3. I. Current ratio

Current ratio = current Assets / Current liabilities

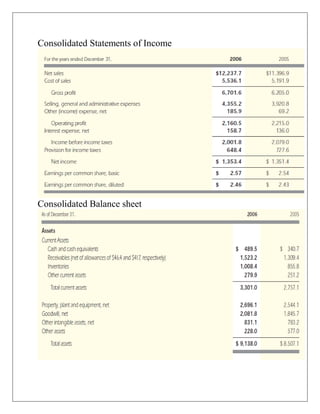

Current ratio2005 = 2757.1$ / 2743.0$ = 1.005

Current ratio 2006 = 3301.0$ / 3469.1$ = 0.95

Years 2005 2006

Current Ratios 1.005 0.95

interpretation:

In 2005 the company ability to pay its current Liabilities with current assets was

1.005 in 2006 the current ratio goes down from 1.005 to 0.95 which means that the

company has not ability to pay its Liabilities, Higher the ratio higher the ability of

the company to pay its bills. the ratio in 2006 tells that the Colgate company not

improving their liquidity and efficiency, because their current ratio is not improving

it goes down from previous year.

II. Acid-Test (Quick Ratio)

Quick ratio = (current assets - inventory) / current liabilities

Quick ratio 2005 = 2757.1$ -1008.4$ / 2743.0$ = 0.63

Quick ratio 2006 = 3301.0$ -1008.4$ / 3469.1$ = 0.66

Years 2005 2006

Quick ratios 0.63 0.66

interpretation:

According to the definition of Acid Test Ratio, the company should have the ability

to pay its liabilities through its most liquid assets. The Colgate company Quick ratio

in 2005 is 0.63. then in 2006 it goes up from 063 to 0.66. So we can figure out from

the ratios that Colgate still cannot pay its debts without its inventory.

4. III. Inventory Turnover

Inventory Turnover = Sales / inventory

Inventory Turnover 2005= 11396.9$/855.8$ = 13.31

Inventory Turnover 2006=12237.7$/1008.4$ = 12.13

Years 2005 2006

In. Turnover ratio 13.31 12.13

interpretation:

Inventory turnover ratios goes down from 2005to 2006, which means that its ability

to sell inventory has relatively come down. Higher inventory turnover ratios are

considered a positive sign of effective inventory management. Inventory turnover is

a measure of the company's ability to sell its products for cash.

IV. Average Collection Period

ACP = Receivables / Average sales per day

ACP = Receivables / Sales/365

ACP 2005= 1309.4$/ 11396.9/365$ = 42 days

ACP2006= 1523.2$ /12237.7$/365 = 45 days

Years 2005 2006

ACP ratios 42 days 45 days

Interpretation

An average collection period shows the average number of days necessary to convert

business receivables into cash.in 2005 the Colgate company ACP was 42 days.in

2006 the ratio increase from 42 to 45 days. the increase in ratio shows that the

company cash receiving department not work efficiently. Low average collection

period is good and favorable for the company.

5. V. Total Assets Turnover

TA Turnover = Sales / Total Assets

TA Turnover 2005 = 11396.9$/8507.1$ = 1.33

TA Turnover 2006 = 12237.7$/9138.0$ = 1.33

Years 2005 2006

TA turnover ratio 1.33 1.33

interpretation:

The asset turnover ratio is an efficiency ratio that measures a company ability to

generate sales from its assets by comparing net sales with average total assets. higher

ratio is always more favorable. Higher turnover ratios mean the company is using its

assets more efficiently. In 2005 & 2006 TA assets turnover ratio is same, its means

that the company generate more revenue per dollar investment the asset turnover

ratio is based on company performance. Some companies use assets more efficiently

than others.

VI. Fixed Assets Turnover

FA turnover = Sales / Net fixed assets

FA turnover 2005=11396.9$/5950$ = 1.91

FA turnover 2006=12237.7$/5837$ = 2.09

Year 2005 2006

FA turnover ratio 1.91 2.09

Interpretation:

Fixed asset turnover measures how well a company is using its fixed assets to

generate revenues. The Colgate company FA turnover ratio in 2005 is 1.91 in 2006

it goes up to 2.09. the increase ratio indicates that a company spent less money in

fixed assets for each dollar of sales revenue.

6. VII. Debt Ratio

Debt ratio = Total liabilities / Total assets

Debt ratio 2005 =7157.0$/8507.1$ = 0.84%

Debt ratio 2006 =7727.1$/9138.0$ = 0.84%

Years 2005 2006

Debt ratios 0.84% 0.84%

Interpretation:

The ratio shows the company’s ability to cover its debts through its total assets.

There is no difference in ratio in 2005 & 2006.

VIII. Times-Interest-Earned (TIE) Ratio

TIE = EBIT / Interest expense

TIE ratio 2005 =2079.0$/136.0$ = 15.28

TIE ratio 2006= 2001.8$/158.7$= 12.61

Years 2005 2006

TIE ratio 15.28 12.61

Interpretation:

In 2005 the TIE ratio is 15.28 in 2006 it goes down from 15.28 to 12.61. which is

not favorable for the company Times interest earned (TIE) is used to measure a

company's ability to meet its debt obligations. the larger ratios are considered more

favorable than smaller ratios.

7. IX. Gross Profit Margin

Profit Margin = Gross profit/ sales

Profit Margin 2005 = 6205.0$/11396.9= 54%

Profit Margin 2006= 6701.6$/12237.7= 54%

Years 2005 2006

Profit Margin ratio 54% 54%

Interpretation:

The ratio should be high according to the definition. Because higher the ratio, higher

will be the firm’s ability to produce goods and services at low cost with high sales.

Here in this table there is no difference between the ratios in two years, but it’s still

high, which means it is favorable.

X. Operating Profit Margin

Operating Profit Margin = EBIT/Sales

OPM 2005= 2079.0$/11396.9$=18%

OPM 2006=2001.8$/12237.7$= 16%

Years 2005 2006

OPM ratio 18% 16%

Interpretation:

operating profit margin has decreased in 2006 the profit ratio 1n 2005 is 18%. The

low ratio in 2006 reflects that the Colgate company is not more efficient in cost

management Operating margin ratio shows whether the fixed costs are too high for

the production or sales volume. High or increasing operating margin is preferred

because if the operating margin is increasing, the company is earning more per dollar

of sales.

8. XI. Net Profit Margin

Net Profit Margin = Net income /Sales

NPM ratio 2005=1351.4$/11396.9$= 11%

NPM ratio 2006=1353.4$/12237.7$= 11%

Years 2005 2006

NPM ratio 11% 11%

Interpretation:

According to the definition, higher the ratio, higher will be the firm’s ability to pay

its taxes. The Colgate NPM ratio in 2005 & 2006 is 11% there is no difference

between the ratios in two years. Company is more efficient at converting sales into

actual profit and its cost control is good.

XII. Return on total assets (ROA)

ROA = Net income /Total Assets

ROA 2005 =11396.9$/8507.1$ =33.9%

ROA 2006=12237.7$/9138.0$= 33.9%

Years 2005 2006

ROA ratio 33.9% 33.9%

Interpretation:

The return on assets ratio measures how effectively a company can earn a return on

its investment in assets. Colgate ROA ratio 1n 2005 & 2006 are equal. There is no

increase decrease in Return on Assets indicates that the company is generating

more profits from all of its resources