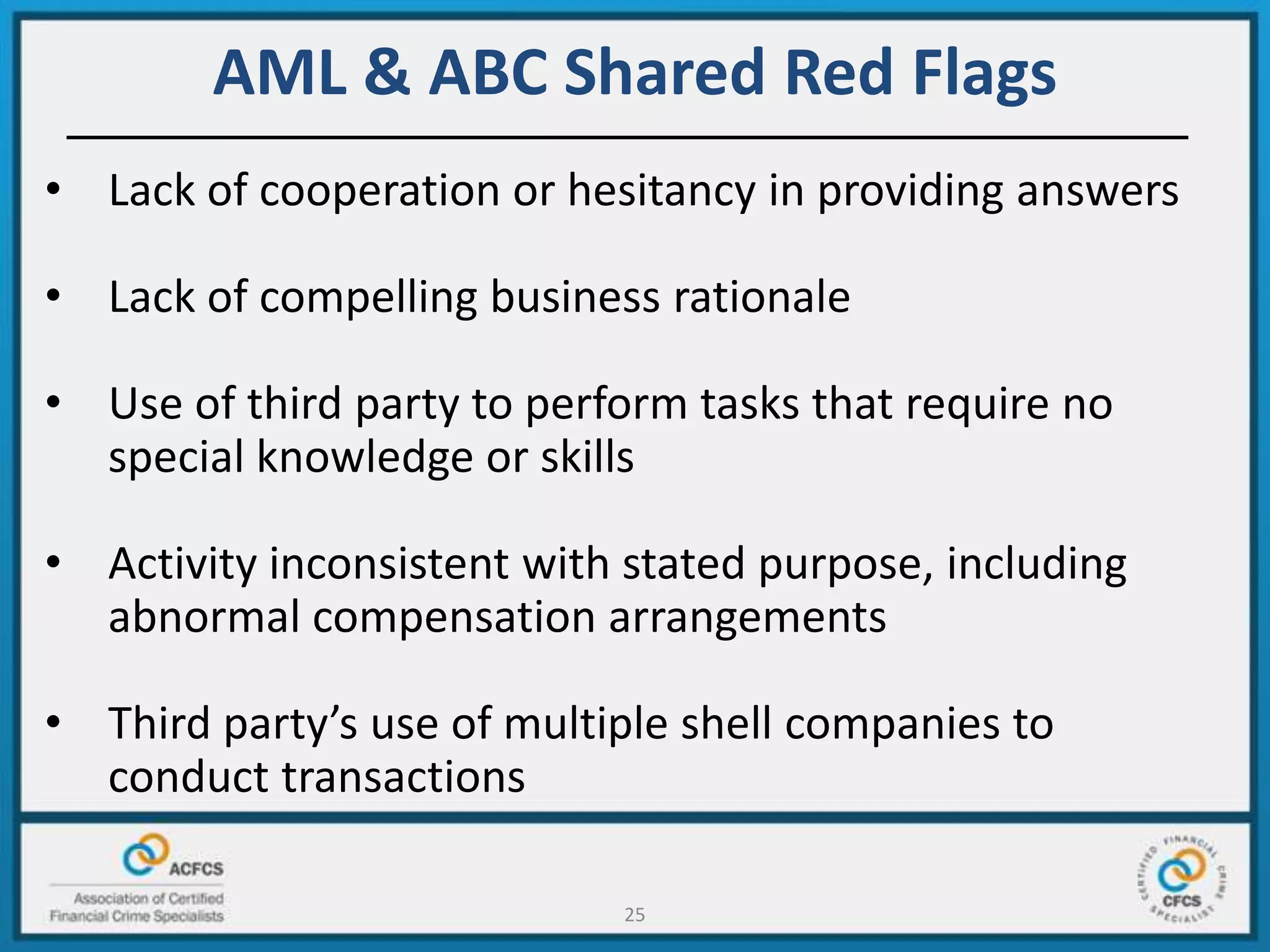

The webinar discusses the integration of anti-money laundering (AML) tools into anti-bribery and corruption (ABC) programs, emphasizing the need for operational optimization and third-party due diligence. Key points include the urgency of addressing global corruption, the overlap between AML and ABC risks, and the importance of compliance frameworks that incorporate governance, risk assessments, and due diligence. Participants are guided on how to leverage their existing systems to enhance compliance and mitigate risks associated with financial crimes.

![Emphasis on Anti-Corruption

“As we’ve all seen – and as President Obama has said – “[t]he struggle against corruption is

one of the great struggles of our time.” Fortunately [...] corruption is no longer widely seen

as an accepted cost of doing business. It is no longer tolerated as an unavoidable aspect of

government. On the contrary – it is now generally understood that the consequences of

corruption are devastating – eroding trust in public and private institutions, undermining

confidence in the fairness of free and open markets, siphoning precious resources at a

time when they could hardly be more scarce, and all too often breeding contempt for the

rule of law [...] This is why, as Attorney General, I’ve consistently worked to ensure that

anticorruption remains a top priority for my colleagues at every level of the United States

Department of Justice – within as well as beyond our borders.”

– Attorney General Eric Holder at the Arab Forum on Asset Recovery in Morocco (Oct.

28, 2013)

I am acutely aware that we have many urgent law enforcement priorities –

fighting child exploitation, stemming the flow of narcotics from South

America and elsewhere, stopping gang violence. I am here to tell you that

fighting global corruption is just as urgent, and with the momentum of many

countries behind us, now is the time to redouble our anti-corruption efforts.

– Former Deputy Attorney General, Lanny Breuer, ACI Conferences on the

Foreign Corruption Practices Act (Nov. 16, 2012)

4](https://image.slidesharecdn.com/acfcswebinaramlmeetsabchr21914-140221173704-phpapp02/75/AML-Meets-ABC-Webinar-Deck-2-19-14-4-2048.jpg)

![Examples – Money Laundering

• Cash proceeds from drug trafficking are used to purchase chips at a

casino.

– Money launderer gambles for a while, cashes in the chips, and

receives a check payment

– Check is deposited into the bank

– Cash is later withdrawn to purchase consumer goods

• The deputy minister of mining [in the corruption example] deposits

the $100K from Company A’s third party agent into his local bank

account. He then transfers the $100K into his son’s account at a

U.S. financial institution. The son, who lives in the U.S., then uses

the $100K to purchase a fancy sports car.

10](https://image.slidesharecdn.com/acfcswebinaramlmeetsabchr21914-140221173704-phpapp02/75/AML-Meets-ABC-Webinar-Deck-2-19-14-10-2048.jpg)