Recommended

More Related Content

Viewers also liked

Viewers also liked (20)

Calculate Income Tax in Spain

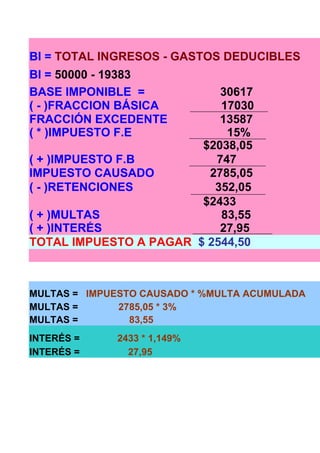

- 1. BI = TOTAL INGRESOS - GASTOS DEDUCIBLES BI = 50000 - 19383 BASE IMPONIBLE = 30617 ( - )FRACCION BÁSICA 17030 FRACCIÓN EXCEDENTE 13587 ( * )IMPUESTO F.E 15% $2038,05 ( + )IMPUESTO F.B 747 IMPUESTO CAUSADO 2785,05 ( - )RETENCIONES 352,05 $2433 ( + )MULTAS 83,55 ( + )INTERÉS 27,95 TOTAL IMPUESTO A PAGAR $ 2544,50 MULTAS = IMPUESTO CAUSADO * %MULTA ACUMULADA MULTAS = 2785,05 * 3% MULTAS = 83,55 INTERÉS = 2433 * 1,149% INTERÉS = 27,95