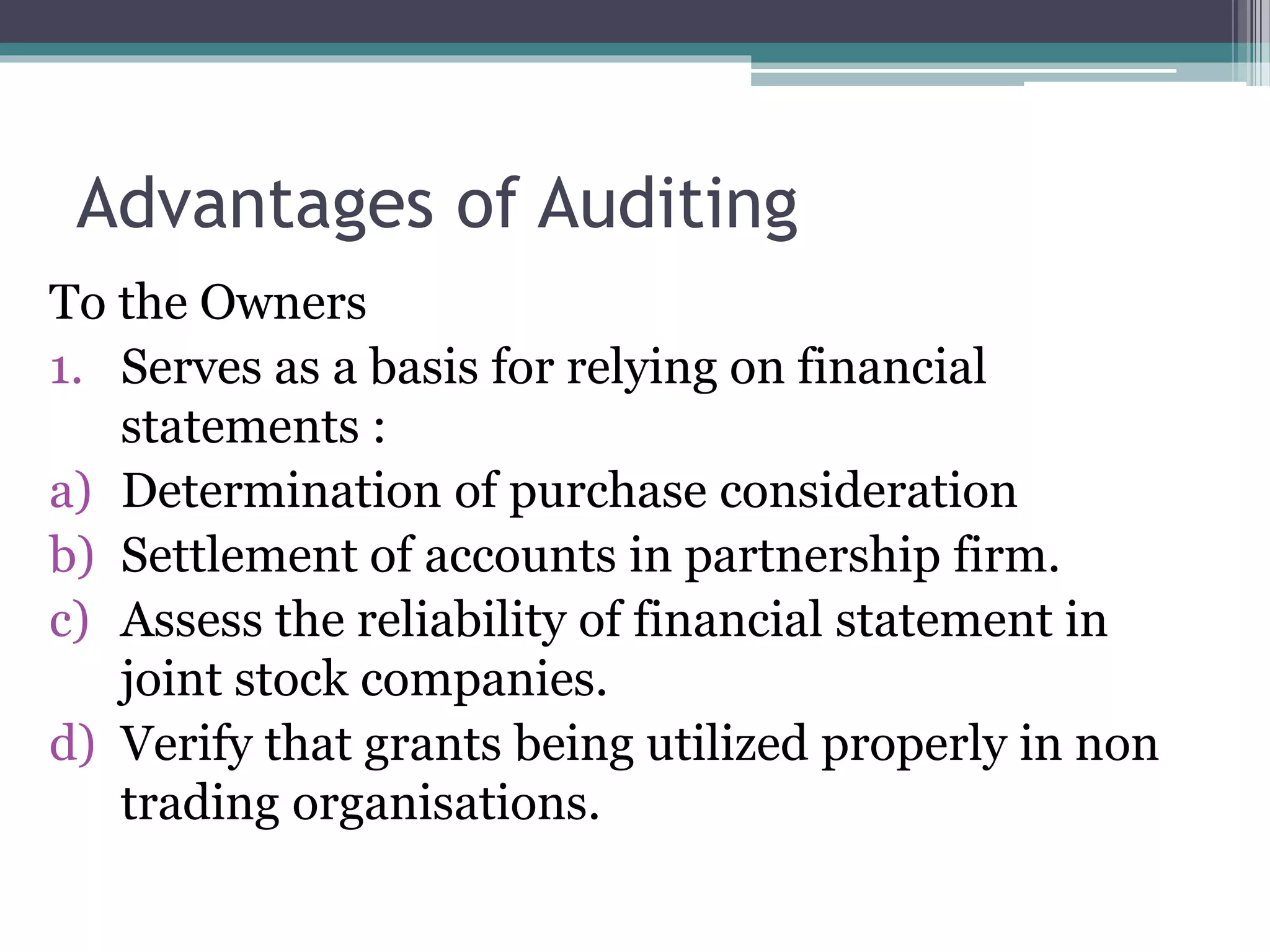

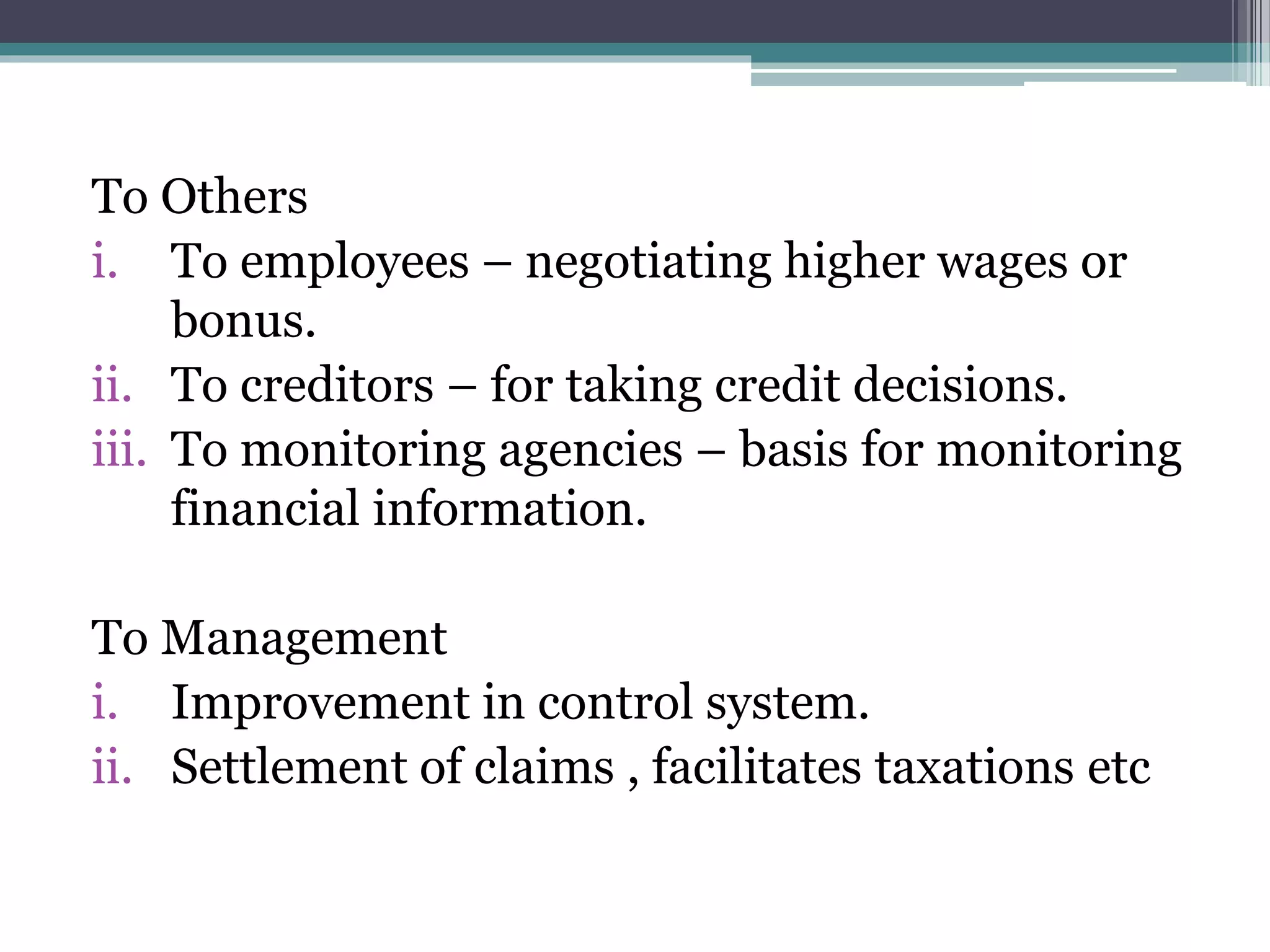

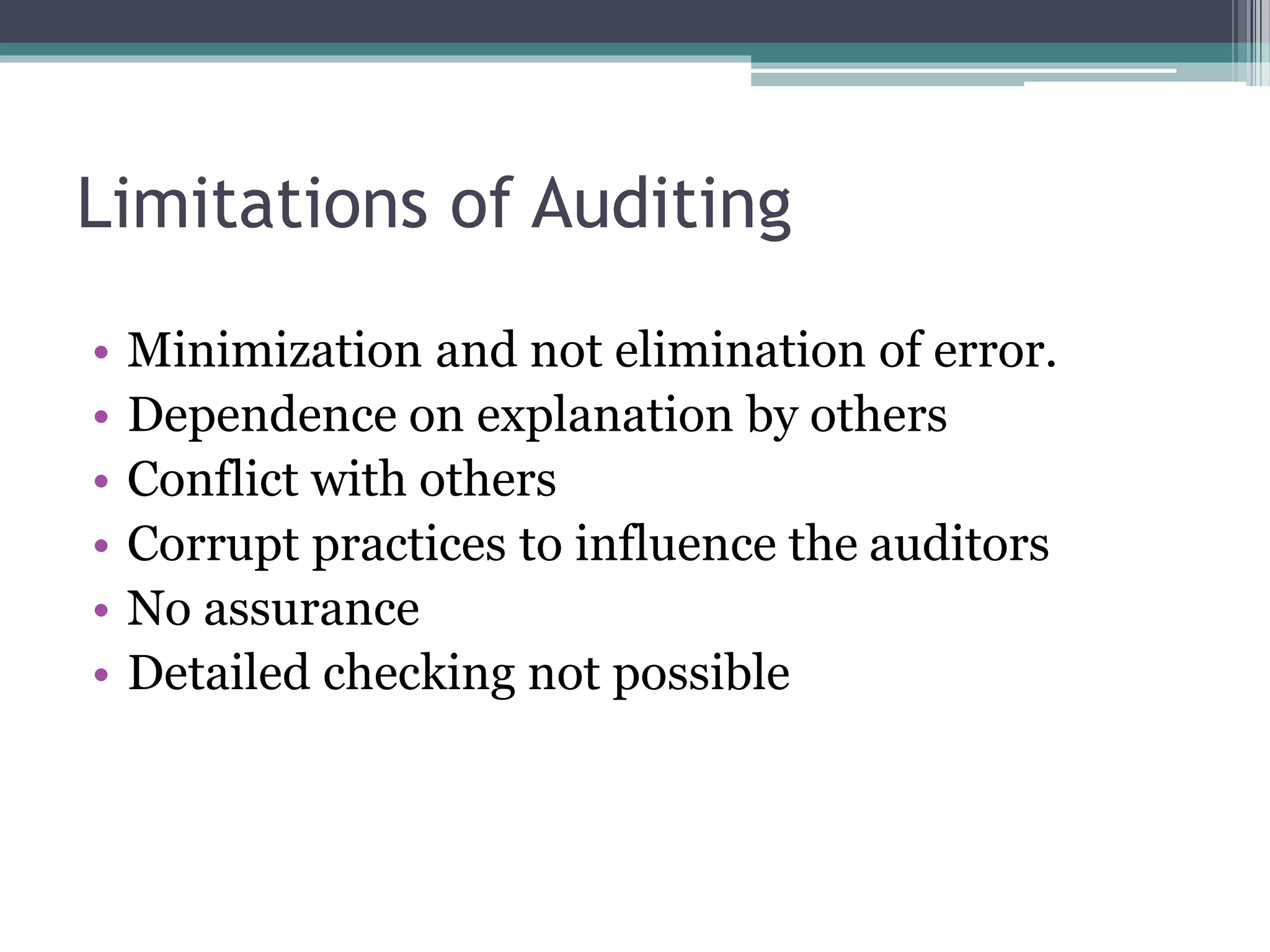

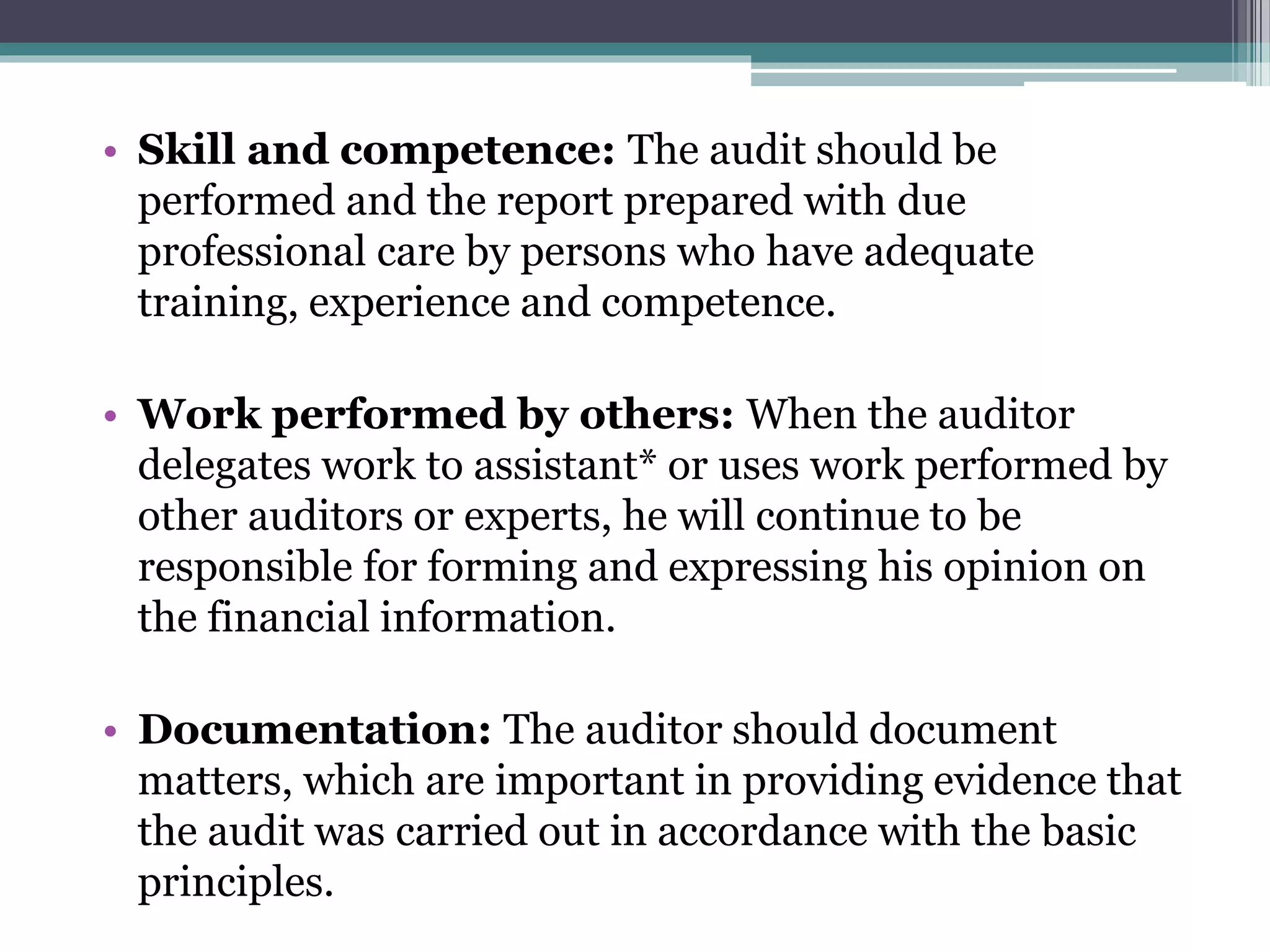

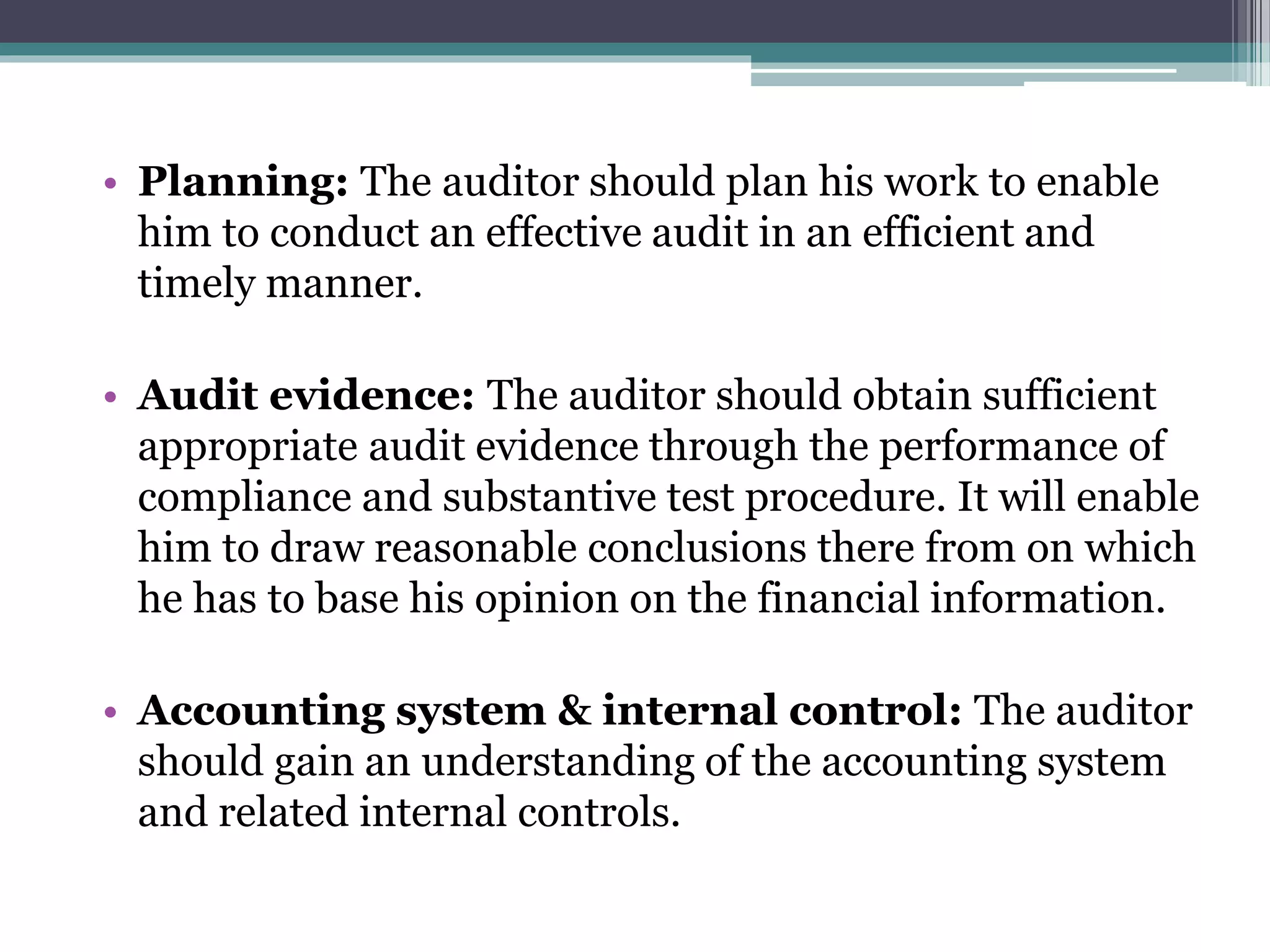

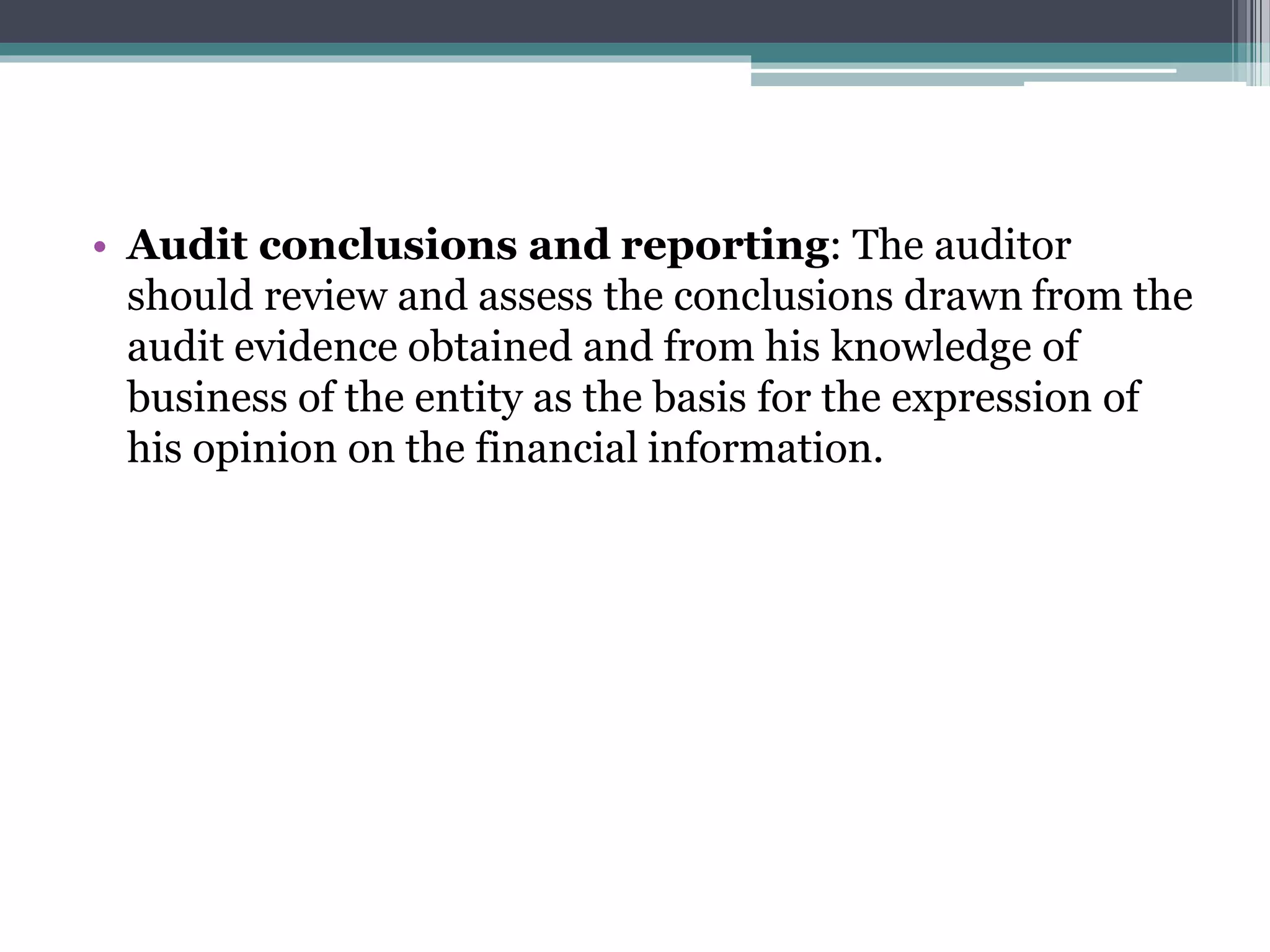

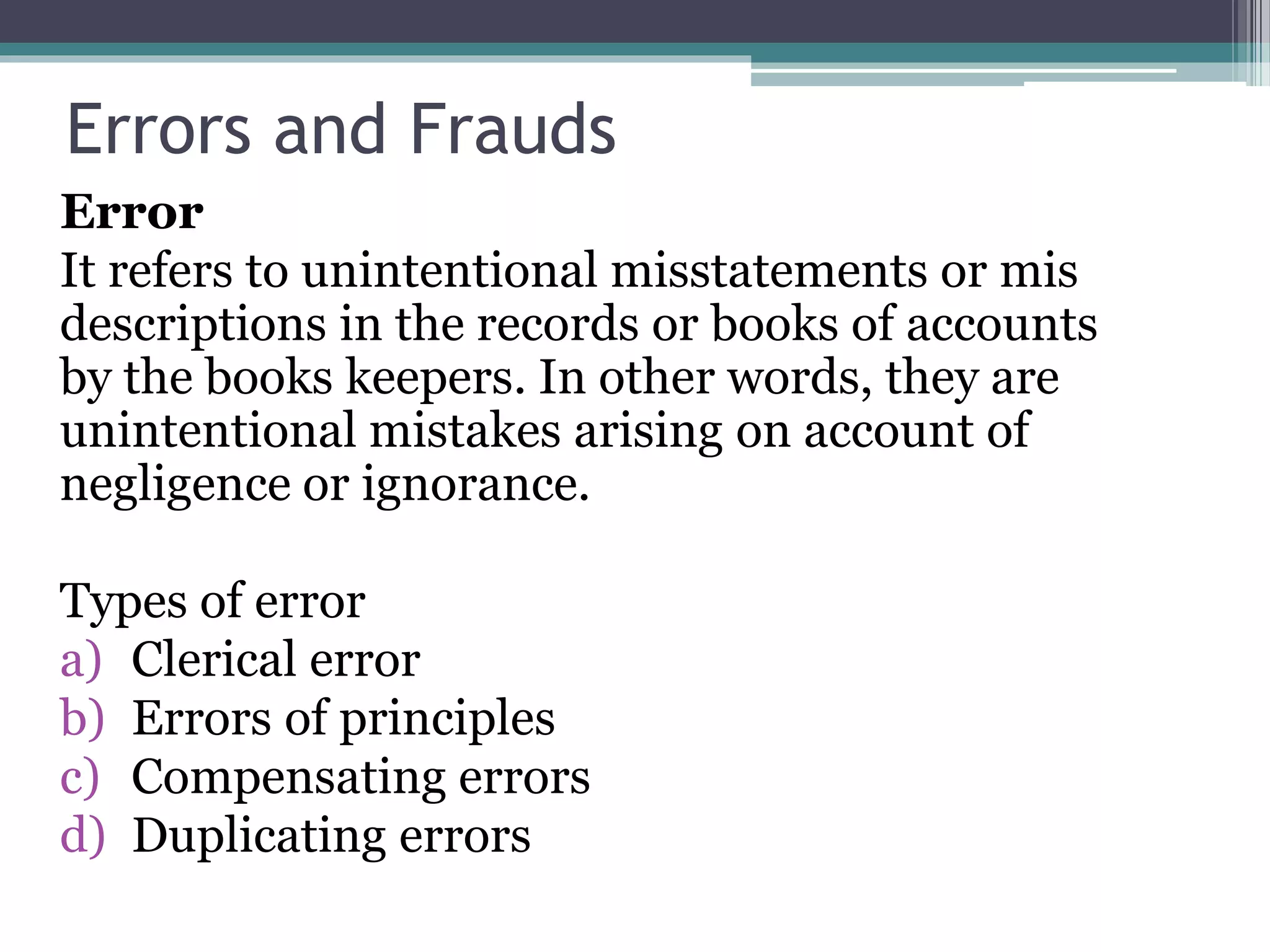

This document provides an overview of auditing, including:

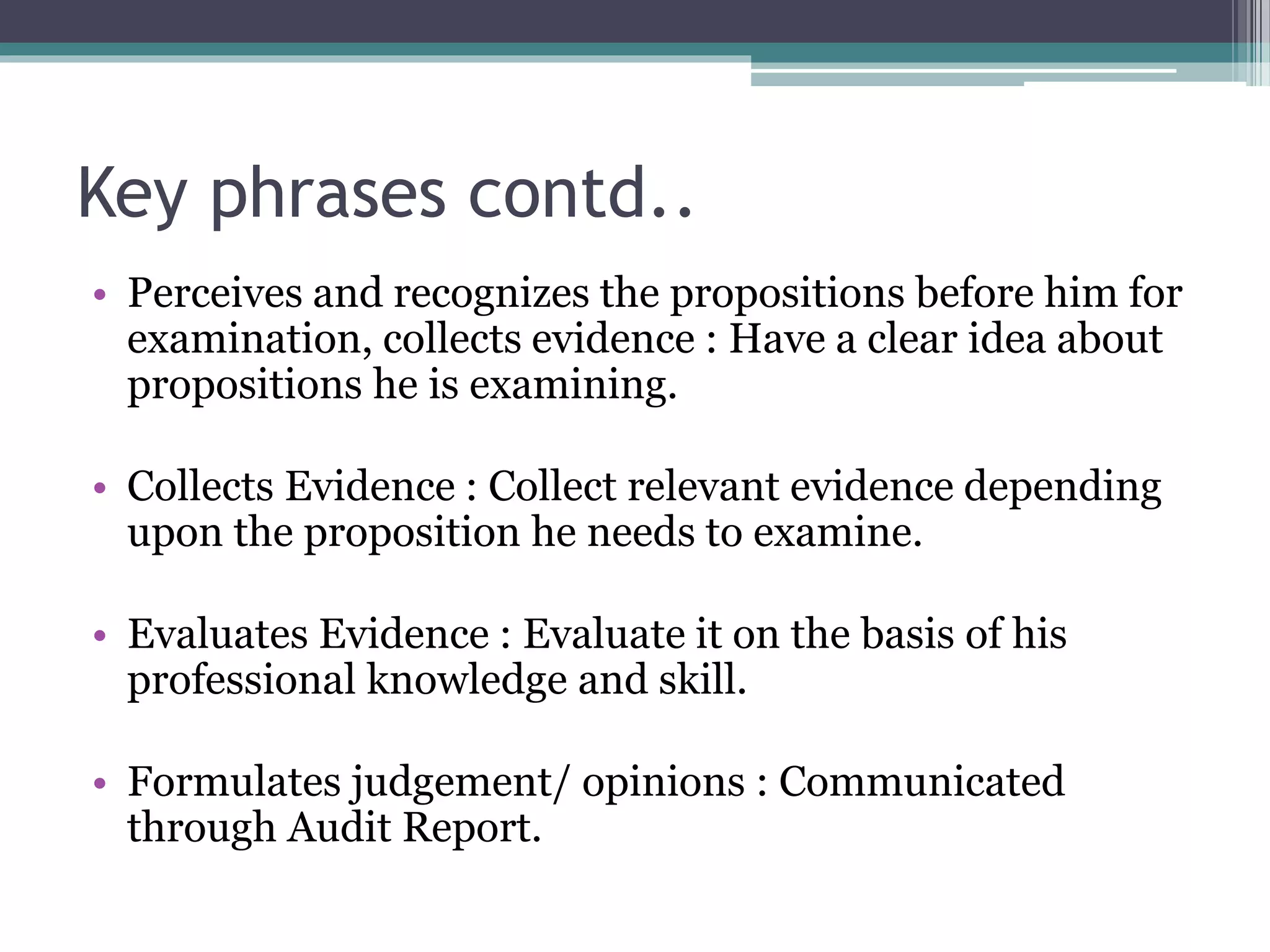

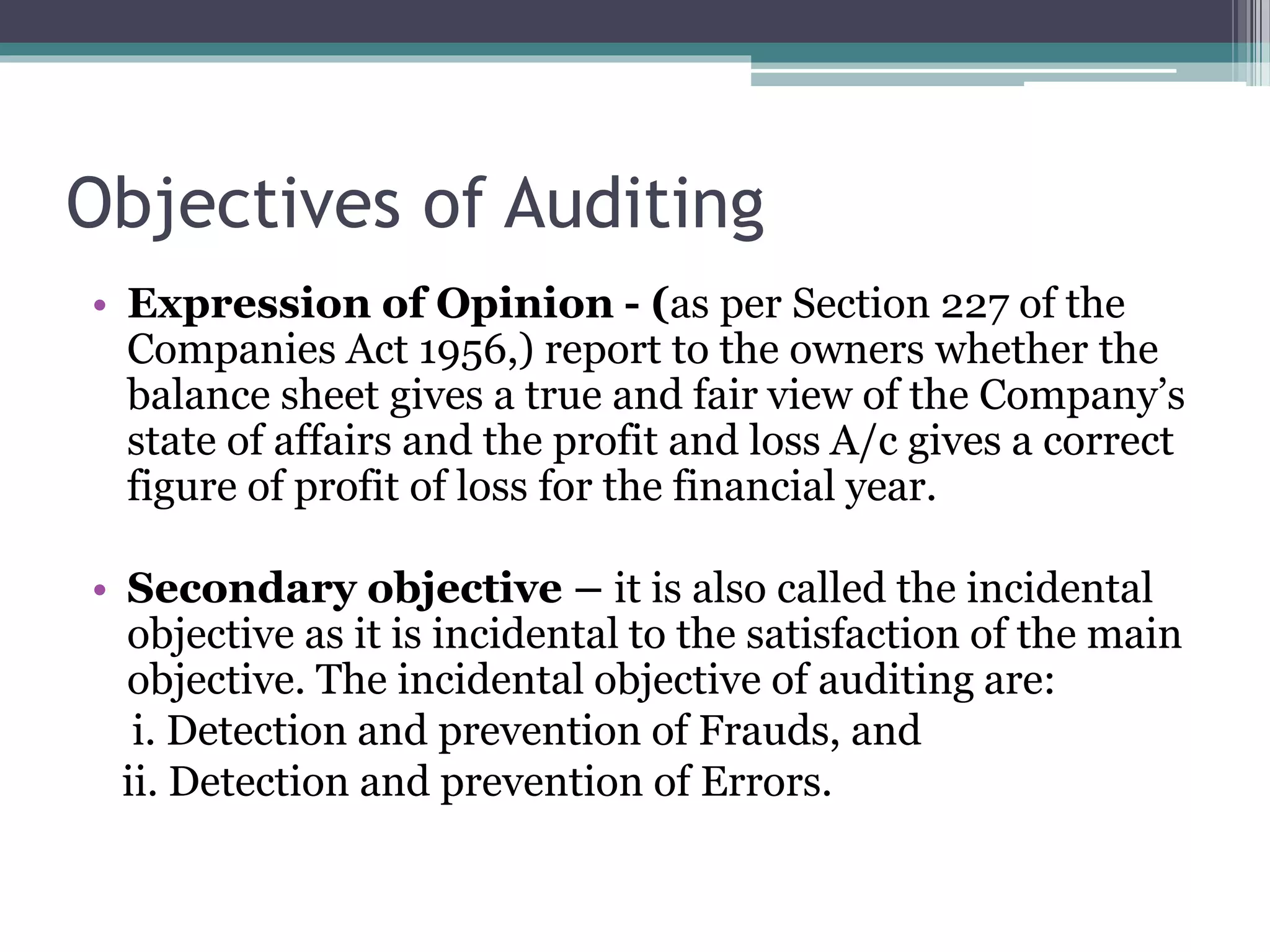

- The objectives and evolution of auditing from detecting errors and frauds to ascertaining if accounts are true and fair.

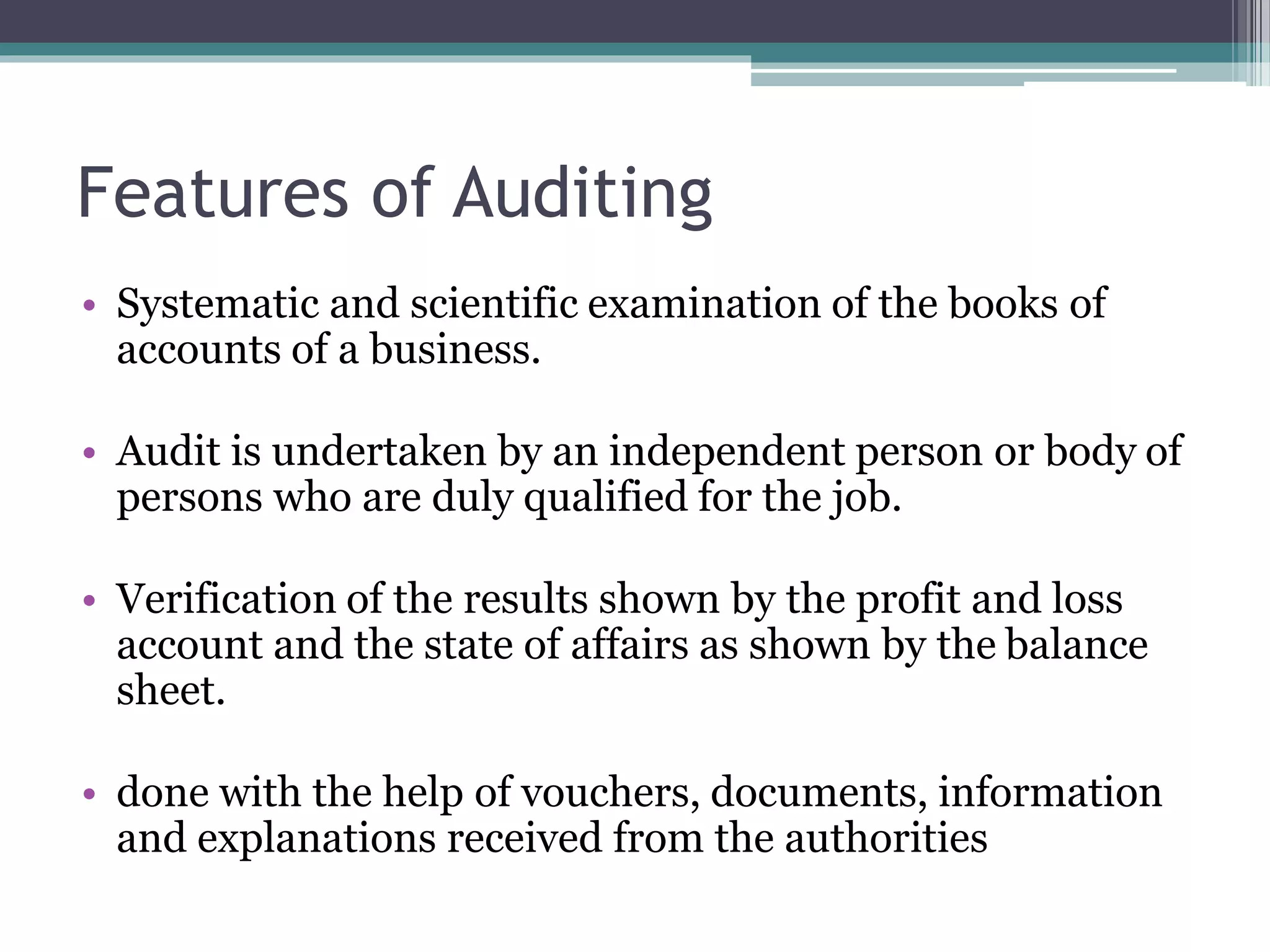

- Key definitions including that auditing is a systematic and independent examination of data, statements, records, operations and performance for a stated purpose.

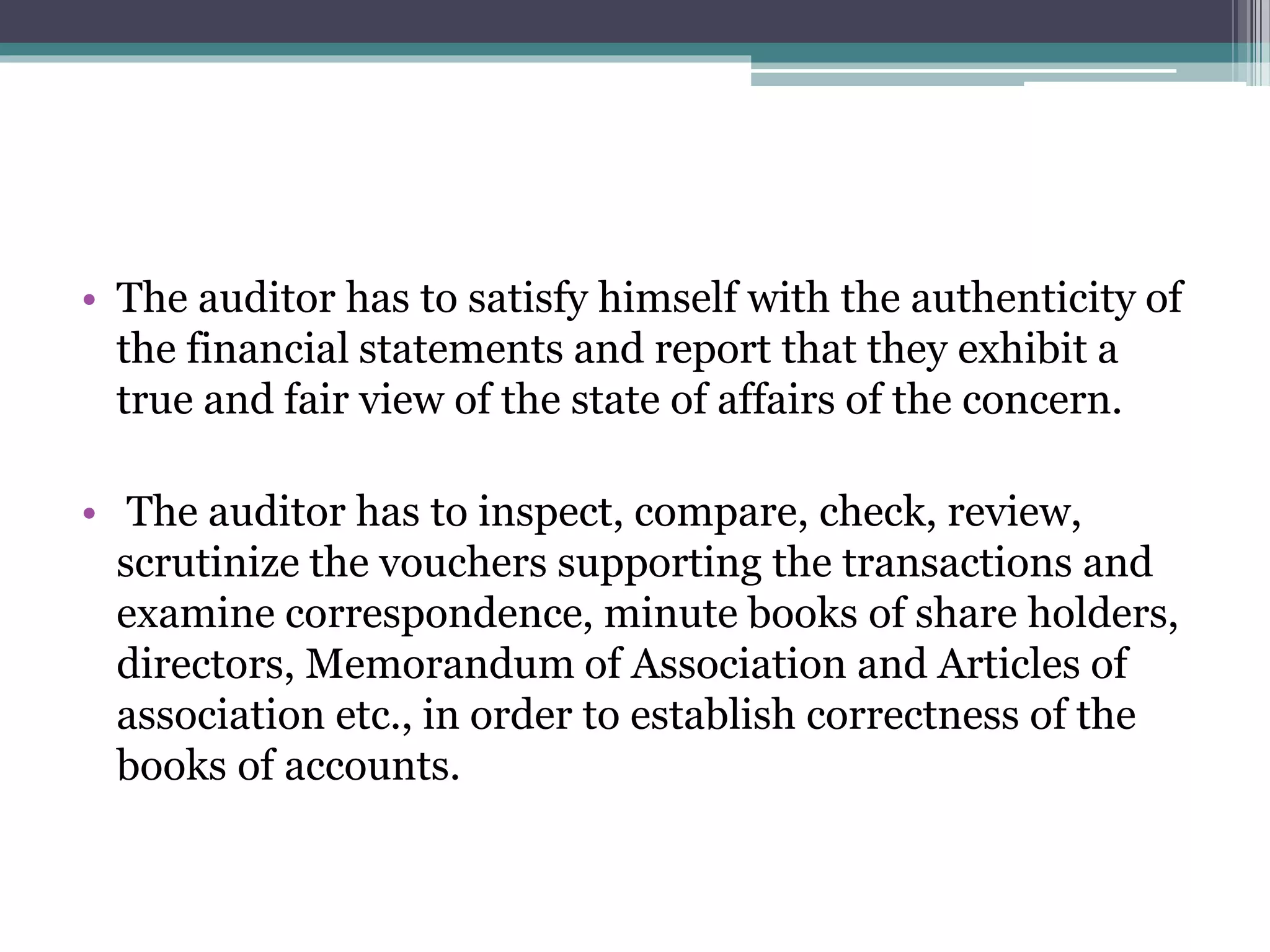

- The features and objectives of auditing including verifying financial statements exhibit a true and fair view, and expressing an opinion on the statements.

![AUDIT REPORT [ AUDITING ]](https://cdn.slidesharecdn.com/ss_thumbnails/auditingtypesofauditreport-210303052610-thumbnail.jpg?width=640&height=640&fit=bounds)