The Time Valueof Money

Interest Rate

Simple Interest

Compound Interest

Amortizing a Loan

Compounding More Than Once per

Year

3.

“Compound interestis the eighth wonder of

the world. He who understands it, earns it ...

he who doesn't ... pays it.”

― Albert Einstein

4.

Why TIME?

TIME allowsyou the opportunity to

postpone consumption and earn

INTEREST.

Why is TIME such an important

element in your decision?

5.

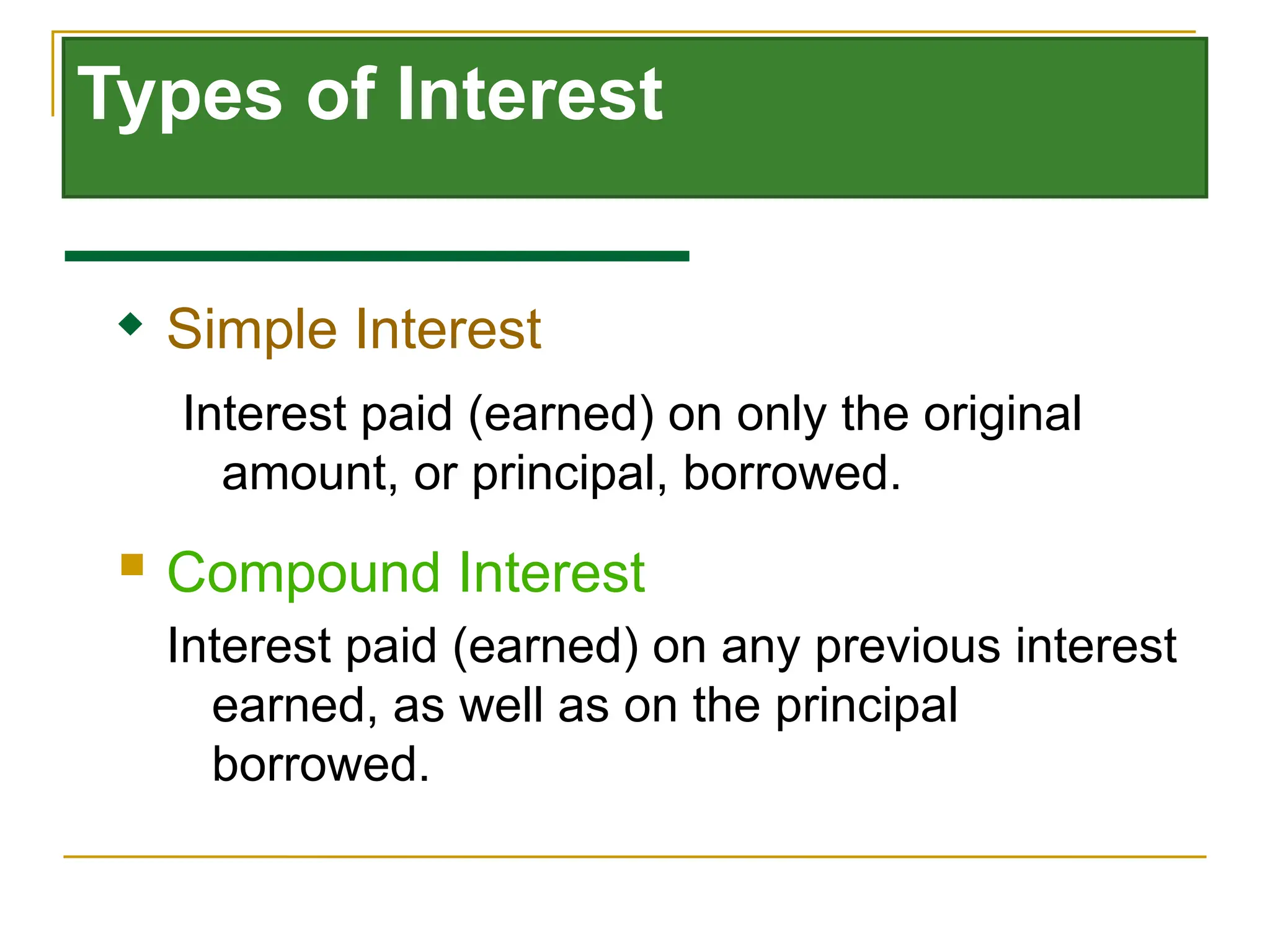

Types of Interest

Compound Interest

Interest paid (earned) on any previous interest

earned, as well as on the principal

borrowed.

Simple Interest

Interest paid (earned) on only the original

amount, or principal, borrowed.

6.

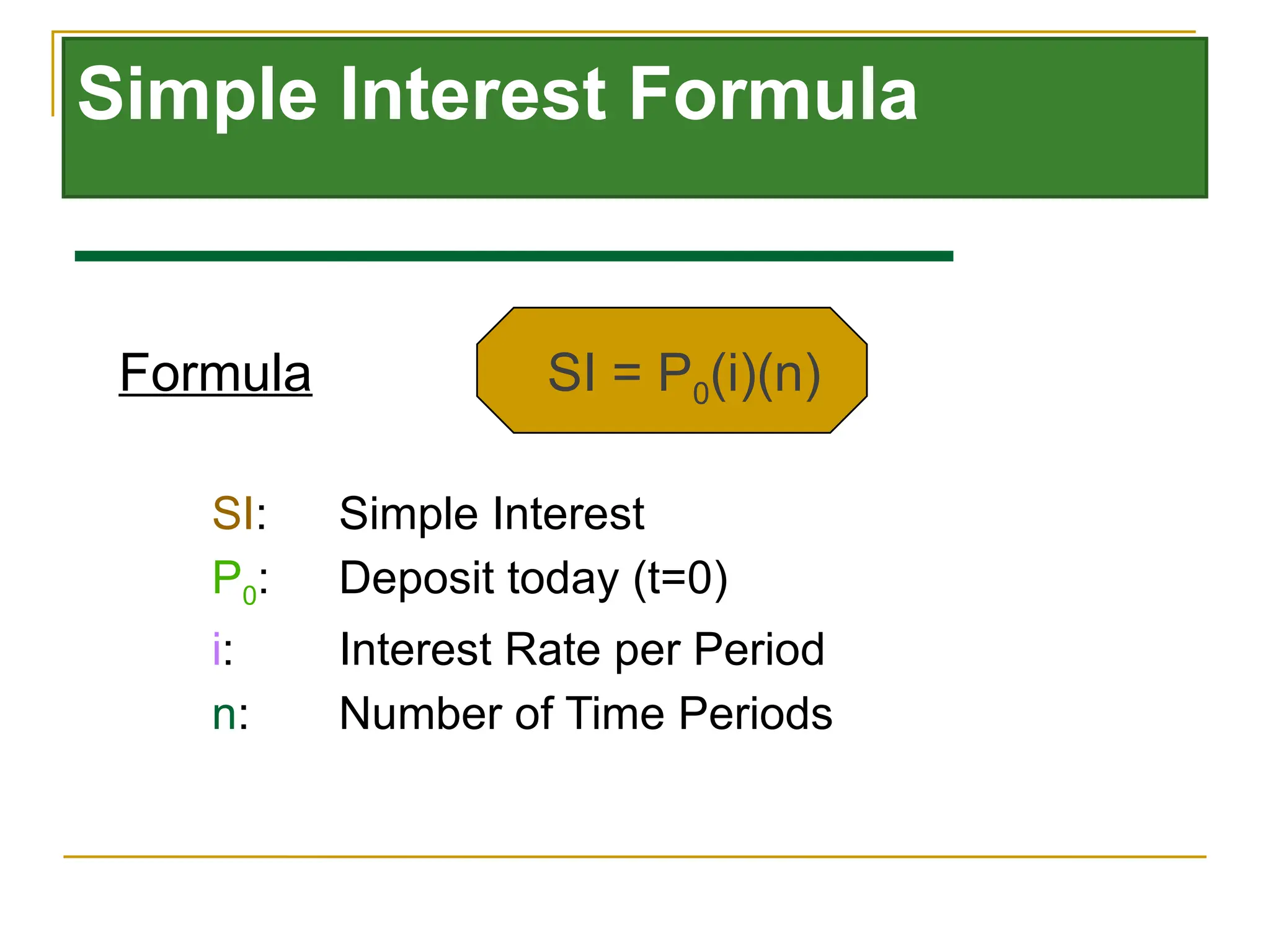

Simple Interest Formula

FormulaSI = P0(i)(n)

SI: Simple Interest

P0: Deposit today (t=0)

i: Interest Rate per Period

n: Number of Time Periods

7.

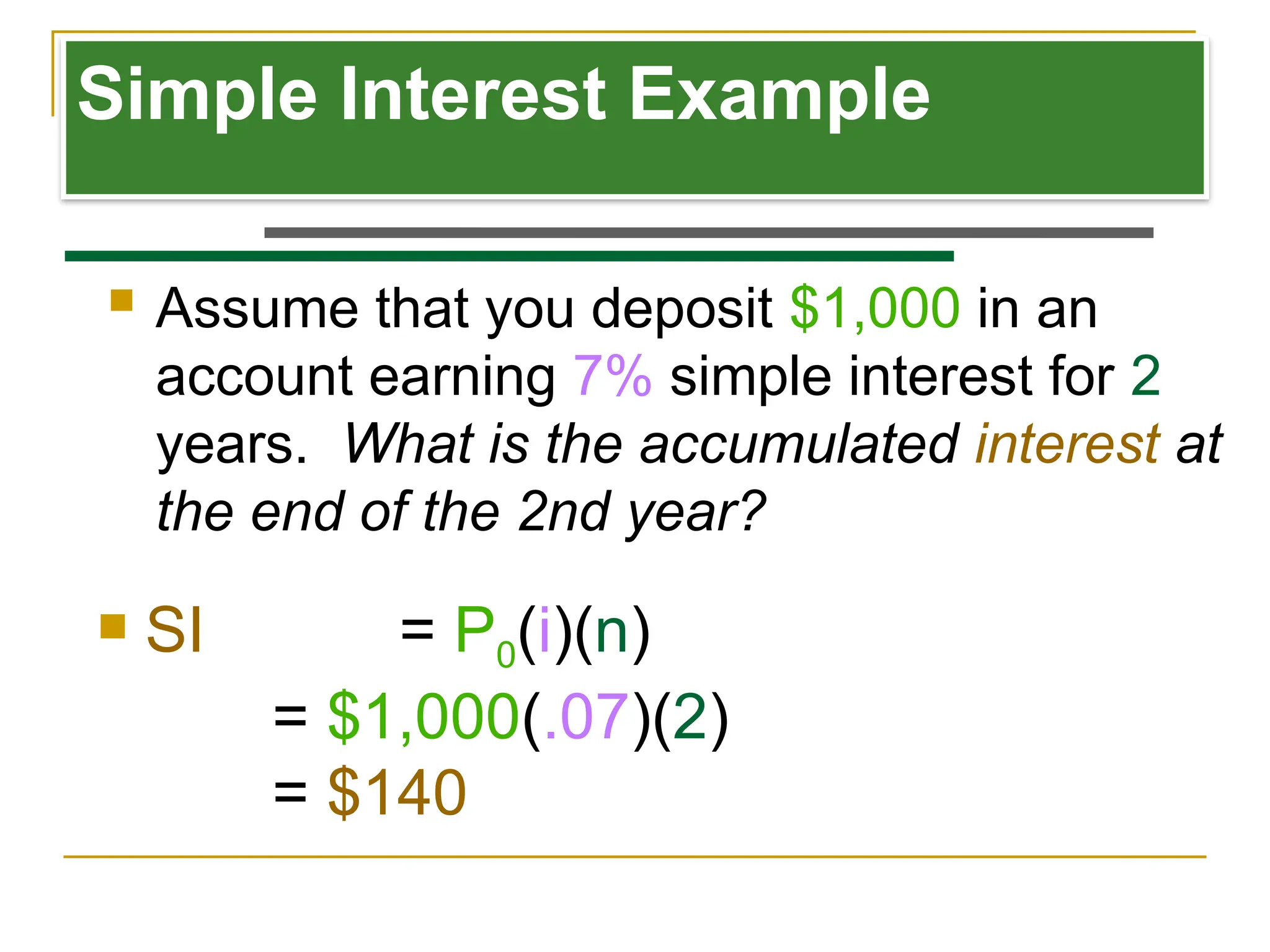

Simple Interest Example

SI = P0(i)(n)

= $1,000(.07)(2)

= $140

Assume that you deposit $1,000 in an

account earning 7% simple interest for 2

years. What is the accumulated interest at

the end of the 2nd year?

8.

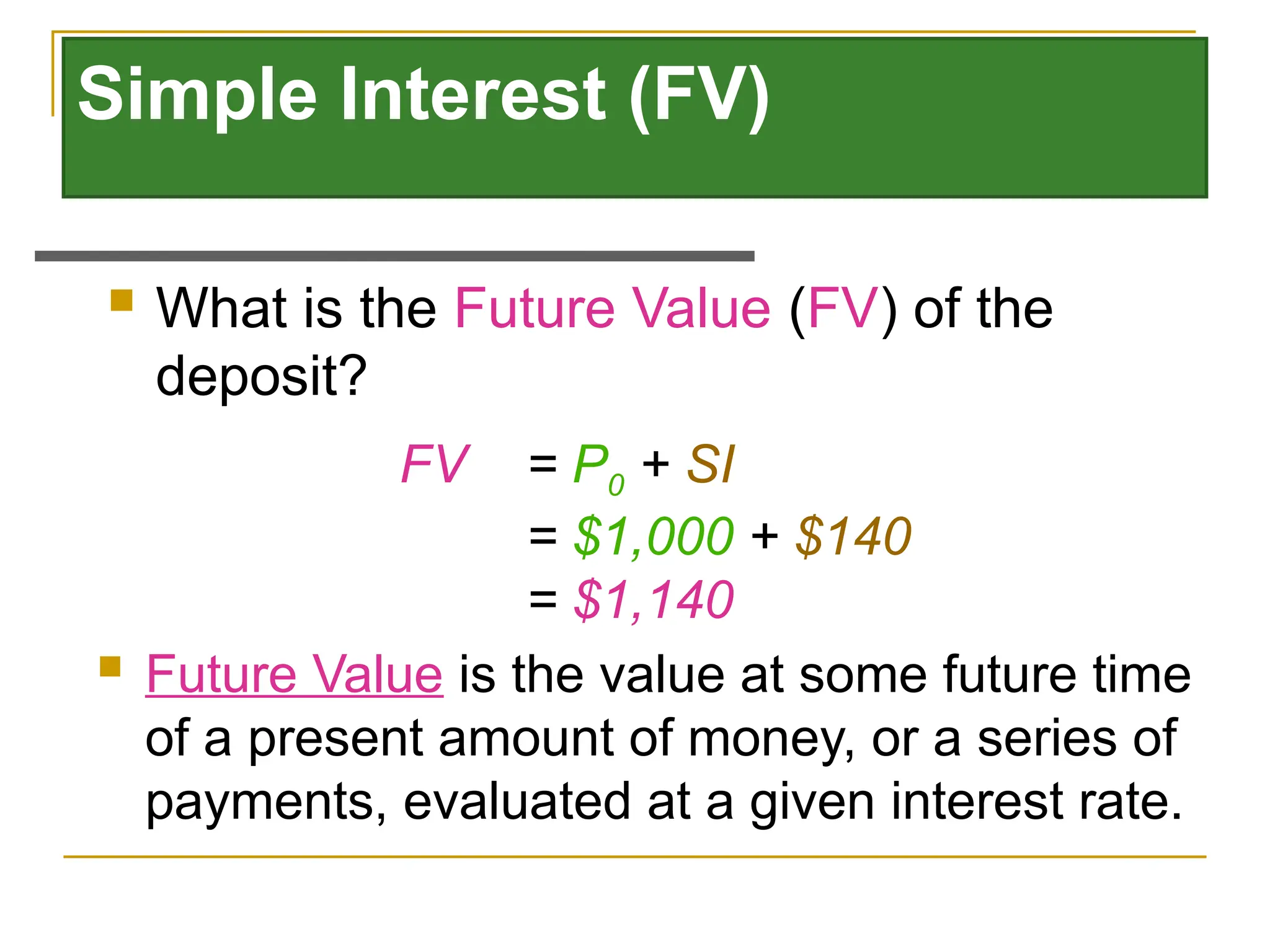

Simple Interest (FV)

FV= P0 + SI

= $1,000 + $140

= $1,140

Future Value is the value at some future time

of a present amount of money, or a series of

payments, evaluated at a given interest rate.

What is the Future Value (FV) of the

deposit?

9.

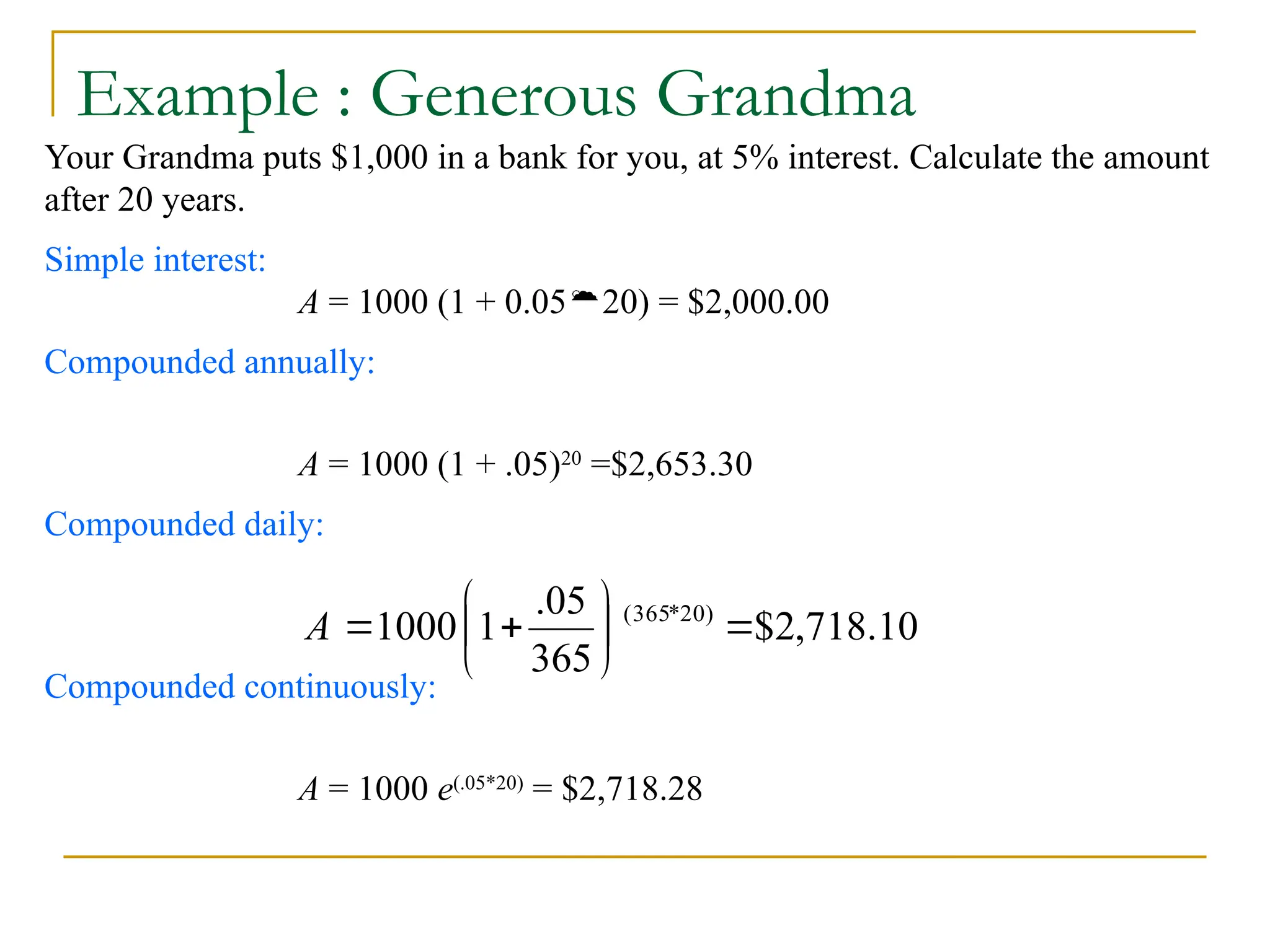

Example : GenerousGrandma

Your Grandma puts $1,000 in a bank for you, at 5% interest. Calculate the amount

after 20 years.

Simple interest:

A = 1000 (1 + 0.0520) = $2,000.00

Compounded annually:

A = 1000 (1 + .05)20

=$2,653.30

Compounded daily:

Compounded continuously:

A = 1000 e(.05*20)

= $2,718.28

10

.

718

,

2

$

365

05

.

1

1000 )

20

*

365

(

A

10.

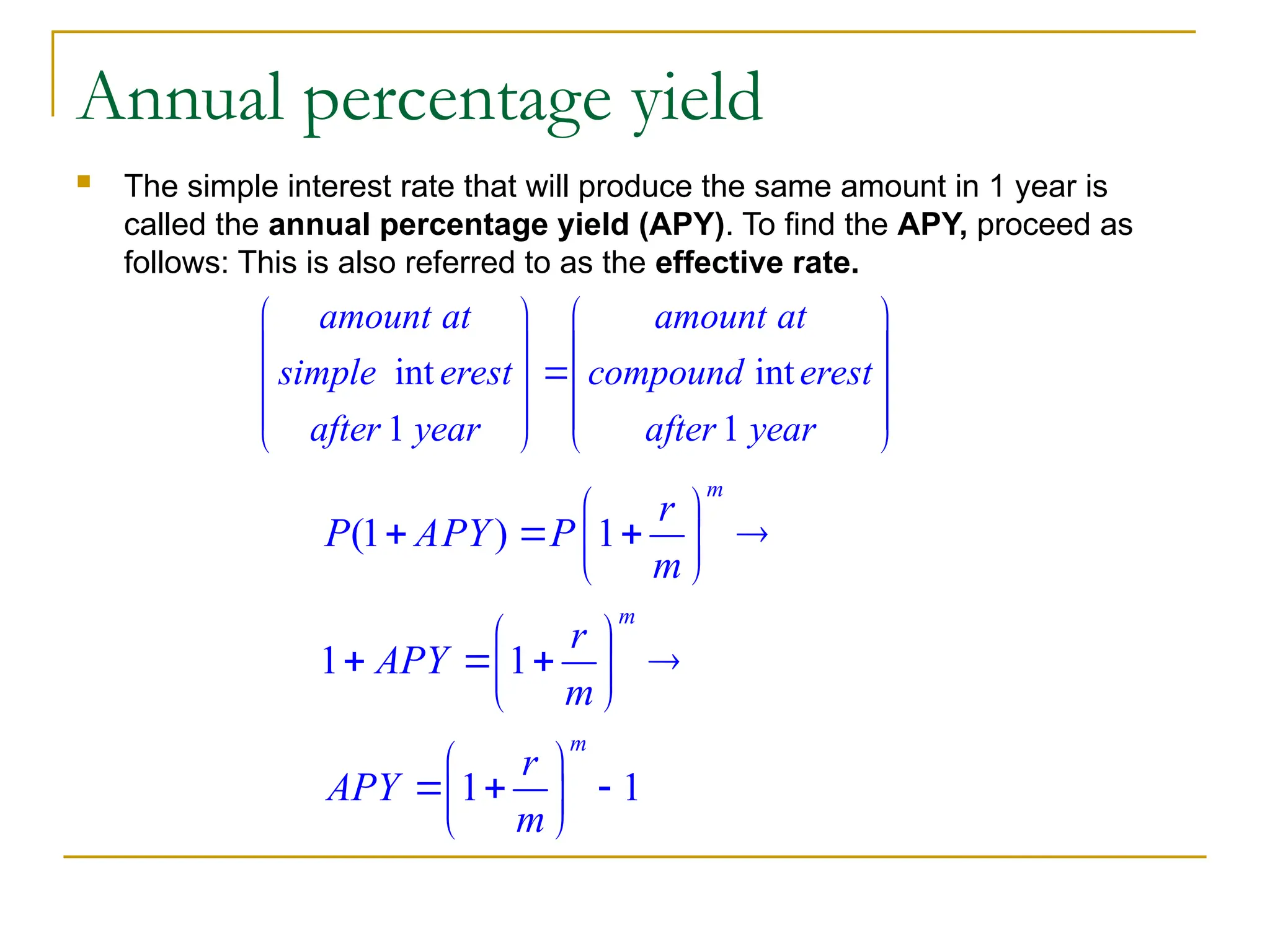

Annual percentage yield

The simple interest rate that will produce the same amount in 1 year is

called the annual percentage yield (APY). To find the APY, proceed as

follows: This is also referred to as the effective rate.

int int

1 1

amount at amount at

simple erest compound erest

after year after year

(1 ) 1

1 1

1 1

m

m

m

r

P APY P

m

r

APY

m

r

APY

m

11.

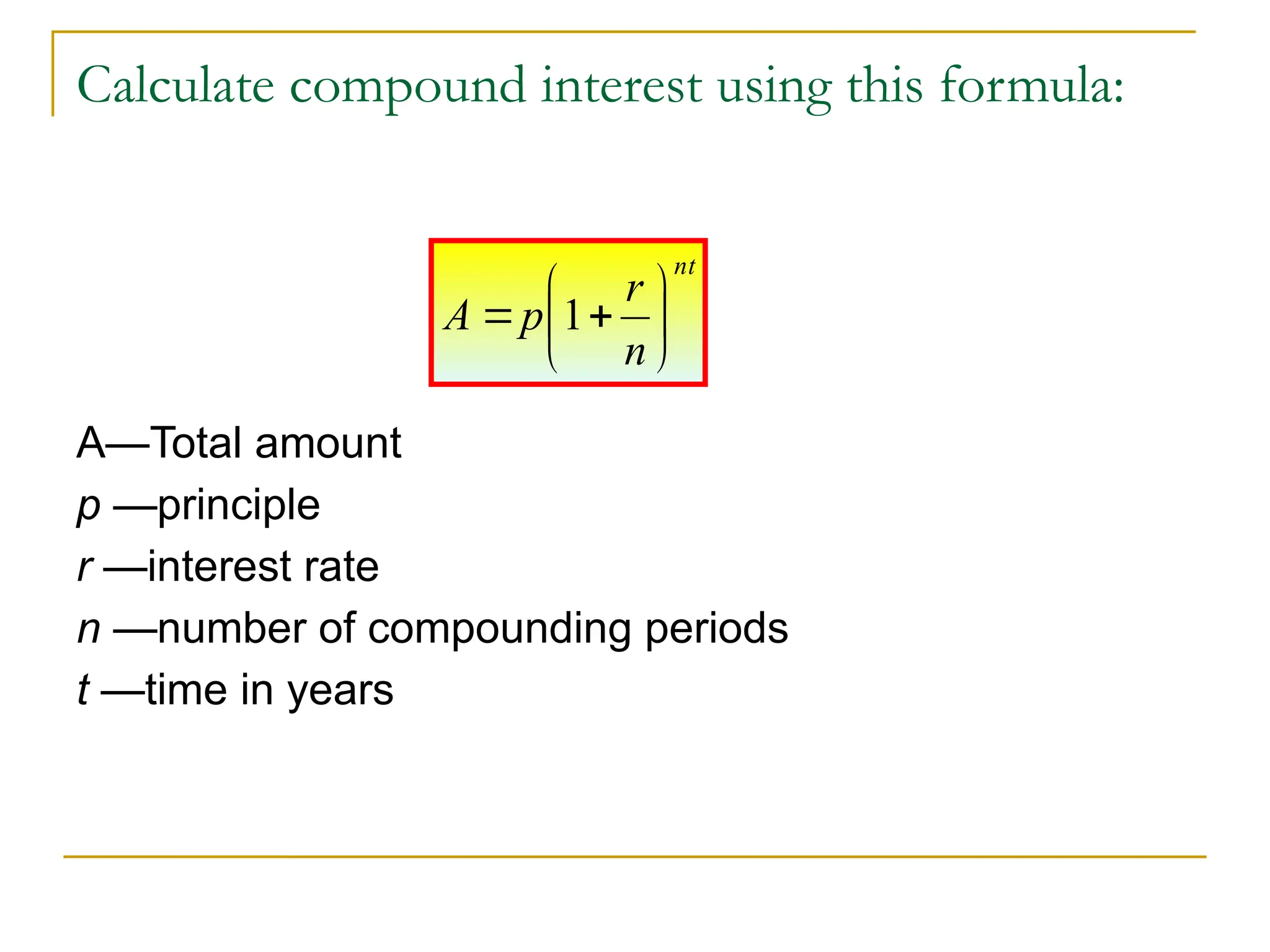

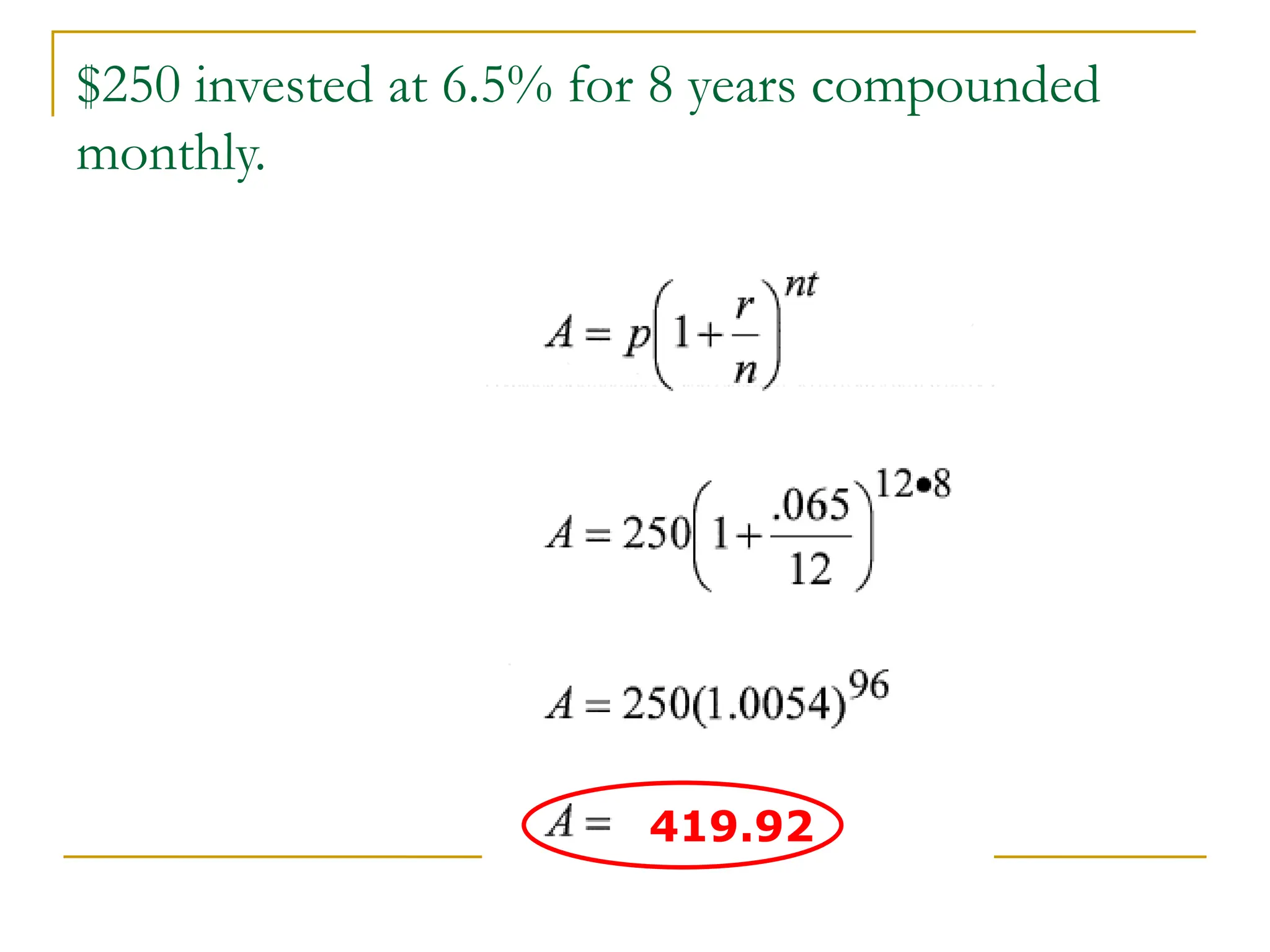

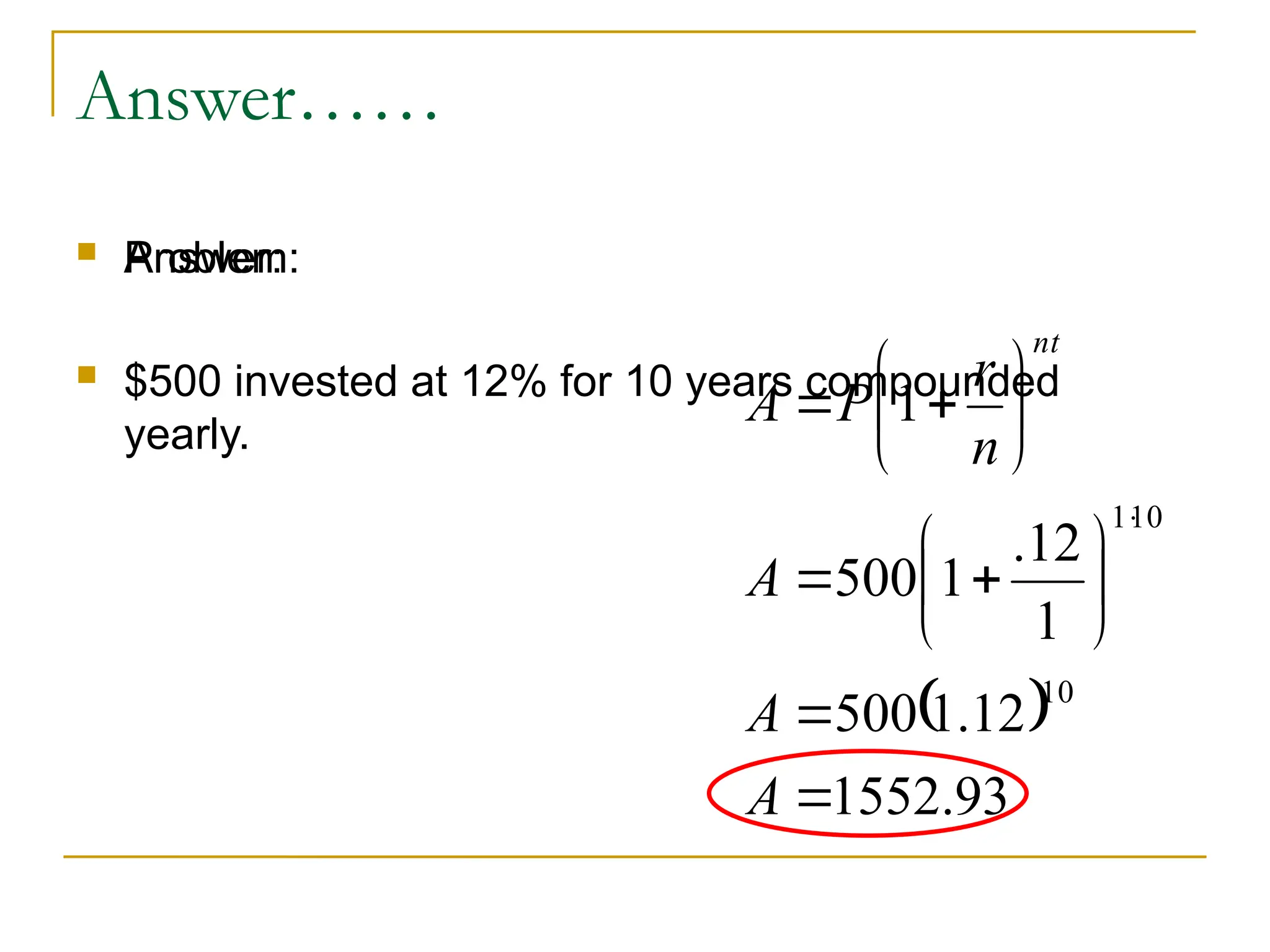

Calculate compound interestusing this formula:

A—Total amount

p —principle

r —interest rate

n —number of compounding periods

t —time in years

nt

n

r

p

A

1

12.

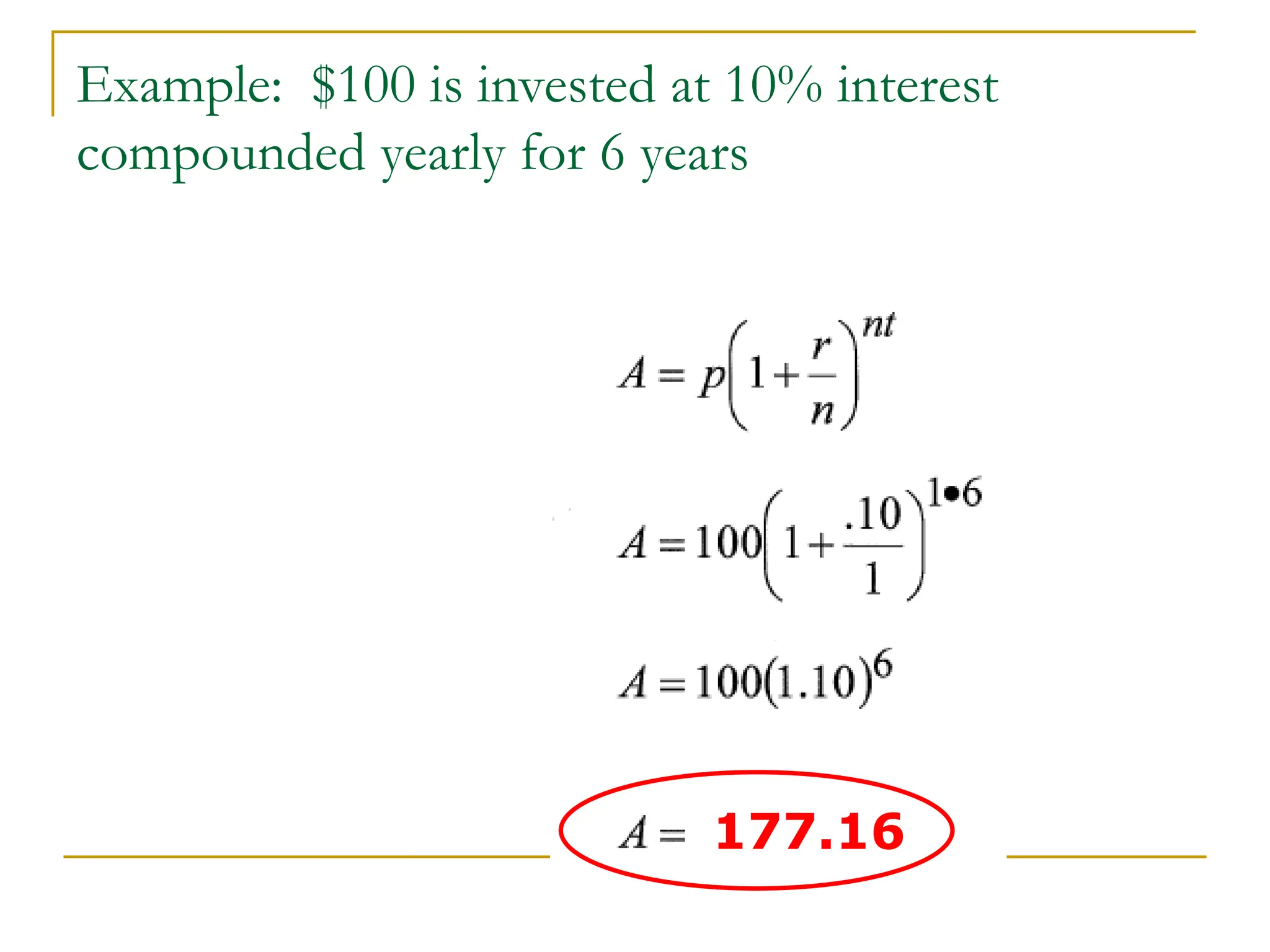

Example: $100 isinvested at 10% interest

compounded yearly for 6 years

177.16

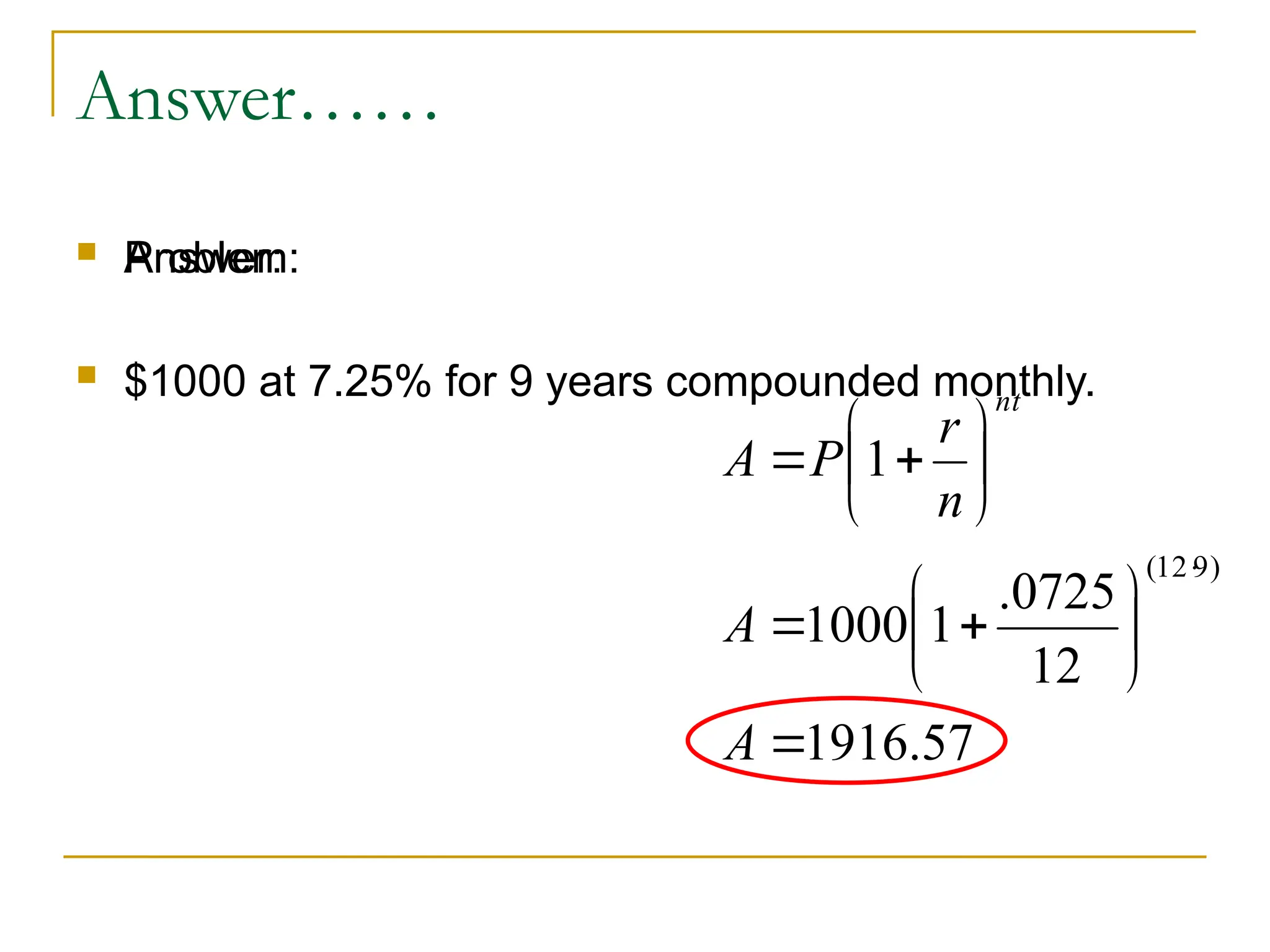

Answer……

Problem:

$1000at 7.25% for 9 years compounded monthly.

Answer:

57

.

1916

12

0725

.

1

1000

1

)

9

12

(

A

A

n

r

P

A

nt

18.

18

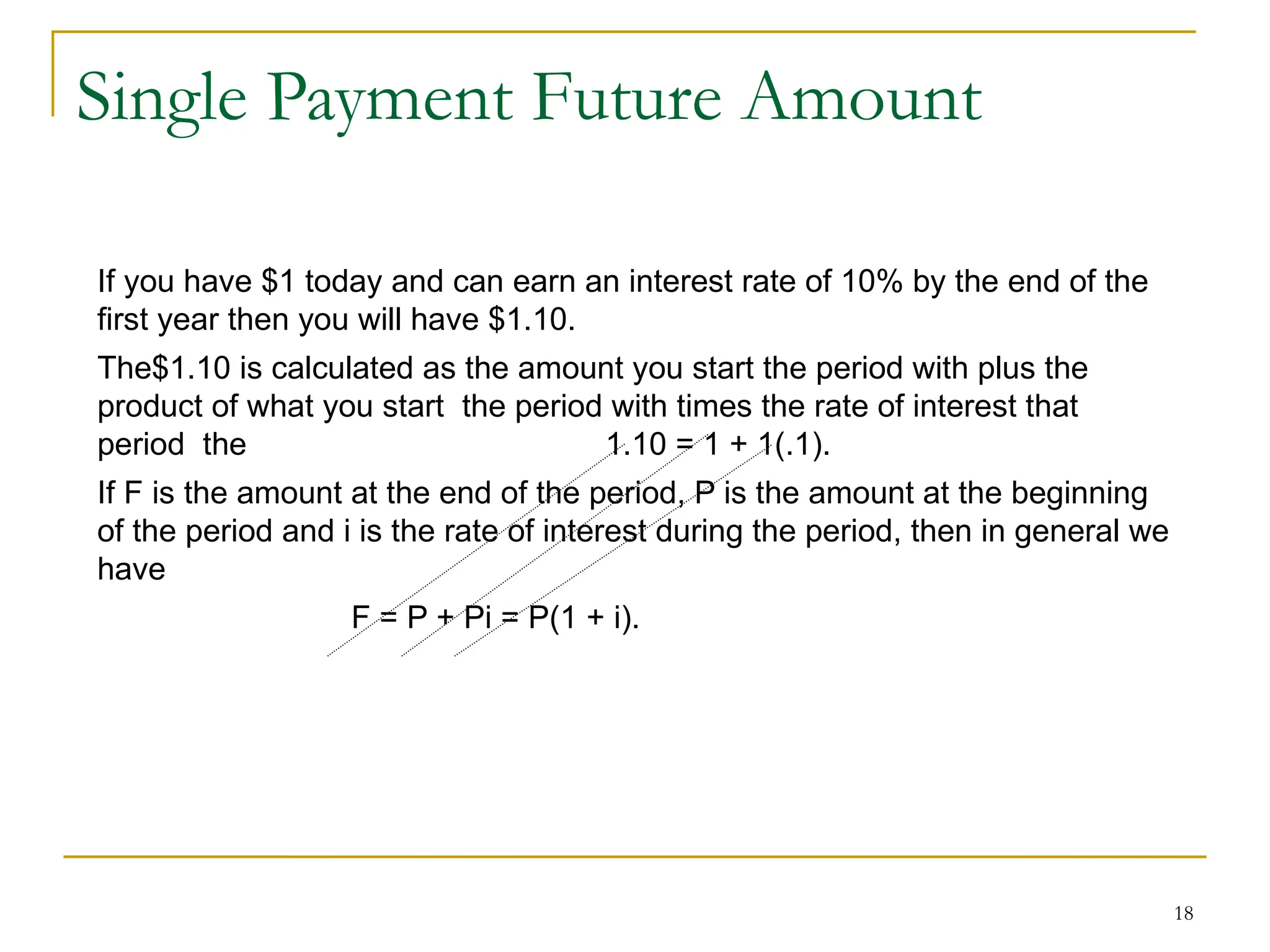

Single Payment FutureAmount

If you have $1 today and can earn an interest rate of 10% by the end of the

first year then you will have $1.10.

The$1.10 is calculated as the amount you start the period with plus the

product of what you start the period with times the rate of interest that

period the 1.10 = 1 + 1(.1).

If F is the amount at the end of the period, P is the amount at the beginning

of the period and i is the rate of interest during the period, then in general we

have

F = P + Pi = P(1 + i).

19.

19

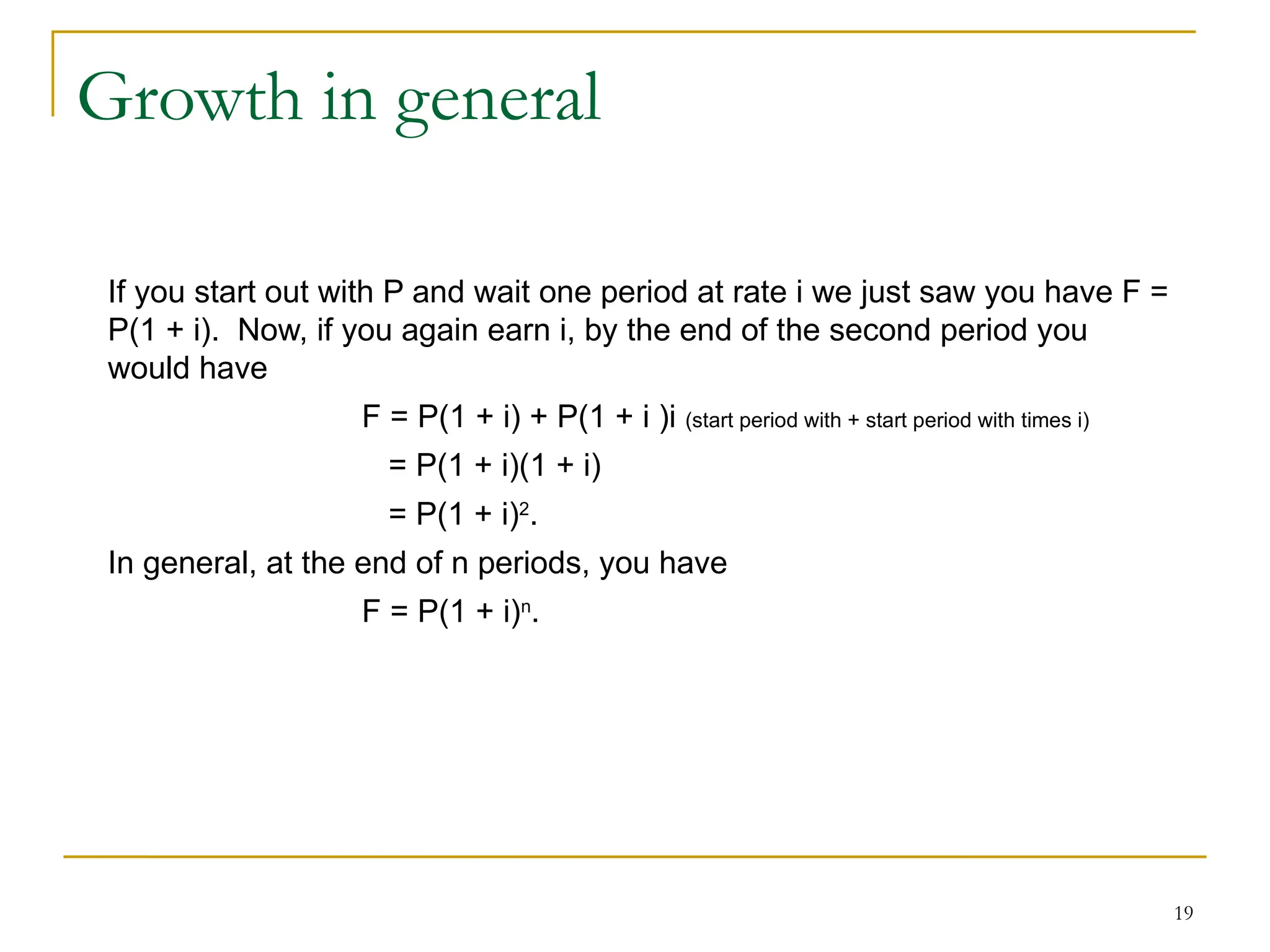

Growth in general

Ifyou start out with P and wait one period at rate i we just saw you have F =

P(1 + i). Now, if you again earn i, by the end of the second period you

would have

F = P(1 + i) + P(1 + i )i (start period with + start period with times i)

= P(1 + i)(1 + i)

= P(1 + i)2

.

In general, at the end of n periods, you have

F = P(1 + i)n

.

20.

20

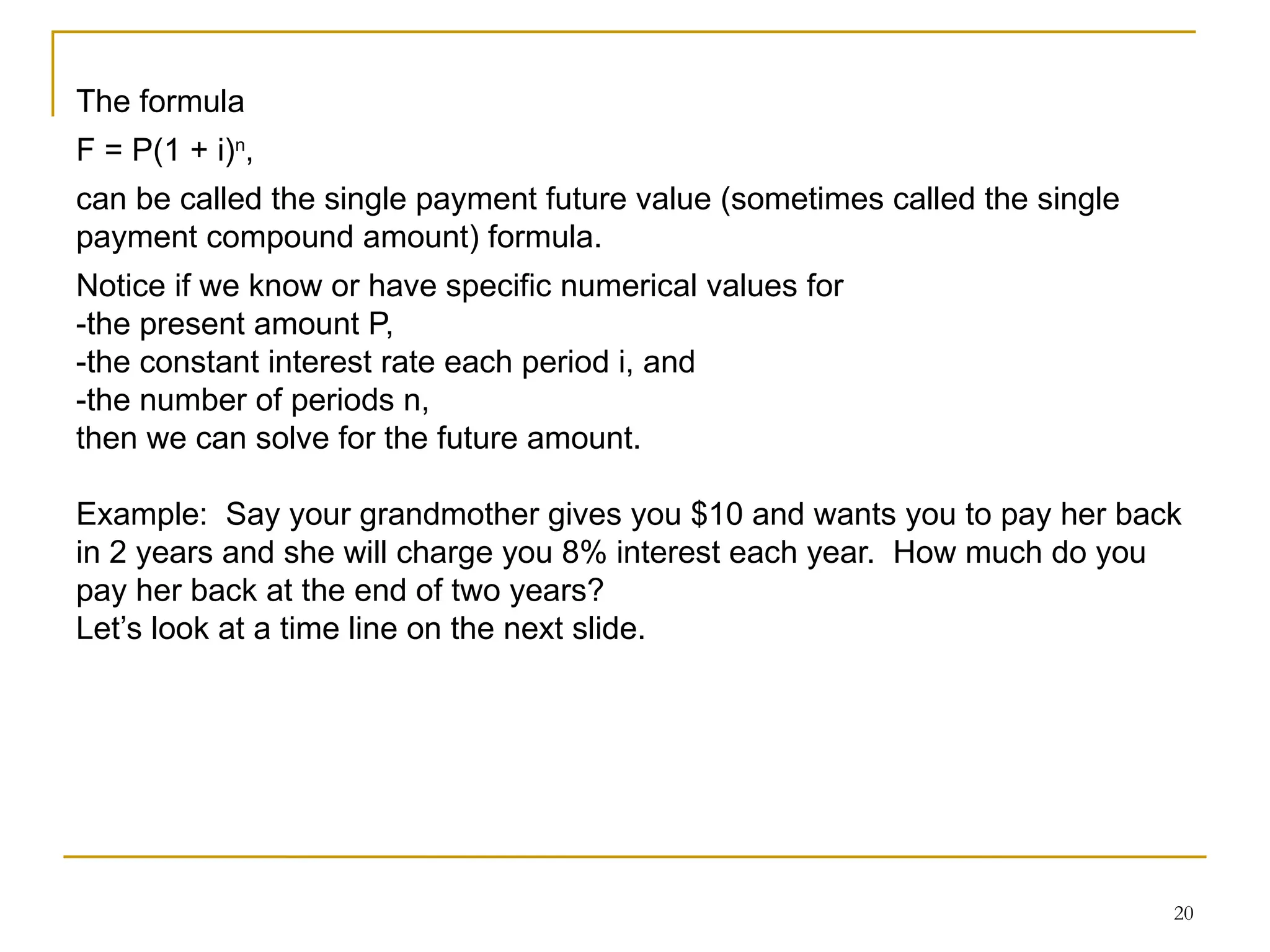

The formula

F =P(1 + i)n

,

can be called the single payment future value (sometimes called the single

payment compound amount) formula.

Notice if we know or have specific numerical values for

-the present amount P,

-the constant interest rate each period i, and

-the number of periods n,

then we can solve for the future amount.

Example: Say your grandmother gives you $10 and wants you to pay her back

in 2 years and she will charge you 8% interest each year. How much do you

pay her back at the end of two years?

Let’s look at a time line on the next slide.

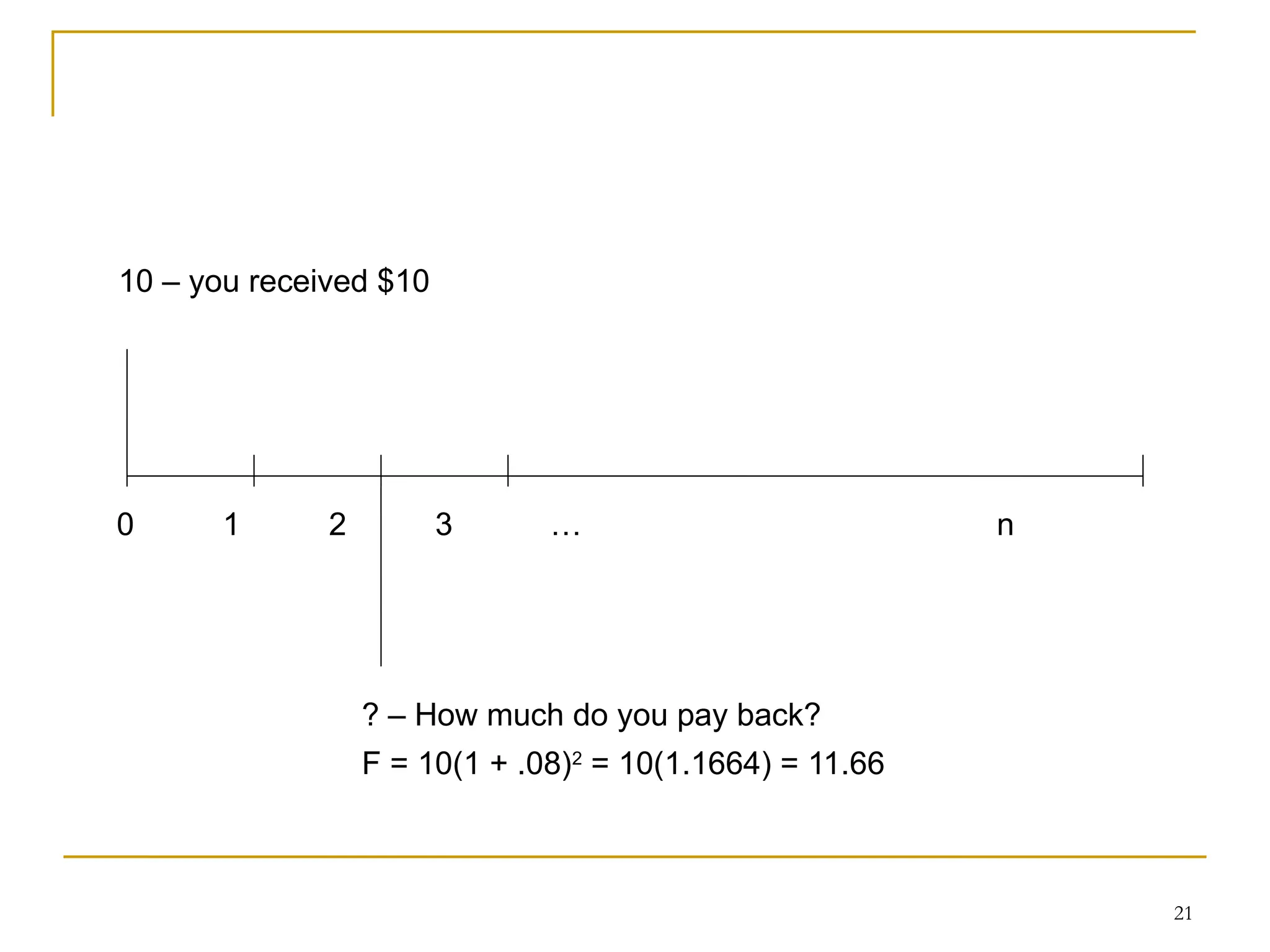

21.

21

0 1 23 … n

10 – you received $10

? – How much do you pay back?

F = 10(1 + .08)2

= 10(1.1664) = 11.66

22.

22

The Future ValueFactor

We saw on the last page that the amount to be paid back was

F = 10(1 + .08)2

= 10(1.1664) = 11.66.

Remember in general we know

F = P(1 + i)n

.

(1 + i)n

is called the interest factor by which we multiple the present

amount to get the future amount.

The interest factor is part of the formula and includes the interest rate.

23.

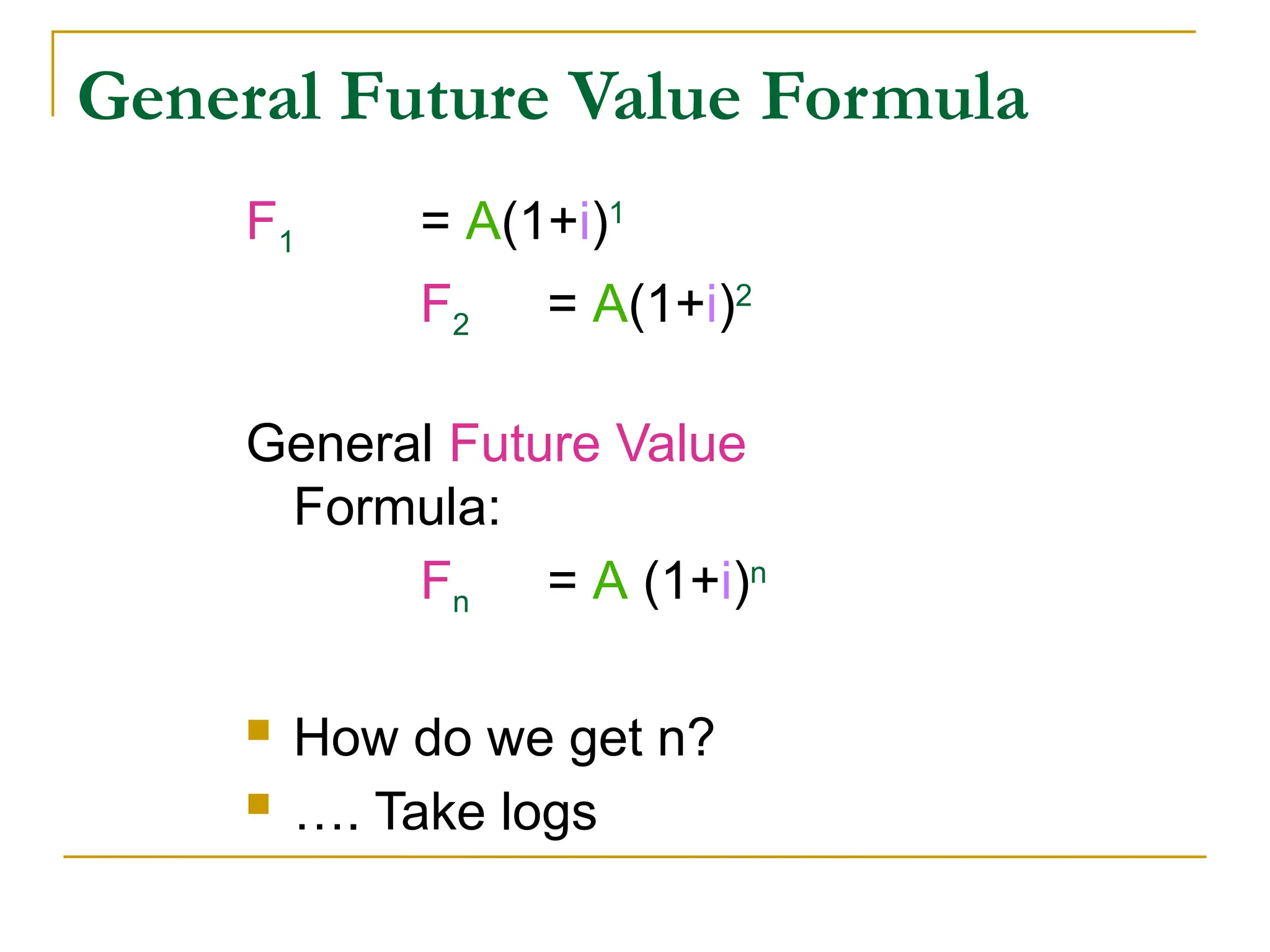

General Future ValueFormula

F1 = A(1+i)1

F2 = A(1+i)2

General Future Value

Formula:

Fn = A (1+i)n

How do we get n?

…. Take logs

24.

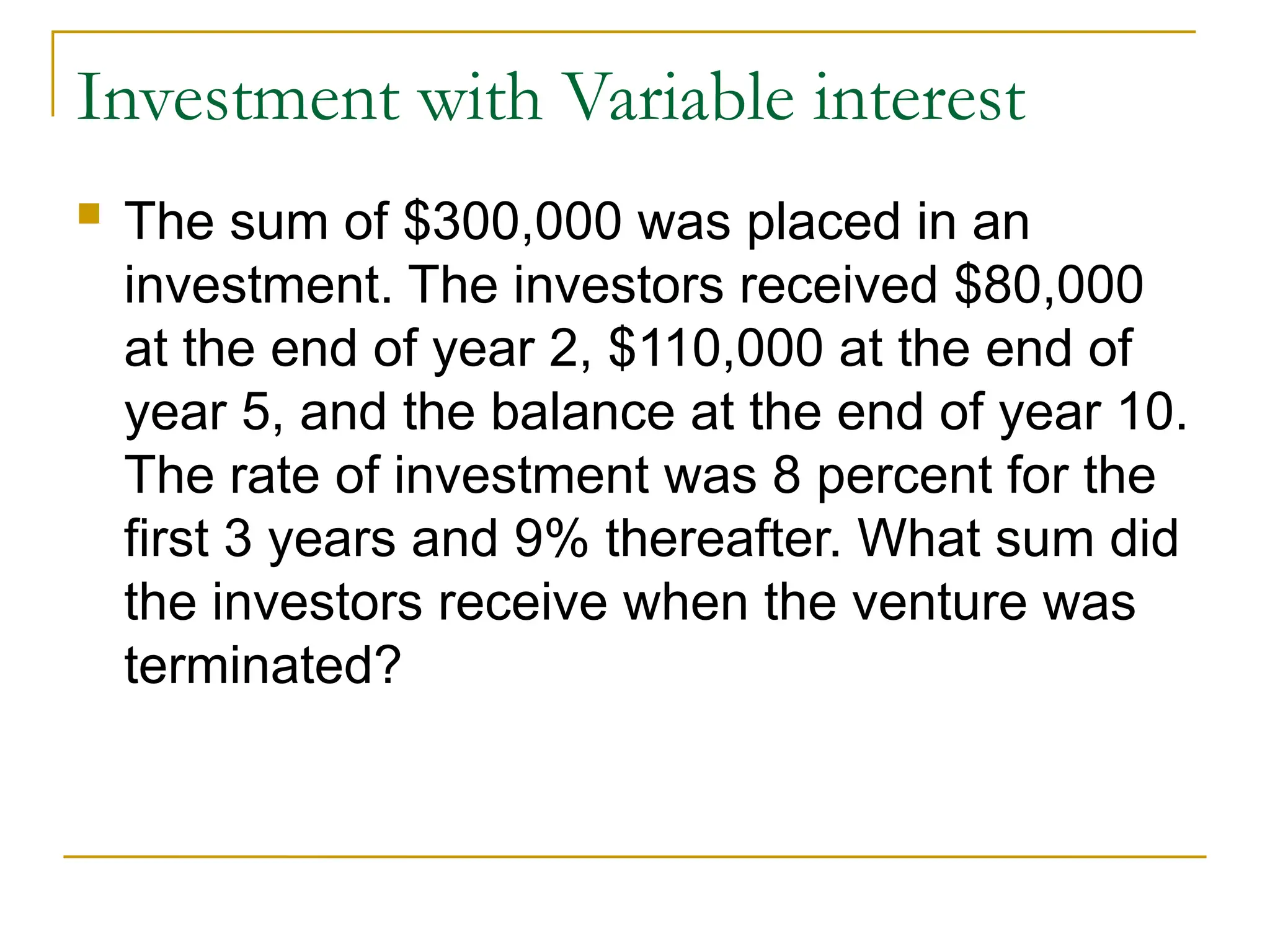

Investment with Variableinterest

The sum of $300,000 was placed in an

investment. The investors received $80,000

at the end of year 2, $110,000 at the end of

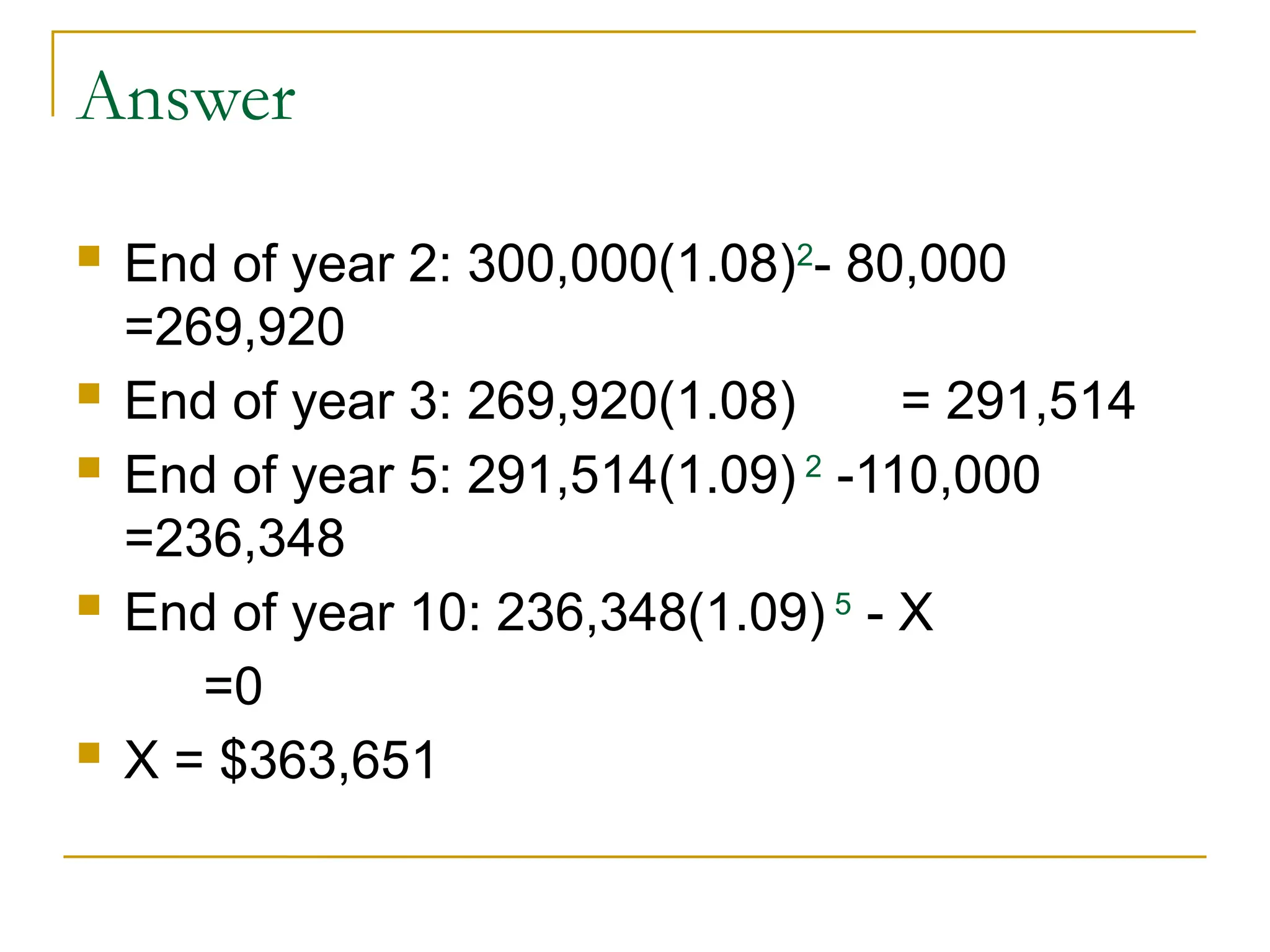

year 5, and the balance at the end of year 10.

The rate of investment was 8 percent for the

first 3 years and 9% thereafter. What sum did

the investors receive when the venture was

terminated?

25.

Answer

End ofyear 2: 300,000(1.08)2

- 80,000

=269,920

End of year 3: 269,920(1.08) = 291,514

End of year 5: 291,514(1.09) 2

-110,000

=236,348

End of year 10: 236,348(1.09) 5

- X

=0

X = $363,651

26.

Annuity

When thesum of principal and interest is

equal for each period.

27.

Types of Annuities

Ordinary Annuity: Payments or receipts

occur at the end of each period.

Annuity Due: Payments or receipts occur at

the beginning of each period.

An Annuity represents a series of equal

payments (or receipts) occurring over a

specified number of equidistant periods.

28.

Examples of Annuities

Student Loan Payments

Car Loan Payments

Insurance Premiums

Mortgage Payments

Retirement Savings

29.

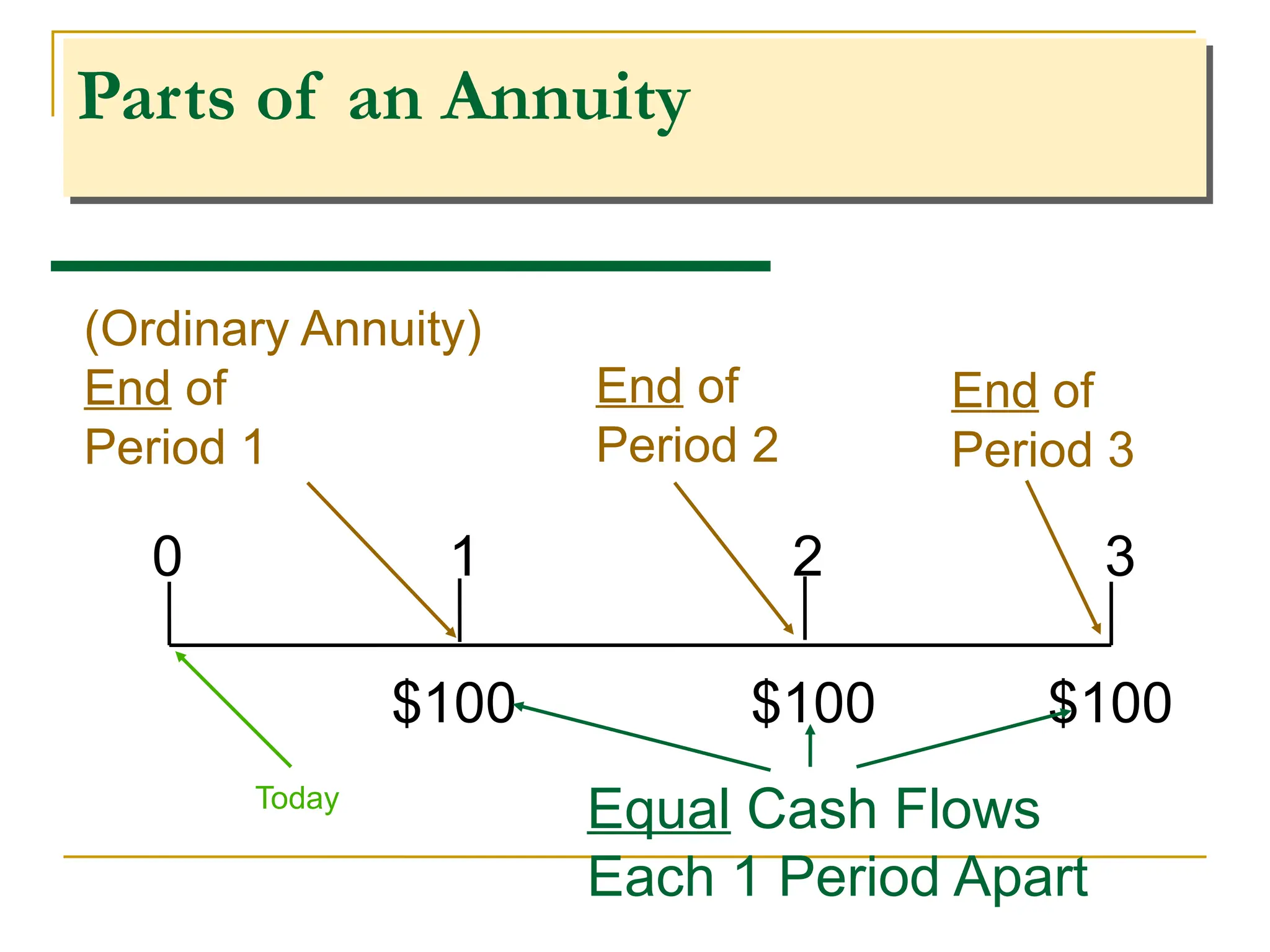

Parts of anAnnuity

0 1 2 3

$100 $100 $100

(Ordinary Annuity)

End of

Period 1

End of

Period 2

Today

Equal Cash Flows

Each 1 Period Apart

End of

Period 3

30.

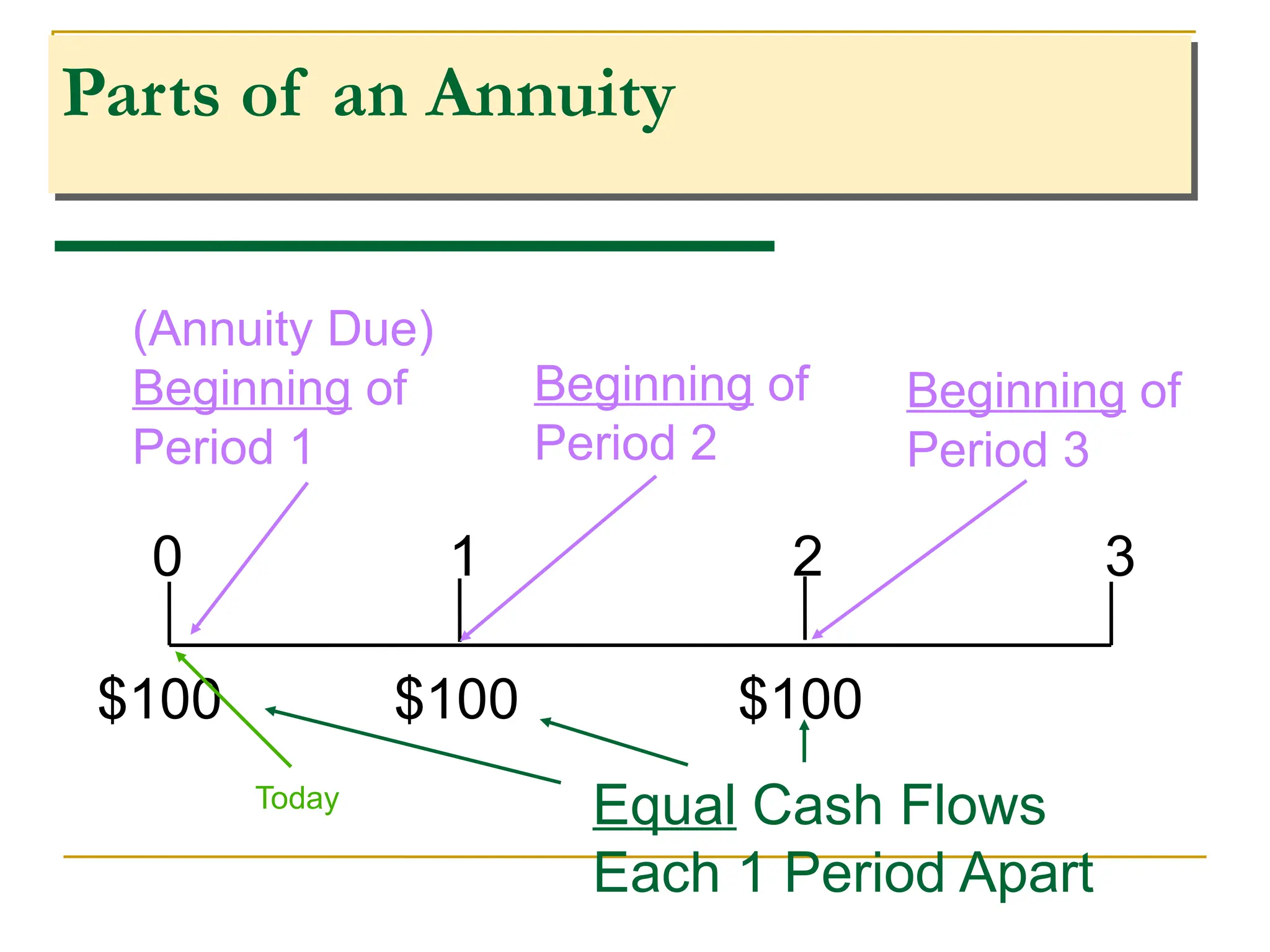

Parts of anAnnuity

0 1 2 3

$100 $100 $100

(Annuity Due)

Beginning of

Period 1

Beginning of

Period 2

Today Equal Cash Flows

Each 1 Period Apart

Beginning of

Period 3

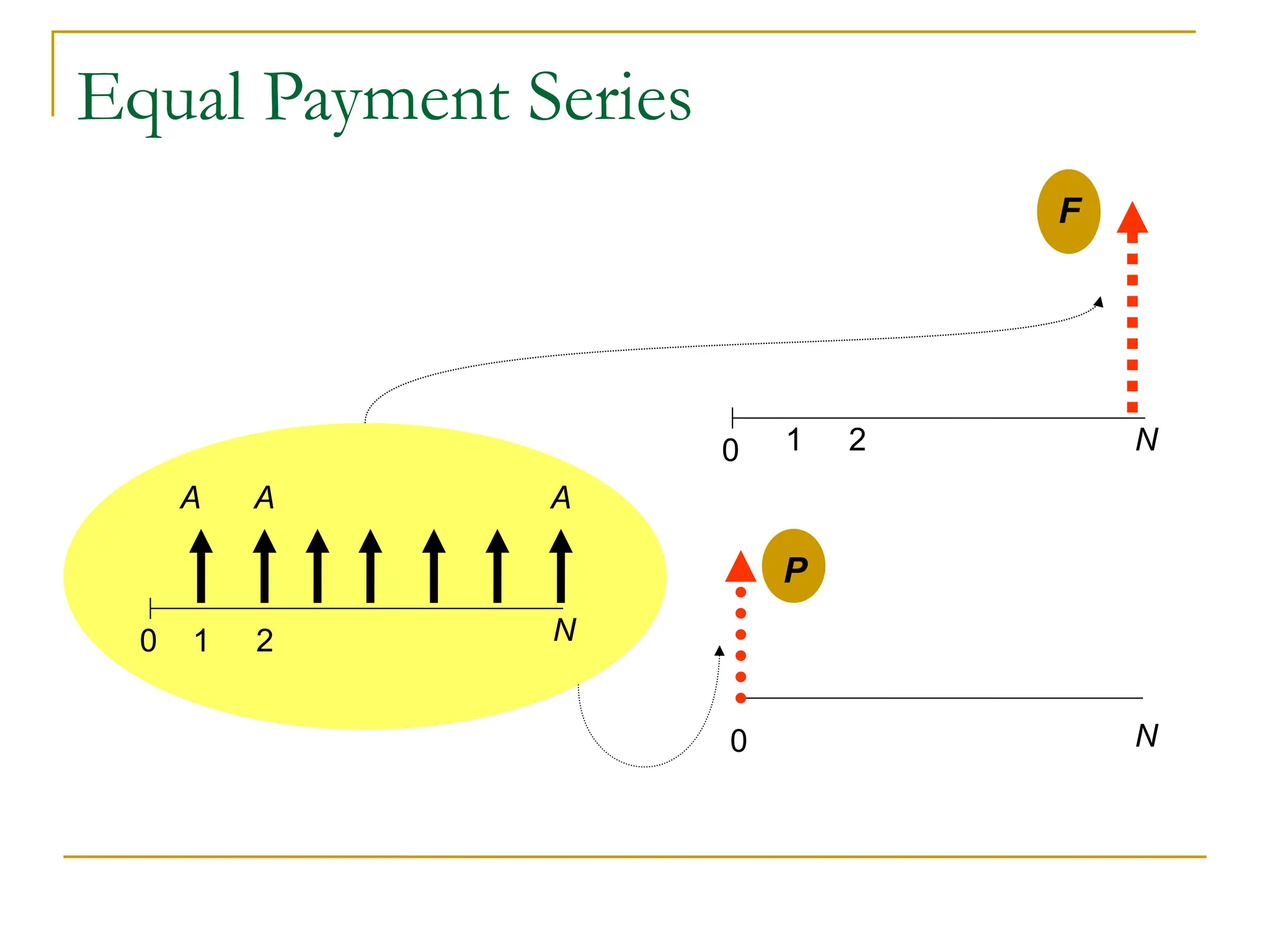

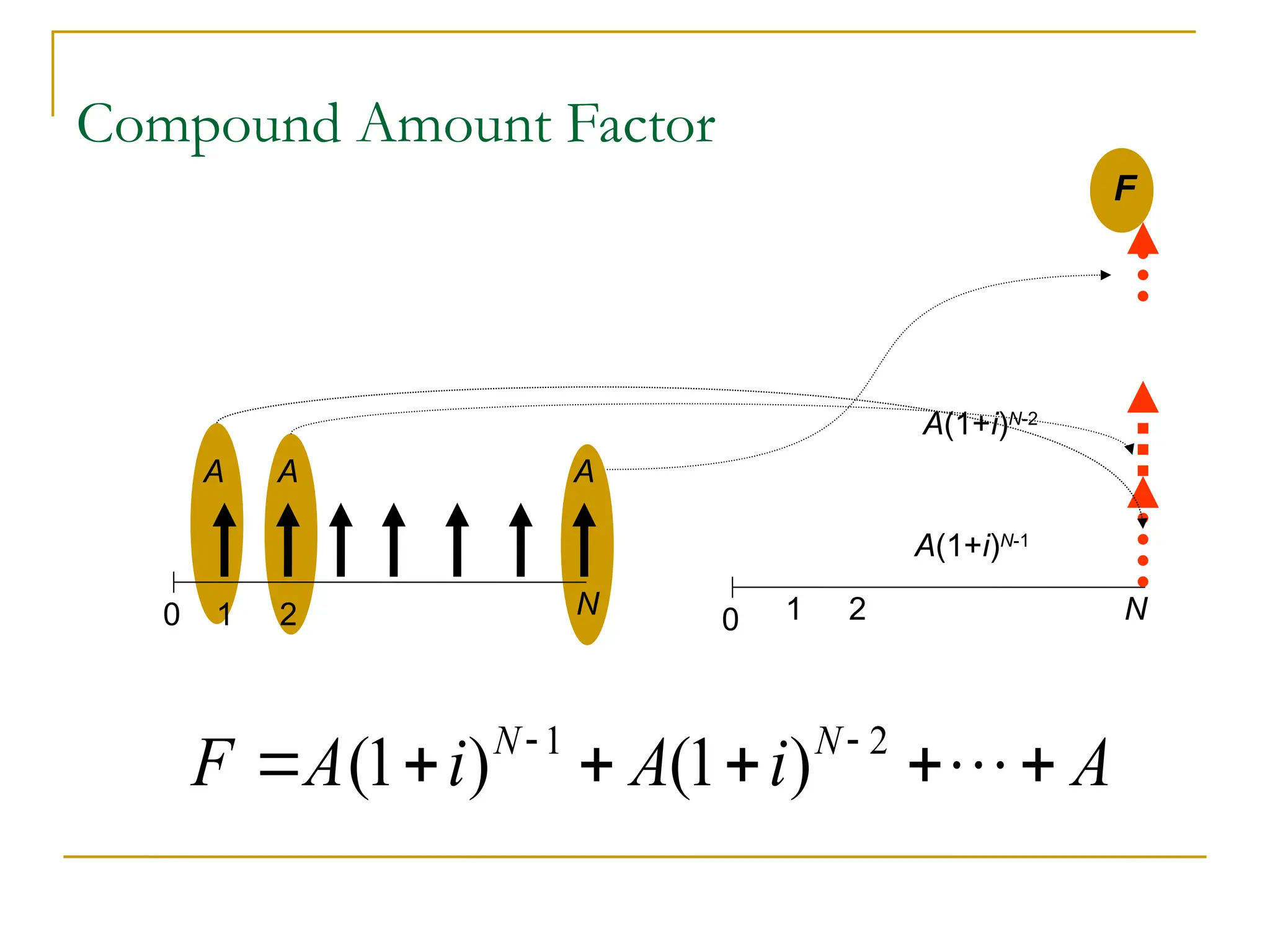

Equal Payment Series– Compound Amount

Factor

0 1 2 N

0 1 2 N

A A A

F

0 1 2

N

A A A

F

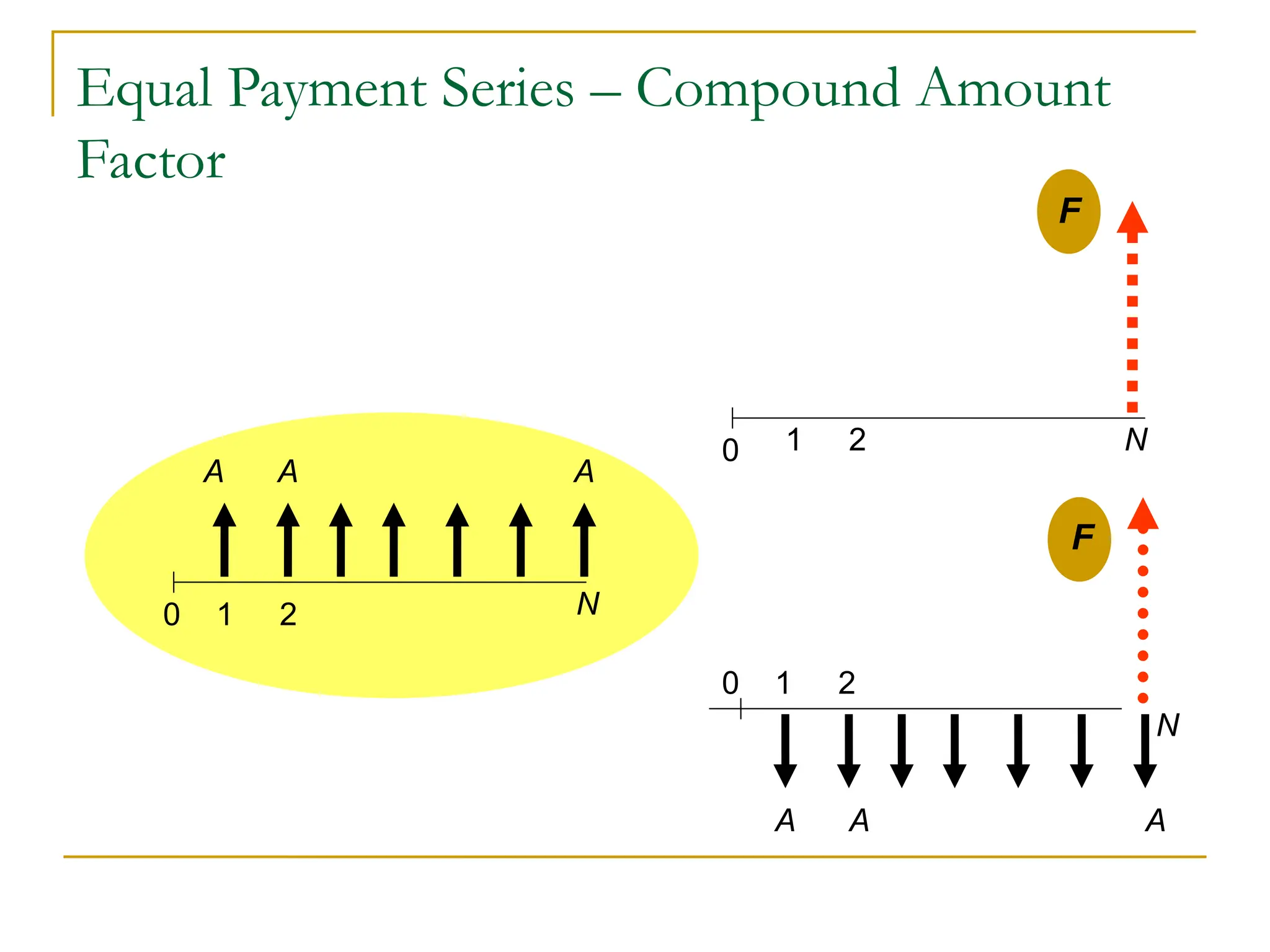

33.

Compound Amount Factor

01 2 N 0 1 2 N

A A A

F

A(1+i)N-1

A(1+i)N-2

1 2

(1 ) (1 )

N N

F A i A i A

34.

Uniform Series CompoundAmount Factor

This factor is used to calculate a future single

sum, F, that is equivalent to a uniform series

of equal end of period payments, A.

35.

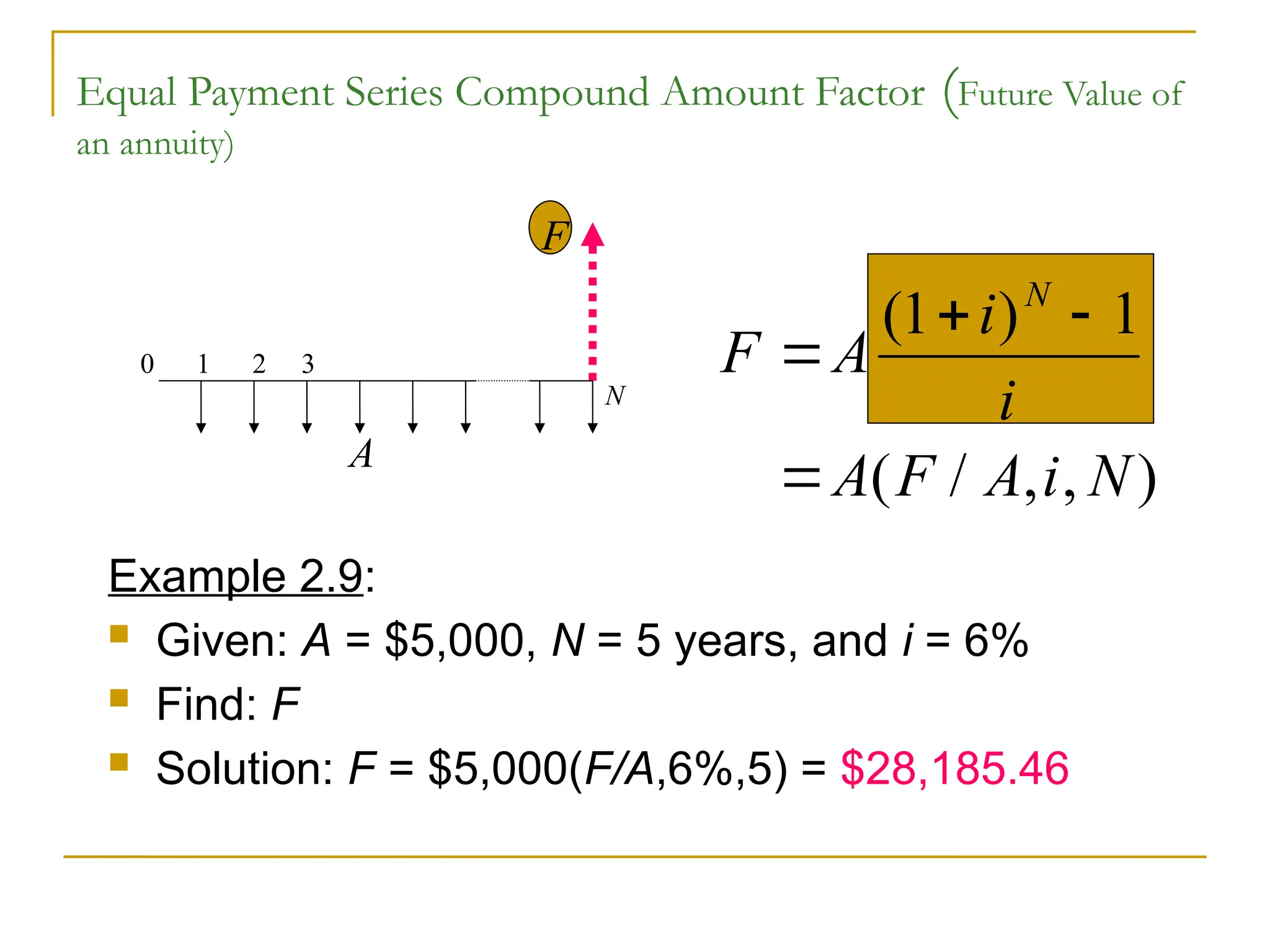

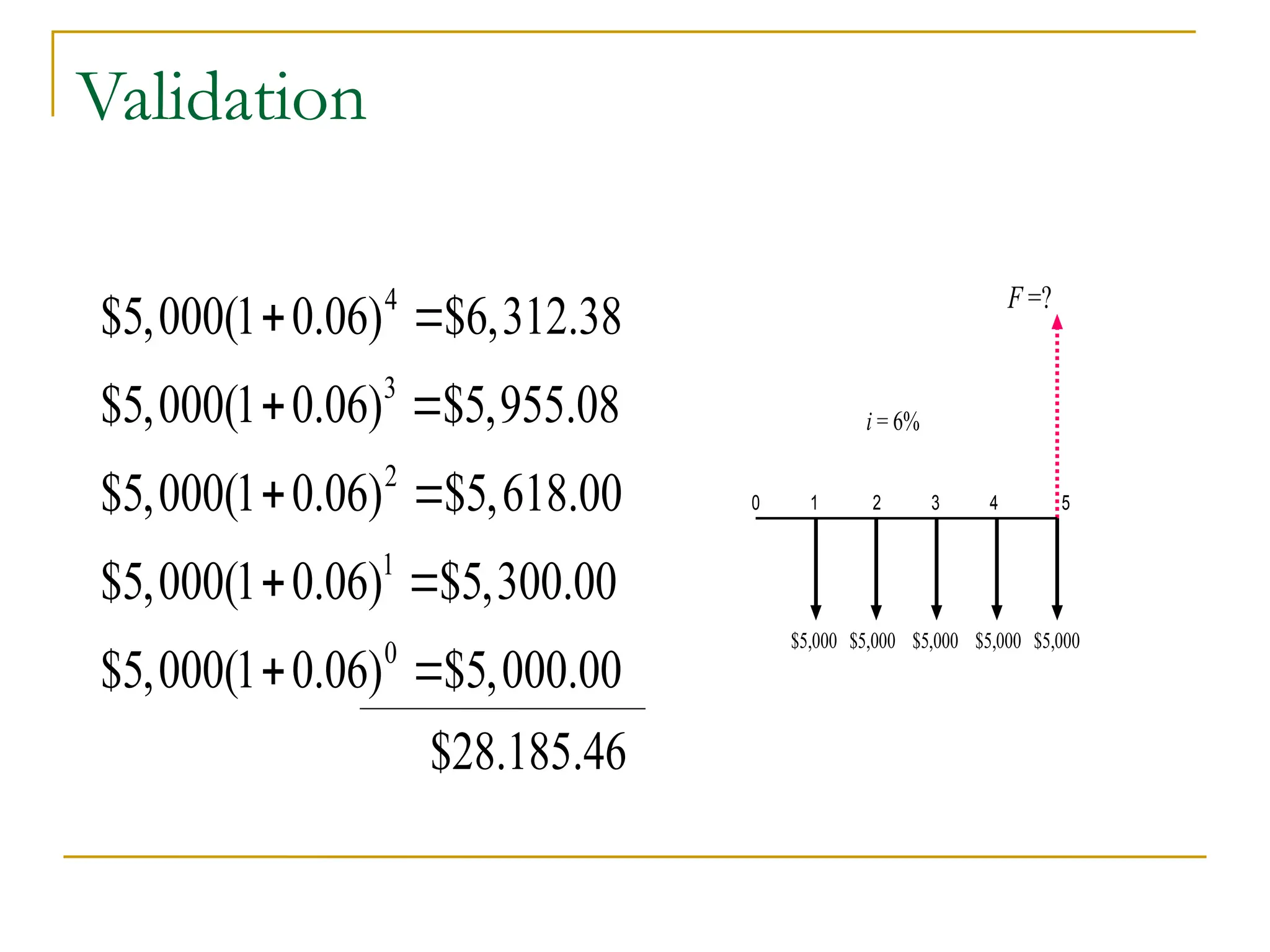

Equal Payment SeriesCompound Amount Factor (Future Value of

an annuity)

F A

i

i

A F A i N

N

( )

( / , , )

1 1

Example 2.9:

Given: A = $5,000, N = 5 years, and i = 6%

Find: F

Solution: F = $5,000(F/A,6%,5) = $28,185.46

0 1 2 3

N

F

A

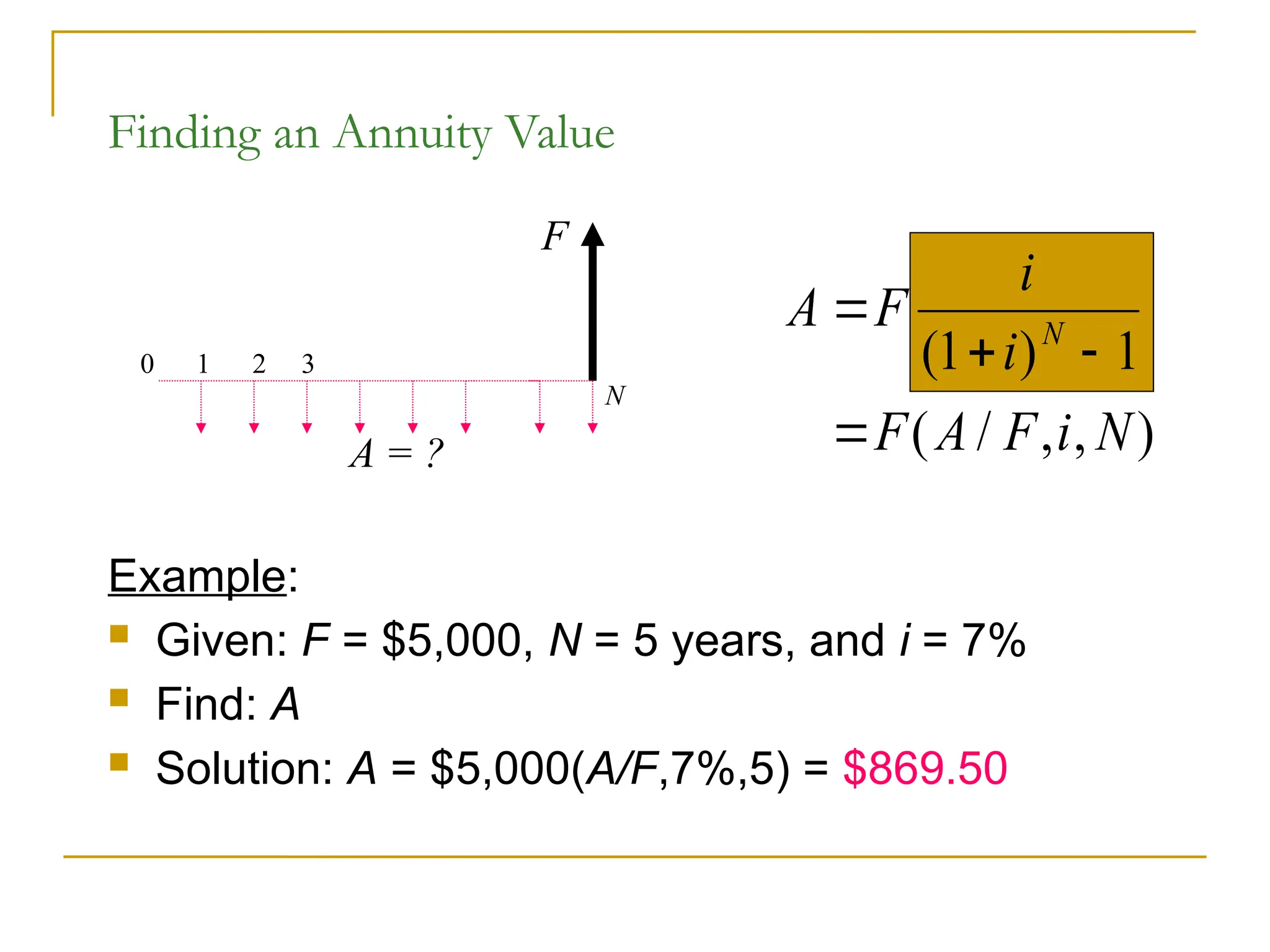

Finding an AnnuityValue

Example:

Given: F = $5,000, N = 5 years, and i = 7%

Find: A

Solution: A = $5,000(A/F,7%,5) = $869.50

0 1 2 3

N

F

A = ?

A F

i

i

F A F i N

N

( )

( / , , )

1 1

38.

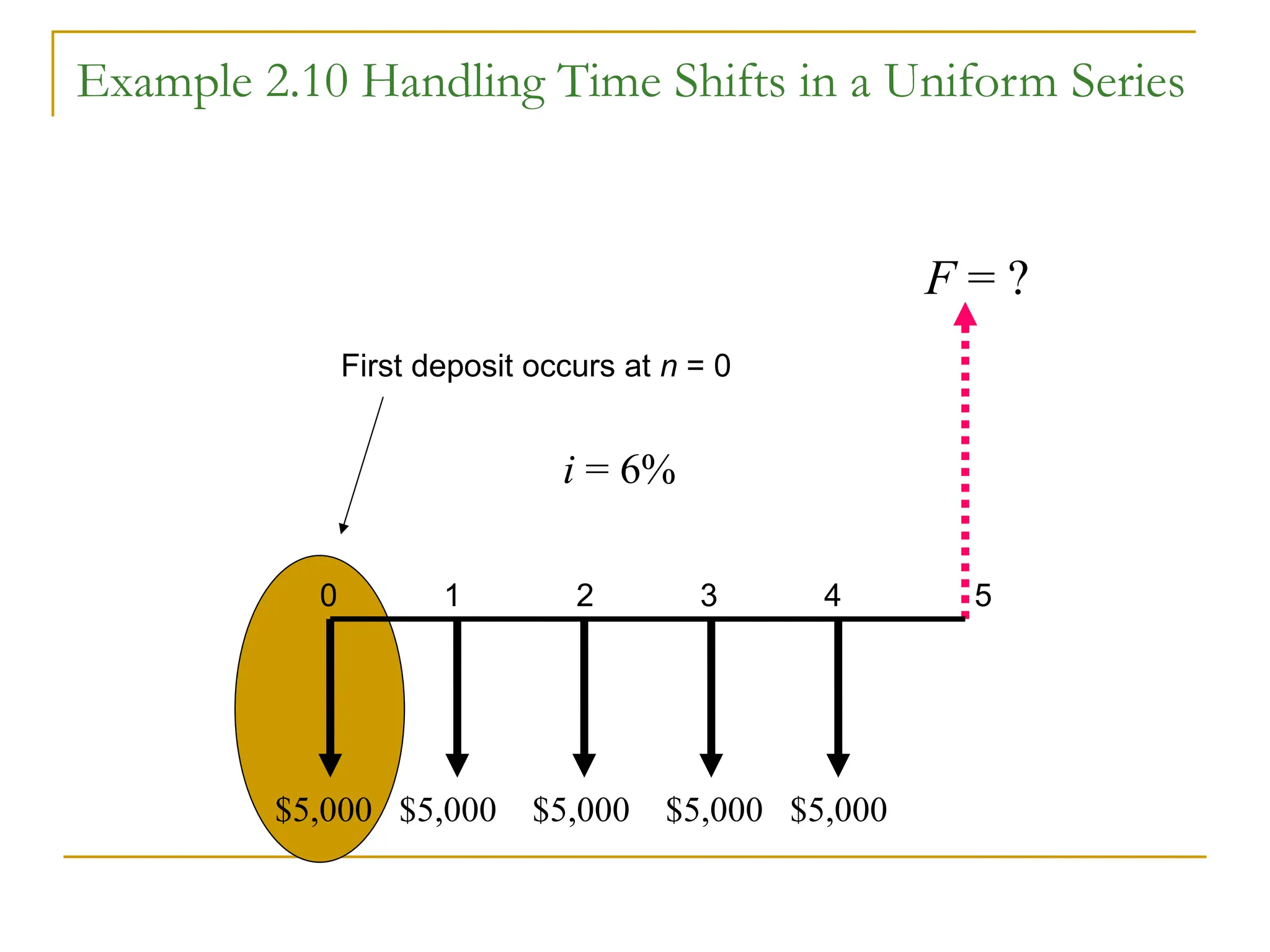

Example 2.10 HandlingTime Shifts in a Uniform Series

F = ?

0 1 2 3 4 5

$5,000 $5,000 $5,000 $5,000 $5,000

i = 6%

First deposit occurs at n = 0

39.

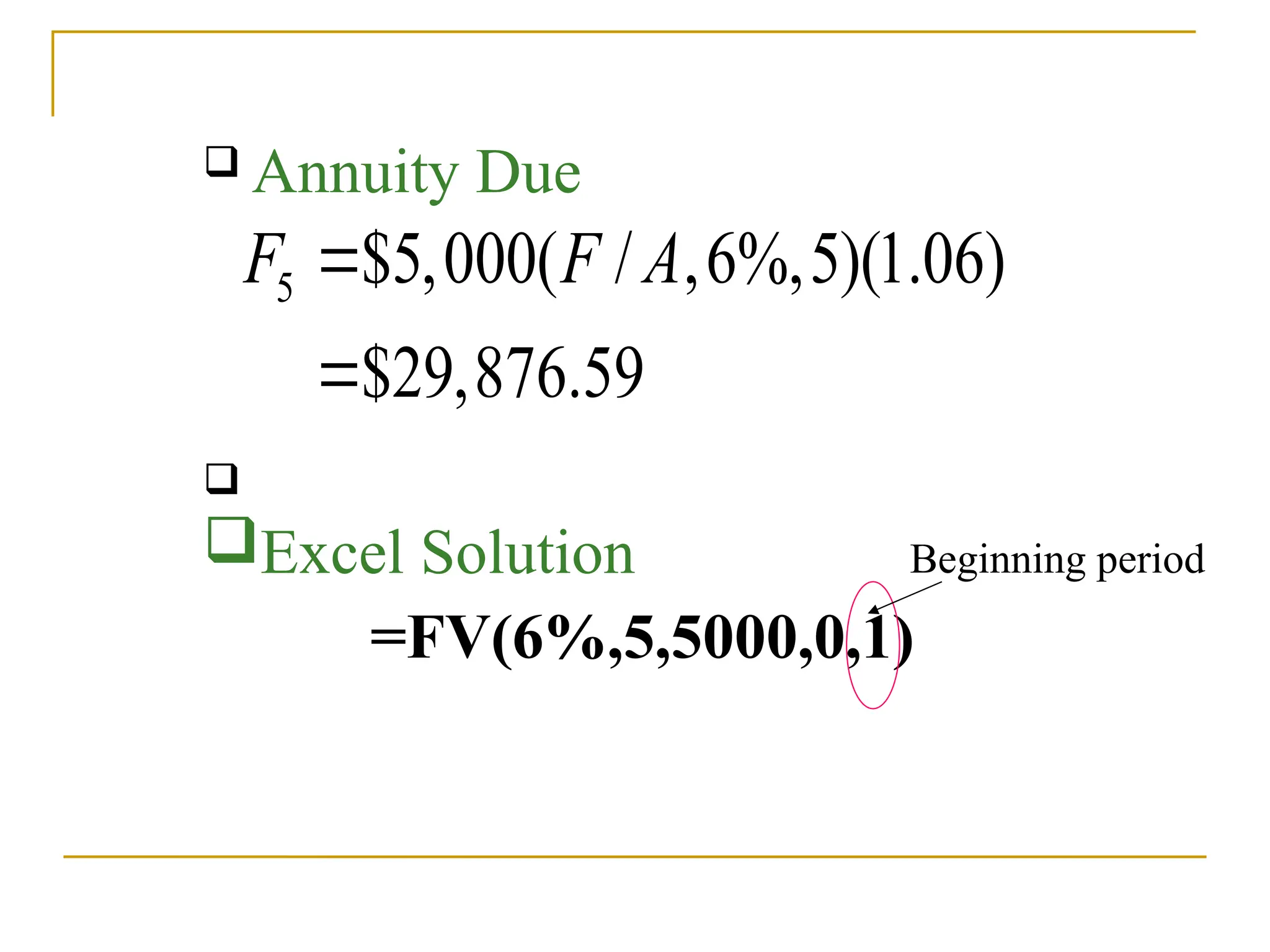

5 $5,000( /,6%,5)(1.06)

$29,876.59

F F A

Annuity Due

Excel Solution

=FV(6%,5,5000,0,1)

Beginning period

40.

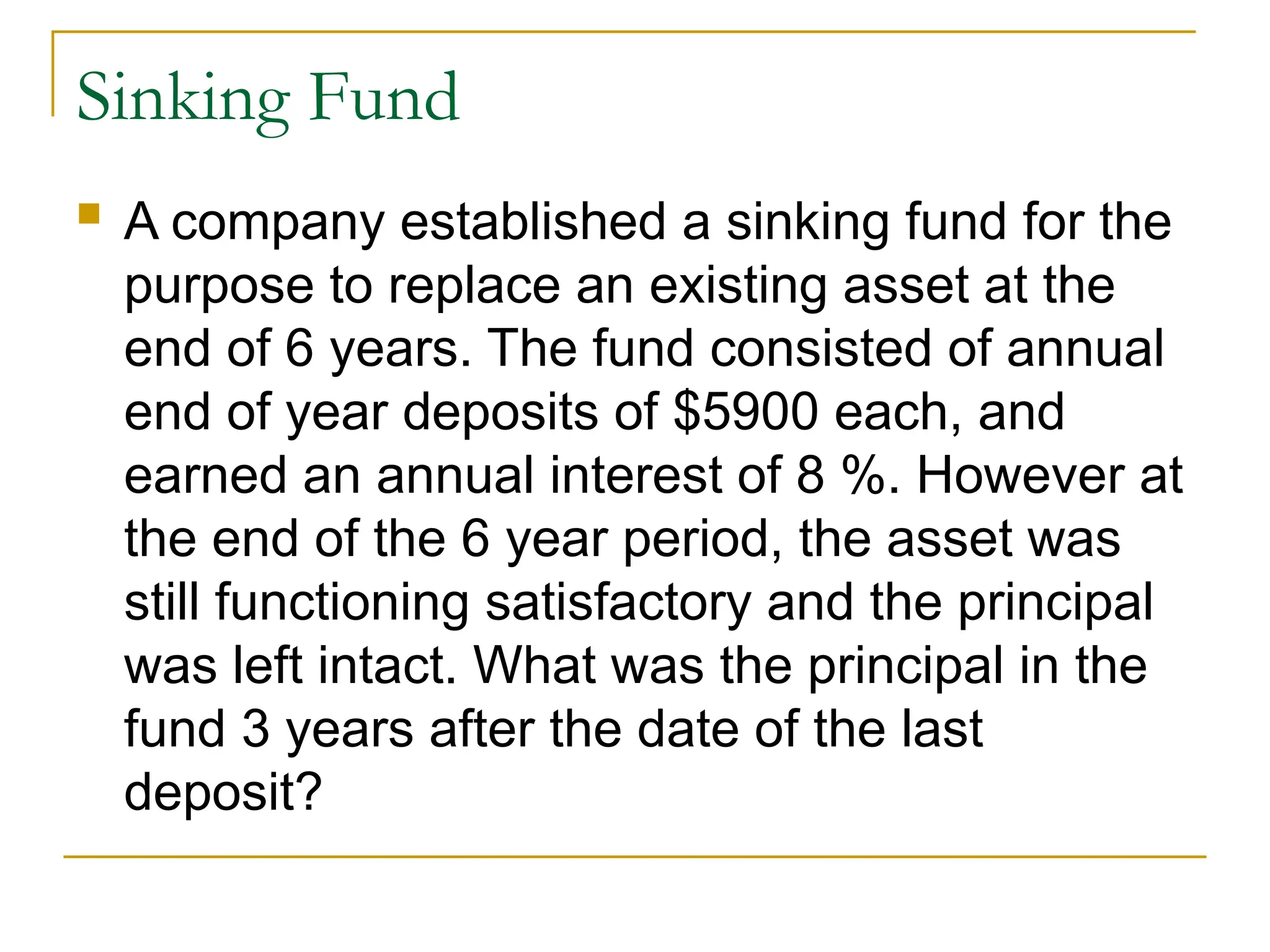

Sinking Fund

Acompany established a sinking fund for the

purpose to replace an existing asset at the

end of 6 years. The fund consisted of annual

end of year deposits of $5900 each, and

earned an annual interest of 8 %. However at

the end of the 6 year period, the asset was

still functioning satisfactory and the principal

was left intact. What was the principal in the

fund 3 years after the date of the last

deposit?

41.

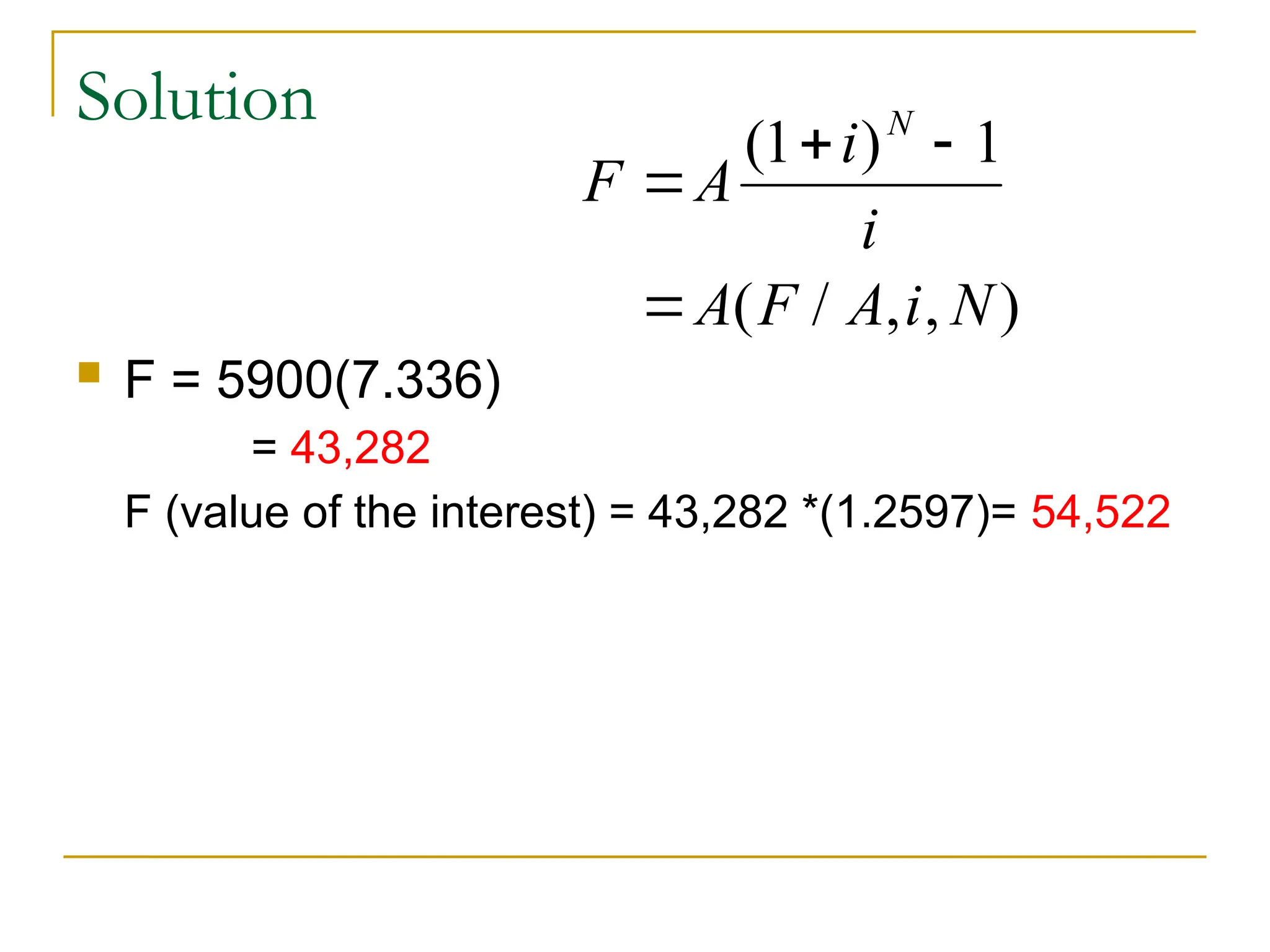

Solution

F =5900(7.336)

= 43,282

F (value of the interest) = 43,282 *(1.2597)= 54,522

F A

i

i

A F A i N

N

( )

( / , , )

1 1

42.

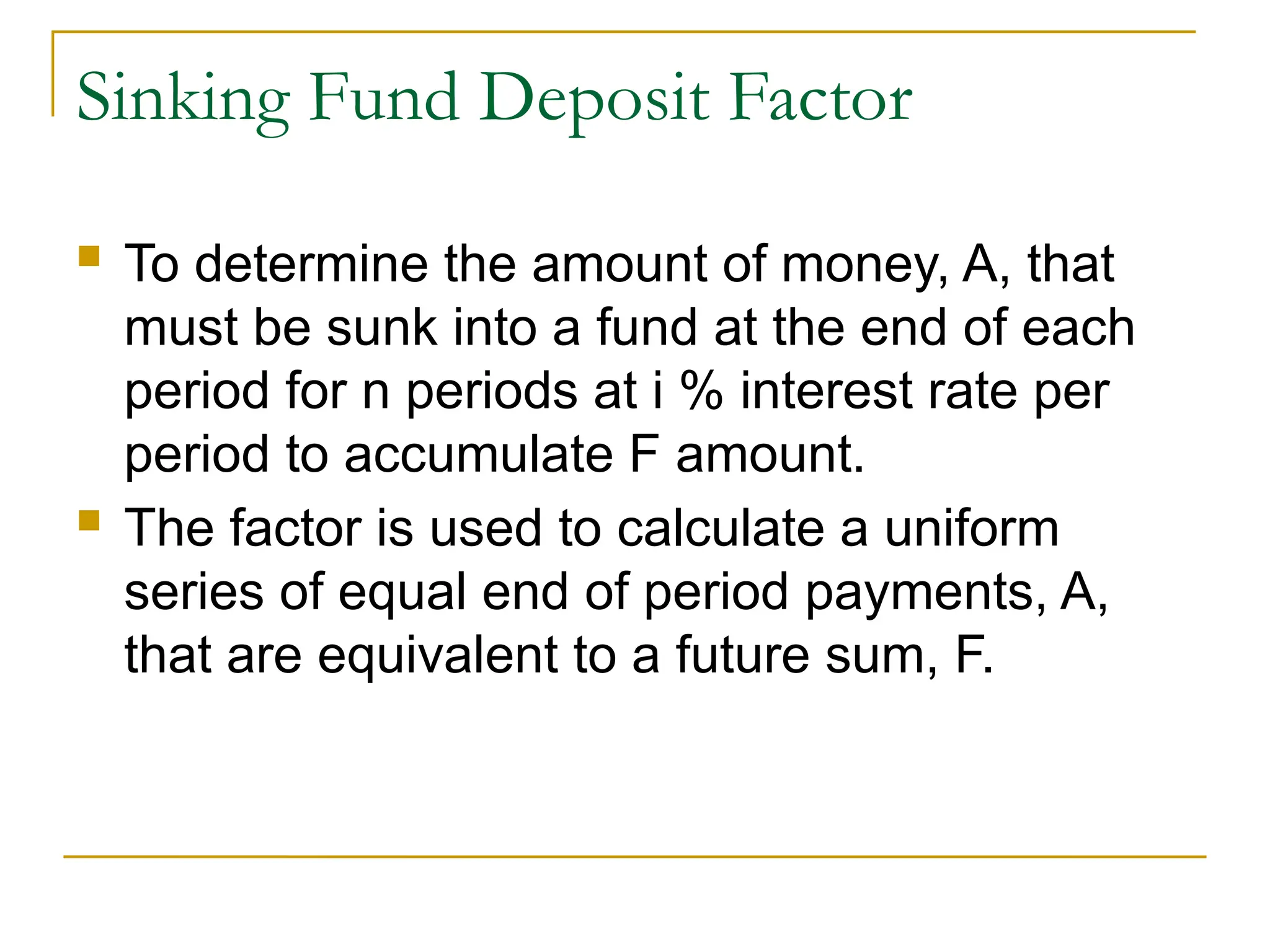

Sinking Fund DepositFactor

To determine the amount of money, A, that

must be sunk into a fund at the end of each

period for n periods at i % interest rate per

period to accumulate F amount.

The factor is used to calculate a uniform

series of equal end of period payments, A,

that are equivalent to a future sum, F.

43.

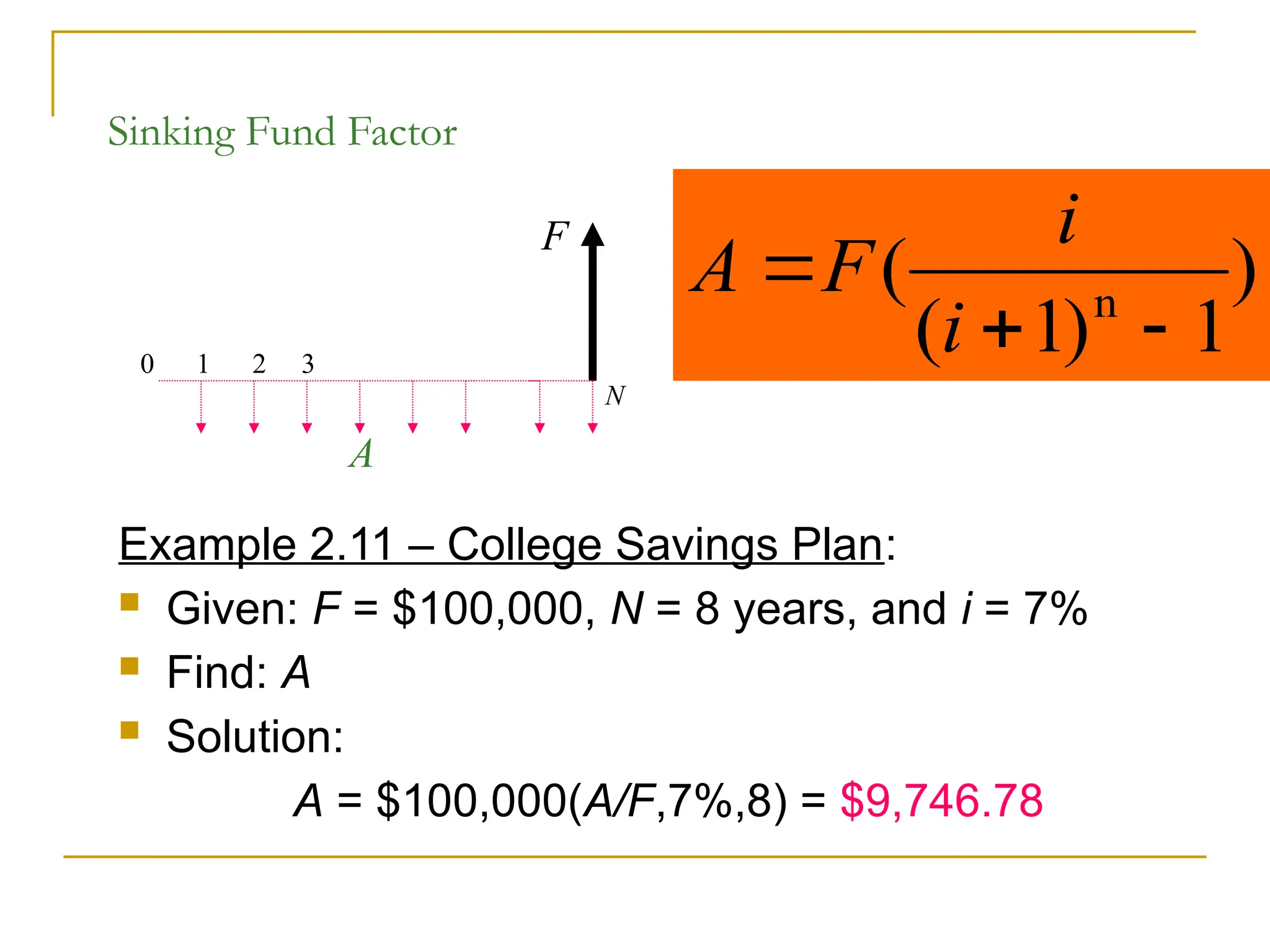

Sinking Fund Factor

Example2.11 – College Savings Plan:

Given: F = $100,000, N = 8 years, and i = 7%

Find: A

Solution:

A = $100,000(A/F,7%,8) = $9,746.78

0 1 2 3

N

F

A

)

1

)

1

(

( n

i

i

F

A

44.

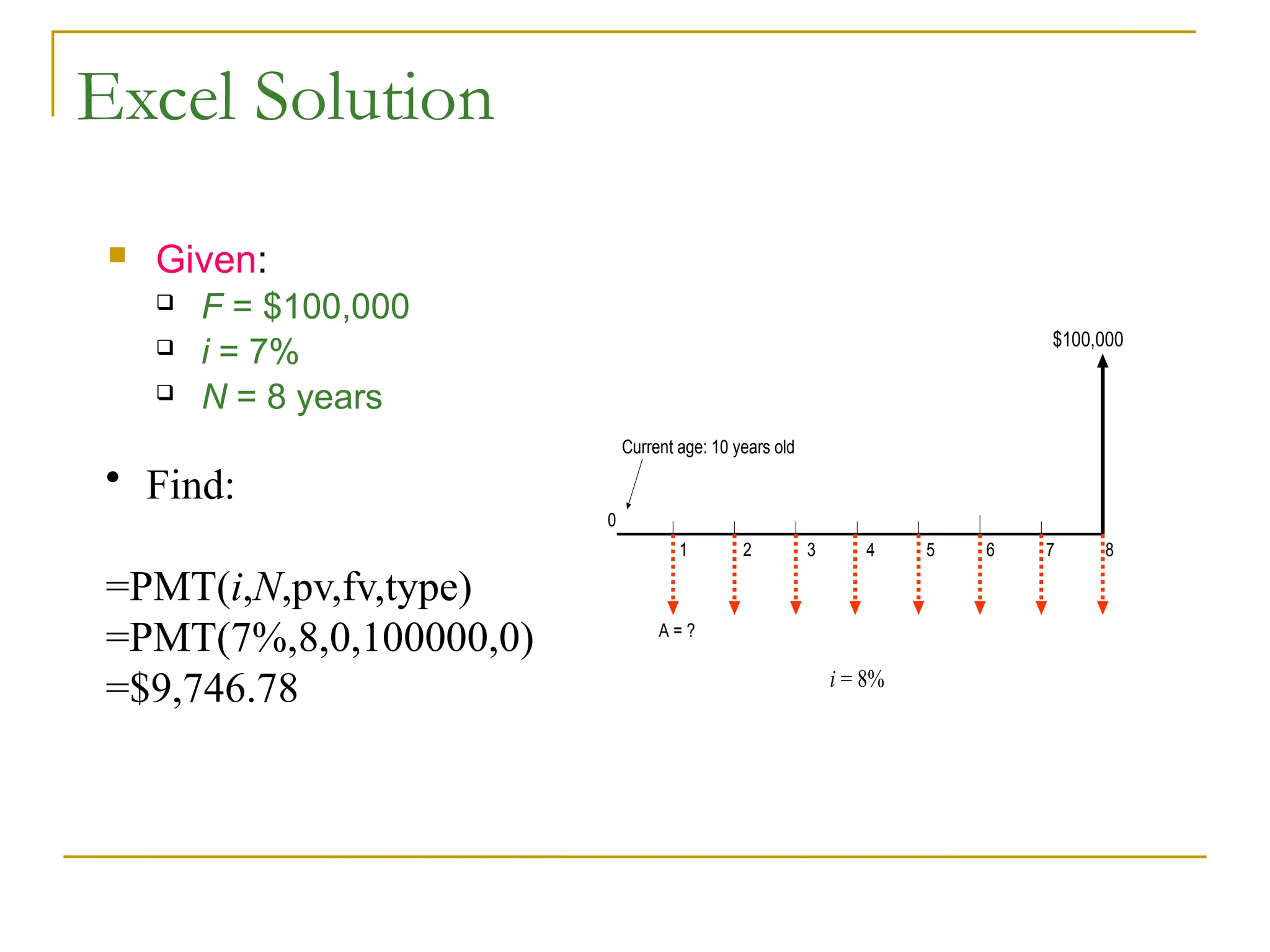

Excel Solution

Given:

F = $100,000

i = 7%

N = 8 years

0

1 2 3 4 5 6 7 8

$100,000

i = 8%

A = ?

Current age: 10 years old

• Find:

=PMT(i,N,pv,fv,type)

=PMT(7%,8,0,100000,0)

=$9,746.78

45.

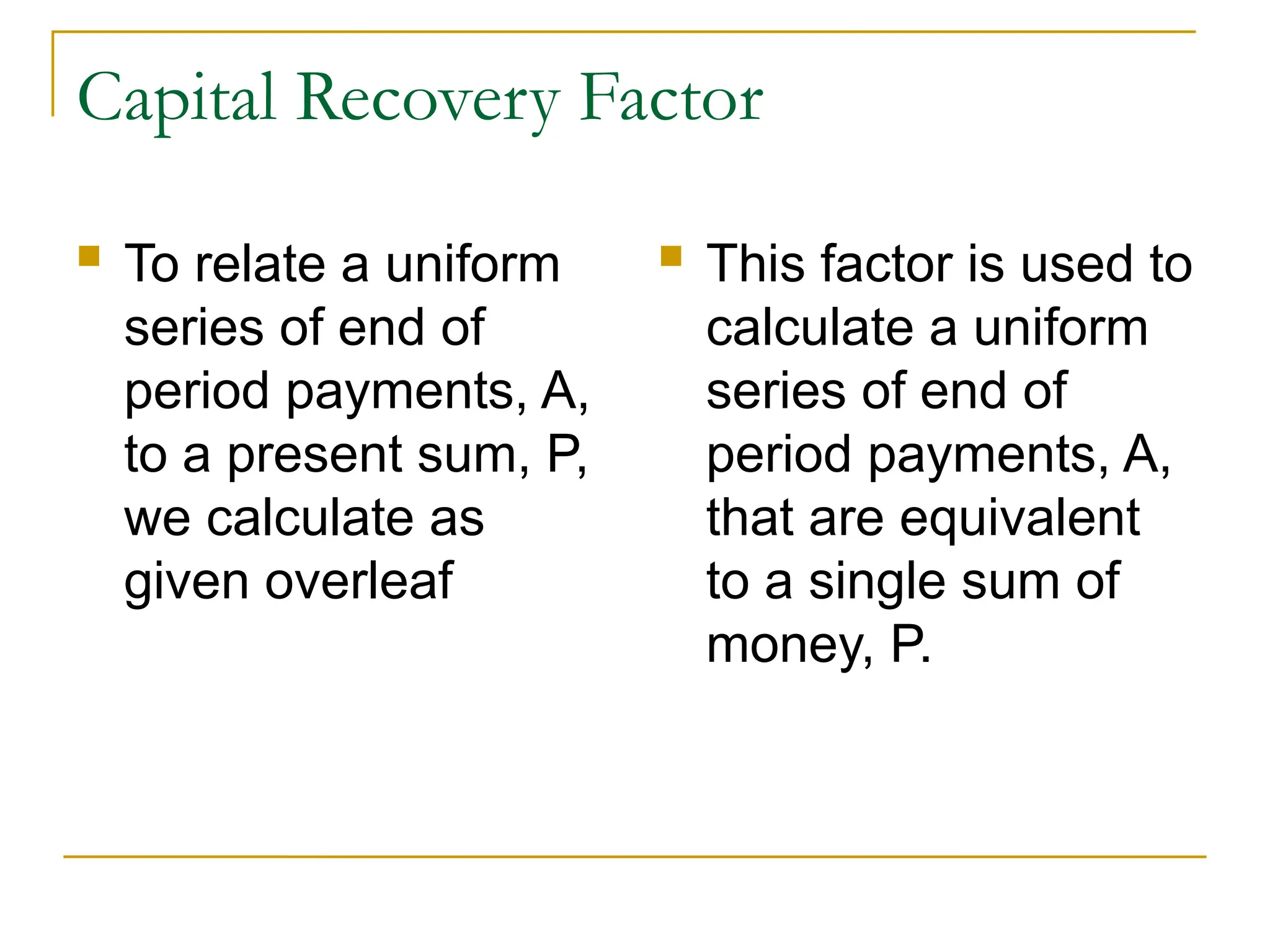

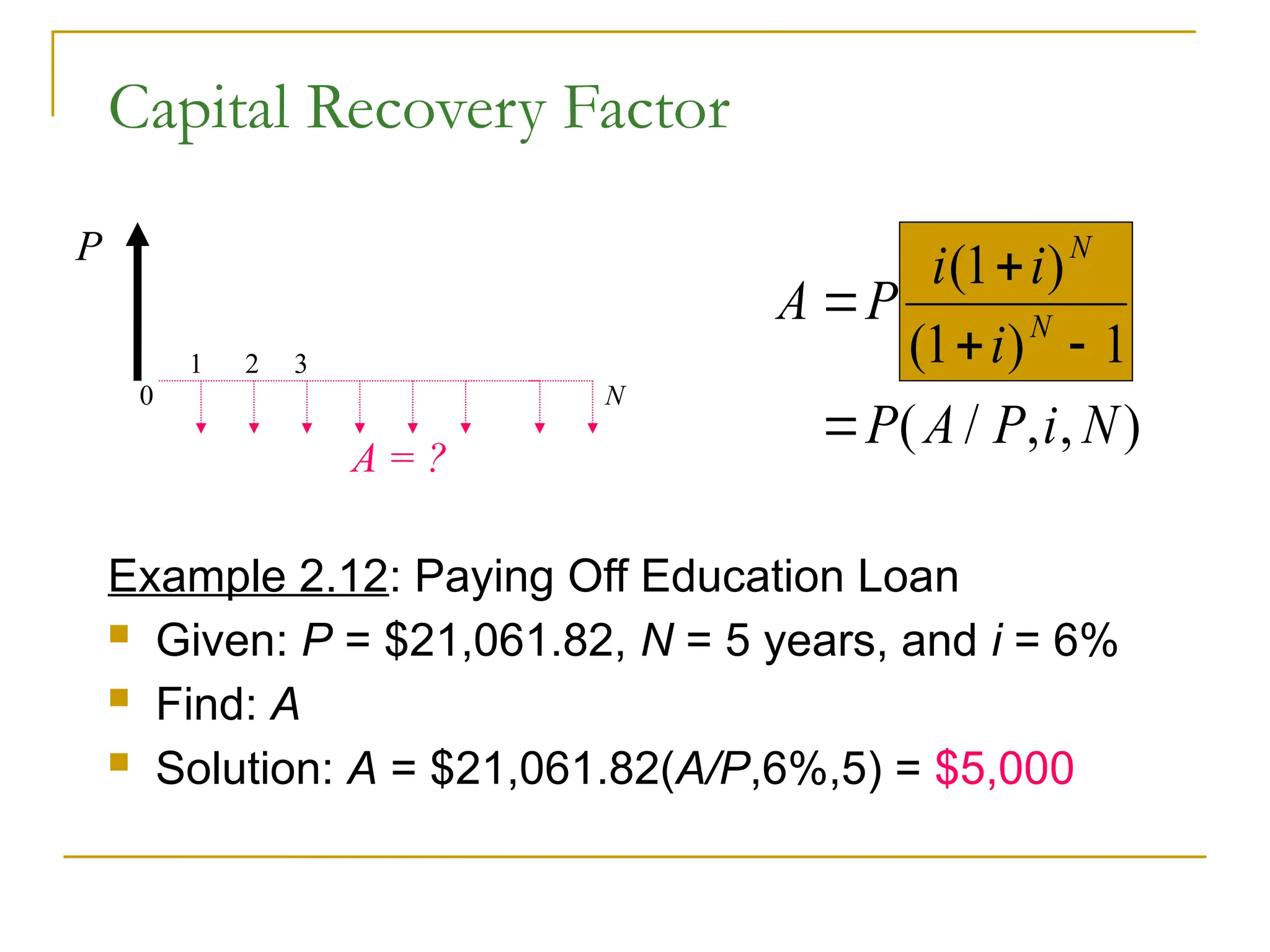

Capital Recovery Factor

To relate a uniform

series of end of

period payments, A,

to a present sum, P,

we calculate as

given overleaf

This factor is used to

calculate a uniform

series of end of

period payments, A,

that are equivalent

to a single sum of

money, P.

46.

Capital Recovery Factor

Example2.12: Paying Off Education Loan

Given: P = $21,061.82, N = 5 years, and i = 6%

Find: A

Solution: A = $21,061.82(A/P,6%,5) = $5,000

1 2 3

N

P

A = ?

0

A P

i i

i

P A P i N

N

N

( )

( )

( / , , )

1

1 1

47.

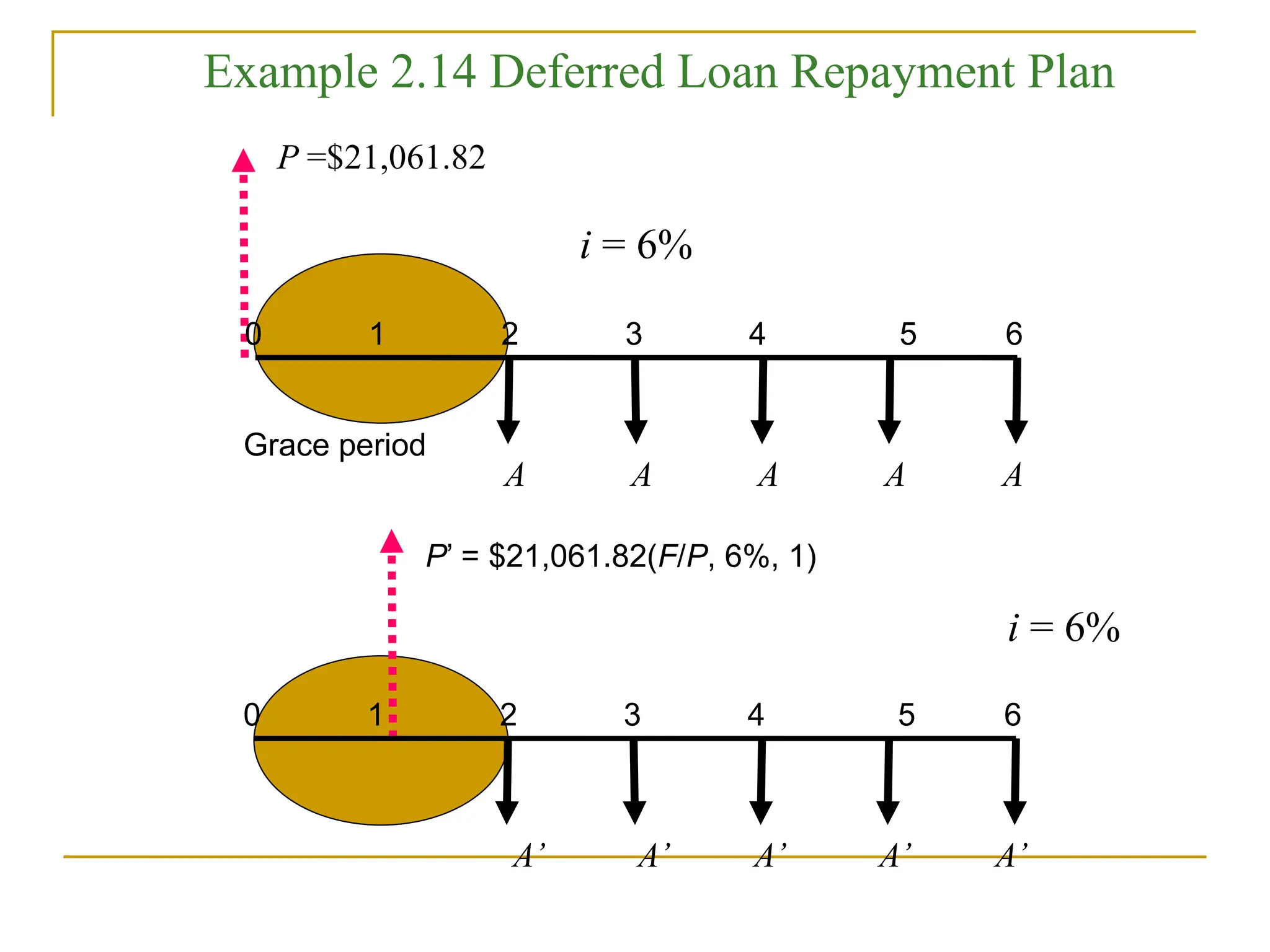

P =$21,061.82

0 12 3 4 5 6

A A A A A

i = 6%

0 1 2 3 4 5 6

A’ A’ A’ A’ A’

i = 6%

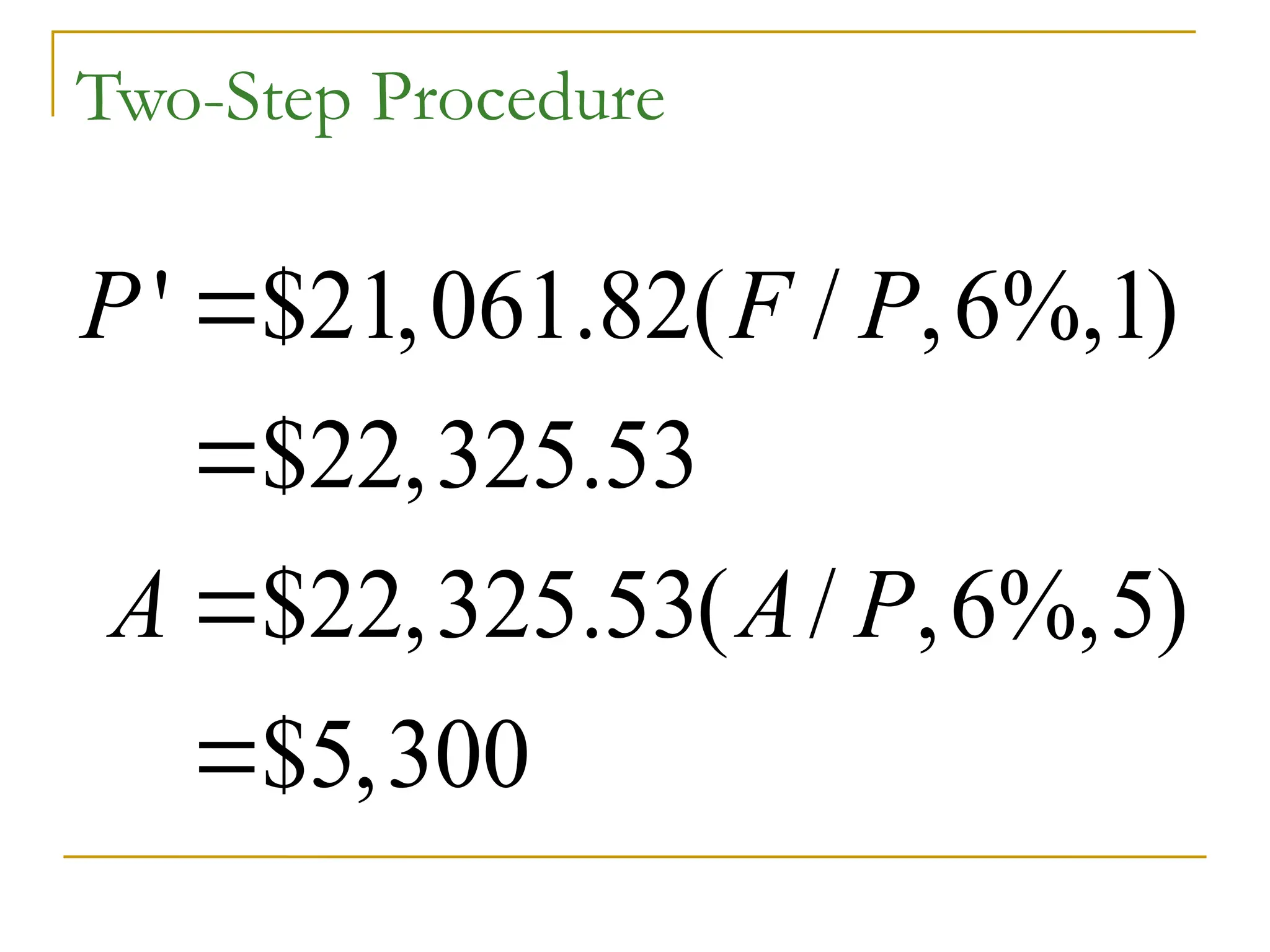

P’ = $21,061.82(F/P, 6%, 1)

Grace period

Example 2.14 Deferred Loan Repayment Plan

Uniform Series PresentWorth

To determine the present single value sum of

money, P, that is equivalent to a uniform

series of equal payments, A, for n periods at i

% interest per period;

This factor is used to calculate the present

sum, P, that is equivalent to a uniform series

of equal end of period payments, A.

50.

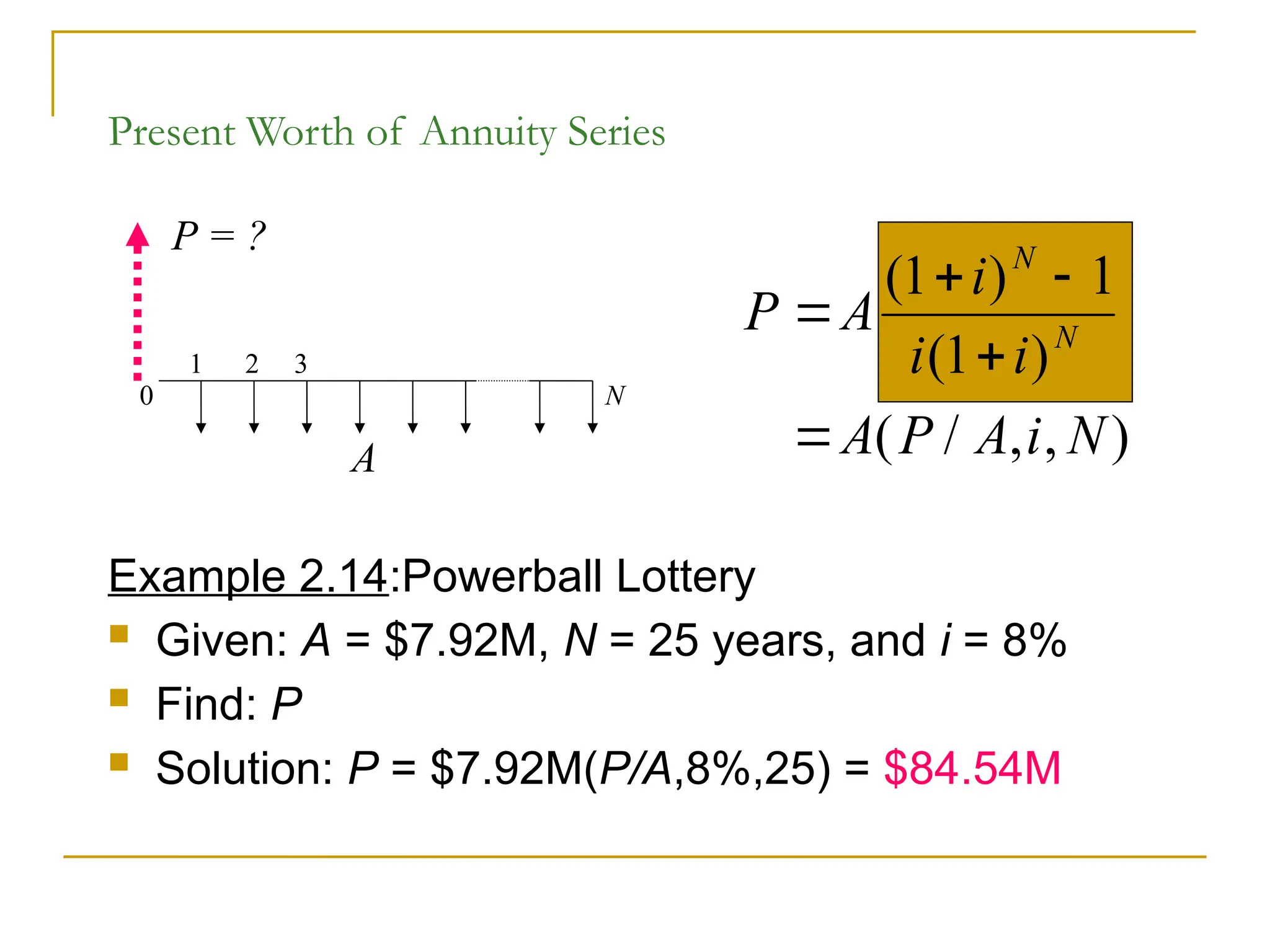

Present Worth ofAnnuity Series

Example 2.14:Powerball Lottery

Given: A = $7.92M, N = 25 years, and i = 8%

Find: P

Solution: P = $7.92M(P/A,8%,25) = $84.54M

1 2 3

N

P = ?

A

0

P A

i

i i

A P A i N

N

N

( )

( )

( / , , )

1 1

1

51.

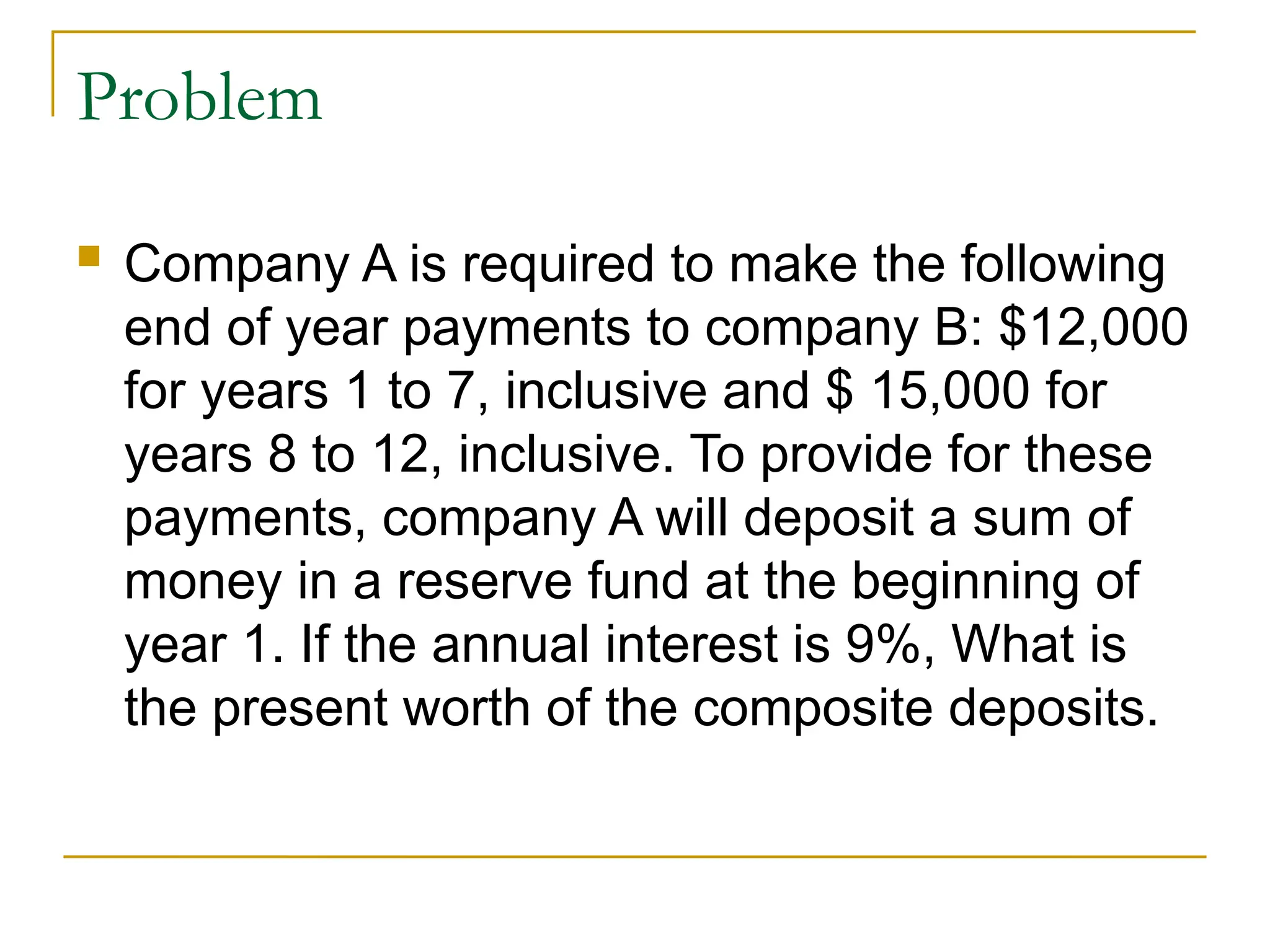

Problem

Company Ais required to make the following

end of year payments to company B: $12,000

for years 1 to 7, inclusive and $ 15,000 for

years 8 to 12, inclusive. To provide for these

payments, company A will deposit a sum of

money in a reserve fund at the beginning of

year 1. If the annual interest is 9%, What is

the present worth of the composite deposits.

52.

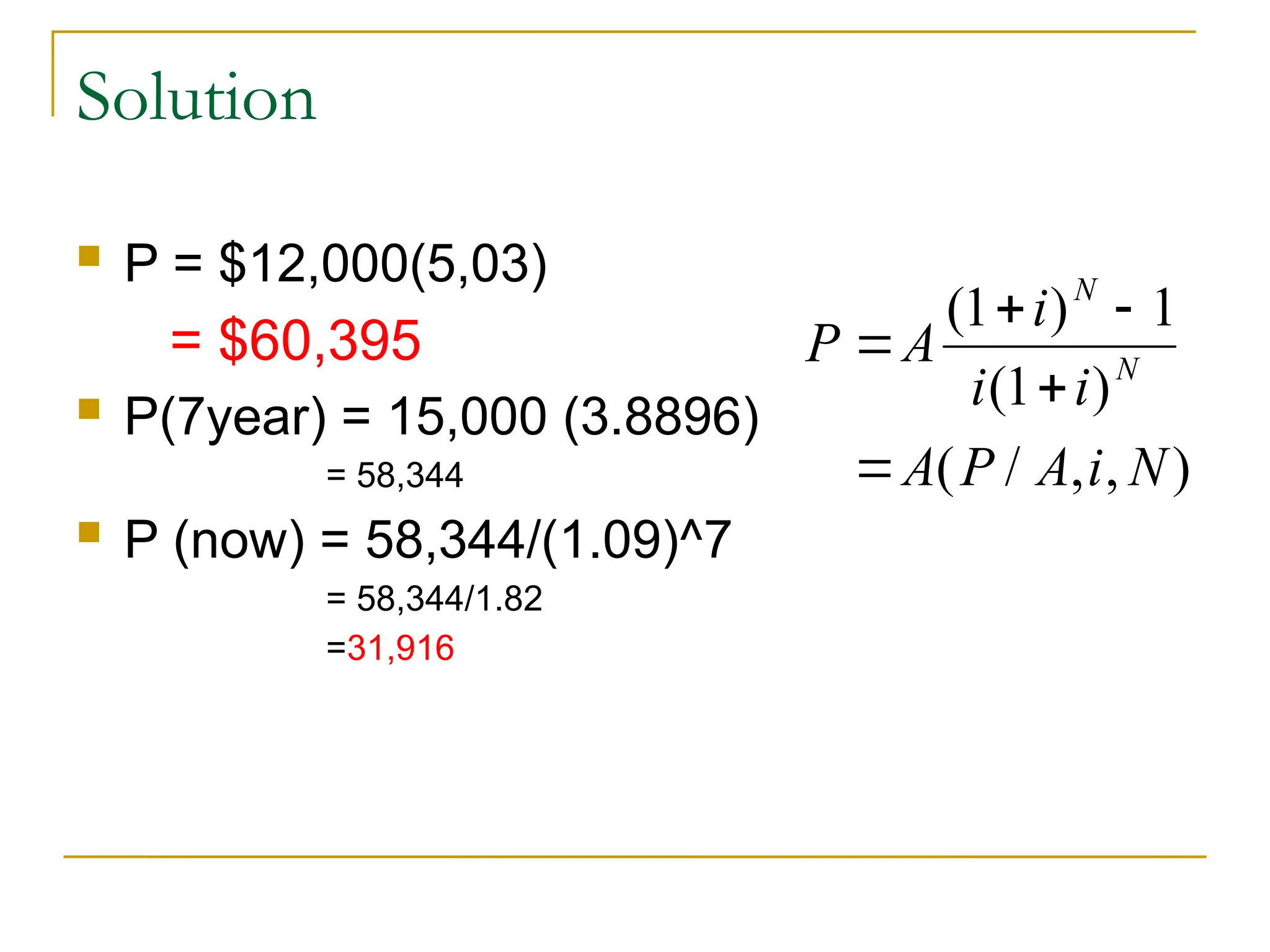

Solution

P =$12,000(5,03)

= $60,395

P(7year) = 15,000 (3.8896)

= 58,344

P (now) = 58,344/(1.09)^7

= 58,344/1.82

=31,916

P A

i

i i

A P A i N

N

N

( )

( )

( / , , )

1 1

1

53.

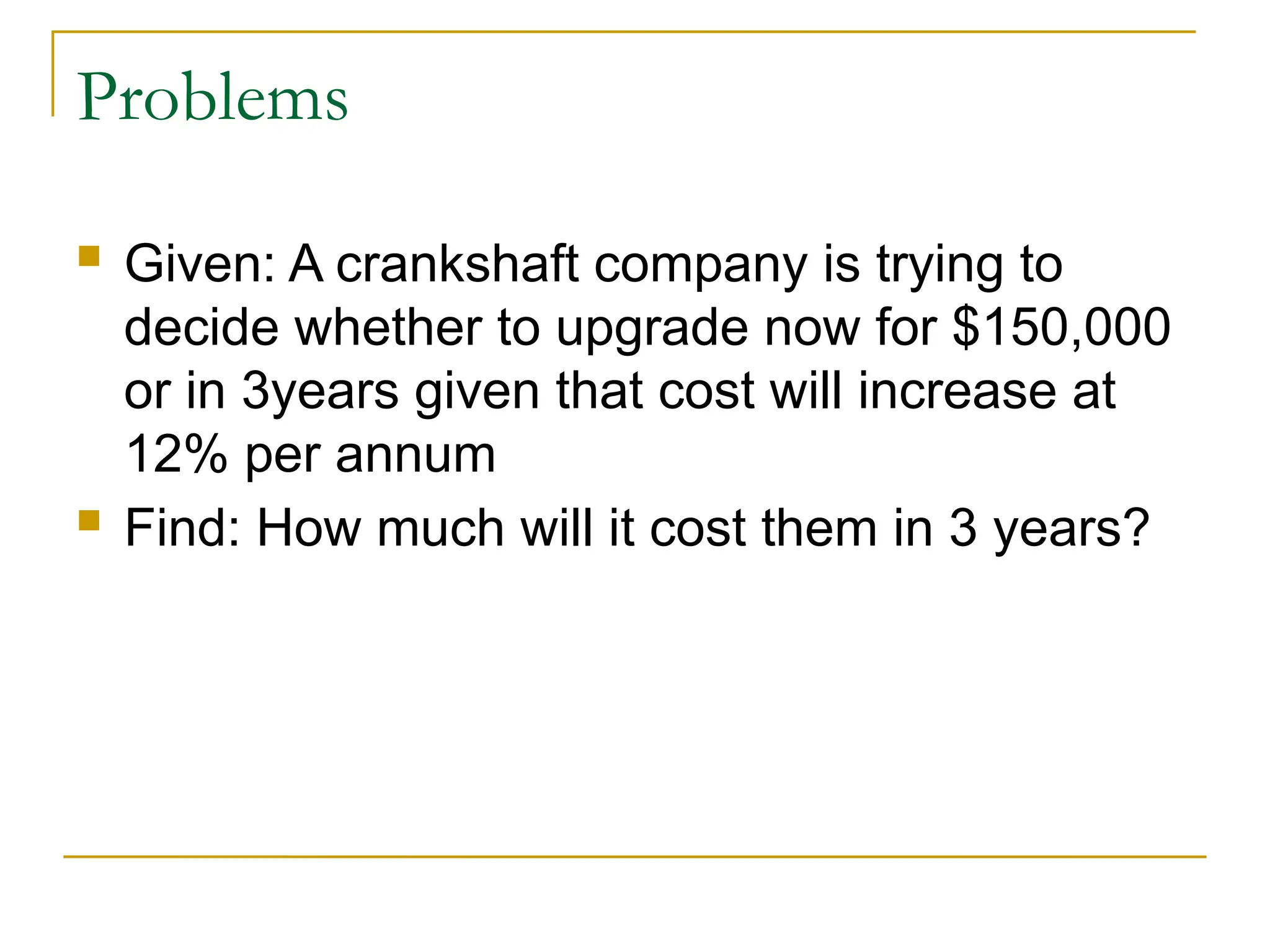

Problems

Given: Acrankshaft company is trying to

decide whether to upgrade now for $150,000

or in 3years given that cost will increase at

12% per annum

Find: How much will it cost them in 3 years?

54.

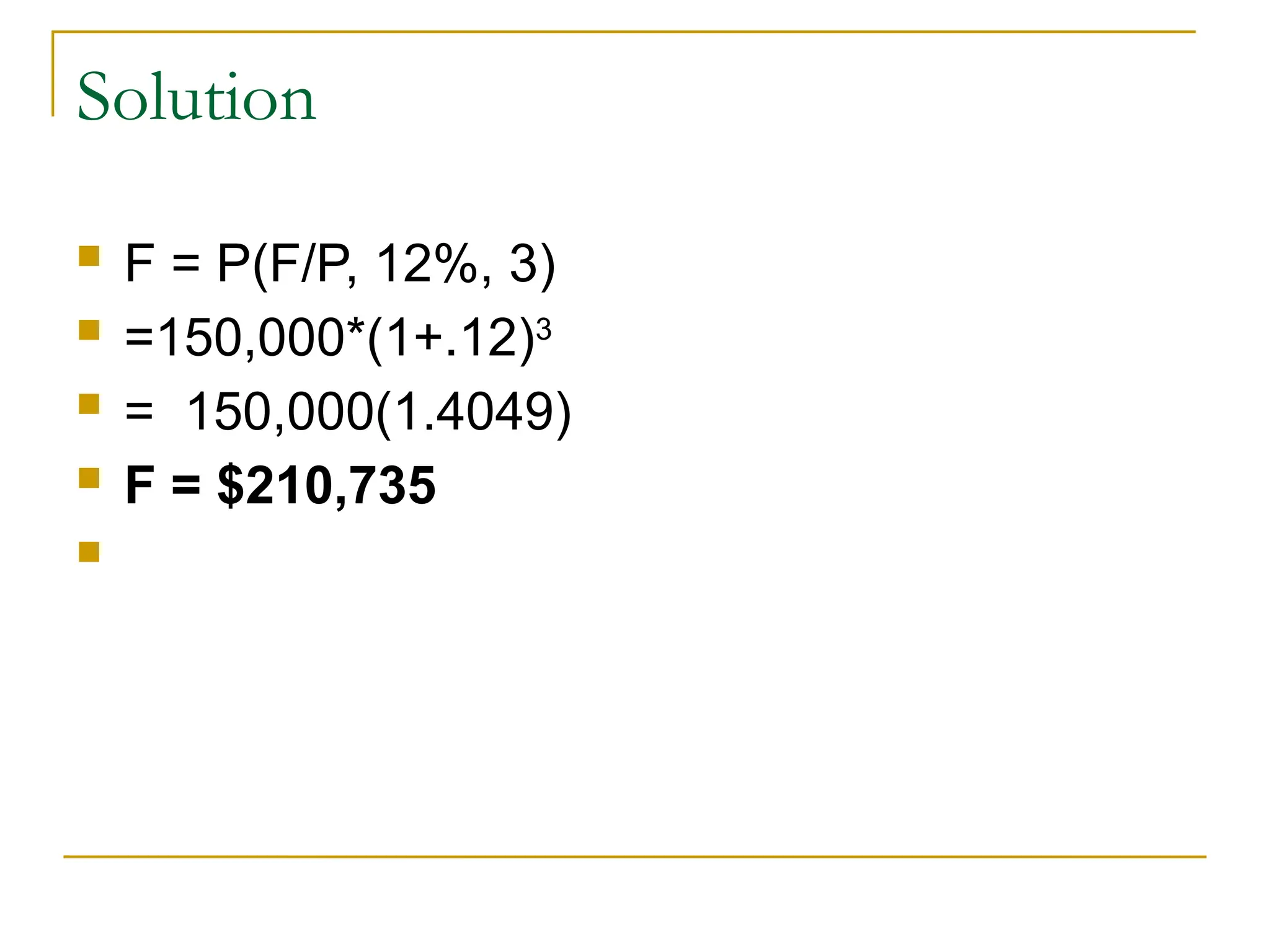

Solution

F =P(F/P, 12%, 3)

=150,000*(1+.12)3

= 150,000(1.4049)

F = $210,735

55.

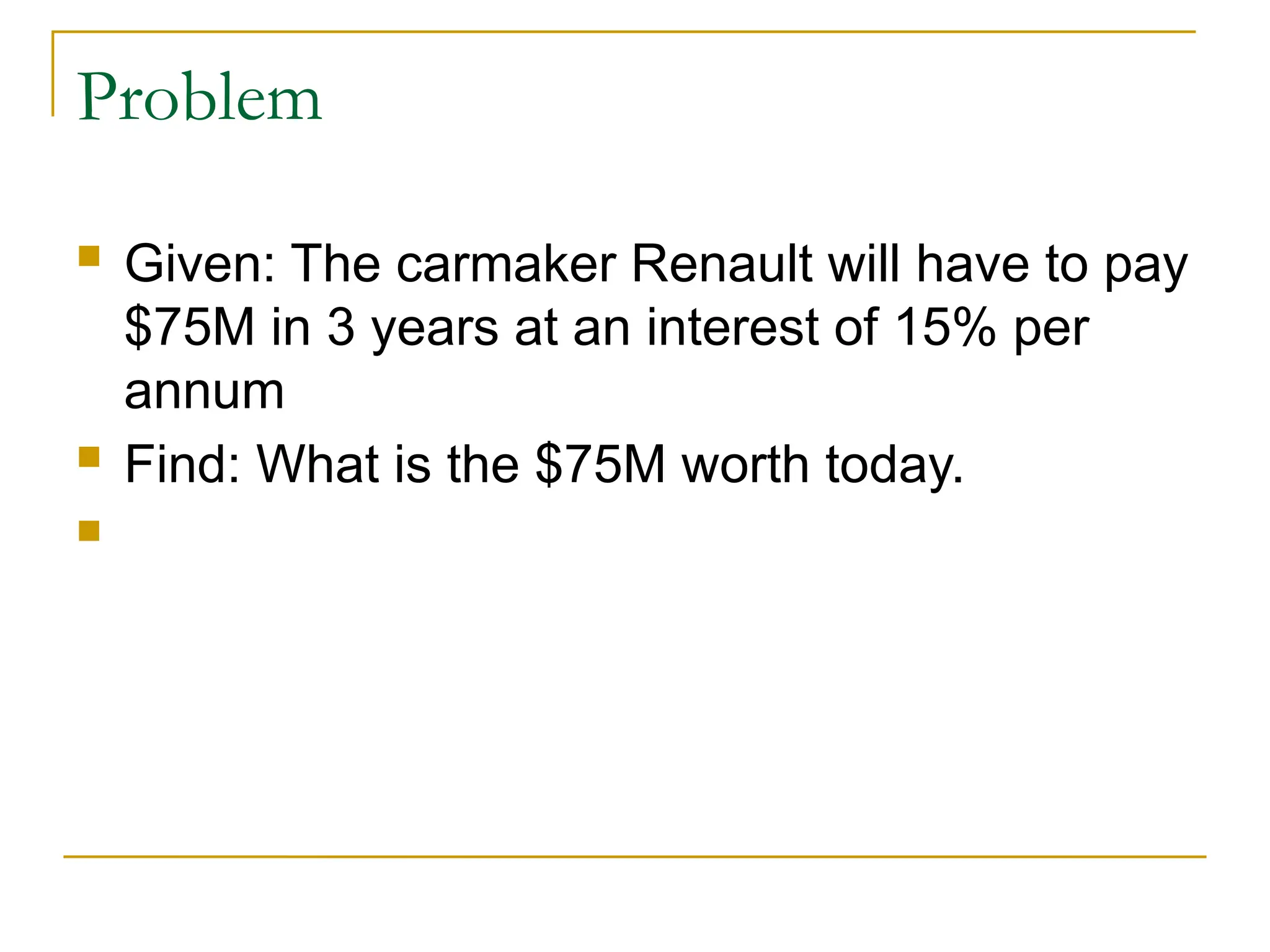

Problem

Given: Thecarmaker Renault will have to pay

$75M in 3 years at an interest of 15% per

annum

Find: What is the $75M worth today.

56.

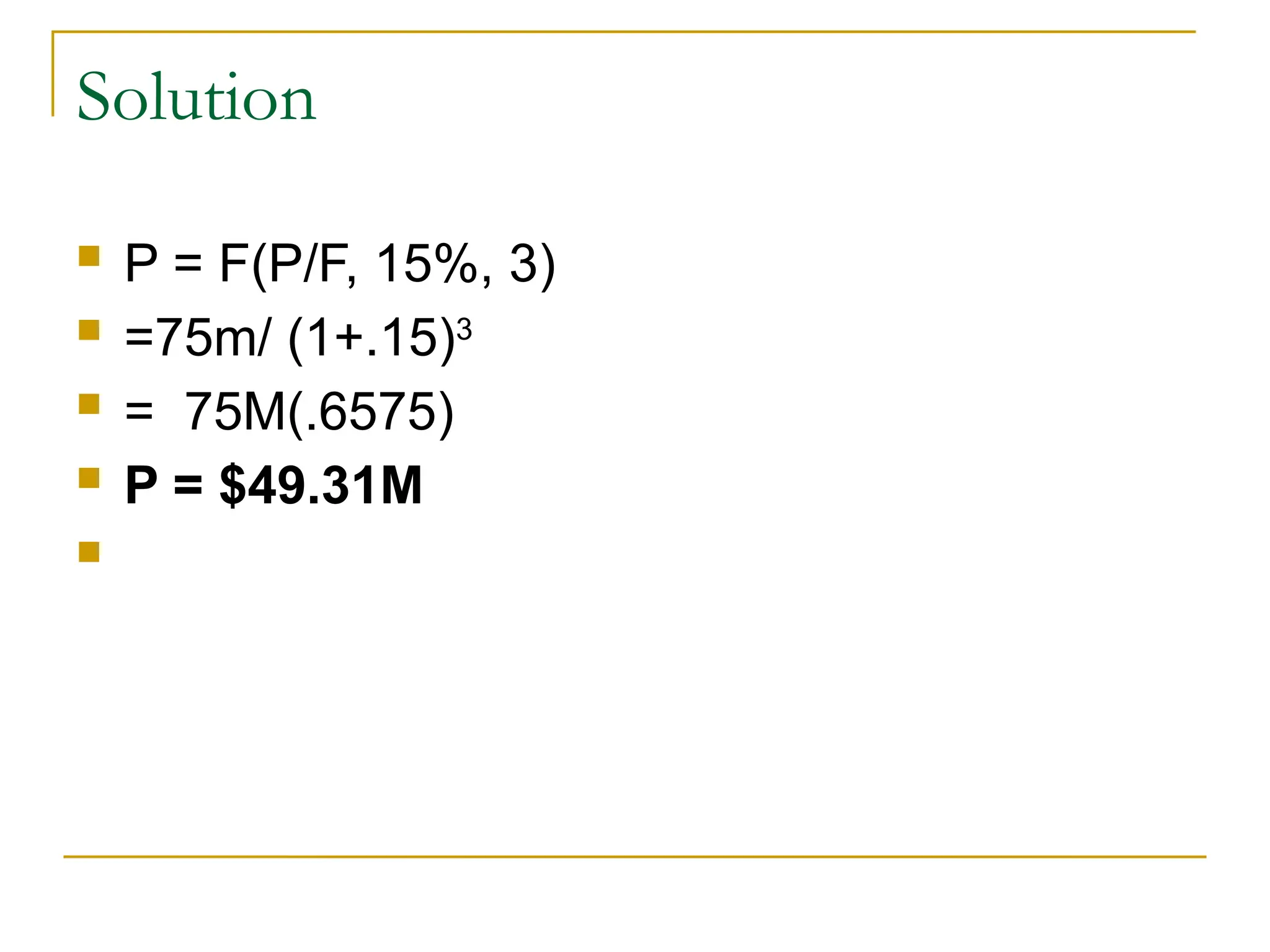

Solution

P =F(P/F, 15%, 3)

=75m/ (1+.15)3

= 75M(.6575)

P = $49.31M

57.

Problem

Given: Anamusement park intends to pays

$55,000 per year for 5 years at 15% per

annum interest.

Find: Using the same amount of money, how

much is that today.

58.

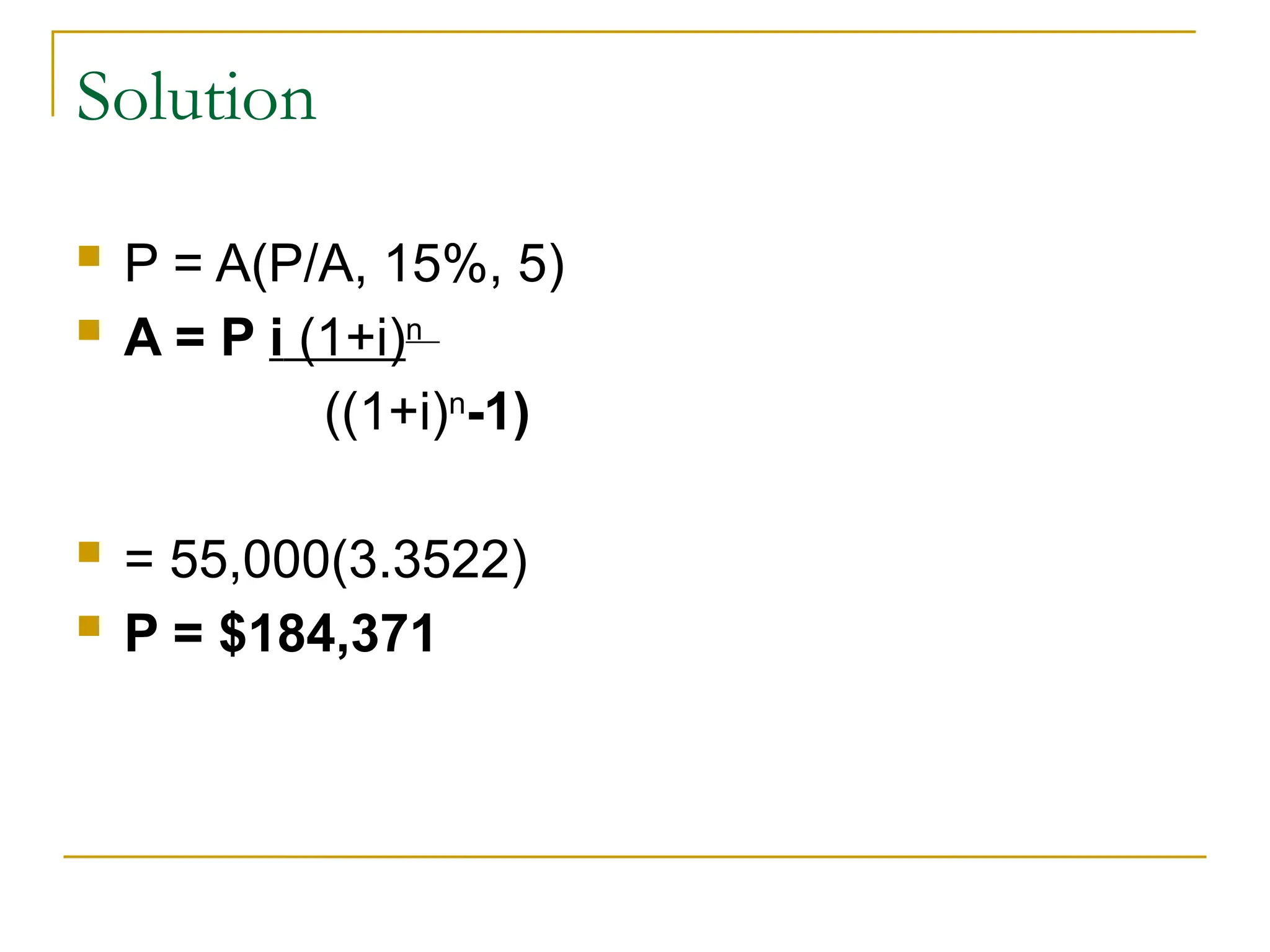

Solution

P =A(P/A, 15%, 5)

A = P i (1+i)n

((1+i)n

-1)

= 55,000(3.3522)

P = $184,371

59.

Problem

Given: Amoving company wants to buy a

new truck for $250,000 in 4 years and

interest rates are 10% per year.

Find: How much should they set aside each

year?

60.

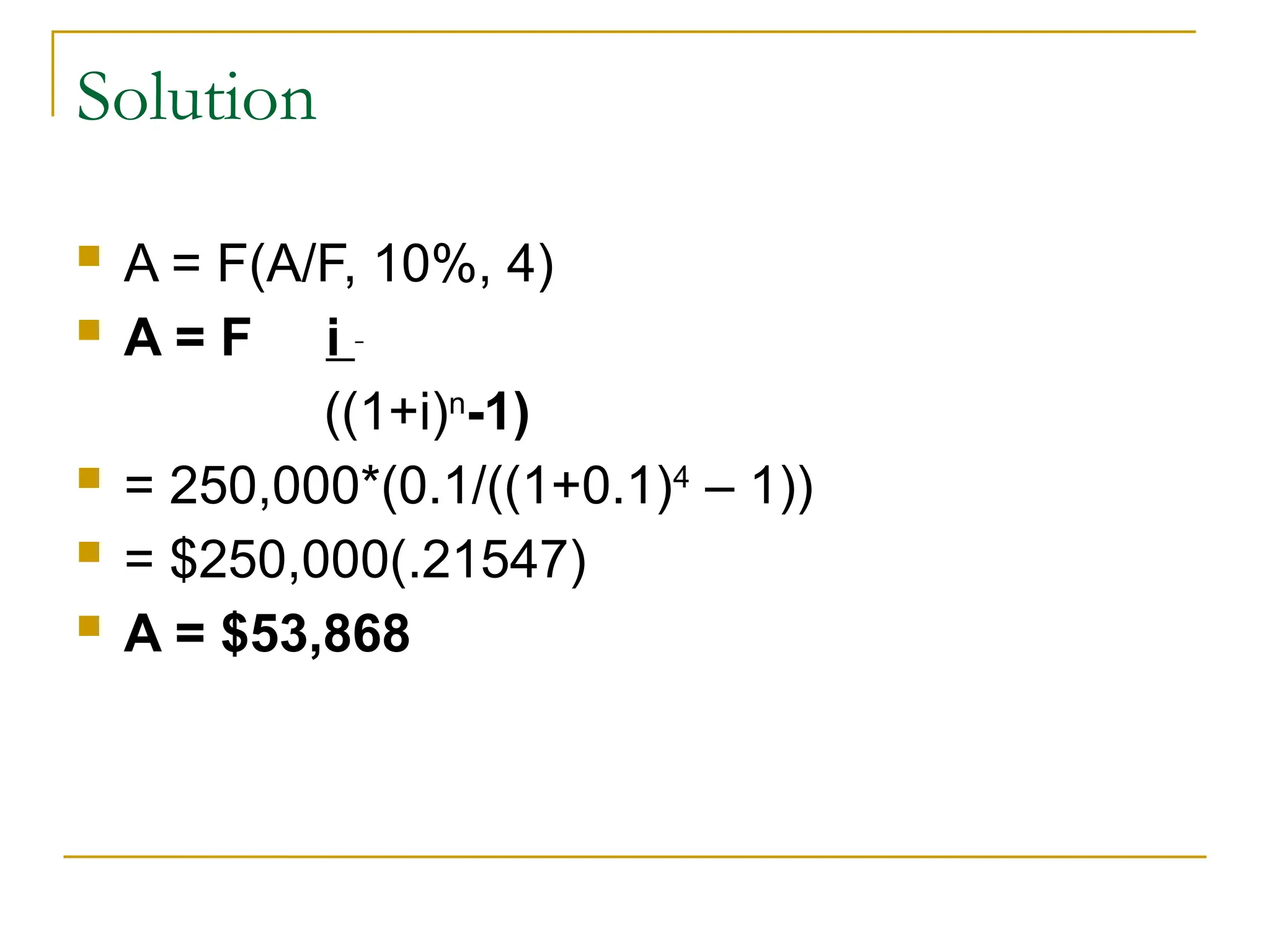

Solution

A =F(A/F, 10%, 4)

A = F i

((1+i)n

-1)

= 250,000*(0.1/((1+0.1)4

– 1))

= $250,000(.21547)

A = $53,868