The monetary policy committee in Nigeria voted to hike the monetary policy rate by 2 percentage points to 14%, surprising markets who expected no change. Inflation is high and rising in Nigeria, with negative real interest rates, so the committee prioritized price stability over economic growth. By raising rates, the central bank aims to support the recently liberalized foreign exchange policy and improve foreign inflows to boost liquidity. Further rate hikes are expected as inflation climbs into the early 20s by the fourth quarter of 2016.

Summary of the CBN Governor’s Press Conference on the Flexible Exchange Rate ...

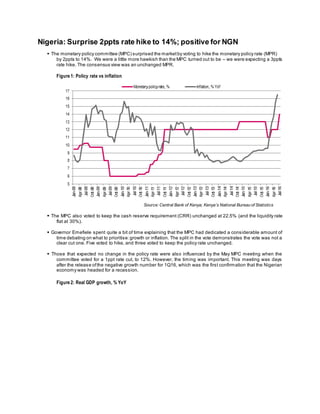

Nigeria. Surprise 2ppts rate hike to 14%; positive for NGN

1. Nigeria: Surprise 2ppts rate hike to 14%; positive for NGN

The monetary policy committee (MPC) surprised the marketby voting to hike the monetary policy rate (MPR)

by 2ppts to 14%. We were a little more hawkish than the MPC turned out to be – we were expecting a 3ppts

rate hike. The consensus view was an unchanged MPR.

Figure 1: Policy rate vs inflation

Source: Central Bank of Kenya; Kenya’s National Bureau of Statistics

The MPC also voted to keep the cash reserve requirement (CRR) unchanged at 22.5% (and the liquidity rate

flat at 30%).

Governor Emefiele spent quite a bit of time explaining that the MPC had dedicated a considerable amount of

time debating on what to prioritise:growth or inflation. The split in the vote demonstrates the vote was not a

clear cut one. Five voted to hike, and three voted to keep the policy rate unchanged.

Those that expected no change in the policy rate were also influenced by the May MPC meeting when the

committee voted for a 1ppt rate cut, to 12%. However, the timing was important. This meeting was days

after the release ofthe negative growth number for 1Q16, which was the first confirmation that the Nigerian

economy was headed for a recession.

Figure 2: Real GDP growth, % YoY