Download to read offline

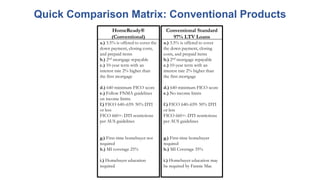

This document provides an overview and summary of a training on Chenoa Fund programs offered by CBC Mortgage Agency. The training covers all aspects of originating and processing loans through the Chenoa Fund programs, including: an overview of conventional and FHA programs; how to calculate AMI; how to complete the 1003; underwriting; locking loans; securing down payment assistance; document drawing; purchase clearing; final documents; servicing; and why to use Chenoa Fund programs. It also includes a matrix comparing the conventional standard 97% LTV and HomeReady products and program guidelines.