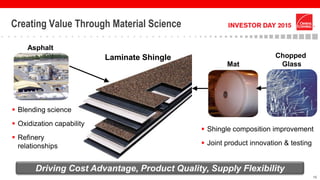

This document discusses Owens Corning's Roofing and Asphalt business. It notes that the business operates in a $10 billion residential roofing market, has a leading brand, and generates mid-teen operating margins on average. The business has experienced weaker market conditions recently but expects modest growth going forward, driven by components which are growing at attractive margins. It also has a national manufacturing footprint and differentiates itself through products, material science expertise, and a strong distribution network.