More Related Content More from Realty411 Magazine for Real Estate Investors (20) 12. 12

32

Maria Sol Bruemmer:

Lending Consultant and

Partner of Entrepreneur

Funding Experts

Maria Bruemmer

36

The Capitalization Approach

to Income Property Valuation

Dan Harkey

49

Have You Considered Adding

Brownfield Development to

Your Real Estate Portfolio?

Patricia Gage

55

An LLC for Real Estate

Investing

Stephanie Mojica

TABLE OF CONTENTS

Serving Investors Since 2007

Realty411

Photo by Max Vakhtbovych from Pexels

17

Live Your Life with Intention -

My Interview with

Jason Oppenheim

Linda Pliagas

24

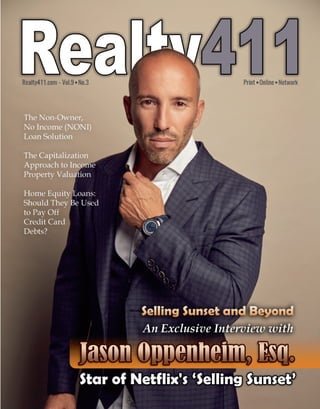

Selling Sunset and Beyond

An Exclusive Interview

with Jason Oppenheim, Esq.

Star of Netflix’s Selling Sunset

Stephanie Mojica

13. 13

60

Retirement Savings Lost After

Investment in Fraudulent Company

Resembling SDIRA Custodian

By Stephanie Mojica

67

Strength in Numbers: Victor Cuevas

Gives Us Advice About Crowdfunding

as a Tool for Investments

Victoria Kennedy

73

Investors See Average Return

on Investment Down Amid Tight

Market plus Labor

and Supply Shortages

Stephanie Mojica

77

Picking The Right NNN Lease

& The Downfall of CVS

Clinton Lu

82

The Non-Owner, No Income (NONI)

Loan Solution

Rick Tobin

91

Home Equity Loans: Should

They Be Used to Pay Off

Credit Card Debts?

Catherine Burke

100

Young California Homebuyers

Are the 3rd Most Likely

to Need a Co-signer

Lauren Thomas

107

Sponsored Section

Realty411's REI Resources

FEATURED

17. 17

LINDA'S LETTER

Hello everyone!

W

elcome to another

special edition of

Realty411. We have

another issue jam

packed with resources to help you

begin, maintain, or expand your real

estate investment career.

On the cover of this celebrated

issue, we feature Jason Oppenheim,

Esq., founder of The Oppenheim

Group. The Oppenheim family has

operated a respected brokerage for

generations in Beverly Hills and West

Hollywood.

Beginning with family patriarch,

Jacob Stern, who owned the land

where the world’s first fulllength

feature film, The Squaw Man, was

produced, studio chiefs and celebrities

have sought out the family for realty

By Linda Pliagas,

Publisher/Editor

Photo by John De Cindis

guidance with their real estate

transactions.

Now, five generations later, twin

greatgreat grandsons Jason and Brett

Oppenheim star in Netflix's hit

original series, Selling Sunset. The

reality show is based on the Oppenheim

Group agency on Sunset Boulevard.

Selling Sunset is best described as a

hautecouture soap opera focused on

luxury, fashion and Hollywood fun.

Live Your Life with Intention -

My Interview with Jason Oppenheim

The team from Selling Sunset, courtesy of The Oppenheim Group

18. 18

LINDA'S LETTER

The exquisite homes featured for

sale are exclusive estates in Beverly

Hills and West Hollywood, ranging

from the low millions to $50M and up.

It's an exclusive world of glamour,

creativity, prestige and influence. At

The Oppenheim Group, agency

commissions can be as high as

$250,000 per transaction.

Recently, it was reported by news

source Business Insider that the

Oppenheim twins have expanded the

family legacy by building a brokerage

transacting hundreds of millions of

dollars' worth of properties each year.

In fact, since opening in 2014, The

Oppenheim Group has had an

estimated total of nearly $2 billion in

estate sales.

The brokerage recently expanded

its operation to Newport Beach,

California, plus might be planning a

future launch in Las Vegas, Nevada,

and Cabo San Lucas, Mexico. Selling

Sunset has already been renewed for

two more seasons, plus the hit show

has expanded to spinoffs: Selling

Tampa and Selling the OC.

The success of the Oppenheim

twins is a wonderful tribute to their

greatgreat grandfather, Jacob Stern.

Founded in Hollywood in 1889 as The

Stern Realty Co., the Oppenheim

family have now operated five

generations of property development,

management and brokerage services in

Los Angeles.

The family's major professional

milestones include: a central role in

fostering Hollywood’s early

entertainment industry, becoming one

of the nation’s largest developers of

HUD housing in the 1980s, and a

fivegeneration legacy in the

development and brokering of luxury

residential properties.

I had the pleasure of interviewing

Jason and interacting with his

amazing team to prepare for his cover

feature in our publication. One of the

best business lessons I learned from

watching Selling Sunset and

interviewing Jason is the positive way

that he handles career stress.

Anyone who watches the show

knows that major drama can exist at

times in the office. There are tears,

fits, breakups and escrows that fall

out. Highlevel properties often equal

busy, jetsetting clients and the luxury

industry is highly competitive. Yet

despite all this high pressure, Jason

remains calm and composed.

He's a firm believer in spending

time with loved ones and taking all

the rest in stride. Jason actively

creates his own reality by surrounding

himself with a select staff and

customer base, people whom he

chooses to spend time with.

He is intentional about maintaining

his quality of life and his mental and

physical health.

What an important lesson to be

aware of. Too often people are

working themselves into a frenzy to

grow their wealth, but they neglect

themselves and their loved ones in the

process.

Jason is a reminder that in the race

to build a billiondollar business, we

need to stop, take a deep breath, be

grateful for all the blessings, and

share the wealth with others.

With this lesson in mind, I encourage

you to slow down on your way to the

top. Take in the beauty and magic of

each moment. Be intentional with your

actions and words and know the power

and impact they have on others.

My team and I hope you enjoy our

new Realty411 issue. Please share

your thoughts and feedback with us

at: info@realty411.com. As always, if

we can assist you, please don't

hesitate to contact us.

Linda Pliagas

info@Realty411.com

Celebrate our new issue featuring

Jason Oppenheim, founder of

The Oppenheim Group in Orange

County. Join us for this awesome

event and receive our new issue:

https://realty411.com/calendar2

24. 24

Selling Sunset and Beyond

An Exclusive Interview with

Jason Oppenheim

Star of Netflix’s 'Selling Sunset'

Interview by Linda Pliagas

Article by Stephanie Mojica

Photographs courtesy of The Oppenheim Group

25. 25

I

n an era when some people are

focusing more on Bitcoin and stocks,

Jason Oppenheim of Selling Sunset

fame is doubling down on real estate.

That’s no surprise, as Oppenheim

was born into one of the most prominent real

estate families in California.

The real estate bug runs deep in

Oppenheim’s family — from his twin brother

Brett, their father Bennett, and their great great

grandfather Jacob Stern.

“I think I got (my interest in real estate)

from my parents when I was pretty young,”

Jason Oppenheim said in a recent interview

with Realty411. “I didn't really follow that

passion until after a career in law. But I think

I'd always been genuinely interested because

my dad was a real estate agent.”

As a child growing up in the San Francisco

Bay Area, some of Oppenheim’s earliest

memories are of his dad conducting open

houses and selling properties in Fremont.

However, Oppenheim didn’t immediately

follow his father — first he earned a law

degree from the University of California,

Berkeley and then spent four years as an

attorney for the major international law firm

O'Melveny & Myers. When he finally entered

the family business, which has existed for five

generations, Oppenheim quickly made a name

for himself. Oppenheim’s clients include

celebrities such as Jessica Alba, Orlando

Bloom, Kris Humphries, Taye Diggs, and

Dakota Johnson.

Even before Oppenheim and his twin

brother got their own Netflix reality show, he

was consistently named Top Agent in Los

Angeles by The Hollywood Reporter and a

member of the Showbiz Real Estate Elite by

Variety. The Wall Street Journal and REAL

Trends honored him three times in 2020 as the

#1 Agent in Los Angeles, the #1 Agent in

Hollywood Hills/Sunset Strip, and the #8

Agent in the United States. The 20202021

International Property Awards named

Oppenheim the Best Real Estate Agent

Worldwide.

26. 26

“The things that I

think helped me the

most was my law

degree and my

practice as an

attorney; I think that

really allowed me to

instill confidence in

my clients,”

Oppenheim said.

“And I look for that

in (hiring) agents.

I've got a couple of

attorney agents and I

can't imagine a better

pedigree for real

estate than a law

degree."

Though the

COVID19 pandemic

affected all segments

of the real estate

industry, Oppenheim

believes the worst is

over for investors, homebuyers, and agents alike.

“The bottom line is with real estate, there's actual need,” he

said. “It's not like stocks or Bitcoin or where you don't need

those things. People need to live in a house, they need to

expand, they have a family, or they need to move.”

He adds: “I think it's one of those kinds of fundamental assets

and investments where despite the ups and downs, it's always

going to have a general trend upwards. It's really hard to keep

real estate down, and you can do it in the short term, but it's like

a bubble in water. It just finds its way back out.”

Less populated areas have become more popular because

people want more space due to more time at home. They have

legitimate concerns about the problems associated with crowded

cities, he noted. Newport Beach and Monterey are increasingly

popular in California and states such as Arizona, Florida, Texas,

Utah and Wyoming are also seeing a flux of investors and

residents alike, according to Oppenheim.

“I think it's too soon for us to see people coming back to

those major dense areas (Los Angeles and New York City),” he

said. “In L.A. specifically, the crime is out of control. And I

think homelessness is becoming an even more serious problem.”

Tax issues are also pulling people out of major urban areas,

Oppenheim added.

'I think it's one of those kinds of

fundamental assets and

investments where despite the

ups and downs, it's always

going to have a general trend

upwards. It's really hard to keep

real estate down and you can do

it in the short term, but it's like

a bubble in water. It just finds

its way back out.'

Photographs courtesy of the Oppenheim Group

“For example, a lot of people who've made a lot of money in

stocks and cryptocurrency are deciding to move to a state that

doesn't have a high state tax before they sell,” he said. And you

know, that makes sense to me.”

Another challenge was the varying COVID measures in

American cities and states, per Oppenheim.

“I think that the past mandates and government intervention

was pushing people out of certain states,” he said.

27. 27

“Now, Florida is a bastion for people

who don’t want to have government

intervention and mandates, but I think as

we accept whatever role COVID is

going to play in our in our lives, you

won't have the disparity between

different states as much as you do now.”

However, all these issues don’t

necessarily mean people won’t return to

Los Angeles and New York, according

to Oppenheim.

“Moving forward into 2022, 2023,

and 2024, I think that we will see people

returning to the big cities,” he said. “And

I think that those areas that have seen

that huge boom, we'll probably see that

they will come down a little bit.”

Overall, densely populated

metropolitan areas are still the best

investment, in Oppenheim’s opinion.

“I do think that these large cities will

eventually get a handle on the

homelessness problem and on the crime

problem,” he said. “And I think that

there'll be a sense of normalcy soon.”

For more information about

The Oppenheim Group, visit

https://ogroup.com/. The agency has

offices in West Hollywood and Newport

Beach, Calif.

'The bottom line is

with real estate,

there's actual need.

It's not like stocks or

Bitcoin or where you

don't need those

things. People need

to live in a house,

they need to expand,

they have a family,

or they need

to move.'

33. 33

F

lipping homes became so

popular it inspired

countless reality shows,

real estate coaches, and

speakers. However,

according to some investors flipping

homes is now less profitable than ever.

The number of people buying fixer

upper houses at low rates, fixing them

up, and then selling them for profit has

dramatically increased. But that isn’t

necessarily the problem — the ongoing

housing shortage is the main issue,

according to a recent housing report on

CNN.

Even homes in dilapidated condition

are selling at skyhigh prices. Another

challenge for wouldbe real estate

flippers is the increased cost of supplies

and labor shortages.

The proof is in the data. The average

return on investment was 32.3% or

$68,847, according to Attom (an official

data provider for the real estate industry).

Things haven’t been this bad for house

flippers since 2011.

However, investors interviewed

during the broadcast are making it work

— and not all are angry about the 32.3%

ROI. Danielle Green of Baltimore has

flipped houses since 2018. Before

COVID19, Green went to auctions and

bought properties for $5,000 to $10,000.

Now she pays $20,000 to $40,000 — a

400% increase.

One of Green’s challenges is that

auctions are held online rather than in

person, dramatically increasing the

number of competing bidders. Also,

fewer auctions were held due to a lack of

available properties.

Another issue is that people from

larger metropolitan areas such as

Washington D.C. and Philadelphia can

no longer afford real estate in their own

cities, so they look to Baltimore for

affordable real estate. However, Green

said outoftowners are more prone to

make notsogreat buying decisions.

'Investors come in

and think it is easy

to buy because the

houses seem cheap

— they'll think

buying a shell (of a

house) for $40,000

is a deal,' she told

CNN. 'But I know

that's not the best

neighborhood. You

have to know the

market and

understand what

you're buying.'

Green changed her strategy and started

buying multifamily homes with three or

four units as opposed to singlefamily

properties. Instead of selling immediately,

she kept some of her properties to use for

ongoing rental income. Now, she does

one to two “big deals” a year as opposed

to three or four. However, Green said it’s

still profitable for her.

Leah Wensink of Harrogate, Tenn.

(about 60 miles from Knoxville) has been

a real estate flipper since 2014 and paid

$170,000 cash for a house to flip this year

— her highest investment ever, according

to the broadcast. Wensink’s project was

delayed by a few months by supply and

labor shortages and is also unsure if she’ll

see a significant profit on the property.

Her philosophy, which sounds like a

solid one for other investors, is to set a

firm boundary about how much money

she will spend on a deal and do a lot of

research on her market.

Investors See Average Return

on Investment Down

Amid Tight Market plus

Labor and Supply Shortages

By Stephanie Mojica

Image by F. Muhammad from Pixabay

37. 37

Stated one more time: Capitalization

Rate represents the annual Net

Operating Income (NOI) divided by

the cap rate to derive the property

asset value (NOI/Cap Rate= Value).

Why do we use Capitalization

Rates?

The capitalization approach is a

“comparative method” of valuing

property with similar properties, similar

income streams, in similar geographic

locations, and similar risks that will yield

a comparable rateofreturn. Once the

value is established, the comparative

method can calculate the loantovalue to

determine if property value falls within

the lender’s loan underwriting

guidelines.

Cap Rates are only one

metric. Since the capitalization

approach is calculated as if the

property is debtfree the value

will be the same whether the

property has leveraged debt or is

debtfree. It represents a market

snapshot at the investment time

and does not consider loan debt

service or financing costs.

If an investor finances his acquisition,

as most people do, further analysis such

as cashoncash return will be helpful.

Sophisticated loan underwriters and

investors may also calculate an Internal

Rate of Return. These calculations assist

in establishing that the property is

incomeproducing and a worthwhile

investment.

A licensed commercial appraiser may

perform a rent survey to determine

market rents for a property type in a

geographic area. Market rents may or

may not be the same as actual rents

(contract rents). There are many

instances where the existing rents are

above or belowmarket rents. A tenant

with a longterm lease may have locked

in lower rents sometime in the past.

I once underwrote a loan transaction

on an industrial building near San

Francisco that was about 100 years old.

The property has a longterm lease of 18

cents per square foot, while the current

market was $1.75 a square foot. Since

current market rents were much higher,

the valuation metric used was based upon

the lockedin lower rental rate.

A property owner may own the

property in one title method such as The

Archie Bunker Corporation and occupy

all or a portion of the building in

different title method such as Archie

Bunker Limited Liability Company. He

may charge above or belowmarket rents

to himself for tax purposes. Actual rents

may also be higher than the market. In

this case, the appraiser would use market

rents rather than actual rents to determine

the Cap Rate.

There are other instances where a

conventional market Cap Rate analysis is

inappropriate. The alternative method is a

discounted cash flow analysis such as

original groundup construction. The

building cost and the cash flow from a

leaseup need to be projected over a

reasonable time to the point of stabilized

occupancy. This is done by a competent

appraiser who can construct a model

estimating a future projected cash flow

and using net present value discount

formulas to estimate the capitalization

rate. The result may differ from the

market comparison method.

Suppose you have income properties

with similar characteristics in a

geographically close location sold in

arm’s length cash transactions, and the

income stream data is available. In that

case, there are webbased databases that

track comparison capitalization rates

(Cap Rates.)

Market rents are the amount of rent

that can be expected for a property,

compared to similar properties in the

same geographic areas. Contract rent or

actual current rent is what the same units

are being rented for today. Many lenders

will request a rental survey from an

appraiser as an addon task to the

requested appraisal job.

There is an essential difference

between market rents and current

actual (contract) rents in the Cap Rate

valuation process. Compare two different

buildings, both identical, but the first

property is wellkept and rented at a

market rate, and a second building that

has deferred maintenance. The property

with deferred maintenance is rented for

undermarket rates by under 30%. In

both cases, a lender and the appraiser will

use market rents to determine the (NOI).

The assumption about the second building

is that a new owner will upgrade the

building and adjust the rents upward to a

market rate. The value of the second

building would be adjusted downward or

discounted to offset the cost to cure (cost

to upgrade the building).

Photo by MOHAMED ABDELSADIG from Pexels

38. 38

The only time that a lender, or

appraiser, would use the lower rents is

when those rates were locked into a

longterm lease or a rentcontrolled

property. I underwrote the following

example: A prospective loan for an

industrial building in Richmond,

California. The property was leased fee,

leased out to a third party for 99 years,

with 50 years remaining. The lockedin

rent was only 18 cents per square foot

triple net. The property owner and

broker argued belligerently that current

value should be based upon today’s

rents.

An inconvenient fact in this example

is that the property owner is locked into

an 18 cent per square foot monthly

income stream for the next 50 years.

Capitalized rents will be based upon 18

cents per square foot lease rate. The

capitalized value with an 18 cents per

square foot will have a dramatically

lower NOI compared to a similar

building next door that rents at $1.75 per

square foot lease rate monthly.

A historic rents comparison databases

are available to determine market rents

to calculate a correct capitalized

valuation. Historic market Cap Rates

may vary, even in the exact geographic

location, depending upon the building

improvements, effective age, class of

construction, offstreet parking, furnished

or unfurnished, condition, compliance

with zoning, easements or lack of needed

easements, and amenities. Examples

include ClassA vs. ClassC office,

industrial, apartments, older dated,

economically obsolete and under parked

compared to a new modern building with

adequate parking and currently popular

amenities.

Advantages and disadvantages

of the Capitalization approach

to value:

Advantages:

1. This method converts an income

stream into an estimate of the value of

the incomeproducing real estate.

2. The method is a common standard in

the appraisal, lending, and

development business.

3. While the income capitalization

approach is common in evaluating

commercial incomegenerating

properties, it can theoretically be

applied to any income stream,

including businesses.

4. Commercial appraisers are a reliable

source for determining market Cap

Rates.

5. Commercial Realtors® provide an

excellent source of cap rates with

websites such as Costar and Crexi

6. There are online databases such as the

CBRE/USCapRateSurveySpecial

Report2020 to obtain reliable data.

https://www.cbre.us/researchand

reports/USCapRateSurveySpecial

Report2020

Disadvantages:

1. The method is used for “comparison

only with similar properties in a close

geographic area.” The method does

not consider liens on the property and

debt service. A Cap Rate calculation is

done as though the property is debt

free. Cap Rates cannot be used to

calculate overall net cash flow or cash

oncash yield when a loan attached to

the property (Income, less operating

expenses, less debt service).

2. The results of a Cap Rate calculation are

specific only to a similar area with

similar properties in certain segments

of the market. You could not use

Newport Beach, California cap rates

to compare with a similar building

with similar usage in Riverside,

California. Also, the demand for

properties and Cap Rates for different

segments of the real estate market

change. Current examples are residential

income properties and Industrial are

and will continue to be in demand. I

read one estimate that industrial in the

U.S. will require an extra billion

square feet of warehouse by 2025.

Office and lodging/resort related

properties, not so well. Patterns change!

3. The method contemplates stable

economic market conditions. If a

market experiences a significant

downturn, collapses, or is subject to

extreme political uncertainty, the

calculations using market cap rates

may be rendered irrelevant.

Photo by Tima Miroshnichenko from Pexels

Historic market Cap rates may

vary, even in the exact geographic

location, depending upon the

building improvements, effective

age, class of construction, offstreet

parking, furnished or unfurnished,

condition, compliance with zoning,

easements or lack of needed

easements, and amenities.

39. 39

4. Relying on a Cap Rate with an unstable

market condition is difficult. Using

market rents may become suspect

because higher rates of foreclosures,

tenants default much more frequently,

vacancy rates go up, and replacement

tenants will ask for higher rent

concessions, thereby bringing the

market rents down. Additionally,

owner operating expenses may

become constrained.

5. Calculating forecasting future income

streams involves a high degree of

professional judgment, and therefore

subject to variation.

6. Professional judgment is subject to

subjective vs. objective interpretations

about expectations of future benefits.

7. The method may result in miscalculations

when estimating the cost of capital

outlay for upgrades to bring the

property up to current standards. All

subsets of the job have a cost, time

and frustration allocation, including

municipal approvals, reconstructing

the building, modern materials,

safety, zoning, environmental, and

social equity requirements.

8. Property amenities, parking, easements,

recorded encumbrances, and

compliance with building and zoning

regulations require a complex analysis.

9. The leaseup period is only an

estimate and may not be correct.

10. Alleged appraiser and lender biases

for racially segregated neighborhoods

have been known to exist.

Tenancies: A landlord and tenant may

enter into four types of rental or lease

agreements. The type depends upon the

agreedupon terms and conditions of the

tenancy. All rental amounts and terms of

a lease will be reflected in the

capitalization evaluation.

Types include:

1) Fixedterm tenancy is a tenancy with

a rental agreement that ends on a specific

date. Fixed terms have a start date and an

ending date. According to the written

lease document, time terms may be short

or long such as ten years with multiple

extensions.

A landlord can’t raise rents or change

lease terms because the terms are

codified in a written agreement. A key

advantage for a landlord is to receive

today’s market rents.A key for a tenant is

to lock in a longterm lease where the

rents are or become below market over

time.

A tenant’s company’s profits are

enhanced if they pay substantial under

market rents. On the other hand, if a

tenant’s company is making a good profit

with rents substantially below market and

a lease is coming due soon, the increased

or negotiated upward lease rate may wipe

out some or all the profits.

2) Periodic tenancy is a tenancy that has

a set ending date. The term automatically

renews into successive periods until the

tenant gives the landlord notification that

he wants to end the tenancy. Monthto

month tenancies are the most common.

The strength of the tenancies from

national credit with longterm leases and

corporate guarantees down to mom &

pops monthtomonth tenancies will result

in a substantially different Capitalization

Rate. National credit tenants with

corporate guarantees have a considerably

lower Cap Rate. Mom and pop tenancies

will reflect a higher Cap Rate because

they inherently have more risk.

The lower the market Cap Rate, the

lower the perceived risks of property

ownership. The higher the market Cap

Rate, the higher the perceived risks. An

exception would be where the national

credit tenant locks in a lease rate that does

not increase as the market dictates or

anticipates increases. Eventually, over

time, this tenant will reflect belowmarket

rents.

A momandpop tenant could be

converted to a market rent more quickly

because the term is usually shorter.

Market rents are obtained by surveying

local brokers and appraisal databases of

local market rents.

3) Tenancyatsufferance (or holdover

tenancy). This form of tenancy is created

when a tenant wrongfully holds over past

the end of the duration of period of the

tenancy.

Image by Gerd Altmann from Pixabay

The lower the market Cap Rate, the lower the perceived risks of property ownership.

40. 40

I bring up this type of tenancy

because of COVID. The government

allowed tenants to skip out and default

on paying rents without consequence.

The tenants either defaulted on the rent

or overstayed the term. In either event,

the tenant becomes delinquent, and the

owner attempts to evict them. The tenant

or affiliates may become illegal

trespassers.

There are many examples of a

landlord attempting to get rid of an

illegal tenant only to be jerked around

through the court system, with multiple

appeals requested by the tenant. They are

usually granted.Then comes multiple

bankruptcies, not only of each tenant,

one by one, but unknown people who

supposedly moved in without notice to

the landlord. Then comes the transients

and fictious folks who show up declaring

that they are a tenant and request that the

process start all over because of their

fraudulentlyclaimed tenancy. The

courts, particularly in states like

California, just turn their backs on this

behavior.

The focus for the property owner

becomes using legal avenues to evict the

tenants and regain occupancy of the

property. This process has great cost and

frustration.

4) TenancyatWill. This form of

tenancy reflects an informal agreement

between the tenant and landlord. The

landlord gives permission, but the period

of occupancy is unspecified. The term

will continue until one of the parties give

notice.

Rehabilitated Property or New

Construction:

Establishing market rents becomes

essential in underwriting a rehabbed or

new building. When there is an extended

time delay for a leaseup period, such as

with the new construction of an income

producing property, future cash flows

need to be estimated to the point of

income stabilization. Then the future

stabilized income will be discounted, using

an estimate of a market capitalization rate

and a discount rate formula.

Work with a competent commercial

appraiser to assist and calculate the

correct market Cap Rate. Do not try to do

this yourself without the help of an

appraiser who knows the type of real

estate and local market.

Below is an example: The market

Cap Rate for a commercial property

with triple net leases (NNN) has been

determined to be 6.5%. Triple Net or

(NNN) refers to a leased or rented property

where the tenant pays all expenses related

to the operation such as taxes, insurance,

maintenance, and occasional capital

improvements. The 10,000 square foot

multitenant property under consideration

generates monthly rents of $1.50 per

foot. On a (NNN) example for a Cap Rate

analysis, one would apply a 10% vacancy

collection and loss factor and 5% for non

chargeable expenses that tenants usually

do not pay including reserves. The NOI

would be $153,900.

The NOI and Market Cap Rate

are known so you can calculate

the value:

10,000 SF rentable X $1.50 = $15,000

Per mo. X 12 Mos. = $180,000 =

potential gross income.

$180,000–$18,000 for 10% vacancy =

$162,000–$8,100 for 5% nonchargeable

expenses to the tenants = NOI = $153,900

$153,900 NOI /.065 Cap Rate = value =

$2,367,692

From an investment standpoint, market

Cap Rates can show a prevailing rate of

return at a time before debt service. The

Cap Rate procedure will assist a lender

and investor to measure both returns on

invested capital and profitability based on

cash flow. An informed lender or investor

should understand that there may be

dramatic variations in a property’s value

when unsupported or unrealistic Cap

Rates are applied.

Image by Paul Brennan from Pixabay

Work with a competent commercial

appraiser to assist and calculate the

correct market Cap Rate. Do not try to

do this yourself without the help of an

appraiser who knows the type of real

estate and local market.

41. 41

Cap Rates as well as demand for

incomeproducing properties will move

up or down depending on market

conditions. The term Cap Rate

compression reflects a movement of

the rate down because investors

perceive real estate as a lowerrisk,

higher reward asset class relative to

other investment options. Cap Rate

decompression may result from demand

for real estate purchases where Cap

Rates increase, reflecting lower

valuations. This may be a byproduct of

higher interest rates or government

intervention such as rent control.

CashonCash Return:

Cashoncash return is a quick

analysis to determine the yield of an

initial investment. The cashoncash

return is developed by dividing the total

cash invested (the down payment plus

initial cost) or the net equity into the

annual pretax net cash flow.

Assume the borrower purchased the

property, which costs $1,200,000 and

provides an NOI of $100,000, with a

$400,000 down payment representing

the equity investment in the project.

The cashoncash return for this

property would be:

$100,000/$400,000 = 25% = cashon

cash yield.

If the borrower were to purchase the

property for all cash, as contemplated in

a Cap Rate calculation, then the cashon

cash return would be:

$100,000/$1,200,000 = 8% (this example

the 8% is both the cashoncash yield and

Cap Rate).

It is clear from this formula that

leveraging or financing real estate

transactions will yield a higher cashon

cash return, provided the transaction is

financed at a favorable interest rate.

Internal Rate of Return (IRR):

Internal rate of return (IRR) refers to

the yield that is earned or expected to be

earned for an investment over the period

of ownership. IRR for an investment is

the yield rate that equates the present

value of the outlay of capital and future

dollar benefits to the amount of money

invested. IRR applies to all dollar

benefits, including the outlay of the initial

down payment plus cost, the positive

monthly and yearly net cash flow, and

positive net proceeds from a sale at the

termination of the investment. IRR is

used to measure the return on any capital

investment before or after income taxes.

Ideally, the IRR should exceed the cost of

capital.

Is there an ideal Cap Rate?

Each investor should determine their

risk tolerance to reflect their portfolio’s

ideal riskreward level. A lower Cap Rate

means a higher property value. A lower

Cap Rate would imply that the underlying

property is more valuable, but it may take

longer to recapture the investment. If

investing for the longterm, one might

select properties with lower Cap Rates. If

investing for cash flow, look for a

property with a higher Cap Rate.

Declining Cap Rates may mean that the

market for your property type is heating

up, and demand is intensifying. For Cap

Rates to remain constant on any

investment, the rate of asset appreciation

and the increase of NOI it produces will

occur in tandem and at the same rate.

42. 42

Below are examples of changes in NOI

and Cap Rates that cause asset values

to rise or to go down:

As NOI increases and Cap Rates remain

the same, asset values will increase.

($300,000 reflects net operating income

and .06 reflects a 6% cap rate)

$300,000 /.06 = $5,000,000

$350,000 /.06 = $5,833,000

$400,000 /.06 = $6,666,666

$450,000 /.06 = $7,500,000

As NOI remains the same and cap

rates rise, asset value will go down:

($500,000 reflects net operating

income and .03 reflects a 3% cap rate)

$500,000 /.03 = $16,666,666

$500,000 /.04 = $12,500,000

$500,000 /.05 = $10,000,000

$500,000 /.06 = $8,333,333

Correlation Between Cap Rates

and US Treasuries:

The US Ten Year Treasury Note

(UST) is deemed to be the riskfree

investment against which returns on

other types of investments can be

measured. USTs yields have been on a

broad decline for many years but may

soon rise. As interest rates increase those

investors who bought USTs at a lower

rate will find that their bonds will go

down in value. Bonds purchased at the

new higher rates will be in high demand.

As interest rates rise, Cap Rates will

go up, and consequently, there will be a

reduction in asset values over time. With

so many uncertainties in the market and

growth projections constantly being

revised, the spread between UST and

Cap Rates has not remained constant.

When the government intrudes in the

market, the results are artificial. This has

caused capitalization rates to go down,

reflecting higher values. Nearzero

interest rates have also caused a dramatic

inflationary spike in all goods and

services.

Summary:

Property appreciation from excess

demand has been one of the most

significant reasons for investing in real

estate Appreciation is not part of the Cap

Rate calculation. For investors, lower

interest rates, tax benefits of owning

commercial real estate may, in and of

themselves, be the driving force to make

such an investment. If the property is to

be leveraged, there may be writeoffs for

loan fees, interest expenses, operating

expenses, depreciation, and capital

expenses.

Interest rates have been forced down to

extremely low rates, below inflation, by

government mandate! Refinancing at

lower rates has resulted in lower debt

service payments. Cash flows of income

producing properties have gone up,

reflecting a higher net operating income.

The government intentionally

creates market distortions that benefit

the insiders at the top of the economic

spectrum. The results are artificial.

This has caused capitalization rates to go

down, reflecting higher values. Nearzero

interest rates have also caused a dramatic

inflationary spike in all goods and

services. All asset classes have now been

“spiked with 200proof illusions” that

make everything seem fantastic on the

surface. But hangovers the day after

the party ends are no fun.

Photo by Mikhail Nilov from Pexels

When the government

intrudes in the market,

the results are artificial.

This has caused

capitalization rates to go

down, reflecting higher

values.

43. 43

Interest rates are increasing because

the government realizes that inflation

will only accelerate if they do not stop or

slow it. Increased interest rates will

result in newly originated loans having

higher payment structures. Higher loan

payments indirectly and over time cause

Cap Rates to rise and values to go down.

Values may not go down immediately,

but the demand to purchase income

producing properties will subside

because ownership makes less economic

sense. To add flames to this fire

government, including federal and state,

is passing legislation that will destroy

investor motivation to own.

Over time the four

pronged whammy will

become apparent. 1)

Rising interest rates, 2)

increase in interest rates

reflecting larger loan

payments, 3) general loss

of investor confidence in

the overall economy, 3)

loss of investor interest in

purchasing an income

property, 4) overburdening

& abusive government

intervention into property

ownership will come

home to haunt the entire

real estate market across

the United States. 5) All of

the above will cause Cap

Rates to go up, and

property values go down.

Remember that increased debt service

based upon higher interest rates is not

considered in the capitalization approach.

But, over time, as interest rates go up,

borrowers will feel the sting of higher

debt service payments. Some property

transactions may become less appealing

financially. As purchasers and borrowers

elect not to purchase, that may compound

and create more unsold inventory. Some

sellers may get desperate and reduce the

price to sell quickly. The lowered price

would result in a higher Cap Rate. Higher

interest rates will lower all real estate

prices on a macro level.

How dramatic will lower real estate

prices be over time? Between 2007 and

2010 we witnessed the downward value

contagion spread resulting in substantially

lower values and increased Capitalization

Rates.

The fourpronged

whammy is not a new

phenomenon. It has just

been forgotten while

enjoying the Federal

Reserve’s 'freeforall 200

proof infused financial

punchbowl.'

A onetotwo hundred basis points increase in lending

rates (1% to 2%) would shatter the punch bowl into

fragments. It is my opinion that an imediate 2% interest

increase would collapse the economy overnight. Main

Street and small capitalist entrepreneurs would bear the

brunt of the widely spread financial damage.

MEET DAN HARKEY

Dan is President and CEO

at California Commercial

Advisers, Inc. He consults

on subjects of Business

Growth & Private Money.

Dan often creates articles interrelated to

these subjects. He has been active in the

real estate and financial services industry

since 1972 and possesses a lifetime

teaching credential for secondary and

adult education. He has taught over 350

educational seminars on subjects related

to real estate lending, private money

lending & loan underwriting for

commercial/industrial properties.

Contact Dan today

Mobile: 949.533.8315

Email: dan@danharkey.com

Image by Gerd Altmann from Pixabay

49. 49

I

t’s understood that having a real estate component

within your investment strategy is a triedandtrue

way to diversify your risk and increase your

investment returns. And while most people and

companies find real estate opportunities with more

common approaches, there is a less conventional way

to turn a profit in real estate: brownfield development.

According to the Environmental Protection Agency, “a

brownfield is a property, the expansion, redevelopment, or reuse

of which may be complicated by the presence or potential

presence of a hazardous substance, pollutant, or contaminant.” It

is estimated that there are more than 450,000 brownfields in the

U.S. Some l brownfields are obvious, like a former oil refinery.

Others may be a surprise, for example, an urban infill site that

housed a dry cleaner in the 1950’s may now be the ice cream

shop you’ve loved since you were a kid – who would ever think

it could be contaminated?

Assuming the developer of a brownfield property has acquired

a Phase One environmental assessment (and a Phase Two

environmental assessment if recommended by the Phase One)

By Patricia Gage, Principal, RE Solutions

and is ready to move forward with the project, potential project

investors should consider the following financial questions:

1. What is the cost of the land? In general, there should be a

discount for a brownfield parcel. When compared to an

equivalent clean site, the price of a brownfield should be

discounted by the cost to remediate the site plus some amount

to compensate for the risk inherent in the cleanup and the

additional profit that should come with cleaning up a

contaminated site.

2. Does the development budget include sufficient contingency for

normal construction risk as well as the risk of remediation cost

overruns or delays? While a 45% contingency is typical for a

greenfield site, the development budget on a brownfield should

include that standard contingency PLUS 2025% of the expected

remediation cost if the remediation contractor is working under a

costplus contract, which is typical. The contingency should

also be sufficient to cover any delays if remediation takes longer

than expected.

Have you considered adding

brownfield development

to your real estate portfolio?

Image by Dr StClaire from Pixabay

50. 50

3. Has the developer obtained environmental insurance? A

Pollution Legal Liability policy will protect against unknown

contaminants and thirdparty liability claims.

4. When you make your investment, will the balance of the

capital (debt and equity) be in place? If not, recognize that a

construction loan on a brownfield property will likely be

underwritten more conservatively than a loan on a greenfield

property. Some commercial banks won’t consider lending on

a brownfield. When a loan is available, the loantovalue and

loantocost ratios may be 510% lower than for a clean property.

5. Is there a financing gap that wouldn’t occur on a similar

greenfield property? Because debt and equity may be less

available for a brownfield site, the developer will often have

the option to cover remediation costs with a public finance

mechanism such as tax increment or special district financing.

Many municipalities have a Brownfields Revolving Loan

Fund to provide developers with lowcost debt to cover

remediation costs, which incents developers to clean up toxic

sites. Some states also offer tax credits for brownfields cleanup.

6. Is the project return reasonable given the risk associated with

a brownfield site? Developers expect a premium return for

taking on the risk of a contaminated property – investors

should be rewarded with a portion of that premium.

This is by no means an allinclusive list of due diligence an

investor should consider, or of the risks associated with brownfield

redevelopment. We always recommend obtaining appropriate legal

and tax advice before investing. That said, the best riskmitigation

strategy lies in underwriting the developer. Invest with those that

have significant brownfields experience and a proven track record.

Ask about their relationships with the regulatory agencies, lenders,

design professionals, contractors, prior investors, insurance

providers, and environmental consultants.

Real estate developers often raise money from individual

investors in relatively small increments, allowing qualified investors

the opportunity to participate directly in the success of a single

development project. These investments are not without risk, and

your due diligence should be thorough. Along with understanding

the project’s market, projected returns, construction risk, and

competition, an investor should be fully aware of the site’s prior

uses and any contamination that may be present.

Everyone can win in a brownfield redevelopment – you as an

investor, the developer, and the overall community. Financial

benefits are compelling but contributing to the elimination of blight

and toxic contamination in a neighborhood is the true reward.

MEET PATRICIA GAGE

Patricia Gage is a principal at RE Solutions, a

company specializing in creating value for

brownfield development projects. She can be

reached at patricia@resolutionsdev.com or

303.482.2618.

Image by Gordon Johnson from Pixabay

We always recommend obtaining

appropriate legal and tax advice

before investing. That said, the best

riskmitigation strategy lies in

underwriting the developer. Invest

with those that have significant

brownfields experience and a proven

track record.

Image by Arek Socha from Pixabay

55. 55

A

critical step for new and existing real estate

investors is to form an LLC or Limited

Liability Company. In the simplest of

terms, an LLC protects an investor’s

personal assets — whether those are cash,

bank accounts, or personal property.

Whether the investor is into flipping houses or being a landlord,

an LLC ensures that the person himself or herself does not actually

owe any debt. The company is responsible for any contracts, debts,

lawsuits, leases, and liabilities.

If business goes bad, the people and companies that believe they

are owed money can only pursue the LLC — not the individual(s)

behind the company unless fraud or another crime was involved,

according to Yahoo! Finance.

However, there are some critical steps to take even after a real

estate investor forms an LLC. Any properties must be purchased in

the company’s name, not an individual’s name. This ensures the

ultimate protection.

If someone buys a home to flip or rent out and ends up owing

more on the mortgage than the property is worth, the bank cannot

come after the individual if the home is officially owned by the

LLC.

A caveat is that many banks do not want to issue mortgage notes to

a new LLC, because it’s risky for them. That’s why a business plan is

so important. (See our past article 'House Flippers Need a Business

Plan' for a more indepth discussion on this topic.)

Other potential drawbacks to an LLC come at tax time and when an

individual transfers assets to it, so an attorney is probably a necessary

resource, according to LegalZoom.com. Also, each state has different

laws regarding an LLC.

However, done properly, an LLC seems to have more benefits than

downsides. Other good news is that the costs are usually minimal. As

always, before making any major decisions in such areas speak to a

qualified real estate attorney.

Sources for this article:

https://finance.yahoo.com/news/formllcrealestateinvesting

194323289.html

https://www.legalzoom.com/articles/forminganllcforrealestate

investmentsproscons

http://reiwealthmag.com/houseflippersneedabusinessplan/

By Stephanie Mojica

An llc

for Real Estate

Investing

Image by Gino Crescoli from Pixabay

60. 60

A

Wisconsin woman lost her entire retirement

savings by investing with a nowdeceased

friend’s business, My IRA, LLC, according to

the Milwaukee NBC television affiliate TMJ4.

It seems the company attempted to resemble an

SDIRA a SelfDirected Individual Retirement Account custodian.

My IRA, LLC was started by a tax preparer and purported

investor, Michael Cuccia, who suddenly died in November 2020,

according to TMJ4. When people who had invested in his company

sought the return of their assets, they were stunned to learn that most

of them were nowhere to be found, according to TMJ4.

Attorney Anne Cohen stated that her client Diane Conklin had a

401(K) account, but needed to figure out her best options when she

broke her back in 2012.

'She had learned that she could no

longer work and wanted to make sure that

the funds she had in her 401(K) were in a

secure account,” Cohen told TMJ4.

“Because she quickly was learning that was

all of the wealth she was going to amass in

her lifetime due to her disability.'

According to Cohen, Conklin knew Cuccia professionally and

also considered him a friend. Cuccia told Conklin to take her money

out of her 401(K) account and invest in his My IRA, LLC company,

according to a lawsuit Conklin filed against Cuccia’s estate.

Cuccia claimed Conklin had no risk of losing her assets and she was

guaranteed a 5% return on investment each year, according to Cohen.

“...after years and years of friendship and going to him for tax

advice, she trusted his advice,” Cohen told TMJ4.

After Cuccia’s sudden death, Conklin and others could not reclaim

their assets, according to Cohen.

People had invested anywhere from $5,000 to $200,000 with

Cuccia’s company, according to Cohen. The total was $1 million, but

Cuccia only had about $200,000 in assets, according to Cohen.

Anyone considering making an investment should be automatically

suspicious if they are told there is no risk involved, according to Robin

Jacobs from the Wisconsin Department of Financial Institutions

Enforcement Bureau.

Retirement Savings Lost

After Investment in

Fraudulent Company

Resembling SDIRA

Custodian

By Stephanie Mojica

Photo by Mikhail Nilov from Pexels

61. 61

'When you invest your money in

something, it means you're going to take

a risk in exchange for getting a return,”

Jacobs explained during her interview

with TMJ4.“Of course there's no

guarantee.'

Investors should also steer clear if one or more of the

following warning signs are present:

• A vague or confusing business model.

• Time limits on when you can invest.

• Highpressure sales tactics.

• A lack of disclosure documents.

• No audited financial records.

Wouldbe investors should also research whether the person

they’re talking to has the proper training and licensure.

In Wisconsin, that can be cleared up with a phone call to the

Department of Financial Institutions Enforcement Bureau.

“...we can tell (you) whether that person is registered either as

an investment advisor or a brokerdealer and if they're not

registered...I would be very suspicious of that person,” Jacobs

said during her interview with TMJ4.

Some brokerdealers and investment advisors must register with

FINRA (the Financial Industry Regulatory Authority) or the SEC

(the Securities and Exchange Commission), while others do not. It

depends on whether the professional does business in one or

multiple states.

The regulation bodies for other states include:

• California Department of Business Oversight

• Texas State Securities Board

• Idaho Department of Finance

• New York State Attorney General

• Arizona Corporation Commission

• Nevada Secretary of State

• Florida Office of Financial Regulation

Any inquiry to your local business licensing or permits office or

a quick Google search should point you in the right direction.

Back to Cuccia’s purported victims, the future is unknown.

Conklin and other people who claim they were swindled by

Cuccia are waiting to see if the courts will award them any of

what’s left from his estate, according to TMJ4.

Attorneys representing Cuccia’s estate declined to be

interviewed by TMJ4.

Image by mohamed Hassan from Pixabay

67. 67

A

n important caveat to

real estate investment,

quite simply, it’s

expensive. It requires

more capital upfront

to get going, and for a lot of potential

investors, it just isn’t feasible. But Victor

Cuevas, founder of Griffin Crowd and

Capital, just might have the answer, and

it’s a surprising, but innovative one. He

suggests using crowdfunding!

When we typically think of

investments, the stock market comes to

mind. However, real estate is emerging

as a competitive alternative to stocks,

one that is safer and can often yield

higher returns. But like so much else in

business, real estate investments lead to

portfolio diversity.

Whatever side of the fence you are

currently on, as either a borrower or

investor, see below for a few tips from

Cuevas to get you started.

Learn about Splitting the Bill

As it turns out, investing in real estate

may not be as costly as it seems. With the

rising popularity of crowdfunding —

online platforms for sourcing capital for a

given project — a creative new approach

has emerged for breaking into the

prohibitively expensive, but wildly

lucrative field of real estate investment.

With a little help from crowdfunding,

you could soon be on your way to

making big bucks, while at the same

time, shaking things up along the way.

Cuevas recommends crowdfunding as a

way to expand your possibilities and

adapt to the rising cost of homes. In the

past year alone, Griffin Crowd and

Capital has crowdfunded over 100

residential apartment complexes totaling

tens of millions in profit as a result.

Find Strength in Numbers

David and Goliath was a close one, but

ultimately, the “little guy” triumphed by

sheer ingenuity. Now imagine if it had

been 10 Davids, all equally resourceful,

taking on that single Goliath — it would

almost be unfair. And that’s the idea here.

Cuevas recommends using crowdfunding

as a way of teaming up and pooling

resources to collectively achieve what is

too often reserved for the already wealthy.

It is a great way to challenge the

longstanding dynamic of the “fat cat”

being the one at the top.

Strength in Numbers:

Victor Cuevas Gives Us Advice About

Crowdfunding as a Tool for Investments

By Victoria Kennedy

'Borrowers using a crowdfunding portal have an

advantage because they can get funds from a

wider pool of investors,' said Cuevas. 'While they

typically have to accept a higher interest rate in

order to get additional funds, the access to those

additional investors is typically worth it.'

Victor Cuevas

68. 68

A Man’s Game? Don’t be So Sure

Any number of factors can explain

the demographic disparity of real estate

investment, and investment in general.

From systemic and interpersonal sexism

and racism, to toxic notions surrounding

women and investment in general,

there’s no question: it’s an uphill battle

for women and minority investors.

But one thing is for sure, regardless

of this inadequate representation, there’s

zero truth to any notion that nonmale,

individuals are in any way, shape, or

form “less fit” for the field. The truth is,

there’s just more to work against. While

this may seem so obvious, nevertheless,

the myths floating around can still be

damaging. The key is to try not to be

dissuaded by all these ‘tall tales’—you

know what you’re capable of. As Cuevas

said, “it’s a fastgrowing market” and

now is the best time to get involved!

Learn Where to Invest Sensibly

Real estate is a huge field encapsulating

all sorts of different subcategories

within it. If you’re seeking to maximize

your returns all while keeping your

overhead to a minimum, Cuevas

recommends looking at multifamily

residentials. These have emerged as

popular living arrangements, and they’re

generally cheaper and easier to invest in

than larger properties. Between

collecting rent and easier mortgage

terms, there are numerous advantages

that should put the multifamily

residential towards the very top of your

list when it comes to prospective real

estate investments.

Pick a Winner: Choose the

Right Bank

When investing in real estate, it’s

essential to choose a bank that’s a good

fit for your investments. Cuevas suggests

paying close attention to the experience

and track record of the institutions you

consider. It’s important to be certain that

the bank you go with has enough

experience in the area you’re investing in

to best assist your specific needs. For

example, at Griffin Crowd and Capital,

Cuevas puts his 30plus years of specific

experience in the field at the disposal of

his clients — all the knowledge, know

how, and vital industry connections go

into helping clients ensure the maximum

possible return on their investments.

It can be a daunting prospect, but with

the right approach, investing could

become your next successful venture.

With crowdfunding, it doesn’t have to

cost an arm and a leg, and by focusing on

real estate, particularly multifamily

residentials, you can start generating

wealth easily and with little risk. While

there may indeed be some obstacles

standing in your way, with the help of

creative solutions, careful planning, and a

little teamwork, it might not be such a

distant dream.

MEET VICTOR CUEVAS

Victor Cuevas is

an industry

professional with

over 30 years of

mortgage finance

experience,

including extensive

knowledge in both residential and

commercial properties. He is a successful

serial entrepreneur with a multitude of

accomplished companies and ventures.

Among them, Victor built a mortgage

empire, spanning 36 offices in several

western and central states. He currently

serves as the founder of Griffin Crowd &

Capital, the next chapter in an already

illustrious career. For more information,

visit griffincrowdcapital.com

Image by Júlio Cesar J.Cesar from Pixabay

Image by Credit Commerce from Pixabay

77. 77

O

n paper, a NNN lease

might seem like a

lowrisk longterm

investment. But like

with any investment,

paying attention to the details can mean

the difference between profit and loss.

This is especially true now more than

ever in our ever changing, fastpaced

world.

In this article, we’ll discuss NNN

leases and what makes it a good

investment. We’ll also offer a case study

(specifically CVS) in order to

demonstrate how investing in a NNN

lease can go wrong. Risk is built into any

investment, but there are ways you can

minimize these factors to set yourself up

for greater success.

What is a NNN Lease?

The triple N acronym describing this

particular lease stands for the following:

● Net of property taxes

● Net of maintenance

● Net of insurance

These types of leases describe a

commercial property that’s often leased

for years at a time. Most of the time,

tenants are bigbox stores that plan on

taking up residence for a long period.

After all, it’s hard to do business and

keep your loyal customers if you keep

relocating.

Why is a NNN Lease a Good

Investment?

In terms of risk, NNN leases score

lower than most investments. At the

same time, that doesn’t mean they’re

without risk completely. As long as you

have the right tenant and right

property, the risks are low enough to

make a NNN lease an excellent source of

passive income.

Another — and potentially the most

attractive — reason NNN leases are low

risk lies in the relationship between

landlord and tenant. In a typical landlord

tenant agreement, the tenant is responsible

for upkeep and maintenance, along with

taxes, insurance, and, of course, rent.

This potentially makes NNN leases a

great investment if everything goes well,

but that is not always the case.

What Makes for a Good NNN

Lease

As we mentioned, it’s important to

choose the right tenant and right property

when it comes to investing in a NNN

lease. Passive income loses definition if

you have to be constantly involved, so

making a smart decision here could save

you time, money, and headaches later on.

The right tenant, in this case,

resembles a quality candidate with a

strong balance sheet and a nationally

recognizable name. Highquality credit

tenants do the best.

Though the right tenant may look

different in each circumstance, the right

property certainly has similar qualities

across the board. For instance, buildings

that are newer may be more desirable,

since the upkeep costs should

theoretically be less. At the same time,

new doesn’t always translate to quality,

so be cautious.

The bottom line is that NNN leases are

longterm investments. Most tenants will

sign a 10 to 20year lease. This makes

NNN leases a powerful investment, even

if inflation occurs. In most leases there

will even be a provision built into the

terms to help combat inflation.

Picking The Right NNN Lease

& The Downfall of CVS

By Clinton Lu, TFS Properties

Image by mohamed Hassan from Pixabay

78. 78

How a NNN Lease Can Go

Wrong

If you’ve kept an eye on the news

recently, you’ll know that CVS plans to

close roughly 900 stores over the next

three years as they shift their focus away

from their drug store facilities to a more

health care based model. For landlords

who hold the NNN leases for those

particular stores, what began as a lowrisk

investment has now become a need to

reinvest and, in some cases, recoup

losses.

While CVS might be at the forefront

of the public eye, it’s not alone in

responding to the changing consumerism

market. In fact, industry projections

demonstrate “that if online shopping

grows from 18% of retail sales today to

27% in five years, it projects that some

80,000 retail stores will close while

others may arise.” Why keep the brick

andmortar doors open if all your

customers are purchasing from you online?

This pivot from drug store to

healthcare facility also gained momentum

with CVS’s acquisition of Aetna in

2018, alongside the possession of

Caremark. With the pressure of online

prescription drug retailers, CVS began

shifting their business model and

liquidating many of their brink and

mortar locations. For landlords, losing

such a large tenant (and income source),

meant that the search had to begin again

to find a quality, longterm tenant. Often

times this is a tricky process and in the

face of rapidly growing ecommerce,

those tenants may not be as easy to find.

Choose the Right Investment

Here at TFS Properties, Inc., we

foresaw the closing of CVS and

Walgreens and advised our clients

accordingly. With an eye on the push to

drive pharmacy business online,

accelerated by the pandemic’s impact on

sales, it was only a matter of time.

In general, we have steered our clients

away from these types of investments

and more towards industries that we find

are more recession resilient. Changing

ways in how consumers spend their

money makes it hard to compete,

especially where technology is involved.

As such, we put our investors into the

types of investments that have proved

their resilience during the previous

recession as well as the pandemic.

Owning a property with recession

resilience is something every investor

should integrate into their game plan.

We hope you’ve found this article

helpful in differentiating between

profitable NNN lease opportunities.

There are many options out there and

picking the right NNN Lease can mean

the difference between making or losing

money on your investment.

For further questions, feel free to

reach out to us at 6265514326.

'that if online shopping grows from 18% of

retail sales today to 27% in five years, it

projects that some 80,000 retail stores will

close while others may arise.'

Image by mohamed Hassan from Pixabay

82. 82

A

re all loans second to

NONI (NonOwner,

No Income) for cash

flow purposes? Does

your investment

property give you a positive annual cash

flow with or without significant vacancy

rates, repairs, nonpayment of rents due

to tenant moratoriums or other reasons,

and costly management expenses? How

many investment property owners are

stuck with high 7% to 10%+ private

money or an expensive 30year fixed

mortgage that creates negative monthly

cash flow? The NONI interestonly loan

or fully amortizing loan with 7, 10, 30,

and 40year fixed terms is an exceptional

financial choice.

NONI InterestOnly Loans

First off, can you afford your monthly

mortgage payment? Without positive

cash flow and the ability to pay your

mortgage payments on time, your

investment properties may be at risk for

future forbearance, loan modification, or

distressed sale situations where you

could later lose your positive equity in a

future foreclosure. The combination of

positive cash flow and compounding

equity gains should be the primary goal

for investors instead of having

unaffordable mortgage payments.

Here’s some eyeopening NONI loan

products highlights that keep customers

coming back for more NONI products,

especially if the investor owns 2, 5, 10, or

20+ rental properties:

• Starting interestonly rates as low as

3.875%*

• Designed for business purpose 14 unit

residential loans in most states

• No income or employment collected

on the loan application

• Loan amounts to $3.5 million for non

owner properties

• No 4506T, tax returns, W2s or pay

stubs

• Qualification is based on property

cashflow, NOT borrower income

• First time investors allowed

• Multipurpose LLC allowed

• Unlimited cashout up to 75% LTV

• As little as 0 months reserves (use cash

out for reserve qualifications)

• NONI doesn’t care how many

properties a borrower owns

• The lower I/O payment (when I/O

option is chosen) is used when

calculating DSCR and cash reserves

• 85% LTV available for purchase and

rate/term transactions (680+ FICO)

• Rental income is taken from an

existing lease or the rent survey from

the appraisal and compared to the

mortgage payment to determine debt

coverage ratio. (ALL program

guidelines and rates subject to change

and qualification.)

The Non-Owner,

No Income (NONI)

Loan Solution

By Rick Tobin

Image by ErikaWittlieb from Pixabay

The combination

of positive cash

flow and

compounding

equity gains should

be the primary goal

for investors

instead of having

unaffordable

mortgage

payments.

83. 83

Loan amount: $1,000,000

30year fixed rate payment:

$4,702.37/mo. (principal and interest)

10year fixed interestonly:

$3,229.17/mo.

Loan amount: $2,000,000

30year fixed rate payment:

$9,404.74/mo. (principal and interest)

10year fixed interestonly:

$6,458.33/mo.

Loan amount: $3,000,000

30year fixed rate payment:

$14,107.11/mo. (principal and interest)

10year fixed interestonly:

$9,687.50/mo.

*APRs from 4.79%: The 10year fixed

loan converts to an adjustable for the

remaining 20 or 30 years with 30year

and possible 40year loan term options.

There are also 30year and 40year fixed

interestonly loan programs at higher

rates (ALL rates and programs subject to

change.)

For traditional loan programs, many

lenders will take 75% of your gross rents

to qualify for a new mortgage loan

because the lender assumes that you

have vacancies, repairs, and property

management fees. For easy math, a

rental property with $1,000 per month in

gross income is underwritten as if it were

$750 per month and another pricier

property with $10,000 per month in

rental income is analyzed as if it were

$7,500 per month.

For NONI, on the other hand, you can

qualify at 1.0 DSCR (Debt Service

Coverage Ratio) or breakeven levels.

For example, your rental home averages

$2,000 per month, so your newly

proposed mortgage payment (including

property taxes, insurance, and

homeowners association fees, if

applicable) must be equal or lower to

that same gross rental income. As a

result, it’s much easier to qualify for a

NONI loan product than any other

residential mortgage loan that I know of

today.

30Year Fixed vs. 10Year

InterestOnly

A 30year mortgage payment doesn't

usually begin to pay down any significant

amount of loan principal until after the

7th year. The average mortgage borrower

keeps their loan for nearly seven years,

so an interestonly loan product can be a

much more solid choice today for many

borrowers.

Let's compare the fully amortizing 30

year fixed payment with a 10year

interestonly payment with cashout

options to see the difference for the same