Meaning & Definitionof

Accounting

Introduction

Barter System – In this system product was exchanged against

product or product was exchanged against service

Definition of Accounting –

“Accounting is an art of recording, classifying and

summarizing in a significant manner and in terms of money,

transactions and events which are in part at least of a

financial character and interpreting the result thereof.”

“It is a service activity. Its function is to provide quantitative

information, primarily financial in nature, about economic

entities, that is intended to be useful in making economic

decisions.”

3.

Characteristics of Accounting

•I M R C S A C H

Identification of financial transactions & events

• It involves the identification of those transactions, which are of a financial nature

and relate to the organisation.

Money as medium of exchange

• Only those business transactions and events, which can be quantified or measured

in monetary terms, are considered.

Recording

• Recording is the process of entering business transactions of financial character in

the books of original entry. Once the economic events are identified and measured in financial

terms, these are recorded in books of accounts in monetary terms and in a chronological

order.

Classifying

• It can be defined as the process of grouping transactions or entries of one nature

at one place.

4.

Characteristics of Accounting

§Summarising

§ It involves presenting the classified data in a manner which

is understandable and useful to various users of accounting statements.

§ Analysis and interpretation

§ Analysing and interpreting the financial data helps users to make a

meaningful judgment of the profitability and financial position of the

business. It also helps in planning for the future in a better manner.

§ Communicating to users

§ It involves communicating the financial statements to the various users

i.e., management and other internal and external users.

§ Historical Information

§ In accounting all past transactions and events are recorded. Accounts

prepared on the basis of historical information and result.

5.

Advantages of Accounting

Availability of accounting information

To know profitability

To know financial status

Tax planning

Valuation of business

Decision making

As an evidence

Comparision with past operations

Moral Control

Corrective measures

6.

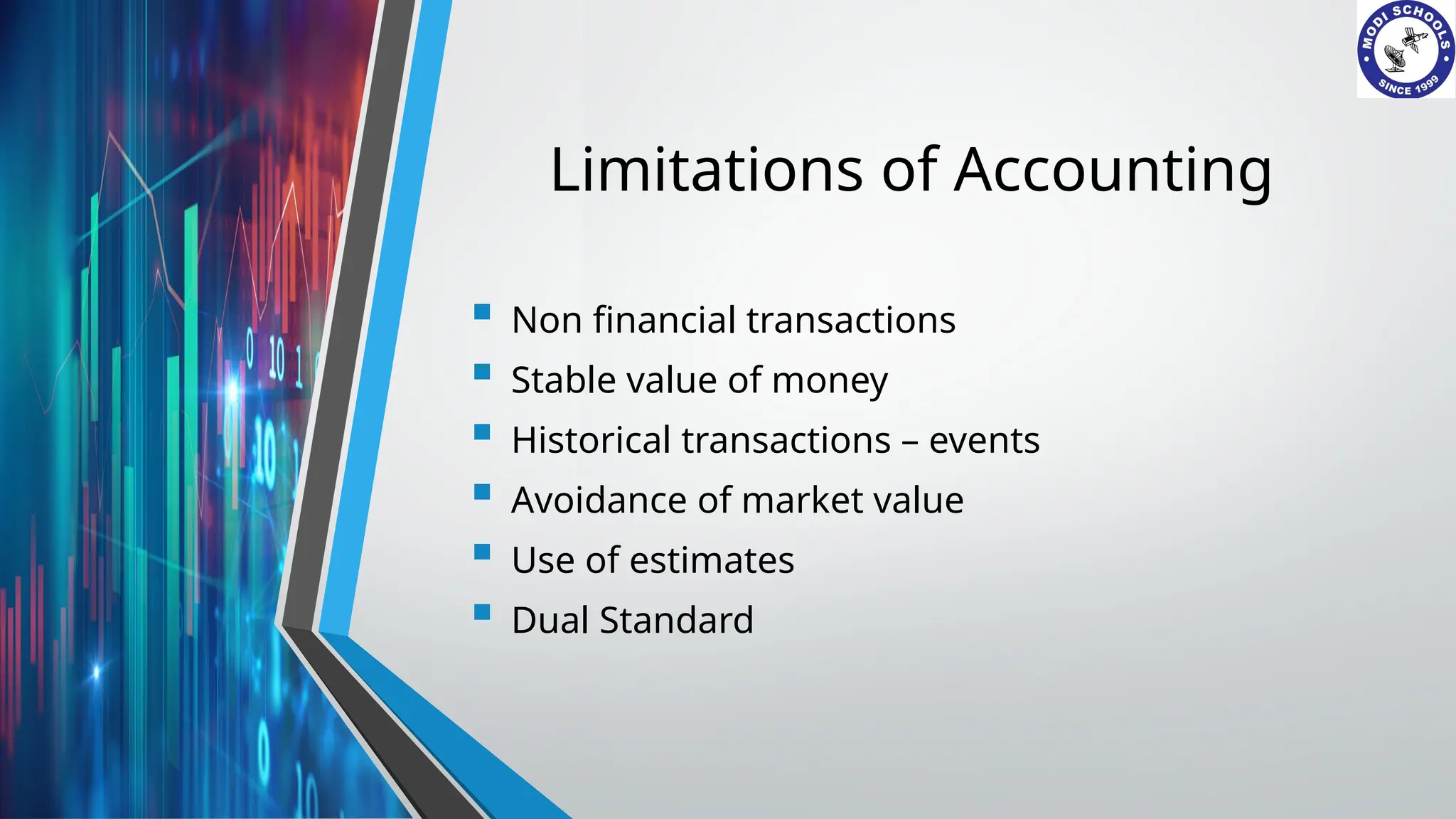

Limitations of Accounting

Non financial transactions

Stable value of money

Historical transactions – events

Avoidance of market value

Use of estimates

Dual Standard

7.

Accountin

g as a

Language

of

business

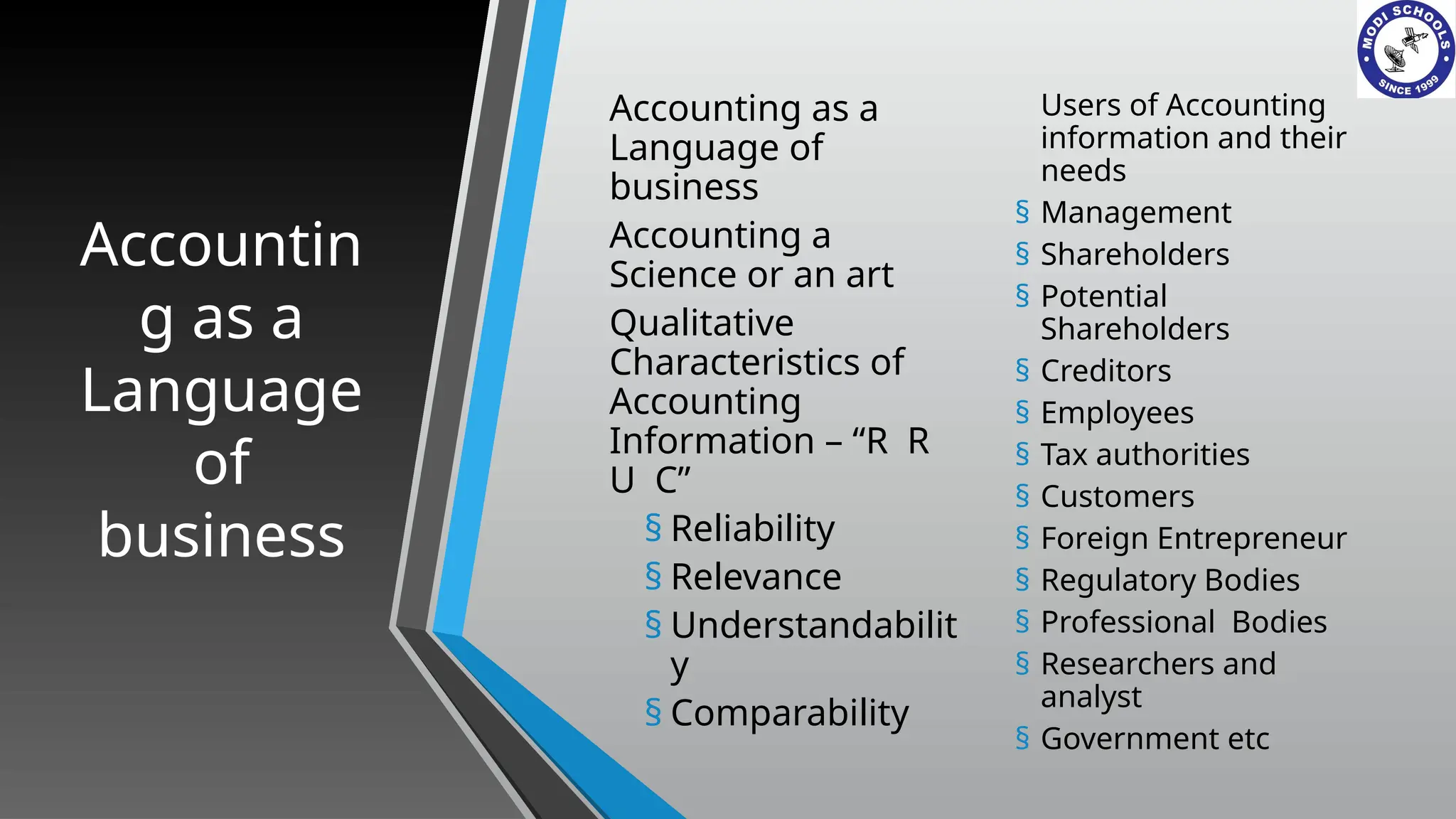

Accountingas a

Language of

business

Accounting a

Science or an art

Qualitative

Characteristics of

Accounting

Information – “R R

U C”

§ Reliability

§ Relevance

§ Understandabilit

y

§ Comparability

Users of Accounting

information and their

needs

§ Management

§ Shareholders

§ Potential

Shareholders

§ Creditors

§ Employees

§ Tax authorities

§ Customers

§ Foreign Entrepreneur

§ Regulatory Bodies

§ Professional Bodies

§ Researchers and

analyst

§ Government etc

8.

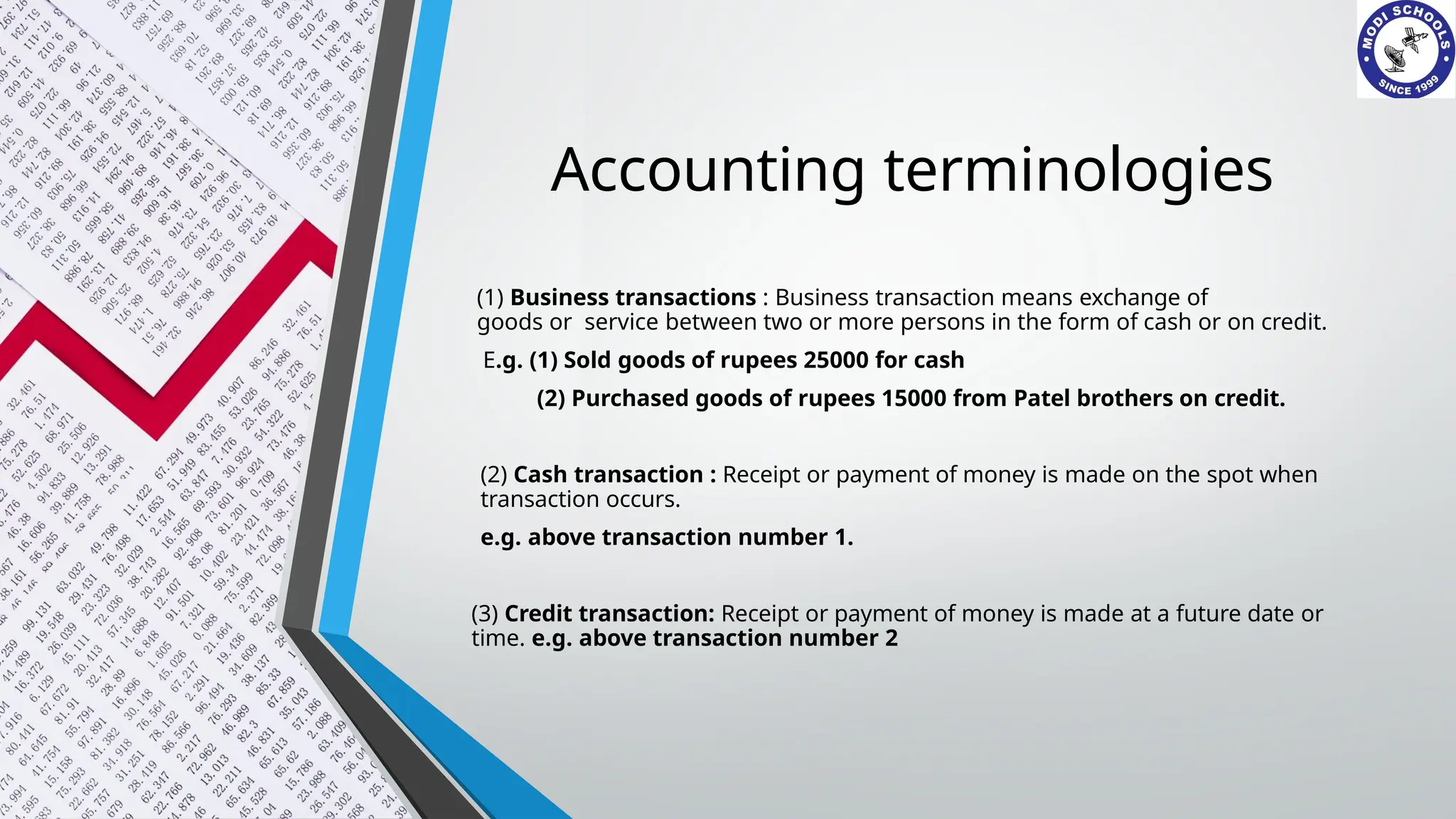

Accounting terminologies

(1) Businesstransactions : Business transaction means exchange of

goods or service between two or more persons in the form of cash or on credit.

E.g. (1) Sold goods of rupees 25000 for cash

(2) Purchased goods of rupees 15000 from Patel brothers on credit.

(2) Cash transaction : Receipt or payment of money is made on the spot when

transaction occurs.

e.g. above transaction number 1.

(3) Credit transaction: Receipt or payment of money is made at a future date or

time. e.g. above transaction number 2

9.

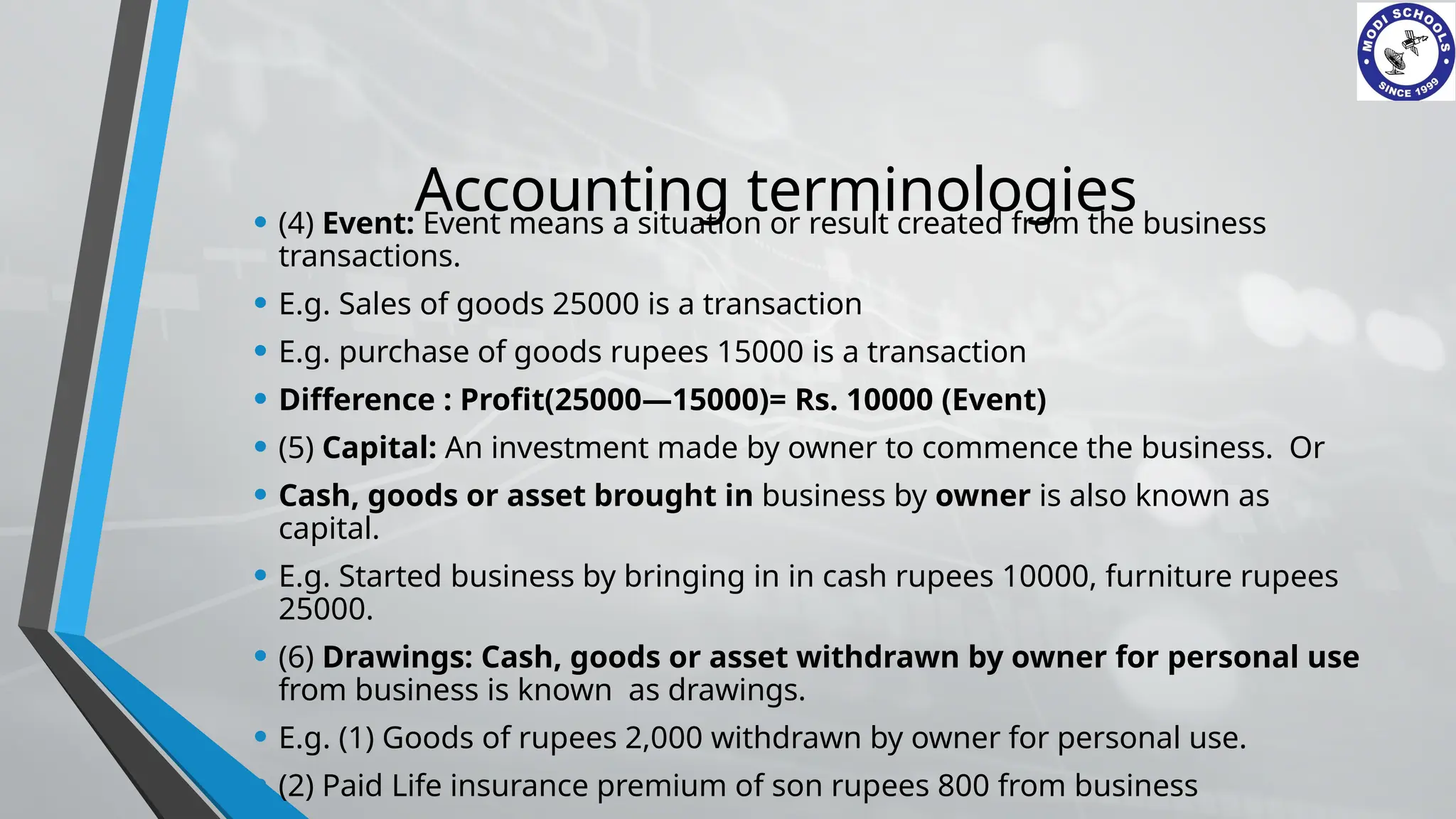

Accounting terminologies

• (4)Event: Event means a situation or result created from the business

transactions.

• E.g. Sales of goods 25000 is a transaction

• E.g. purchase of goods rupees 15000 is a transaction

• Difference : Profit(25000—15000)= Rs. 10000 (Event)

• (5) Capital: An investment made by owner to commence the business. Or

• Cash, goods or asset brought in business by owner is also known as

capital.

• E.g. Started business by bringing in in cash rupees 10000, furniture rupees

25000.

• (6) Drawings: Cash, goods or asset withdrawn by owner for personal use

from business is known as drawings.

• E.g. (1) Goods of rupees 2,000 withdrawn by owner for personal use.

• (2) Paid Life insurance premium of son rupees 800 from business

10.

Accounting terminologies

(7) Liability:Any amount payable by the business for credit purchase of goods or assets or amount payable for

borrowed money is known as a liability.

E.g. (1) purchased goods of rupees 18000 on credit from Raj traders.

E.g. (2) purchased a laptop of rupees 35000 from IBM company for one month credit.

Internal liabilities: The liability of the business towards owner (Capital) is known as internal Liability.

External liabilities: The liabilities of the business towards third party other than owner is known as external

Liability

E.g. Rent rupees 20000 become payable to landlord.

(10) Current liabilities: The liabilities which is to be paid within the duration of one year are known as current

liabilities or short term liabilities.

E.g. amount payable to supplier of goods and service providers

(11) Non current liabilities: The liabilities which is to be paid Within the duration of more than one year is

known as non current liabilities or long term liabilities.

E.g. amount payable for borrowed loan

11.

Accounting terminologies

(12) Assets:Asset means any such tangible or intangible product or item which is of ownership of

Business and has economic value.

E.g. land-building, plant-machine, Goodwill, patent , trademark, copyright, stock of goods, cash

balance

(13) Non current asset : The assets which are long term useful without changing its form are known

as non current or fixed assets

E.g. land-building, plant-machines, computer etc.

(14) Current assets: The assets which can be converted into cash within one year is known a current

assets.

E.g. Cash balance, bank balance, stock of goods, debtors, bills receivables etc.

(15) Tangible assets: The assets which can be seen and touch are known as tangible assets.

E.g. land-building, plant-machines, computer etc.

(16) Intangible assets: The assets which cannot be seen or touched are known as intangible assets.

E.g. Goodwill, patent, trademark, copyright, software etc.

12.

Accounting

terminologies

Real assets: Realassets means assets that have value in reality,

these assets have market price and it can be converted into

cash.

E.g. Any of the assets which are discussed earlier.

Fictitious Assets: Fictitious assets do not have physical existence.

They do not have any realisable value in the market. Actually

these are huge expenses the benefit of which is going to receive

by the firm for a long time.

E.g. Advertisement campaign expenses.

Receipts (Income) : When money is received due to sales of goods

or service or assets are known as receipts or incomes.

Capital receipts: When money is received due to Sales of any

asset or borrowing loan are known as capital receipts or

income. This receipt is not received regularly

E.g. Sold old furniture for cash Rs. 3000

13.

Accounting terminologies

Revenuereceipts: When money is received due to sales of goods or providing other

services is known as revenue receipts. These receipts are regular in nature.

E.g. Income of sales of goods, commission received, rent received, discount

received, interest received, sale of scrap etc.

Payments (Expenses): When money is paid for purchase of goods or service or assets

are known as payments or expenses.

Capital payments: When money is paid for purchase of any assets is known as capital

payments or expenses. This payment is not paid regularly.

E.g. Purchased a computer of Rs. 20000 for business.

Revenue payments: When money is paid for purchase of goods or services is known as

revenue payments or expenses. These payments are regular in nature

E.g. payment of salary, wages, telephone bill, advertisement expense, purchase of

goods expense etc.

14.

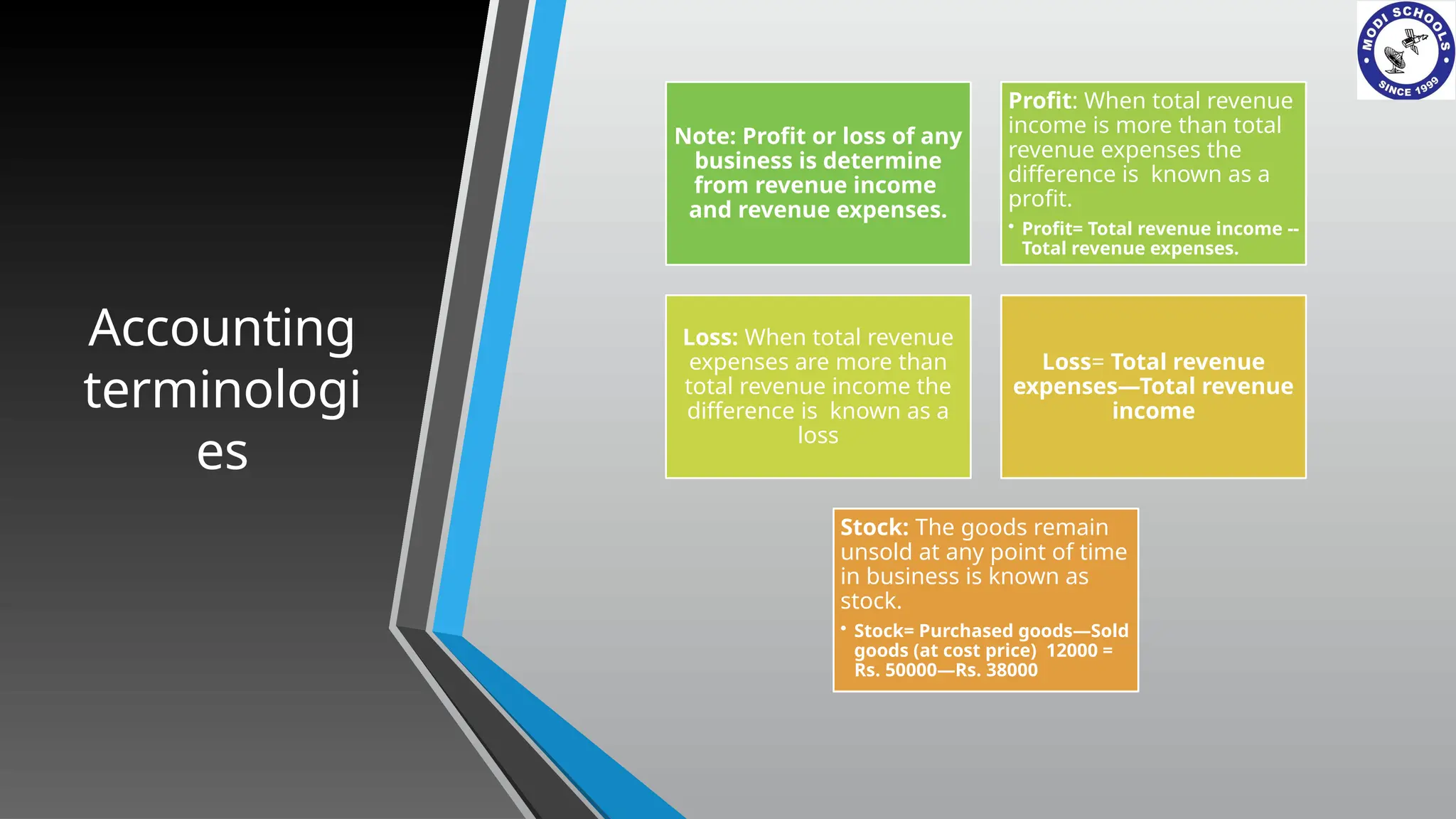

Accounting

terminologi

es

Note: Profit orloss of any

business is determine

from revenue income

and revenue expenses.

Profit: When total revenue

income is more than total

revenue expenses the

difference is known as a

profit.

• Profit= Total revenue income --

Total revenue expenses.

Loss: When total revenue

expenses are more than

total revenue income the

difference is known as a

loss

Loss= Total revenue

expenses—Total revenue

income

Stock: The goods remain

unsold at any point of time

in business is known as

stock.

• Stock= Purchased goods—Sold

goods (at cost price) 12000 =

Rs. 50000—Rs. 38000

15.

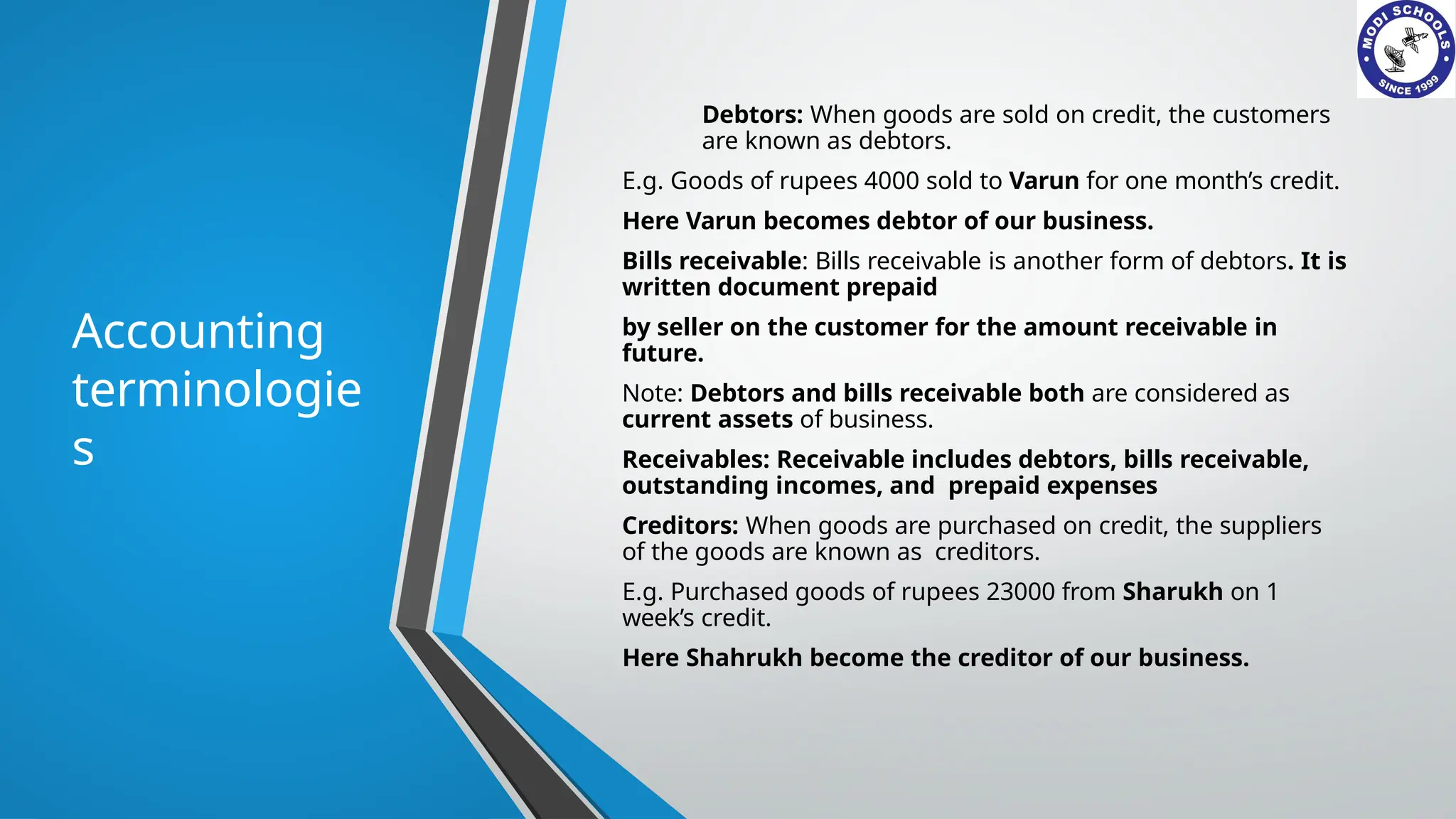

Accounting

terminologie

s

Debtors: When goodsare sold on credit, the customers

are known as debtors.

E.g. Goods of rupees 4000 sold to Varun for one month’s credit.

Here Varun becomes debtor of our business.

Bills receivable: Bills receivable is another form of debtors. It is

written document prepaid

by seller on the customer for the amount receivable in

future.

Note: Debtors and bills receivable both are considered as

current assets of business.

Receivables: Receivable includes debtors, bills receivable,

outstanding incomes, and prepaid expenses

Creditors: When goods are purchased on credit, the suppliers

of the goods are known as creditors.

E.g. Purchased goods of rupees 23000 from Sharukh on 1

week’s credit.

Here Shahrukh become the creditor of our business.

16.

Accounting terminologies

Payables: Includescreditors, bills payable, outstanding expense

and income received in advance.

Voucher: Voucher is a written evidence of transaction in business.

E.g. purchase bill, sales bill, pay in slip, cheque, receipt received,

salary voucher, other expenses voucher

etc.

Bad debts: The amount of credit sales which cannot be recovered

from debtors is known as bad

debts. Bad debts is a loss for business

Bad debts return/ recovered: if any amount recovered from the

debtors which is recorded as a bad debts earlier is known as bad

debt recovered. It is considered as income for business