1) The document discusses various aspects of finance and accounting that are important for software engineers starting their own companies, such as the need for capital, sources of funding, budgeting, sales, costing, pricing, annual statements, capital maintenance, and auditing.

2) It emphasizes that sound financial management is essential for any organization to succeed and covers topics like determining costs, setting prices, producing annual financial reports, and getting accounts audited.

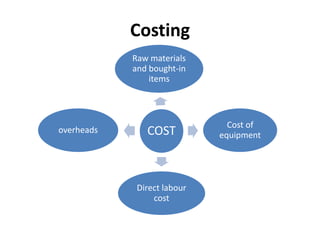

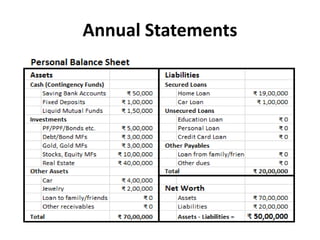

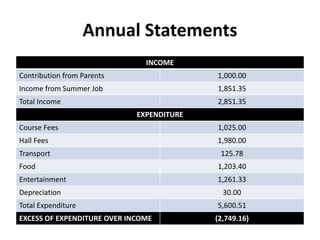

3) Key aspects covered include determining startup capital needs, presenting business plans to potential funders, creating and monitoring budgets, tracking sales and orders, calculating costs including materials, labor and overheads, common pricing approaches, components of annual financial statements like the balance sheet and profit

![제 23회 보아즈(BOAZ) 빅데이터 컨퍼런스 - [MBOAX] : ABSA를 활용한 소비자 반응 분석 기반 운영 효율화 대시보드 설계](https://cdn.slidesharecdn.com/ss_thumbnails/3-1boaz23rdconferencemboax-260203102709-9d519923-thumbnail.jpg?width=640&height=640&fit=bounds)