1. 6363 Woodway Dr Suite 870

Houston, TX 77057

Phone: 713-244-3030

Fax: 713-513-5669

Securities are offered through

RAYMOND JAMES

FINANCIAL SERVICES, INC.

Member FINRA / SIPC

Green Financial Group

An Independent Firm

Weekly Commentary by Dr. Scott Brown

The Job Market – More of The Same...

October 11 – October 15, 2010

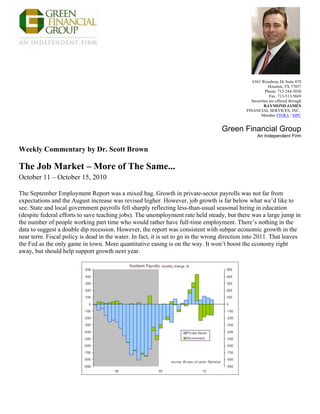

The September Employment Report was a mixed bag. Growth in private-sector payrolls was not far from

expectations and the August increase was revised higher. However, job growth is far below what we’d like to

see. State and local government payrolls fell sharply reflecting less-than-usual seasonal hiring in education

(despite federal efforts to save teaching jobs). The unemployment rate held steady, but there was a large jump in

the number of people working part time who would rather have full-time employment. There’s nothing in the

data to suggest a double dip recession. However, the report was consistent with subpar economic growth in the

near term. Fiscal policy is dead in the water. In fact, it is set to go in the wrong direction into 2011. That leaves

the Fed as the only game in town. More quantitative easing is on the way. It won’t boost the economy right

away, but should help support growth next year.

2. The impact of the 2010 census on payrolls is mostly behind us (as of mid-September, there were only 6,000

temporary workers remaining). We’ve also seen a decrease in state and local government payrolls in recent

months (down 1.2% over the 12 months ending in September). Some of this drop is in education (which fell

58,000 last month, largely reflecting reduced seasonal hiring at the start of the school year). The (seasonally

adjusted) decline in education came despite federal aid to save teacher jobs. However, ex-education, state and

local government payrolls fell by 1.7% over the last 12 months. Normally, one looks to the government to

provide some base of support in tough economic times. Instead, state and local government is adding to overall

economic weakness.

Contrary to expectations, the unemployment rate and the employment-to-population ratio held steady in

September. However the BLS reported a sharp jump in involuntary part-time workers. The U-6 measure of

unemployment (which includes discouraged workers and involuntary part-time workers) rose to 17.1% in

September, from 16.7% in August and 16.5% in July (it was 17.0% a year ago). We need to see much stronger

job growth (monthly gains in nonfarm payrolls on the order of 200,000 to 300,000 or more) to push the

unemployment rate down significantly. That kind of job growth does not seem likely to occur over the next few

quarters.

The Bureau of Labor Statistics has released its initial estimate of the annual benchmark revision to nonfarm

payrolls (to be implemented with the release of the January 2011 jobs report in early February). The March

2010 payroll figure is expected to be revised down by 366,000. That’s a large revision by historical standards,

but not as bad as feared (and well below the monster -902,000 revision to March 2009 reported earlier this

year).

3. The September Employment Report is consistent with a lackluster-to-moderate pace of economic growth in the

near term and the outlook doesn’t look much better for the next few quarters. Further Fed accommodation won’t

provide a strong lift in the near term, but should prevent the economy from weakening much further in 2011.