Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Similar to Financial planning essential amid pension crisis

Similar to Financial planning essential amid pension crisis (20)

Financial planning essential amid pension crisis

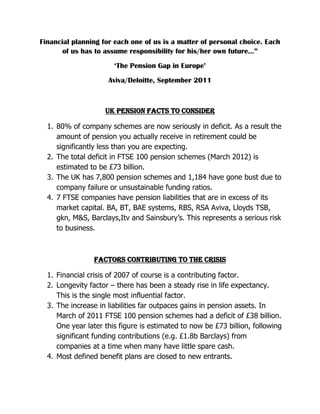

- 1. Financial planning for each one of us is a matter of personal choice. Each of us has to assume responsibility for his/her own future…” ‘The Pension Gap in Europe’ Aviva/Deloitte, September 2011 UK Pension FACTS to consider 1. 80% of company schemes are now seriously in deficit. As a result the amount of pension you actually receive in retirement could be significantly less than you are expecting. 2. The total deficit in FTSE 100 pension schemes (March 2012) is estimated to be £73 billion. 3. The UK has 7,800 pension schemes and 1,184 have gone bust due to company failure or unsustainable funding ratios. 4. 7 FTSE companies have pension liabilities that are in excess of its market capital. BA, BT, BAE systems, RBS, RSA Aviva, Lloyds TSB, gkn, M&S, Barclays,Itv and Sainsbury’s. This represents a serious risk to business. Factors contributing to the crisis 1. Financial crisis of 2007 of course is a contributing factor. 2. Longevity factor – there has been a steady rise in life expectancy. This is the single most influential factor. 3. The increase in liabilities far outpaces gains in pension assets. In March of 2011 FTSE 100 pension schemes had a deficit of £38 billion. One year later this figure is estimated to now be £73 billion, following significant funding contributions (e.g. £1.8b Barclays) from companies at a time when many have little spare cash. 4. Most defined benefit plans are closed to new entrants.

- 2. 5. Changes in pension rules and accounting practices, such as BAE’s introduction of LAF or longevity adjustment factor, significantly reduce benefits payable. Changes to CPI from RPI also play a role. 6. Asset allocation and historically low interest rates. Questions you should ask yourself 1. Do you know that defined benefit pension are not guaranteed? 2. When did you see your last valuation? How have your investments performed? 3. When can you access your pension? 4. Do you like paying a high rate of tax on your money? 5. What will happen to your pension when you die? There are solutions today for your pension problem. Kevin McNee 646-664-0687 kevin.mcnee@devere-group.com