Download to read offline

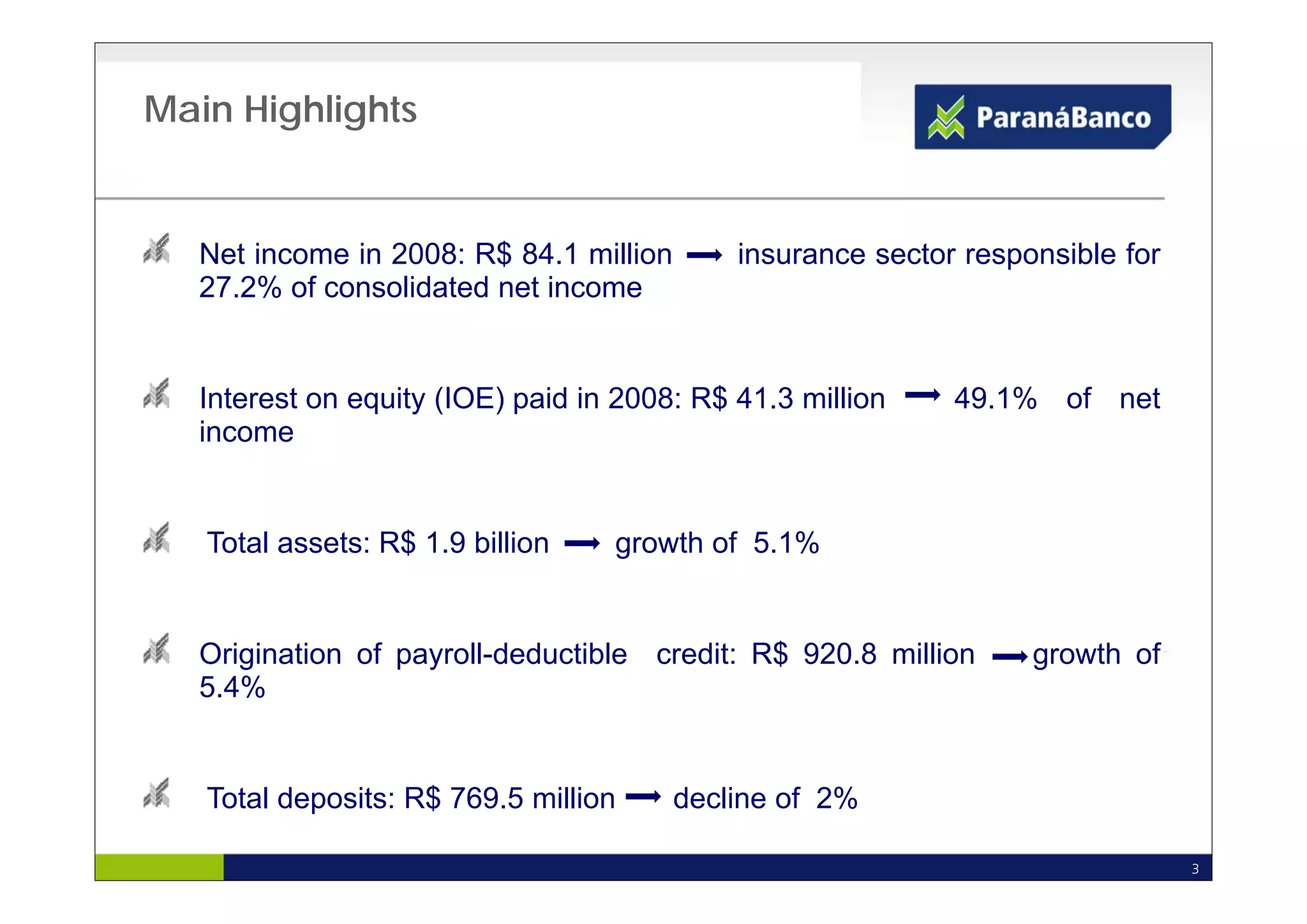

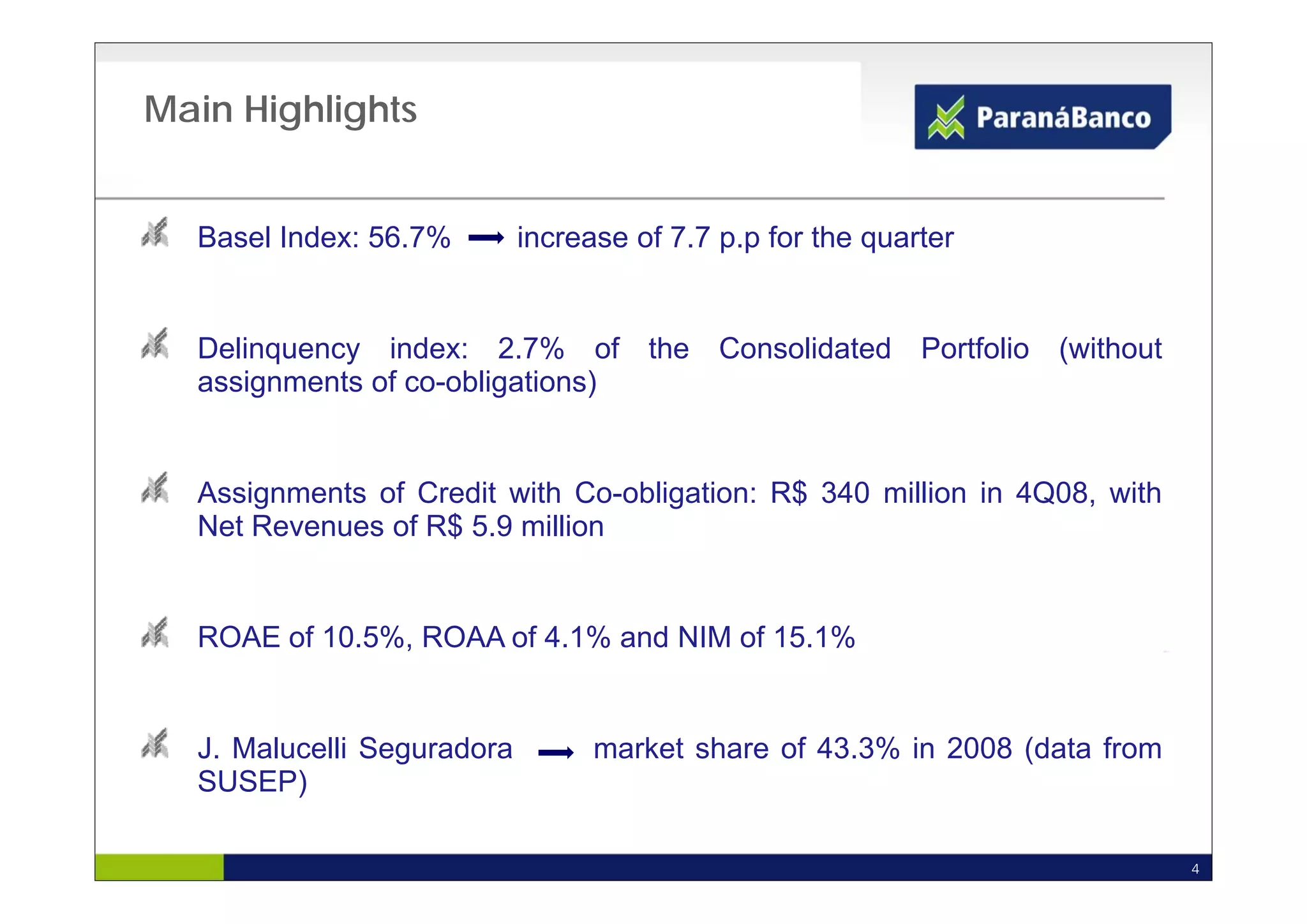

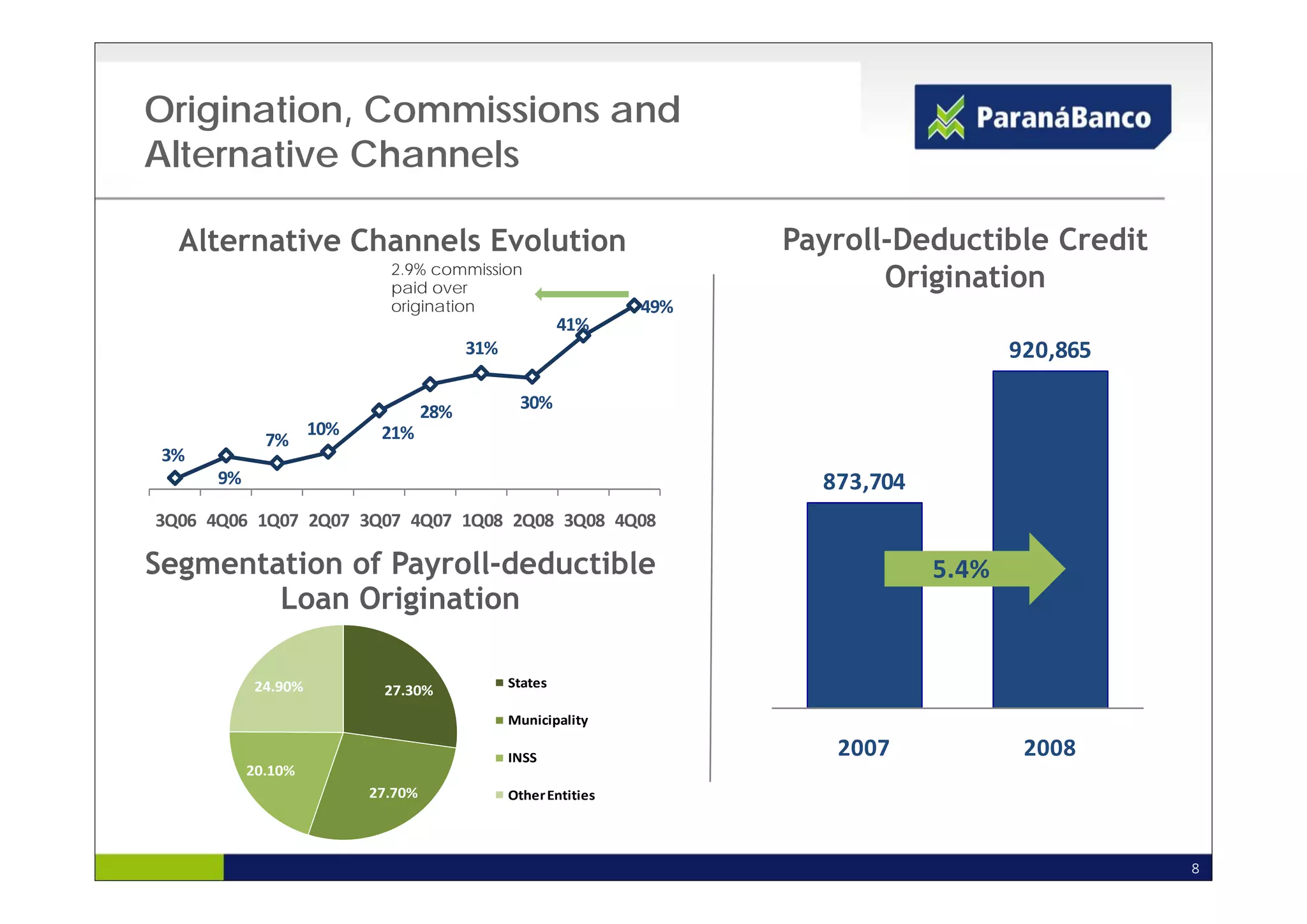

Paraná Banco reported its financial results for 4Q08 and full year 2008. Key highlights include: - Net income of R$84.1 million in 2008, with the insurance sector contributing 27.2% - Total assets of R$1.9 billion, growing 5.1% - Origination of payroll-deductible