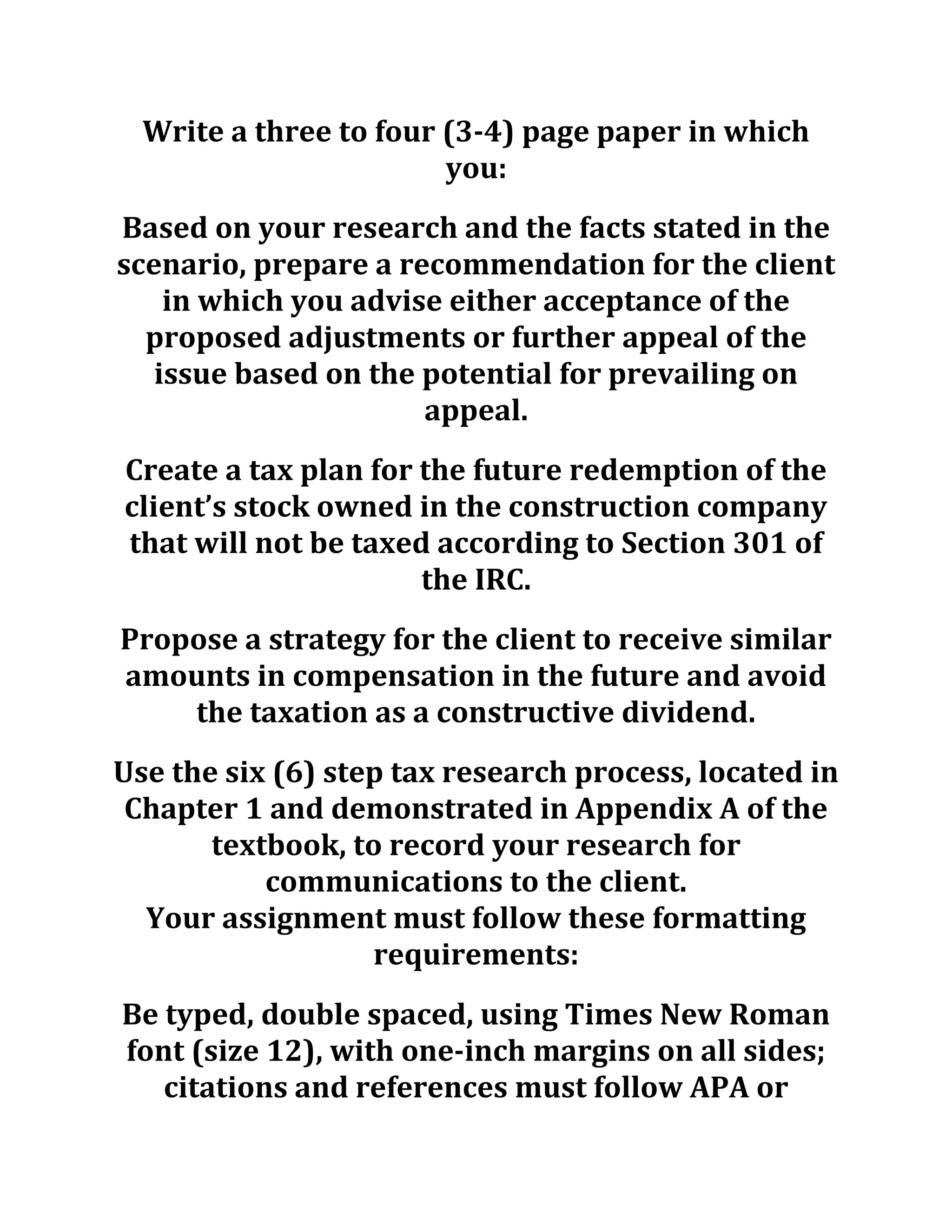

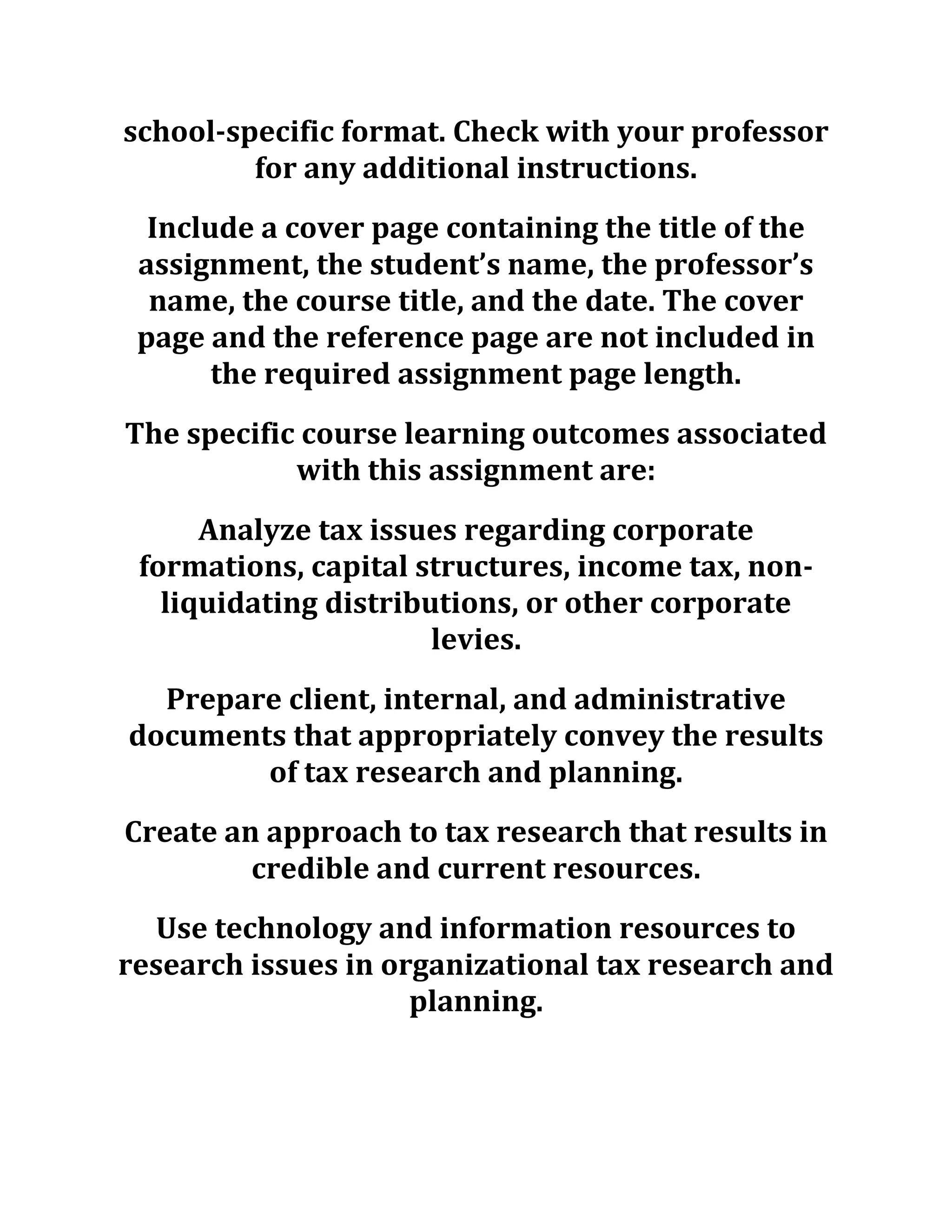

The document outlines an assignment for a CPA representing a client facing IRS examination on issues including unreasonable compensation, stock redemptions, and rental losses related to the client's business. The CPA is directed to conduct tax research and provide recommendations on accepting IRS adjustments or appealing them, along with creating a tax plan for future stock redemptions and compensation strategies. The assignment emphasizes following a six-step tax research process and adhering to specific formatting and content requirements.