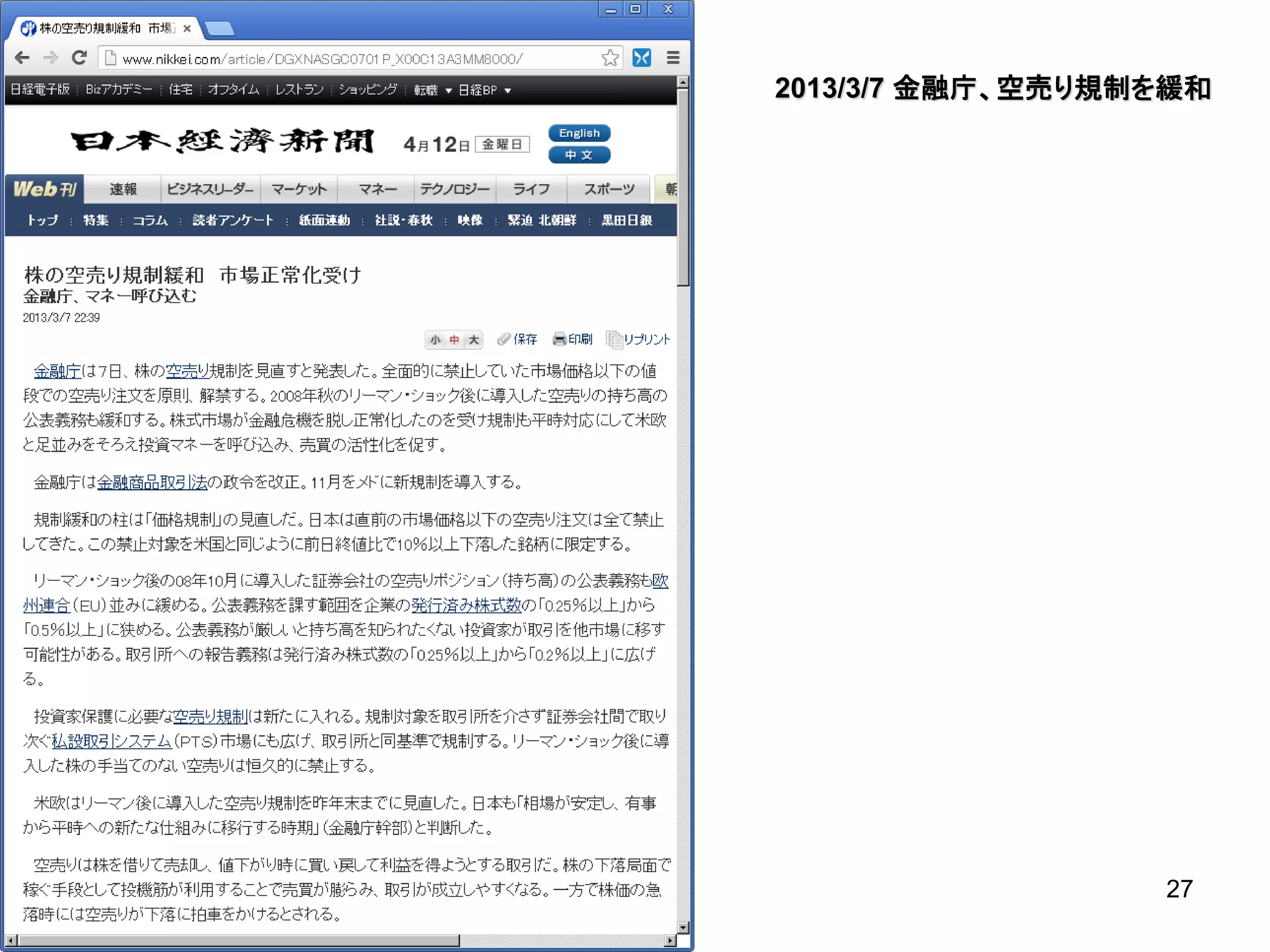

参考文献 (1/4)

* 水田孝信,八木勲,和泉潔(2012)

現実の価格決定メカニズムを考慮した人工市場の設定評価手法の開発,人工知能学会論文誌,27,6,320-327(2012)

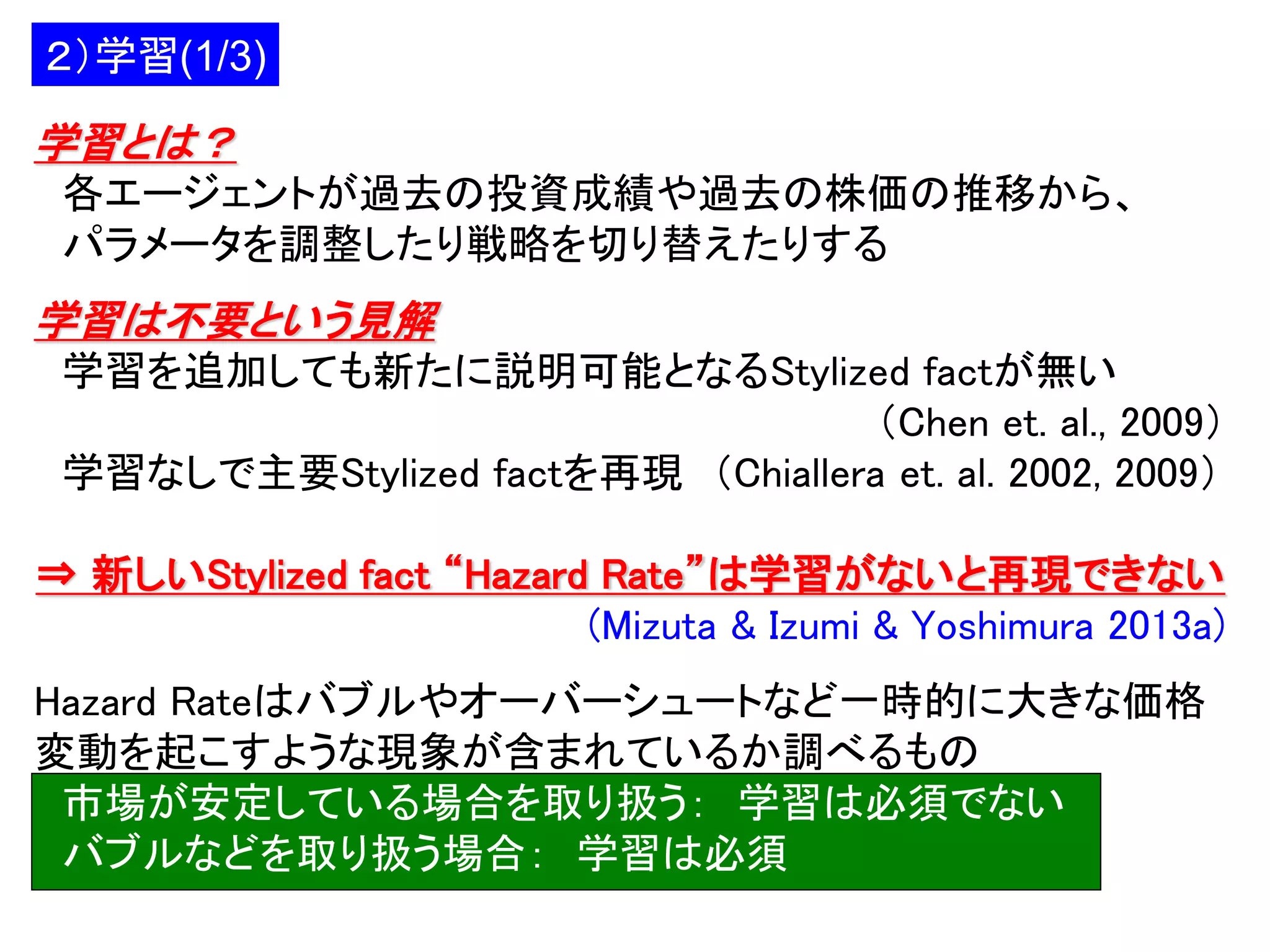

* Mizuta, T., Izumi, K., Yoshimura, S. (2013a)

Price Variation Limits and Financial Market Bubbles: Artificial Market Simulations with Agents' Learning Process, IEEE Symposium

Series on Computational Intelligence, Computational Intelligence for Financial Engineering and Economics (CIFEr), 2013.

http://www.slideshare.net/mizutata/cifer2013 (slide)

* Mizuta, T., Izumi, K., Yagi, I., Yoshimura, S. (2013b)

Design of Financial Market Regulations against Large Price Fluctuations using by Artificial Market Simulations, Journal of

Mathematical Finance, Scientific Research Publishing, Vol.3, No. 2A.

http://www.scirp.org/journal/PaperInformation.aspx?PaperID=30551

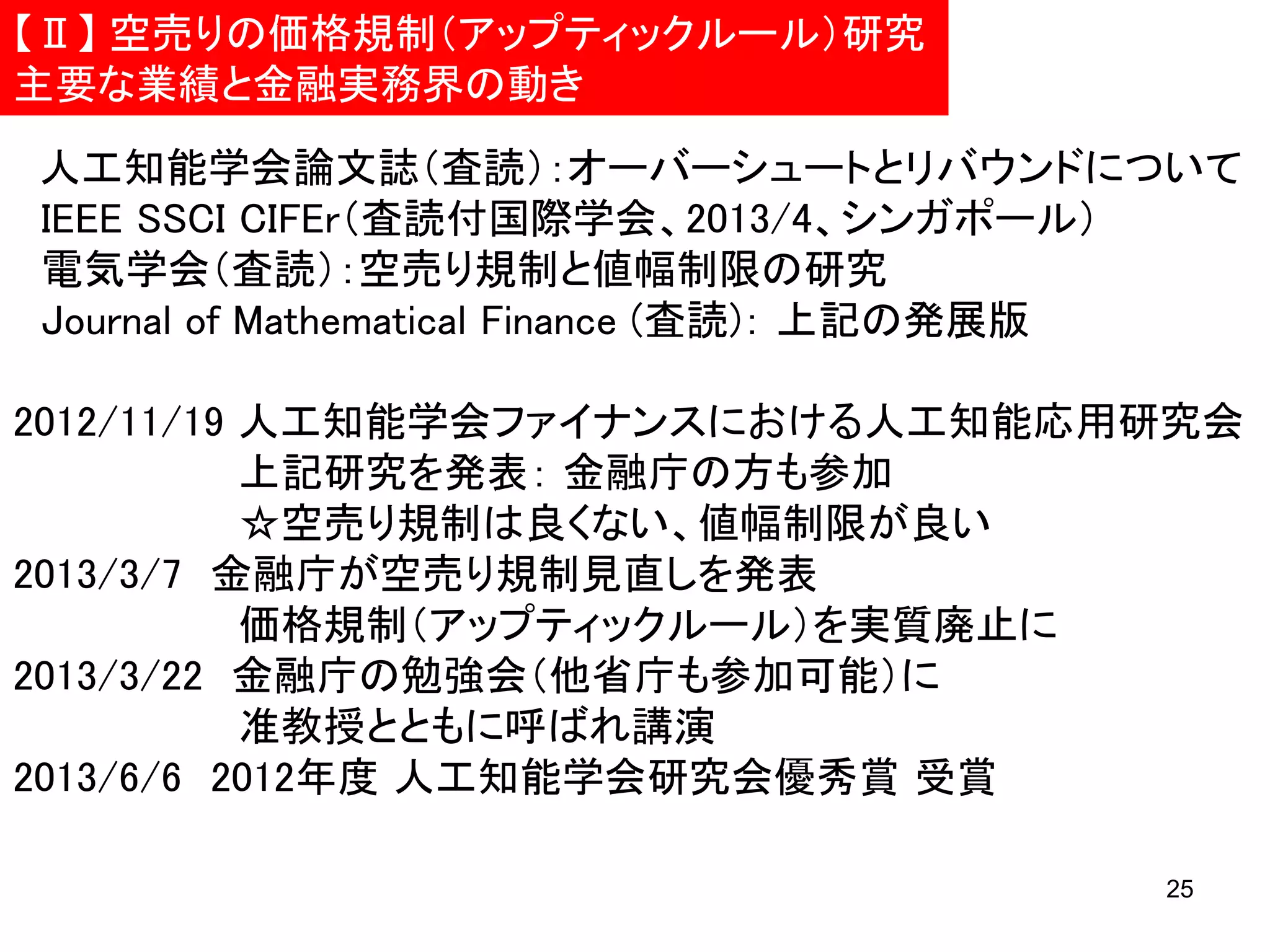

* 水田孝信, 和泉潔, 八木勲, 吉村忍 (2013c)

人工市場を用いた値幅制限・空売り規制・アップティックルールの検証と最適な制度の設計, 電気学会論文誌 論文誌C, Vol. 133, No.9.

* 水田孝信, 早川聡, 和泉潔, 吉村忍 (2013d)

人工市場シミュレーションを用いた取引市場間におけるティックサイズと取引量の関係性分析, JPXワーキング・ペーパー, Vol. 2, 東京

証券取引所.

* Mizuta, T., Hayakawa, S., Izumi, K., Yoshimura, S. (2013e)

Simulation Study on Effects of Tick Size Difference in Stock Markets Competition, The 8th International Workshop on Agent-based

Approach in Economic and Social Complex Systems (AESCS 2013), 2013, http://www.slideshare.net/mizutata/AESCS2013 (slide)

* 水田孝信, 和泉潔, 八木勲, 吉村忍 (2013f)

人工市場を用いた大規模誤発注による市場混乱を防ぐ制度・規制の検証 ~ トリガー式アップティック・ルールを中心に ~, 人工知能

学会 金融情報学研究会, 東京, 10/12.

86

87.

参考文献 (2/4)

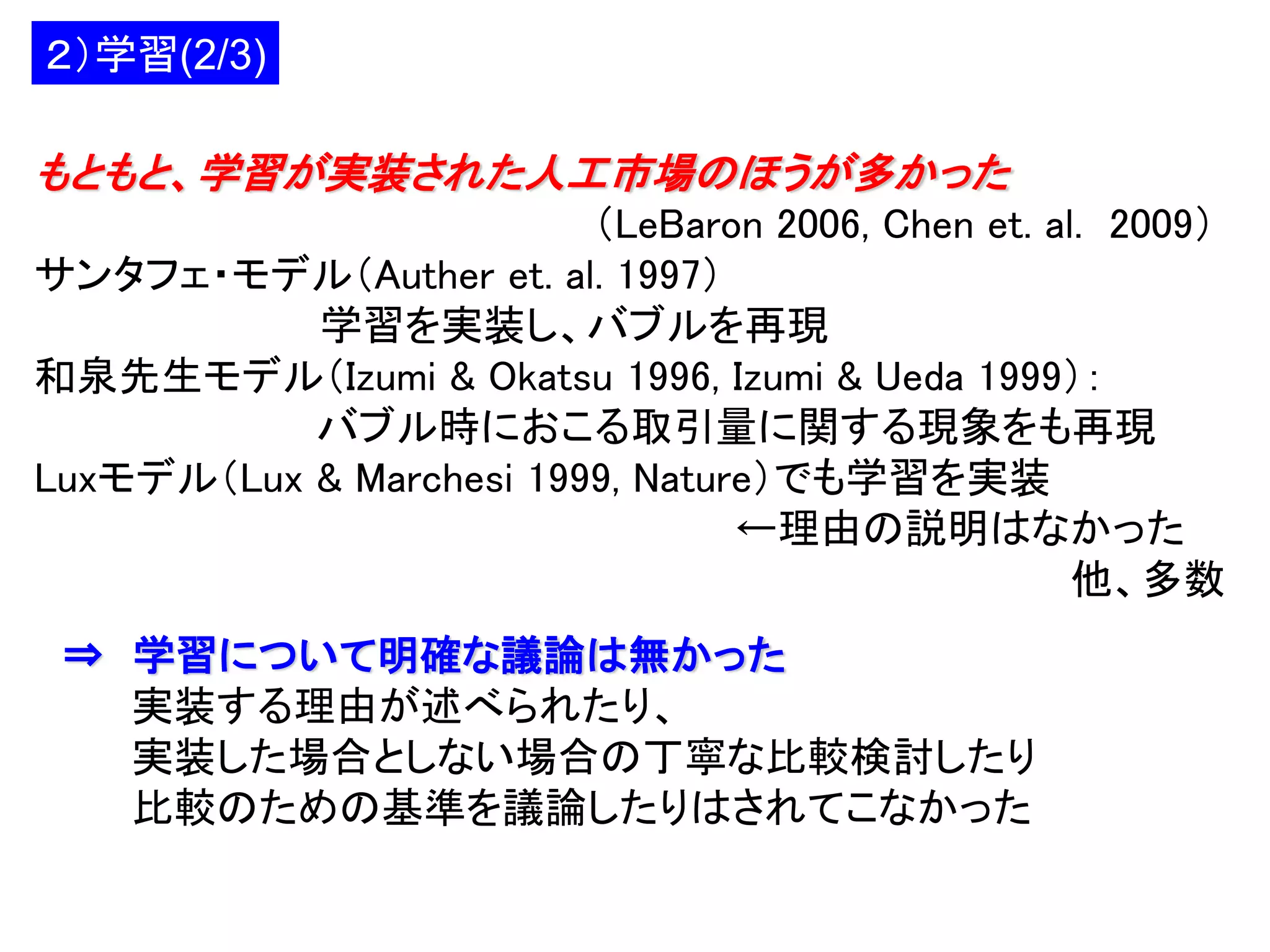

* Arthur,W.B., J.H. Holland, B. Lebaron, R. Palmer and P. Tayler (1997)

Asset Pricing Under Endogenous Expectations in an Artificial Stock Market . In: Arthur, W.B., Durlauf, S., Lane, D. (Eds.), The Economy

as an Evolving Complex System II. Addison-Wesley, Reading, MA, pp. 15–44.

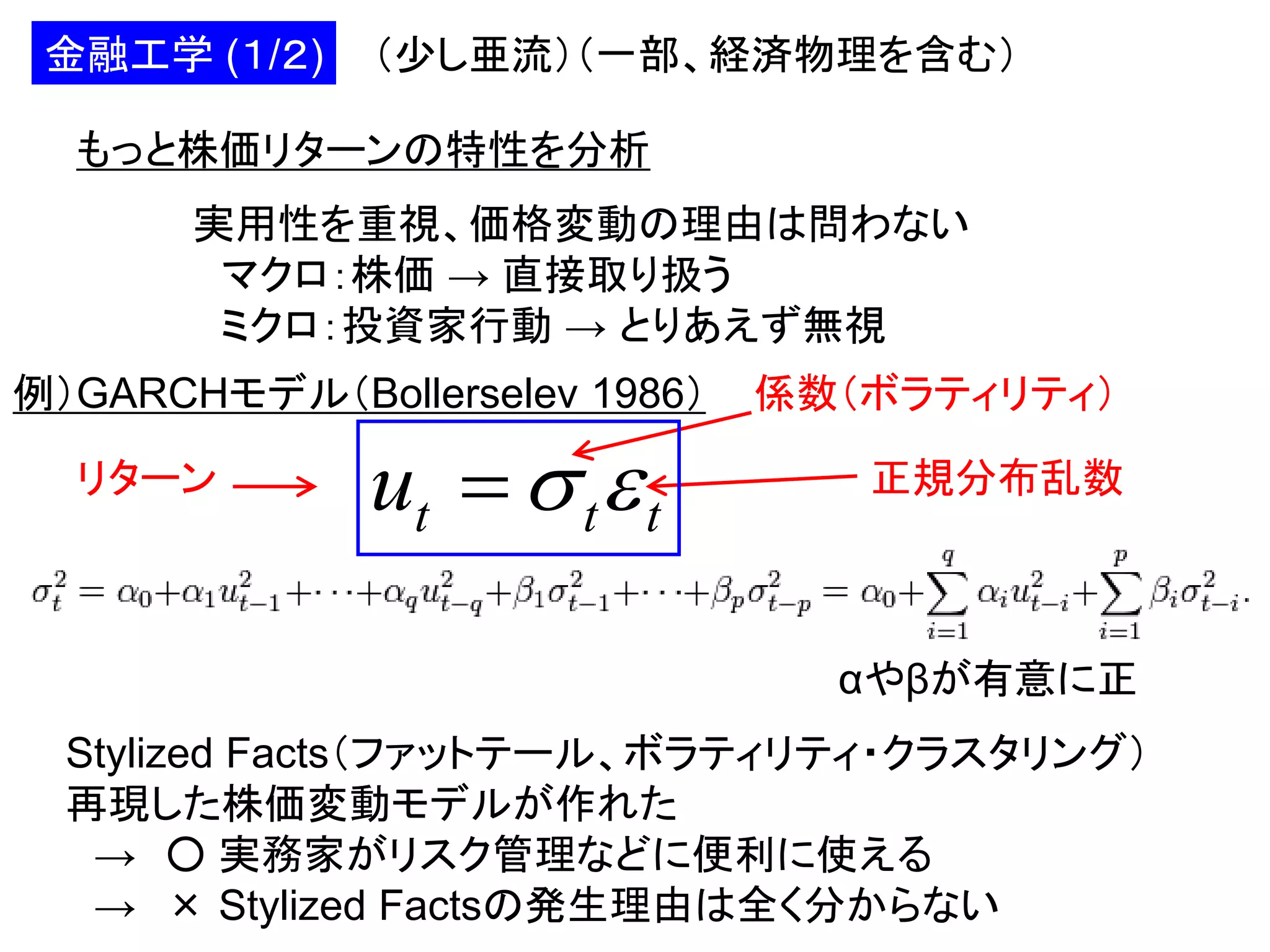

* Bollerslev, T. (1986)

Generalized Autoregressive Conditional Heteroskedasticity, ournal of Econometrics 31, 3, 307-327

* Brock, W., Hommes, C., (1998)

Heterogeneous beliefs and routes to chaos in a simple asset pricing model. Journal of Economics Dynamics and Control 22, 12351274

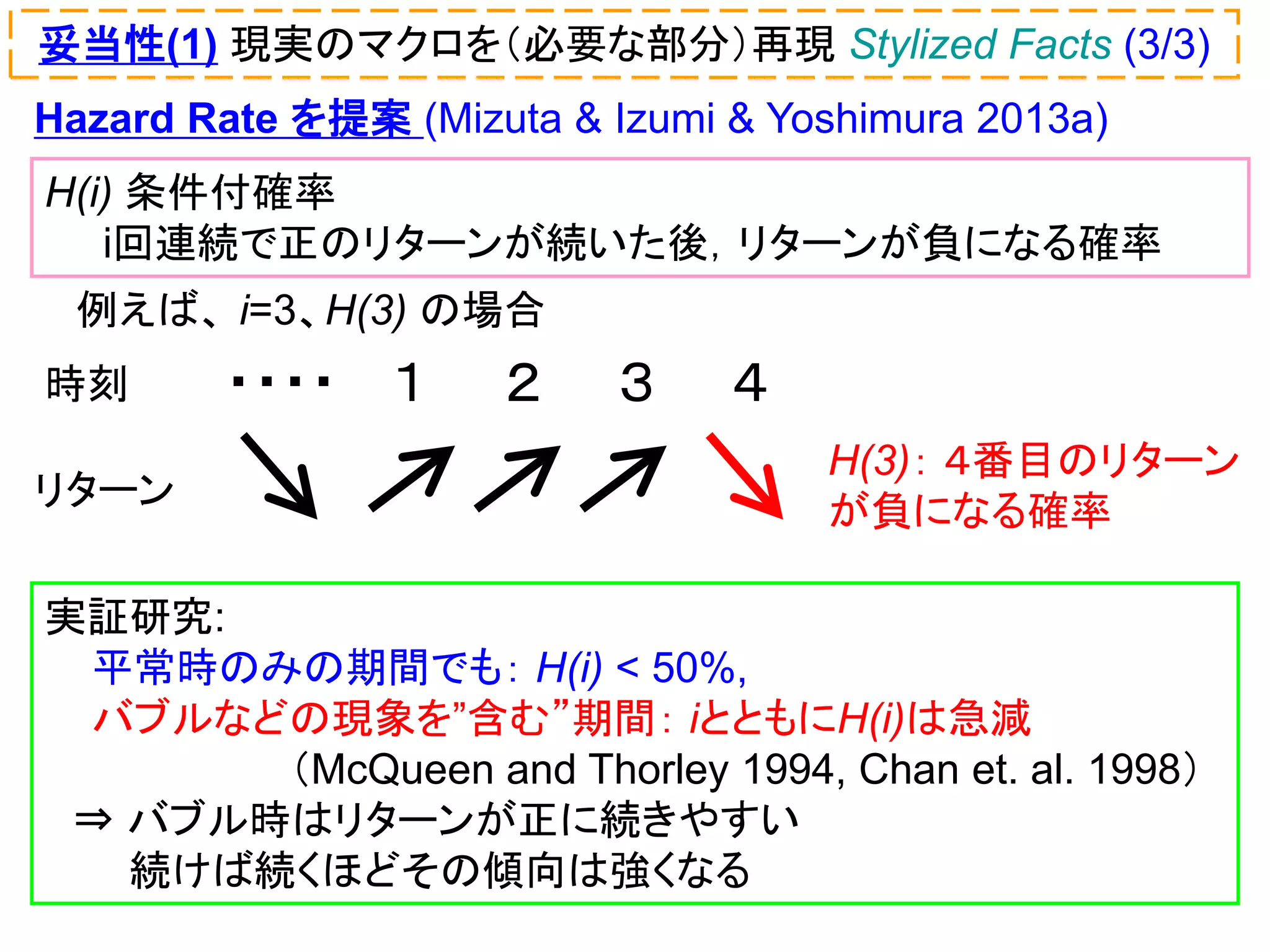

* Chan, K., G. McQueen and S. Thorley (1998)

Are there rational speculative bubbles in Asian stock markets?, Pacific-Basin Finance Journal, 6, 1-2, 125-151

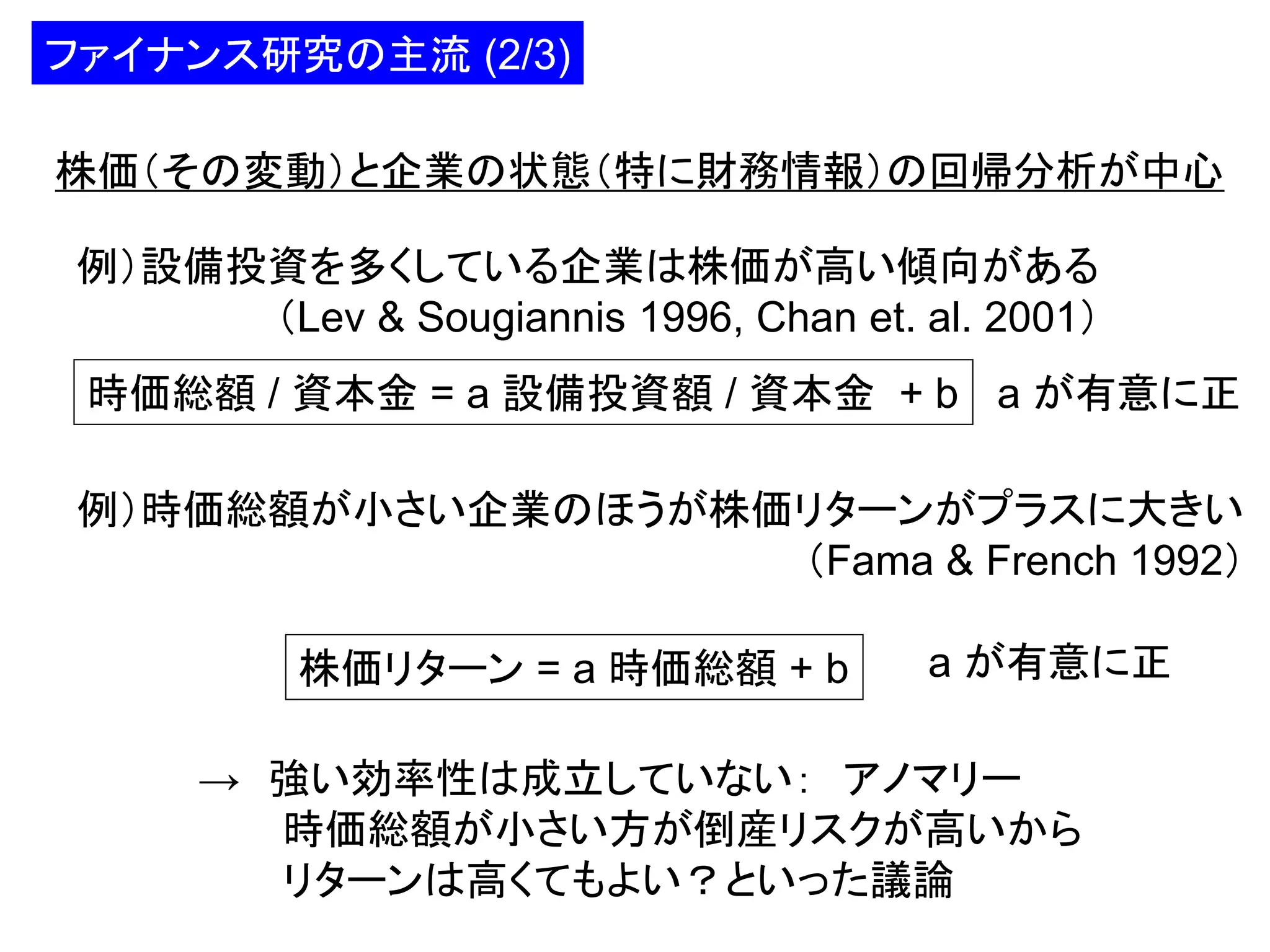

* Chan, L. KC, J. Lakonishok and T. Sougiannis (2001)

The stock market valuation of research and development expenditures, The Journal of Finance, 56, 6, 2431-2456

* Chen, S.H., C.L. Chang and Y.R. Du (2009)

Agent-based economic models and econometrics, Knowledge Engineering Review

* Chiarella C. and G. Iori (2002)

A simulation analysis of the microstructure of double auction markets, Quantitative Finance, 2, 5, 346-353

* Chiarella C., G. Iori and J. Perello (2009)

The impact of heterogeneous trading rules on the limit order book and order?, Journal of Economic Dynamics and Control, 33, 3, 525537

* Cont, R. (2001)

Empirical properties of asset returns: stylized facts and statistical issues, Quantitative Finance , 1, 223-236

* Fama.E.F and K.R. French (1992)

The Cross-Section of Expected Stock Return, Journal of Finance, 47, 427-465

* Friedman M. (1953)

The Case for Flexible Rates, Essays in Positive Economics, University of Chicago Press, Chicago

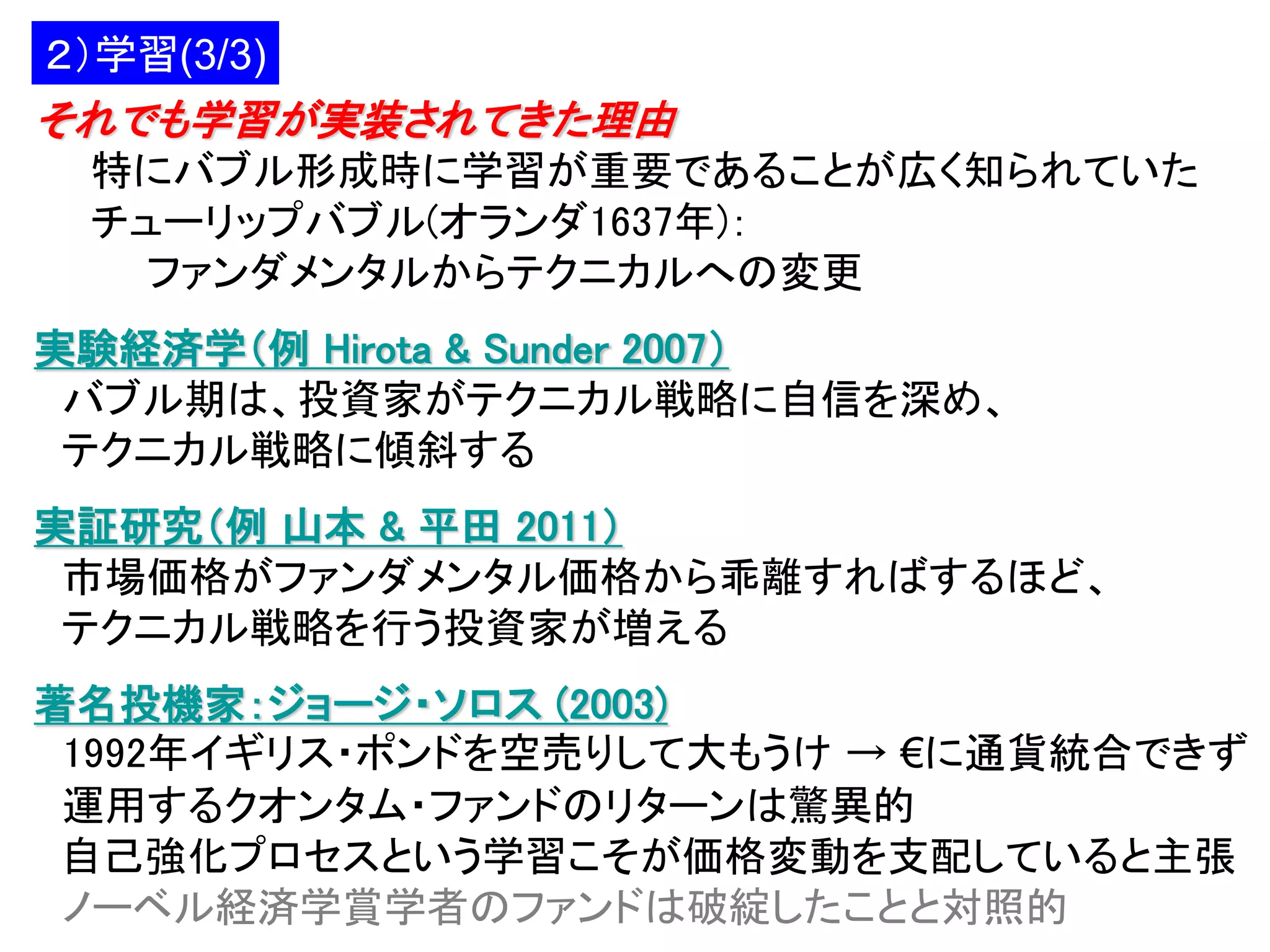

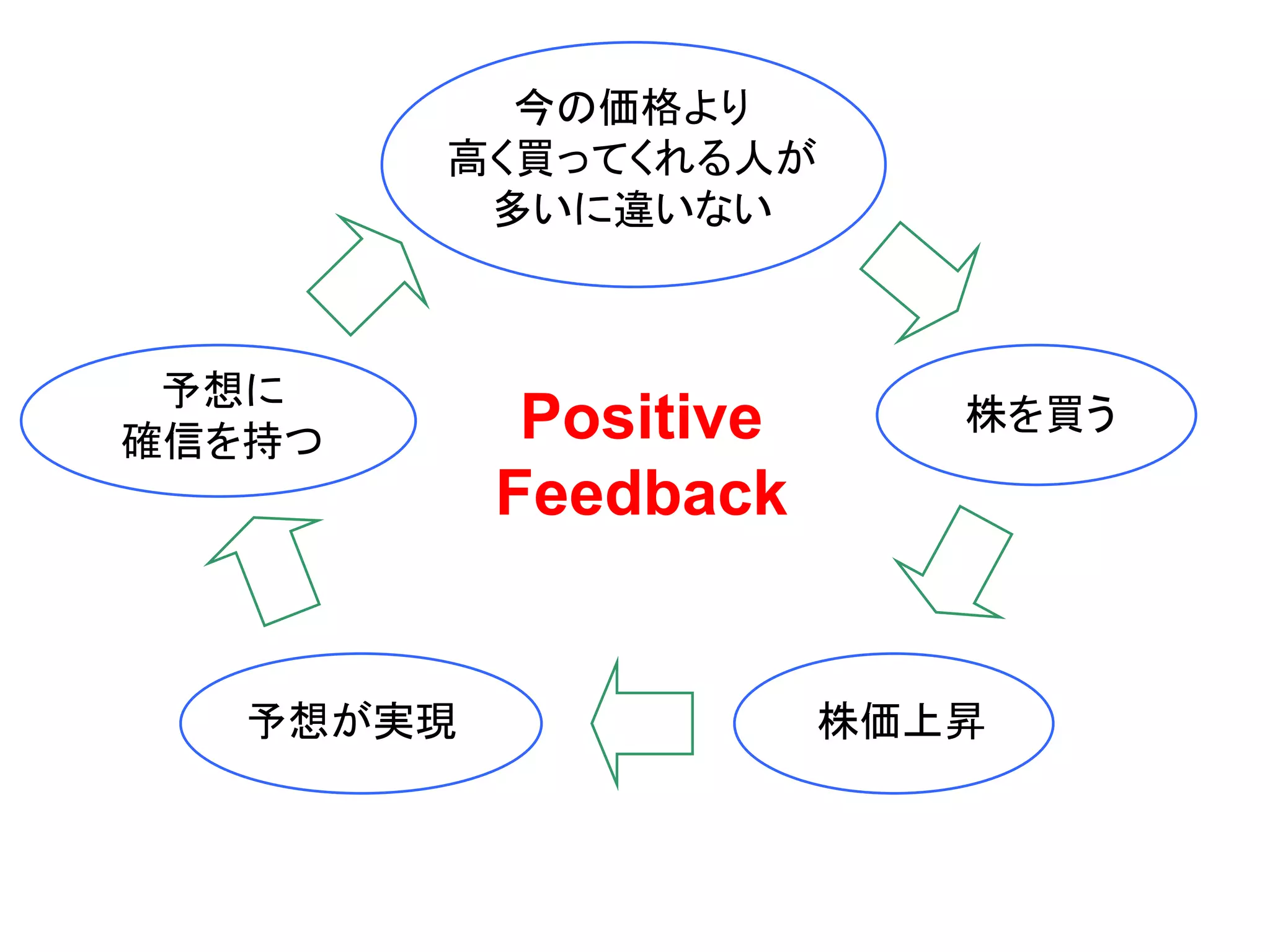

* Hirota, S. and S. Sunder (2007)

Price bubbles sans dividend anchors: Evidence from laboratory stock markets, Journal of Economic Dynamics and Control, 31, 6,

1875-1909

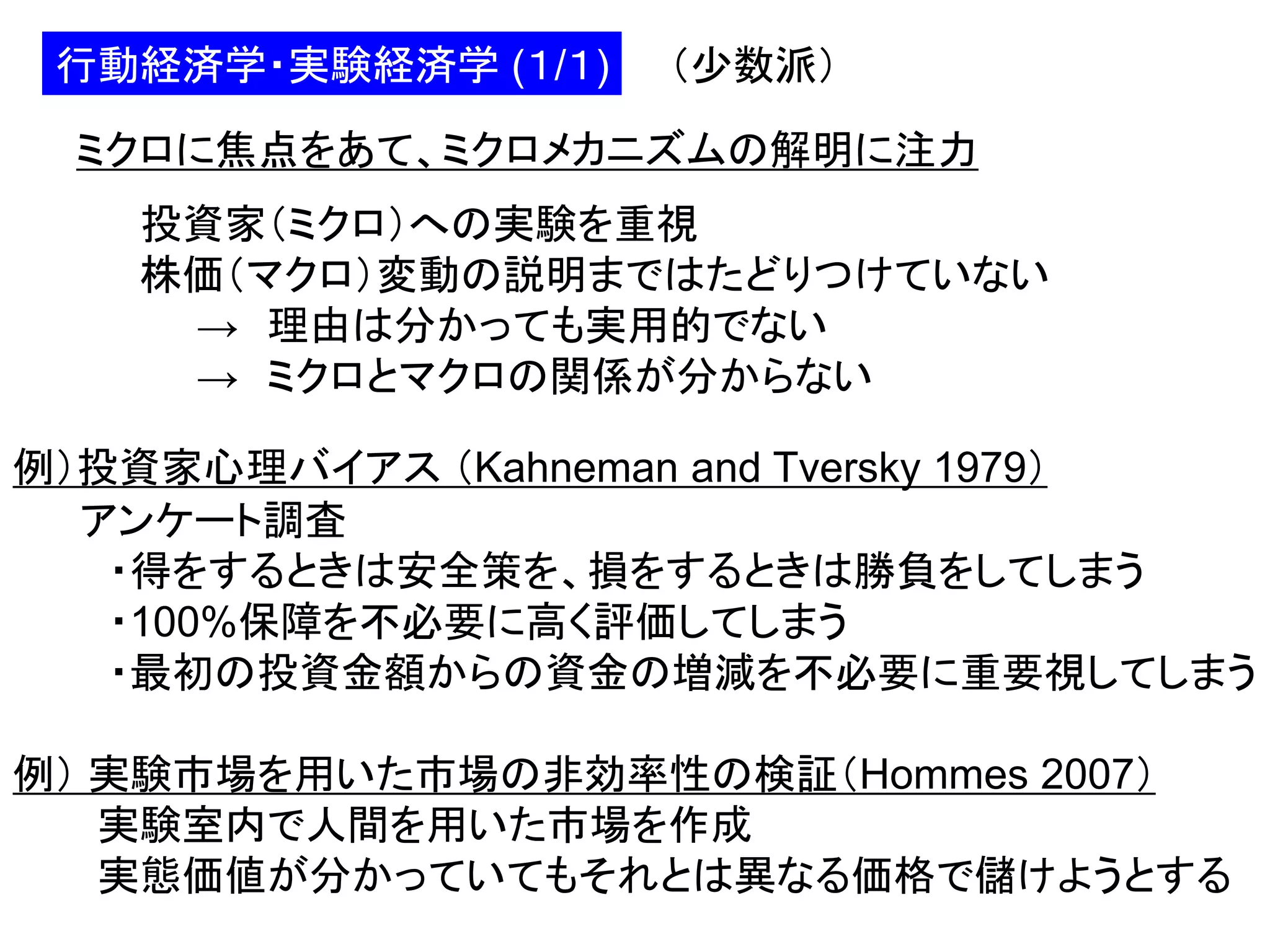

* Hommes, CH (2007)

Bounded rationality and learning in complex markets, eNDEF Working Paper Universiteit van Amsterdam, 7

* Izumi, K. and T. Okatsu (1996)

An artificial market analysis of exchange rate dynamics, Evolutionary Programming V, 27-36

87

88.

参考文献 (3/4)

* Izumi,K. and K. Ueda (1999)

Analysis of dealers' processing financial news based on an artificial market approach, Journal of Computational Intelligence in

Finance, 7, 23-33

* Kahneman, D. and A. Tversky (1979)

Prospect theory: An analysis of decision under risk, Econometrica: Journal of the Econometric Society, 263-291

* LeBaron, B. (2006)

Agent-based computational finance, Handbook of computational economics, 2, 1187-1233

* Lev, B. and T. Sougiannis (1996)

The capitalization, amortization, and value-relevance of R&D, Journal of accounting and economics, 21, 1, 107-138

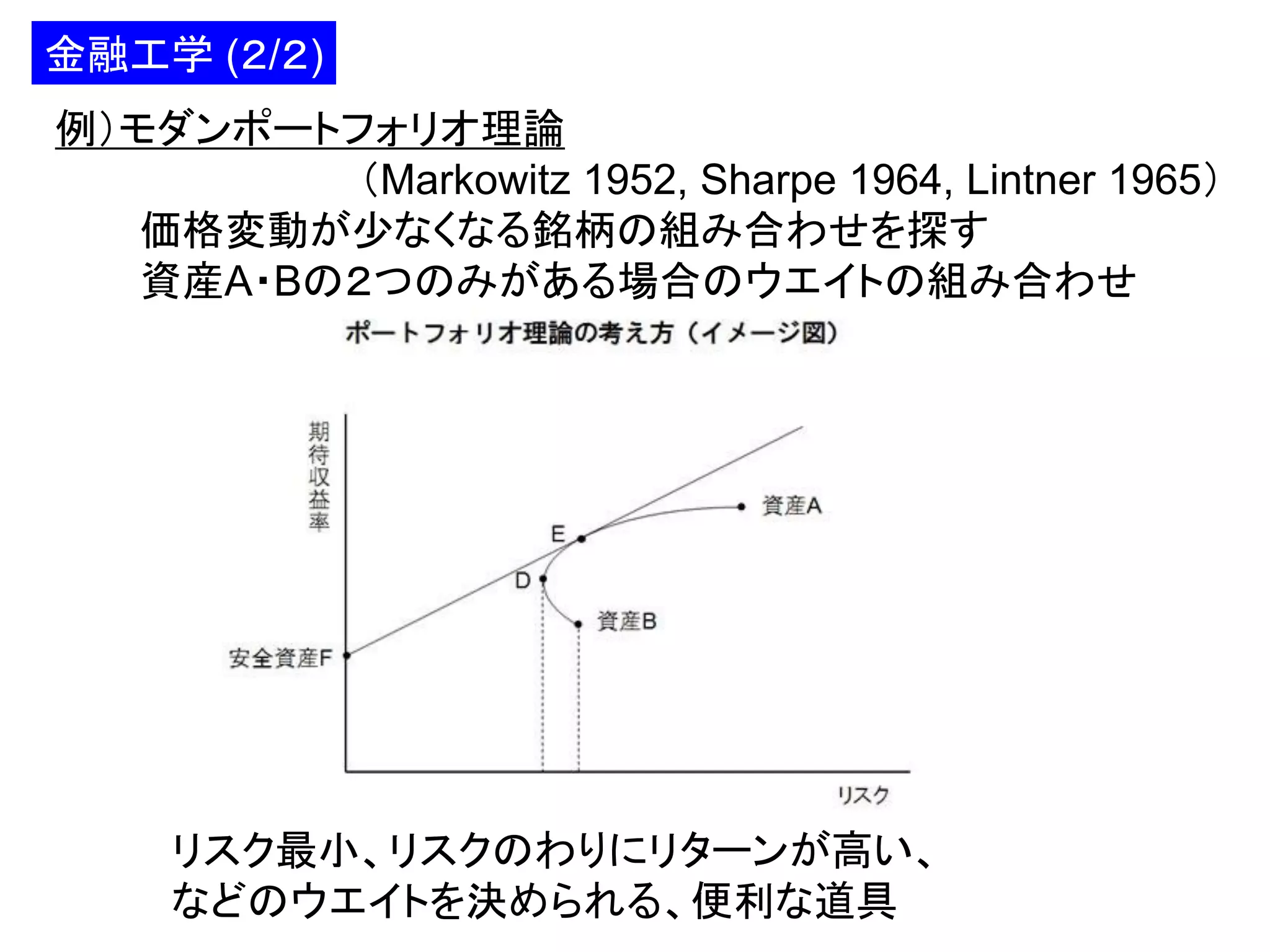

* Lintner, J. (1965)

The Valuation of Risk Assets and the Selection of Risky Investments in Stock Portfolios and Capital Budgets, The Review of

Economics and Statistics, 47, 1, 13-39

* Lux and Marchesi (1999)

Scaling and criticality in a stochastic multi-agent model of a financial market, Nature

* Mandelbrot, B. (1963)

The variation of certain speculative prices, The journal of business, 36, 4, 394-419

* Mandelbrot, B. (1972)

Statistical Methodology for Nonperiodic Cycles: From the Covariance to R/S Analysis, Annals of Economic and Social Measurement,

1, 259-290

* Markowitz, Harry M. (1952)

Portfolio Selection, Journal of Finance, 7, 1, 77-91

* McQueen, G. and S. Thorley (1994)

Bubbles, stock returns, and duration dependence, Journal of Financial and Quantitative Analysis, 29, 3

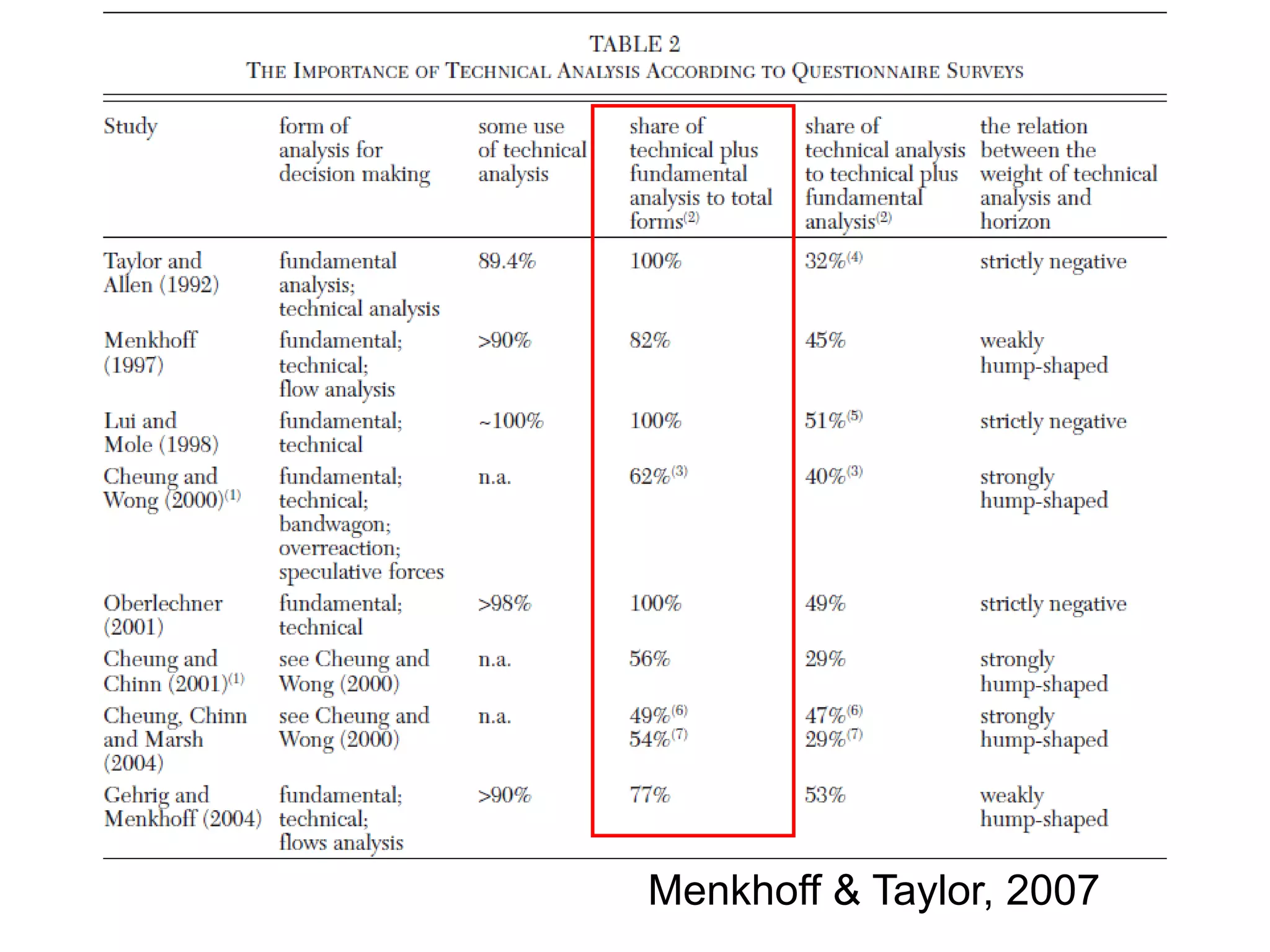

* Menkhoff, L. and M.P.Taylor (2007)

The obstinate passion of foreign exchange professionals: technical analysis, Journal of Economic Literature, 45, 4, 936-972

* Sewell, M. (2006)

Characterization of Financial Time Series, http://nance.martinsewell.com/stylized-facts/

* Sharpe, William F. (1964)

Capital asset prices: A theory of market equilibrium under conditions of risk, Journal of Finance, 19, 3, 425-442

88

89.

参考文献 (4/4)

* Soros,G. (2003)

The alchemy of finance, Wiley

* Yamada, K., H. Takayasu and T. Ito and M. Takayasu (2009)

Solvable stochastic dealer models for financial markets, Physical Review E, 79, 5, 051120

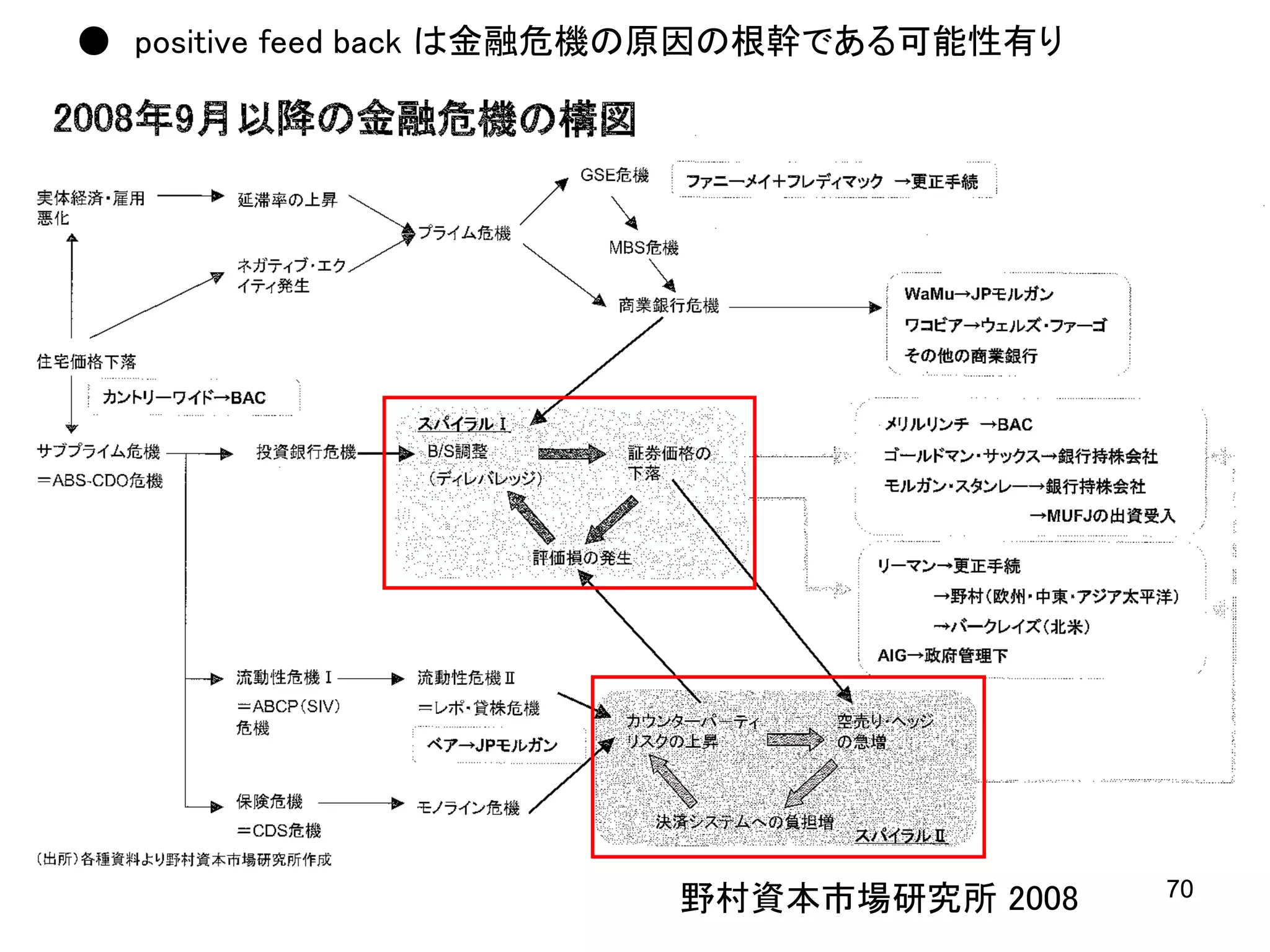

* 野村資本市場研究所 (2008)

サブプライム問題に端を発する金融危機の全貌, 資本市場クォータリー秋号付属資料

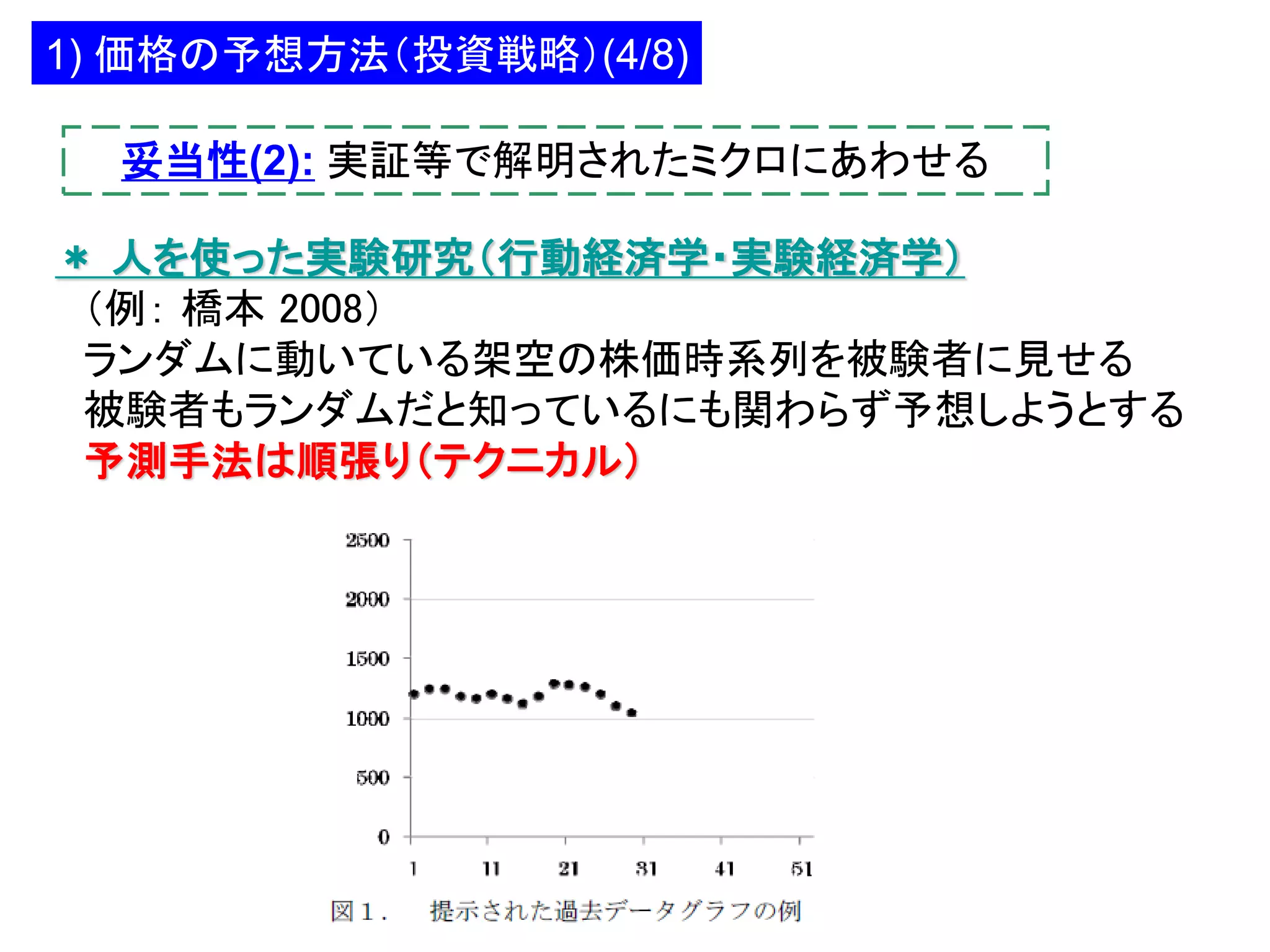

* 橋本文彦 (2008)

人は、過去の株価時系列にどのような未来を投影するのか?, 第1回人工知能学会ファイナンス研究会

* 山本竜市, 平田英明 (2011)

日本の株式市場における戦略の切り替えの実証分析, 第5回行動経済学会プロシーディングス

89

![金融レジリエンス情報学

2013/12/12

スパークス・アセット・マネジメント

東京大学大学院工学系研究科

水田孝信

mizutata[at]gmail.com

@takanobu.mizuta

http://www.geocities.jp/mizuta_ta/jindex.htm

http://www.slideshare.net/mizutata/20131212

1](https://image.slidesharecdn.com/20131212-131023225724-phpapp01/75/2013-12-12-1-2048.jpg)

⇒ 反対

28](https://image.slidesharecdn.com/20131212-131023225724-phpapp01/75/2013-12-12-28-2048.jpg)

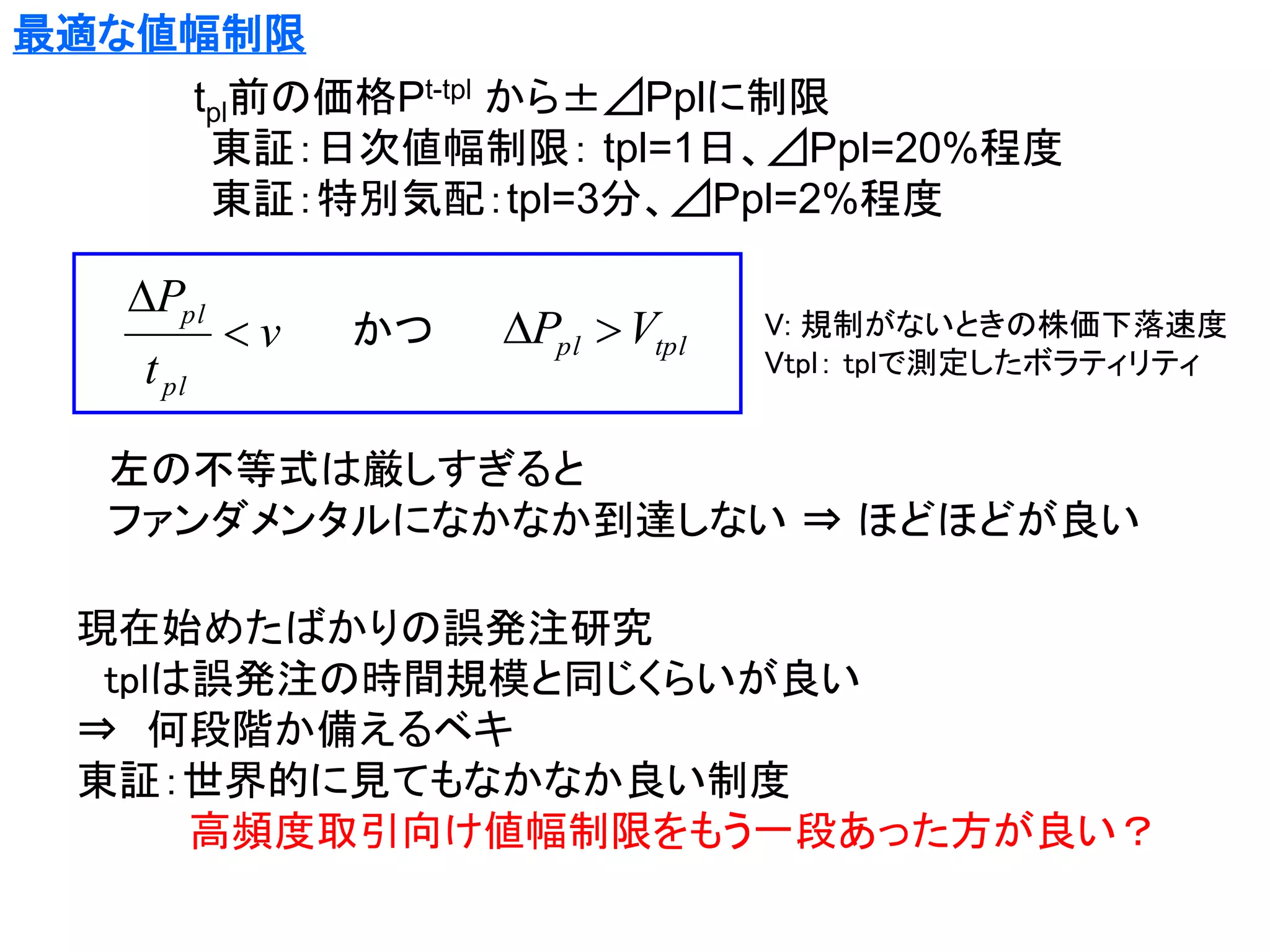

![【2】シミュレーション結果

株価の推移

ファンダメンタル価格一定(=10000)

10500

規制なし

値幅制限

10300

価格

10400

完全空売り

アップティック

10200

10100

10000

9900

900

800

700

600

500

400

300

200

100

0

9800

ティック時刻 (×1000)

空売り規制は平常時に常に割高で取引され非効率

⇒ 実証研究(大墳[2012])と整合的

⇒ モデルが異なる八木ら[2011]とも整合的 ⇒ 頑健性高い](https://image.slidesharecdn.com/20131212-131023225724-phpapp01/75/2013-12-12-29-2048.jpg)

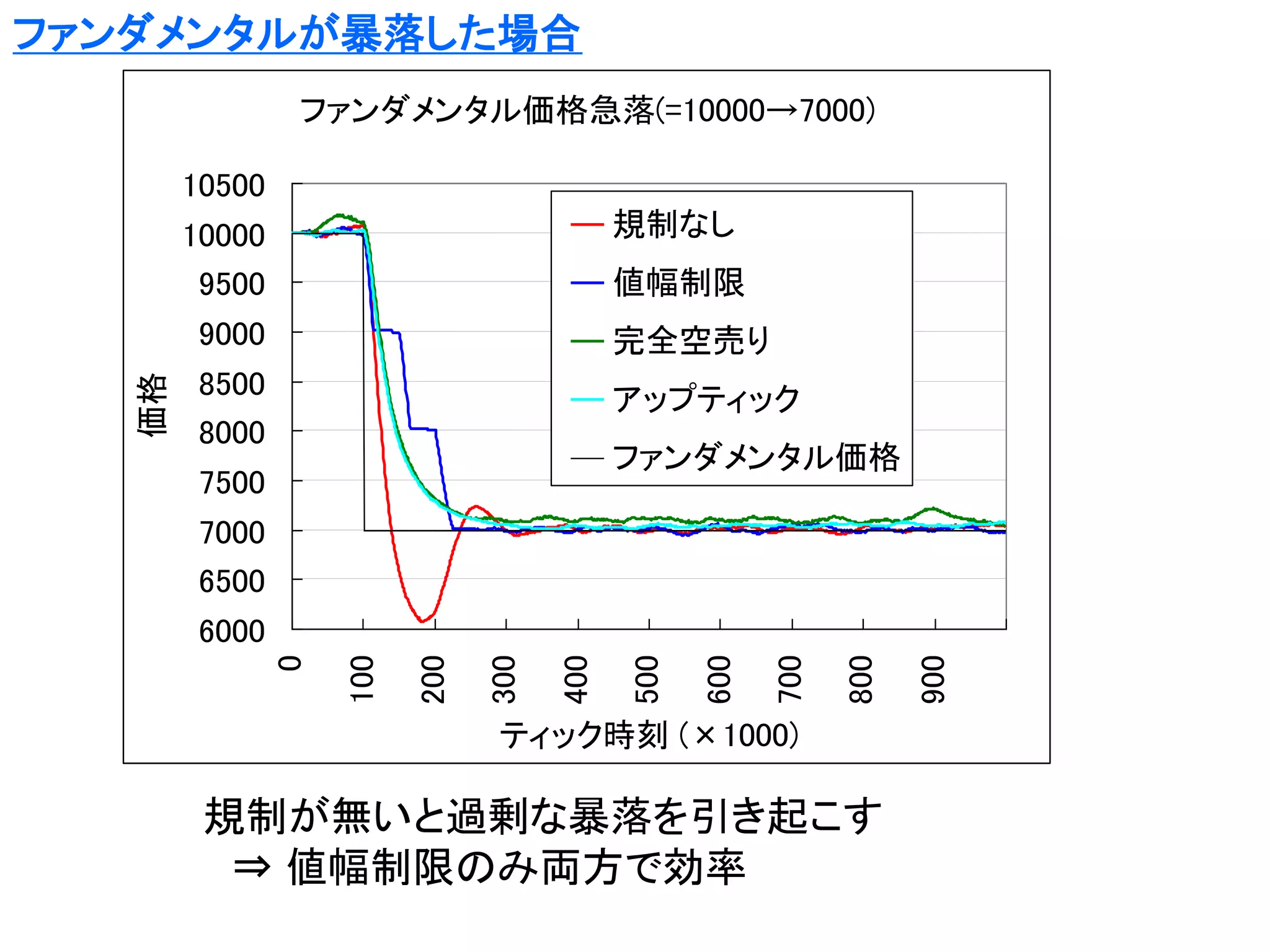

![ファンダメンタルが暴騰した場合 ⇒ バブル時

20000

18000

16000

14000

規制なし

値幅制限

アップティック

ファンダメンタル価格

12000

10000

8000

0

100

200

300

400

500

600

700

800

900

完全空売り規制、アップティックルール

⇒ バブルを大きく助長する:八木ら[2011]のモデルでも確認

⇒ コロンブスのたまご的発見: 空売り規制は下落時ではなく

安定時・上昇時こそ検証されるべきという発見](https://image.slidesharecdn.com/20131212-131023225724-phpapp01/75/2013-12-12-31-2048.jpg)

![ご清聴ありがとうございました

水田孝信

mizutata[at]gmail.com

@takanobu.mizuta

http://www.geocities.jp/mizuta_ta/jindex.htm

http://www.slideshare.net/mizutata/20131212](https://image.slidesharecdn.com/20131212-131023225724-phpapp01/75/2013-12-12-85-2048.jpg)