1. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 9, 2016

Consumer Finance

Discover Financial Services

Key Drivers:

Economic growth and interest rates: 97% of DFS’s revenues come from

interest income. I expect a 3.5% increase in loan receivables which will drive

up interest income.

Net charge-off rate: DFS has a very low net charge-off rate compared to its

peers, which gives the firm an edge when it comes to increasing sales and

improving margins.

Housing starts: An increase in housing starts is positive for sales.

Student loans: Student loans generate the second most revenue behind credit

card loans. Student loans have grown by 2.3% and growth is expected to

continue at 3.2% in 2016.

Valuation: Using a relative valuation approach, Discover Financial appears to be

undervalued in comparison to other revolving credit firms. DCF analysis provides the

best way to value the stock because of the ability to fine tune inputs. A combination

of the approaches suggests that DFS is undervalued, as the stock’s value is about $62

and the shares trade at $55.23.

Risks: Threats to the business include a decrease in credit card rates, an increase in

the deposit rate, a rise in the unemployment rate, and a rise in the charge-off rate.

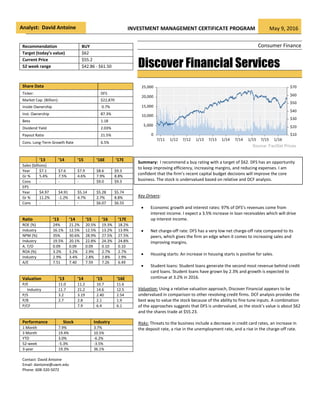

Recommendation BUY

Target (today’s value) $62

Current Price $55.2

52 week range $42.86 - $61.50

Share Data

Ticker: DFS

Market Cap. (Billion): $22,870

Inside Ownership 0.7%

Inst. Ownership 87.3%

Beta 1.18

Dividend Yield 2.03%

Payout Ratio 21.5%

Cons. Long-Term Growth Rate 6.5%

‘13 ‘14 ‘15 ‘16E ‘17E

Sales (billions)

Year $7.1 $7.6 $7.9 $8.6 $9.3

Gr % 5.4% 7.5% 4.6% 7.9% 8.8%

Cons - - - $9.0 $9.3

EPS

Year $4.97 $4.91 $5.14 $5.28 $5.74

Gr % 11.2% -1.2% 4.7% 2.7% 8.8%

Cons - - - $6.07 $6.55

Ratio ‘13 ‘14 ‘15 ‘16 ‘17E

ROE (%) 24% 21.2% 20.5% 19.3% 18.2%

Industry 16.1% 12.5% 12.5% 13.2% 13.9%

NPM (%) 35% 30.6% 28.9% 27.5% 27.5%

Industry 19.5% 20.1% 22.8% 24.3% 24.8%

A. T/O 0.09 0.09 0.09 0.10 0.10

ROA (%) 3.2% 3.2% 2.9% 2.7% 2.7%

Industry 2.9% 3.4% 2.8% 2.8% 2.9%

A/E 7.51 7.40 7.59 7.26 6.49

Valuation ‘13 ‘14 ‘15 ‘16E

P/E 11.0 11.2 10.7 11.6

Industry 11.7 21.2 14.6 12.5

P/S 3.2 3.19 2.40 2.54

P/B 2.7 2.8 2.1 1.9

P/CF 7.9 6.4 6.1

Performance Stock Industry

1 Month 7.9% 3.7%

3 Month 19.4% 10.5%

YTD 3.0% -6.2%

52-week -5.3% -3.5%

3-year 19.3% 36.1%

Contact: David Antoine

Email: dantoine@uwm.edu

Phone: 608-320-5072

Analyst: David Antoine

Summary: I recommend a buy rating with a target of $62. DFS has an opportunity

to keep improving efficiency, increasing margins, and reducing expenses. I am

confident that the firm’s recent capital budget decisions will improve the core

business. The stock is undervalued based on relative and DCF analysis.

2. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 9, 2016

2

Company Overview

Discover Financial Services (DFS) is a direct banking and payment services company, headquartered in

Riverwoods, IL. Through its subsidiaries, the company provides direct banking and payment services to its

customers. The Direct Banking segment includes consumer banking products such as credit card loans,

checking and savings account, and lending products such as private student loans, personal loans, and

home loans. The Payment Services segment is comprised of the Discover Network, Pulse, and Diners

International Club. Discover Network is responsible for processing all the Discover-branded credit card

transactions that occur in United States. Pulse, acquired in 2005, provides ATM/debit network services to

banks, credit unions, and saving institutions across United States. It also gives credit and debit cardholders

full access to ATMs domestically and internationally. Unlike many banks and credit card companies,

Discover is the only credit card issuer that offers direct banking and payment services while owning its

receivables.

Discover Financial Services generates 97% of its revenue from interest income earned on private student

loans, credit card loans, and home loans through Direct Banking. The remaining 3% is from payment and

network services, such as fees earned from merchants for processing transaction payments. The following

are the main business activities of each segment:

Direct Banking: This segment includes Discover Card, Discover Bank, and Discover Home Loans.

Discover Card is one the largest credit card issuers in the United States, and also a major source

of revenue for Discover Financial Services. For instance, in 2015 interest income from credit card

loans alone was 76% of net revenue and 75% the year prior. Discover Bank provides personal

loans, home loans services, and is the third largest private student loans provider in the United

States, behind Sallie Mae and Wells Fargo. Discover Home Loans offers home financing, and

home equity services. In 2015, Direct Banking grew 4.6%.

Payment Services: Represents a very small portion of the company’s total revenue. As showed in

the pie chart below, this segment only generates 3% of the total revenue due. However, it does

provide Discover with some international exposure through Diners Club International, which

offers a multi-purpose charge card that is accepted in more than 185 countries.

Figures 1 and 2: Revenue sources for DFS, year-end 2014 (left) and revenue history since 2005 (right)

Source: FactSet

Direct Banking

97%

Payment Services

3%

DFS Payment Services

segment has been

struggling for the past

six years and will

continue to do so

because MA and V alone

own 80% of this market.

3. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 9, 2016

3

Source: DFS financial reports (2015)

Geographic Distribution of DFS loans

Discover Financial Services is primarily located in the United States. As indicated below, the firm has

customers throughout most of the country and they continue to grow. In 2015, the firm increased its

national presence by 3% when compared to 2014. Discover’s primary goal has been to increase loans

growth by acquiring new customers that will generate more interest income. DFS has been doing that

through direct mail and emails to existing and potential customers. The firm has tried to increase its

international exposure by acquiring Diners Club International, which was supposed to allow it to compete

internationally with Visa and American Express. Unfortunately, the acquisition failed to meet the

expectations and poor performance forced DFS to sell the business operations of Diners Club Italy on

October 1, 2015.

Figures 3, 4: Geographic distribution of DFS credit card loan receivables (top left), personal and private student loans (top right) 2105,

DFS credit card loan receivables (bottom left), and personal and private student loans (bottom right) 2014

Business/Industry Drivers

Although multiple factors may contribute to Discover Financial Services’ future earnings, the following are

the key business drivers:

1) Economic growth and interest rates

2) Net charge-off rate

3) Housing starts

4) Student Loans

Economic growth and interest rate

Interest income is a major source of revenue for the company. Interest income is derived from the

interest earned on personal loans, home loans, private student loans, and revolving credit card balances.

However, interest income earned on revolving credit card balances is the most crucial of all, and makes up

83% of the total revenue last year. This means that DFS is highly influence by the state of the economy

and interest rates.

GDP growth is positively correlated with credit growth (0.56 correlation figure 5). The Fed Funds rate is

positively correlated with interest expense as a percent of loans (0.56 correlation figure 6). It is also

negatively correlated with the net interest spread. The net interest spread and loan growth drive the

majority of earnings. Also net interest income is related to interest rates.

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2015-Credit card loans %

0%

10%

20%

30%

40%

50%

2015-Personal and student loans %

DFS significantly

reduce its effort to

grow its business

internationally

DFS relies heavily on

interest income, which is

driven by credit card and

private student loan

growth.

4. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 9, 2016

4

Source: FactSet

Figures 5: Consumer Credit Outstanding, Revolving, Sa & GDP, Current Prices, Saar

Source: FactSet

Figures 6: Fed Funds Rate & Interest expense as a percentage of loans

Net charge-off rate

The charge-off rate can significantly impact profitability. One can see that DFS has a lower charge-off rate

than the average of the industry. This is driven by unemployment (0.94 correlation figure 10).

The correlation between the Federal Reserve charge-off rate and Discover is about 0.86. The better the

economy, the lower the unemployment rate, and in turn, the lower the Federal and Discover charge-off

rates.

DFS has one of the lowest

charge-off rates in the

industry.

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

3/1997

3/1998

3/1999

3/2000

3/2001

3/2002

3/2003

3/2004

3/2005

3/2006

3/2007

3/2008

3/2009

3/2010

3/2011

3/2012

3/2013

3/2014

3/2015

3/2016

(% 1YR)Consumer Credit Outstanding, Revolving, Sa - United States (Left)

(% 1YR)Gdp, Current Prices, Saar - United States (Right)

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Fed Funds Rate (Left) Interest Expense as a % of loans (Right)

5. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 9, 2016

5

-L

Source: Bloomberg Federal Reserve US Charge-Off Rat Index Source: Bloomberg Discover Charge-Off Rate Index

The firm provides customers with access to free credit scores and many financial tools to help them

monitor their accounts efficiently. Also, DFS charges a very low interest rate and providing 24/7 customer

service.

Housing starts

Housing starts is one of the most watched economic indicators in the country, since it greatly impacts

banking and consumer wealth. An increase in housing starts generally suggests that consumers feel good

about the economy and it is related to rising in consumer spending and falling unemployment. This is

clearly shown by the figure 15, Discover’s sales per share rises when housing starts increase (yearly

correlation of 0.82). Discover offers home loans, home equity, and mortgages, which give Discover a slight

advantage over its peers when it comes to diversification. Also, new home sales drive home related sales,

such as furniture which may be purchased with credit cards.

Figures 7, 8 and 9: Unemployment compared to Federal Reserve US charge-off rate (top), Federal Reserve charge-off rate compared to DFS

(bottom left), and DFS charge-off compared to DFS stock price (bottom right)

Source: Bloomberg Unemployment

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

Unemployment Rate (Left) Federal Reserve US-Charge Off Rate (Right)

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

Discover Net Charge-Off (Left)

Federal Reserve US-Charge Off Rate (Right)

$0.0

$12.0

$24.0

$36.0

$48.0

$60.0

$72.0

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

Discover Net Charge-Off (Left) DFS Stock Price (Right)

6. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 9, 2016

6

Student loans

Private student loans is the second largest source of revenue after credit card loans. It has tremendous

impact on operating margin which is driven by a steady increase in interest yield (correlation of 0.97). DFS

private loan receivables is also highly correlated to the student loan owned and securitized index

(correlation of 0.73).

Financial Analysis

I anticipate EPS to grow to $5.28 in FY 2016. I forecast a decrease in EBT Margin due to total operating

expenses increasing at a faster rate (CAGR of 10.8% during 6 years) than interest income (CAGR of 4.4%

during 6 years). This rapid increase in total operating expenses is caused by higher regulatory and

compliance staffing as well as higher compensation and professional fees related to anti-money

laundering remediation expenses.

Figure 11 and 12: Student loan owned and securitized (right) and DFS operating margin and interest yield on student loan

Source: Bloomberg/IMCP

Figure 10: Housing starts compared to sales per share

Source: FactSet

$0

$5

$10

$15

$20

$25

$30

0

200

400

600

800

1,000

1,200

Housing starts Sales PS - LTM(Left) (Right)

-L

-R

-R-L

7. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 9, 2016

7

Figure 13 & 14: Quantification of 2016 EPS drivers (left) and comparison of interest income, total operating cos, and interest expense

On the other hand, net interest margin with slightly increases and adds $0.08 because interest income is

growing faster (CAGR of 6.6% during 6 years) than interest expense (CAGR of 8.7% during 6 years).

Interest income will rise which will add $0.29, driven primarily by continued loan growth and an increase

in interest rates.

I foresee EPS to continue to grow to $5.74 in 2017. I envisage interest income ($0.49) to continue to

improve significantly as a result of continued loan growth, mainly from a considerable growth in personal

loan receivables and a slight increase in student and credit card loan receivables. I expect net interest

margin to add ($0.14) resulting from a decrease in interest expense due to the sale of Diners Club Italy. I

anticipate EBT margin to fall due to higher operating costs, but the drag on earnings will be less than

2016.

Figure 15: Quantification of 2017 EPS drivers

I am slightly more pessimistic than consensus estimates for 2016 and 2017. This is partly due to my

assumption of no share buybacks in 2016 and 2017.

Source: Company Reports, IMCP

On 04/16/15, DFS’s board

of directors approved a

share repurchase program

allowing the repurchase of

up to 2.2 billion of its

outstanding shares of

common stocks. This

program expires on

07/31/2016

Source: Company Reports, IMCP

$0.49

$0.14 ($0.18) $0.02

$5.74$5.28

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$0

$2,000

$4,000

$6,000

$8,000

$10,000

Interest Income Net Interest Income

Total Operating Expenses Interest expense

$0.29

$0.08

($0.32) $0.08

$5.28$5.14

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

8. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 9, 2016

8

Revenue

Discover Financial Services’ revenue has been rising each year since 2008. I anticipate that trend to

continue in 2016 and 2017. I expect a sharp increase in total loans and direct deposits. This will drive up

interest income and net interest income.

Q1 2016E Q2 2016E Q3 2016E Q4 2016E FY 2016E Q1 2017E Q2 2017E Q3 2017E Q4 2017E FY 2017E

Revenue - Estimate $2,224 $2,305 $2,150 $1,892 $8,571 $2,229 $2,275 $2,425 $2,397 $9,326

YoY Growth 2% 6% -2% -14% 8% 0% -1% 13% 27% 9%

EPS - Estimate $1.42 $1.40 $1.25 $1.21 $5.28 $1.47 $1.49 $1.32 $1.46 $5.74

YoY Growth 11% 5% -9% 6% 3% 4% 6% 6% 21% 9%

EPS - Consensus $1.42 $1.49 $1.42 $0.01 $5.65 $1.47 $1.50 $1.58 $1.48 $6.55

YOY Growth 6% 7% 8% 25% 10% 9% 6% 6% 5% 7%

Diners Club Italy (which

was part of Payment

Services segment)

acquired in 2013 was sold

on October 1, 2015. DFS

also stopped providing

financial assistance for the

purchase of the Slovenian

licensee by a European

Bank.

The AML/BSA look-back

project will be largely

complete in the first half

of 2016. This will result

in huge savings for DFS

since it was a huge

burden on earnings

Figure 16: EPS and YOY growth estimates

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

Sales Growth

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Net Interest Income Growth

Figure 17: DFS sales growth, 2011-2017E

Figure 18: DFS net interest income growth, 2011-2017E

Source: Company Reports, IMCP

Source: Company Reports, IMCP

Source: Company Reports

9. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 9, 2016

9

Figure 19: Interest Income vs YoY interest income growth, 2011 – 2017E

Operating Income and Margin

Operating expenses are composed primarily of employee compensation and benefits, marketing and

business development, professional fees, and other expense.

I also predict a reduction in the other expense line item (Payment Services segment) that resulted from

non-recurring expenses related to the purchase of the Diners Club Italy. In addition, the firm will also

benefit from non-recurring cost associated with the financial assistance provided to facilitate the

purchase of the Slovenian licensee by a European Bank.

Figures 20 & 21: Composition of 2015 operating expenses (left) and operating expenses vs YoY operating expense growth

In June 2015, DFS closed

the mortgage

origination business

acquired in 2012, which

was part of the Direct

Banking segment.

Source: Company Reports, IMCP

Source: Company Reports

10. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 9, 2016

10

In the first half of 2016, I anticipate stabilization in marketing, business development, and especially

professional fees expense related to AML/BSA look-back project coming to an end. In 2015 the effective

income tax rate declined 0.7%, which allowed the firm to save $28 million in income tax expense. This was

offset by a 36% increase in professional fees primarily driven by higher employee compensation cost.

Marketing and business development cost dropped 11% in 1Q16 due to timing of advertising campaigns.

However, I anticipate marketing cost to pick up in the second and third quarter, which explains the

increase in revenue for the third quarter of 2016. I anticipate other expense to fall due to non-recurring

expense from the prior year mortgage origination expense.

The firm will also benefit from not having as much expense related to employee’s benefits and

compensation. The sale of Diners Club Italy and the mortgage origination will allow the firm to focus more

on the core business, reduce the firm’s risk, and make more efficient decisions.

Figure 22: DFS operating margins, 2013 – 2017E

Return on Equity

Historically, DFS’ ROE has always been above the average of the industry ROE. The firm’s ROE was 170 bps

above the industry average for 2015, which shows that the firm is more efficient at generating earnings

than its peers. Although, the ROE has been going down over the past years as shown in the table, ROE has

declined due to the drop in margins and financial leverage; although asset turnover has been stable.

Figure 23: ROE breakdown, 2012 – 2017E

I expect ROE to continue to decrease for 2016 and 2017as the firm deleverages further. However, I expect

it to still remain above the industry average.

Source: Company Reports

Source: Company Reports

2013 2014 2015 2016E 2017E

Sales $7,064 $7,596 $7,945 $8,571 $9,326

Interest expense $1,146 $1,134 $1,263 $1,307 $1,327

Net interest income $5,918 $6,462 $6,682 $7,264 $7,999

Interest margin 83.78% 85.07% 84.10% 84.75% 85.77%

Operating expenses

Other $1,876 $2,607 $2,912 $3,365 $3,784

Growth 43.43% 38.97% 11.70% 15.54% 12.46%

EBT $4,042 $3,855 $3,770 $3,900 $4,215

EBT margin 57.22% 50.75% 47.45% 45.50% 45.20%

3-stage DuPont 2012 2013 2014 2015 2016E 2017E

Net income / sales 35% 35% 31% 29% 28% 28%

Sales / avg assets 0.09 0.09 0.09 0.09 0.10 0.10

ROA 3.2% 3.2% 2.9% 2.7% 2.7% 2.8%

Avg assets / avg equity 8.0 7.5 7.4 7.6 7.3 6.5

ROE 26% 24% 21% 21% 19% 18%

11. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 9, 2016

11

Free cash flow

DFS free cash flow to the firm has been negative on average over the past five years due a rising in NOWC

(due to loan growth). In 2015, FCFE was $2 billion primarily due to rising debt. The firm used part of this to

pay $515 million in dividends and buy back $7.9 million shares of stock. I expect FCFF to be positive as

NOPAT rises 3.4% in 2016 and 8.1% in 2017 to a 70 bps drop in the tax rate from 2014 to 2015, and as

growth in NOWC (loans) moderates.

Valuation

DFS was valued using multiples and a 3-stage discounting cash flow model. Based on earnings multiples,

the stock is cheap relative to other firms and is worth $47.93. Relative valuation shows DFS to be

undervalued based on its fundamentals versus those of its peers in the financial industry. Price to book

valuation yielded a price of $169.41. A detailed DCF analysis values DFS slightly lower, at $57.37; I give this

value a bit more weight because it incorporates assumptions that reflect DFS’s ongoing capital structural

and other changes. Finally, a probability-weighted scenario analysis yields a price of $60.27. As a result of

these valuations, I value the stock at $62.

Trading History

DFS is currently trading near its five year low P/E relative to the S&P 500. DFS’s current NTM P/E is at 9.40

compared to its five year average of 9.65. I expect DFS to be at least 9.40 at the end of the year.

Source: Factset

Figure 24: Free cash flows 2011 – 2017E

Free Cash Flow

2011 2012 2013 2014 2015 2016E 2017E

NOPAT $2,274 $2,539 $2,532 $2,424 $2,398 $2,480 $2,681

Growth 11.7% -0.3% -4.2% -1.1% 3.4% 8.1%

NOWC 36,780 40,028 42,207 44,967 47,615 49,443 51,389

Net fixed assets 926 1,010 1,123 1,103 1,116 1,143 1,211

Total net operating capital $37,706 $41,038 $43,330 $46,070 $48,731 $50,586 $52,600

Growth 8.8% 5.6% 6.3% 5.8% 3.8% 4.0%

- Change in NOWC 3,248 2,179 2,760 2,648 1,828 1,946

- Change in NFA 84 113 (20) 13 27 68

FCFF -$793 $240 -$316 -$263 $626 $667

Growth -130.2% -231.8% -16.6% -337.6% 6.5%

- After-tax interest expense - - - - - -

+ Net new short-term and long-term debt $1,676 $601 $12,328 $2,268 $17 $15

FCFE $883 $841 $12,012 $2,005 $643 $682

Growth -4.8% 1329.2% -83.3% -67.9% 6.0%

FCFF per share ($1.51) $0.48 ($0.67) ($0.59) $1.40 $1.49

Growth -131.9% -238.4% -11.7% -337.6% 6.5%

FCFE per share $1.68 $1.69 $25.39 $4.49 $1.44 $1.53

Growth 0.5% 1401.3% -82.3% -67.9% 6.0%

12. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 9, 2016

12

Assuming the firm maintains a 9.4 NTM P/E at the end of 2017, it should trade at $53.96 by the end of the

year.

Price = P/E x EPS = 9.4 x $5.74 = $53.96

Figure 25: DFS NTM P/E relative to S&P 500

Discounting $53.96 back to today at a 12.57% cost of equity (explained in Discounted Cash Flow section)

yields a price of $47.93. Given DFS’s potential for earnings growth and continued profitability, this seems

to be an unusually low valuation. However, this makes sense because I am less bullish about near-term

earnings than consensus.

Relative Valuation

DFS is currently trading at a P/E lower than most of its peers, with a P/E TTM of 10.5 compared to an

average of 12.8; although the median is 10.8. This discount could be from investors penalizing the firm for

write-offs last year associated with Diners Club Italy. P/B is above the median which may reflect the firm’s

above median ROE.

A more thorough analysis of P/B and ROE is shown in figure 31. The calculated R-squared of the

regression indicates that over 91% of a sampled firm’s P/B is explained by its 2015 ROE. DFS P/B is lower

than the industry average, according to this measure, it is slightly undervalued.

Estimated P/B = Estimated 2016 ROE (19.8%) x 26.714 + 1.2382 = 6.5

Target Price = Estimated P/B (6.5) x 2015E BVPS (29.34) = $190.71

Discounting back to the present at a 12.57% cost of equity leads to a target price of $169.41 using this

metric.

Source: Factset

13. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 9, 2016

13

Figure 27: P/B vs NTM ROE

For a final comparison, I created a composite ranking of several valuation and fundamental metrics. Since

the variables have different scales, each was converted to a percentile before calculating the composite

score. An equal weighting of LTD, Payout, 2015 ROE and NPM was compared to an equal weight

composite of NTM P/E. One can see that DFS is below the line, so it is inexpensive based on its

fundamentals.

Source: Factset

Source: Factset

Current Market Price Change Earnings Growth LT Debt/ S&P

Ticker Name Price Value 1 day 1 Mo 3 Mo 6 Mo 52 Wk YTD LTG NTM 2014 2015 2016 2017 Pst 5yr Beta Equity Rating Yield Payout

DFS DISCOVER FINANCIAL SVCS INC $54.83 $22,700 (0.6) 7.0 18.6 (3.7) (6.4) 2.3 6.5 11.6% -1.2% 4.7% 2.7% 8.7% 33.3% 1.41 210.1% A- 1.99% 21.5%

V VISA INC $77.36 $184,474 0.4 0.5 8.1 (2.4) 17.3 (0.2) 16.7 5.0% 13.7% 19.0% 12.5% 16.6% 21.0% 1.02 54.5% 0.67% 18.4%

ALLY ALLY FINANCIAL INC $16.97 $8,209 0.4 (3.0) (0.2) (14.7) (22.8) (9.0) 10.0 -172.9% -63.5% -157.5% -728.3% 16.6% 1.17 228.3% B+ 1.77% 23.2%

SYF SYNCHRONY FINANCIAL $29.83 $24,871 (1.4) 4.3 18.2 (8.5) (6.6) (1.9) 7.3 6.9% -5.0% 9.5% 16.6% 1.34 60.8% B+ 0.72% 21.1%

JPM JPMORGAN CHASE & CO $61.24 $223,934 (0.5) 4.9 6.0 (7.8) (4.9) (7.3) 5.7 0.1% 22.4% 8.5% -50.7% 16.6% 8.6% 1.24 103.9% B 2.21% 23.2%

BAC BANK OF AMERICA CORP $14.05 $144,893 (0.6) 6.5 8.5 (18.8) (14.1) (16.5) 10.0 15.6% -40.0% 241.0% 117.3% 16.6%

SLM SLM CORP $6.54 $2,799 (0.6) 3.0 6.5 (6.6) (36.6) 0.3 3.0 -16.7% -58.2% -69.1% 588.1% 16.6% -6.7%

AXP AMERICAN EXPRESS CO $63.92 $60,790 (0.5) 6.2 18.4 (13.5) (17.9) (8.1) 8.4 8.3% 27.0% 3.0% 0.4% 1.1% 8.5% 1.17 228.3% B+ 1.77% 23.2%

MA MASTERCARD INC $96.19 $105,647 (0.1) 2.0 16.2 (4.5) 6.0 (1.2) 16.0 10.3% 15.8% 10.9% 8.9% 16.9% 19.0% 1.34 60.8% B+ 0.72% 21.1%

COF CAPITAL ONE FINANCIAL CORP $69.12 $35,562 (0.8) 0.9 9.1 (13.1) (16.0) (4.2) 6.7 12.6% 5.5% -1.4% 4.9% 8.3% 3.3% 1.24 103.9% B 2.21% 23.2%

Average $81,388 (0.4) 3.2 10.9 (9.4) (10.2) (4.6) 9.0 -11.9% -8.7% 5.4% -3.5% 13.5% 12.4% 1.24 131.3% 1.51% 21.9%

Median $48,176 (0.6) 3.6 8.8 (8.2) (10.3) (3.1) 7.8 7.6% 5.5% 3.8% 6.9% 16.6% 8.6% 1.24 103.9% 1.77% 22.4%

SPX S&P 500 INDEX $2,051 0.0 0.3 9.1 (2.3) (1.9) 0.3 9.1% -4.4% 3.8% 13.6%

2015 P/E 2015 2015 EV/ P/CF P/CF Sales Growth Book

Ticker Website ROE P/B 2013 2014 2015 TTM NTM 2016 2017E NPM P/S OM ROIC EBIT Current5-yr NTM STM Pst 5yr Equity

DFS http://www.discoverfinancial.com 19.8% 2.11 11.0 11.2 10.7 10.5 9.4 11.6 11.2 25.9% 2.76 37.5% 7.2% 6.3 6.4 -10.2% 3.4% 3.8% $25.97

V http://usa.visa.com 21.0% 6.33 40.7 35.8 30.1 27.4 26.1 26.8 23.0 44.2% 13.29 65.7% 22.1% 21.7 7.6% 15.0% 11.5% $12.22

ALLY http://www.ally.com -1.7% 0.63 7.7 21.2 -36.9 -5.3 7.2 5.9 5.0 -2.2% 0.81 16.5% 1.2% 1.8 -9.2% -0.4% -10.0% $27.15

SYF http://www.synchronyfinancial.com 16.7% 2.09 10.7 11.3 11.1 10.4 10.3 8.9 20.2% 2.29 31.8% 6.0% 5.3 4.8 8.7% 11.5% $15.84

JPM http://www.jpmorganchase.com 9.6% 1.00 13.9 11.3 10.5 10.4 10.4 21.2 18.2 42.0% 4.39 31.2% 4.8% 7.9 0.6% 6.7% -2.0% $61.28

BAC http://www.bankofamerica.com 5.8% 0.61 21.6 36.0 10.6 11.2 9.7 4.9 4.2 27.5% 2.91 23.7% 3.4% 5.7 8.1 -6.0% $23.12

SLM http://www.salliemae.com 11.4% 1.77 2.0 4.8 15.6 10.4 12.5 2.3 1.9 17.8% 2.78 43.4% 12.2% 4.3 -30.0% $3.69

AXP http://www.americanexpress.com 25.4% 3.21 15.1 11.9 11.6 12.8 11.8 11.5 11.4 15.3% 1.77 23.7% 8.0% 7.3 9.3 -9.2% -0.4% 2.6% $21.79

MA http://www.mastercard.com 65.4% 17.47 38.0 32.8 29.6 29.0 26.3 27.2 23.2 36.9% 10.93 52.4% 43.3% 21.1 8.7% 11.5% 11.8% $4.97

COF http://www.capitalone.com 7.8% 0.75 10.0 9.5 9.6 10.0 8.9 9.1 8.4 18.1% 1.74 23.3% 4.6% 3.8 4.0 0.6% 6.7% 5.5% $92.73

Average 18.1% 3.60 17.8 18.5 10.3 12.8 13.3 13.1 11.5 24.6% 4.37 34.9% 11.3% 16.1 5.0 6.7 -0.3% 6.7% -1.4%

Median 14.0% 1.93 13.9 11.6 11.0 10.8 10.4 10.9 10.0 23.1% 2.77 31.5% 6.6% 21.1 5.2 7.2 0.6% 6.7% 2.6%

LTM Dividend

Figure 26: DFS comparable companies

14. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 9, 2016

14

Figure 28: Composite valuation, % of range

Figure 29: Composite relative valuation

Discounted Cash Flow Analysis

A three stage discounted cash flow model was also used to value DFS.

For the purpose of this analysis, the company’s cost of equity was calculated to be 12.57% using the

Capital Asset Pricing Model.

Source: Factset

Source: Factset

Valuation

Weight 15.0% 40.0% 30.0% 15.0% 100.0%

1/(LTD/ 1/ 2015 2015 P/E

Ticker Name Equity) Payout ROE NPM NTM

DFS DISCOVER FINANCIAL SVCS INC 26% 86% 30% 59% 36%

V VISA INC 100% 100% 32% 100% 99%

ALLY ALLY FINANCIAL INC 24% 79% 39% 35% 45%

SYF SYNCHRONY FINANCIAL 90% 87% 100% 84% 100%

JPM JPMORGAN CHASE & CO 52% 79% 12% 41% 34%

BAC BANK OF AMERICA CORP 62% 90% 49% 47% 64%

SLM SLM CORP 62% 90% 28% 56% 51%

AXP AMERICAN EXPRESS CO 24% 79% 21% 52% 40%

MA MASTERCARD INC 90% 87% 49% 47% 64%

COF CAPITAL ONE FINANCIAL CORP 52% 79% 49% 47% 64%

Fundamentals

15. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 9, 2016

15

The underlying assumptions used in calculating this rate are as follows:

The risk free rate of the ten year Treasury bond yield of 1.88%.

A ten year beta of 1.38 was used since the firm has higher risk than the market.

A long term market rate of return of 10% was presumed, since historically, the market has generated

an annual return of about 10%.

Given the above assumptions, the cost of equity is 12.57% (1.88 + 1.38 (10.0 – 1.88)).

Stage One - The model’s first stage simply discounts fiscal years 2016 and 2017 free cash flow to equity

(FCFE). These per share cash flows are forecasted to be $1.44 and $1.53, respectively. Discounting these

cash flows, using the cost of equity calculated above, results in a value of $2.46 per share. Thus, stage one

of this discounted cash flow analysis contributes $2.46 to value.

Stage Two - Stage two of the model focuses on fiscal years 2017 to 2022. During this period, FCFE is

calculated based on revenue growth, NOPAT margin and capital growth assumptions. The resulting cash

flows are then discounted using the company’s 12.57% cost of equity. I assume 6.2% sales growth in 2018,

staying constant through 2022. The NWC and NFA turnover ratios are expected to remain at 2017 levels.

Also, the NOPAT margin is expected to rise to 29.6% in 2022 from 28.7% in 2017.

Figure 30: FCFE and discounted FCFE, 2015 – 2021

Stage Three – Net income for the years 2018 – 2022 is calculated based upon the same margin and

growth assumptions used to determine FCFE in stage two. EPS is expected to grow from $5.28 in 2016 to

$7.67 in 2022.

Figure 31: EPS estimates for 2015 – 2021

Stage three of the model requires an assumption regarding the company’s terminal price-to-earnings

ratio. By 2022 the firm will have matured. Given its current P/E of 10.5 it may not make much sense to use

a higher multiple. However, by 2022 the stigma of being a financial stock may diminish. Thus, I am using a

12 P/E, which is still a discount to the market.

Given the assumed terminal earnings per share of $7.67 and a price to earnings ratio of 12, a terminal

value of $100.13 per share is calculated. Using the 12.57% cost of equity, this number is discounted back

to a present value of $42.46.

Total Present Value – given the above assumptions and utilizing a three stage discounted cash flow model,

an intrinsic value of $57.37 is calculated (2.47 + 12.45 + 42.46). Given DFS’s current price of $55.23, this

model indicates that the stock is slightly undervalued.

Scenario Analysis

Discover Financial Services is difficult to value with certainty because it is really difficult to know what the

Federal Reserve will do with interest rates and how the overall economy will react if interest rates rise or

fall. Also, regulations can have a negative impact on the firm profitability due to large increases in

overhead cost. I valued DFS using the above DCF analysis combinations of three key factors. The resulting

value is $60.27.

2016 2017 2018 2019 2020 2021 2022

EPS $5.28 $5.74 $6.29 $6.61 $6.96 $7.31 $7.67

2016 2017 2018 2019 2020 2021 2022

FCFE $1.44 $1.53 $4.50 $4.74 $5.01 $5.26 $5.53

Discounted FCFE $1.27 $1.19 $3.12 $2.90 $2.71 $2.52 $2.34

DFS is the only credit cards

company that has all of its

call centers based in

United States. This allow

the firm to provide

excellent customer service

to its clients

Increasing the private

student loan receivable

will potentially increase

credit card loan

receivable. Given, that

they are very likely to

become credit cardholder

16. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 9, 2016

16

Sales Growth – High growth presumes that DFS will use its strong marketing strategy to attract and retain

new customers by continuing to offer cash back and rewards, charging low interest, and continuing to

provide excellent customer service. DFS also has to maintain its focus on the core business (Direct

Banking) in order to maximize interest income and manage core expenses more efficiently. I give this

outcome a 30% probability because the company has historically increased his sales in the past 5 years.

Also, the firm recently paid off his short –term debt and sold two divisions that were impacted profits

negatively. Moderate growth is the base assumption used in the prior DCF analysis, and is given a 40%

probability. Poor growth assumes that many of DFS’s most loyal customers do not care about cash back

and low interest rates, and the firm is unable to attract enough new customers to grow revenues strongly.

Under this scenario, revenue in 2022 is still below 2015 levels; I give this outcome a 30% probability

because of the uncertainty surrounding Fed Reserve policy.

Net Interest Margin – Scenario one, moderate margin, supposed that DFS focus on non-wealthy

customers such as students in order to increase the credit card and private student loan receivable. Doing

this, along with managing core expenses more effectively will lead to an increase in net interest margin.

Operating Efficiency – Recently, management has focused on managing costs more effectively, eliminating

waste and streamlining operations. Current management is clearly focused on cost reduction, and has

already begun to succeed in this regard. Therefore, I assign a 40% probability for significant reductions in

both core and other expenses.

Figure 32: Scenario analysis

Sales Net Interest Margin Cost Savings DCF Value Probability Weighted Value

Moderate (p=0.7) $69.70 18.20% $12.69

Stable (p=0.3) 66.48 7.80% 5.19

Moderate (p=0.7) 68.09 27.30% 18.59

Stable (p=0.3) 64.87 11.70% 7.59

Moderate (p=0.7) 47.54 8.40% 3.99

Stable (p=0.3) 46.20 3.60% 1.66

Moderate (p=0.7) 46.87 12.60% 5.91

Stable (p=0.3) 45.53 5.40% 2.46

Moderate (p=0.7) 44.65 1.40% 0.63

Stable (p=0.3) 43.55 0.60% 0.26

Moderate (p=0.7) 44.10 2.10% 0.93

Stable (p=0.3) 43.00 0.90% 0.39

Weak

Growth

(p=0.3)

Significant

(p=0.4)

Moderate

(p=0.6)

Total of Weighted Values: $60.27

High

Growth

(p=0.3)

Moderate

(p=0.4)

Weak

(p=0.6)

Moderate

Growth

(p=0.4)

Significant

(p=0.4)

Moderate

(p=0.6)

17. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 9, 2016

17

Business Risks

Current economic and regulatory environment

As many other financial institutions, DFS is highly correlated to the United States and global economies.

When the economy is doing well, DFS experiences low charge-off and delinquency rates, increases in loan

growth and earnings. However, during a slow economy, charge –off and delinquency rates increase due to

high unemployment rate. Regulations also can have a negative impact on the company’s earnings. After

the 2008 crisis, expenses rose significantly due compliance cost and professional fees.

Interest rate

Interest rates are a crucial factor when it comes to DFS well-being. A good portion of its portfolio is issued

at a fixed rate, in order to attract customers and stay competitive. If borrowing rates increase the

company could experience a setback if rates on loans do not rise as well.

Mortgage Market

DFS has a significant exposure to the mortgage market through the Direct Banking segment. If the

mortgage market were to collapse, DFS would experience a significant loss in interest income and from

charge-offs.

20. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 9, 2016

20

Appendix 3: Ratios

Ratios (in millions)

Items 2011 2012 2013 2014 2015 2016E 2017E

Profitability

Gross margin 77% 80% 84% 85% 84% 85% 86%

Operating (EBIT) margin 57% 61% 57% 51% 47% 46% 45%

Net profit margin 35% 35% 35% 31% 29% 28% 28%

Activity

NFA (gross) turnover 6.92 6.62 6.82 7.16 7.59 7.92

Total asset turnover 0.09 0.09 0.09 0.09 0.10 0.10

Liquidity

Op asset / op liab 2.24 2.21 2.21 2.26 2.28 2.29 2.31

NOWC Percent of sales 573% 582% 574% 583% 566% 541%

Solvency

Debt to assets 27% 27% 26% 40% 41% 39% 38%

Debt to equity 222% 205% 191% 296% 312% 269% 233%

Other liab to assets 19% 16% 17% 4% 4% 4% 4%

Total debt to assets 45% 43% 43% 44% 44% 43% 41%

Total liabilities to assets 88% 87% 86% 87% 87% 85% 84%

Debt to EBIT 5.11 4.92 5.10 8.55 9.34 9.03 8.36

Debt to total net op capital 0.49 0.49 0.48 0.72 0.72 0.70 0.67

ROIC

NOPAT to sales 38% 36% 32% 30% 29% 29%

Sales to IC 17% 17% 17% 17% 17% 18%

Total 6% 6% 5% 5% 5% 5%

Total using EOY IC 6% 6% 6% 5% 5% 5% 5%

ROE

3-stage

Net income / sales 35% 35% 31% 29% 28% 28%

Sales / avg assets 0.09 0.09 0.09 0.09 0.10 0.10

ROA 3.2% 3.2% 2.9% 2.7% 2.7% 2.8%

Avg assets / avg equity 801% 751% 740% 759% 726% 649%

ROE 26% 24% 21% 21% 19% 18%

Payout Ratio 9% 12% 19% 21% 22% 22%

Retention Ratio 91.1% 87.9% 81.3% 79.0% 77.9% 77.9%

Sustainable Growth Rate 23.7% 21.1% 17.2% 16.2% 15.1% 14.2%

21. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 9, 2016

21

Appendix 4: Cash Flow Statement

Cash Flow Statement

Items 2012 2013 2014 2015 2016E 2017E

Cash from Operatings (understated - depr'n added to net assets)

Net income $2,345 $2,470 $2,323 $2,297 $2,358 $2,566

Change in Net Working Capital ex cash (2172) 449 (2030) (360) (2835) (2732)

Cash from operations $173 $2,919 $293 $1,937 ($476) ($166)

Cash from Investing (understated - depr'n added to net assets)

Change in NFA ($84) ($113) $20 ($13) ($27) ($68)

Change in Marketable Securities $665 ($179) ($23) $155 $0 $0

Cash from investing $581 ($292) ($3) $142 ($27) ($68)

Cash from Financing

Change in Short-Term and Long-Term Debt $1,676 $601 $12,328 $2,268 $17 $15

Change in Other liabilities (545) 839 (9890) 97 0 0

Change in Debt/Equity-Like Securities 0 0 0 0 0 0

Dividends (210) (298) (435) (483) (521) (567)

Change in Equity ex NI and Dividends (599) (1141) (1563) (1673) 0 0

Cash from financing $322 $1 $440 $209 ($504) ($552)

Change in Cash 1076 2628 730 2288 (1007) (786)

Beginning Cash 2850 3926 6554 7284 9572 8565

Ending Cash $3,926 $6,554 $7,284 $9,572 $8,565 $7,779

22. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 9, 2016

22

Appendix 5: 3-stage DCF Model

First Stage Second Stage

Cash flows 2016 2017 2018 2019 2020 2021 2022

Sales Growth 7.9% 8.8% 6.2% 6.2% 6.2% 6.2% 6.2%

NOPAT / S 28.9% 28.7% 28.80% 29.00% 29.20% 29.40% 29.60%

S / NWC or S / NOWC 0.17 0.18 0.18 0.18 0.18 0.18 0.18

S / NFA (EOY) 7.50 7.70 7.70 7.70 7.70 7.70 7.70

S / IC (EOY) 0.17 0.18 0.18 0.18 0.18 0.18 0.18

ROIC (EOY) 4.9% 5.1% 5.1% 5.1% 5.2% 5.2% 5.2%

ROIC (BOY) 5.3% 5.4% 5.5% 5.5% 5.5% 5.6%

Share Growth 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Sales $8,571 $9,326 $9,904 $10,518 $11,170 $11,862 $12,598

NOPAT $2,480 $2,681 $2,852 $3,050 $3,262 $3,488 $3,729

Growth 8.1% 6.4% 6.9% 6.9% 6.9% 6.9%

- Change in NWC or NOWC 1828 1946 3186 3384 3593 3816 4053

NWC or NOWC EOY 49443 51389 54575 57959 61552 65368 69421

Growth NWC or NOWC 3.9% 6.2% 6.2% 6.2% 6.2% 6.2%

- Chg NFA 27 68 75 80 85 90 96

NFA EOY 1,143 1,211 1,286 1,366 1,451 1,541 1,636

Growth NFA 6.0% 6.2% 6.2% 6.2% 6.2% 6.2%

Total inv in op cap 1855 2014 3261 3463 3678 3906 4148

Total net op cap 50586 52600 55861 59325 63003 66909 71057

FCFF $626 $667 ($409) ($413) ($417) ($419) ($419)

% of sales 7.3% 7.1% -4.1% -3.9% -3.7% -3.5% -3.3%

Growth 6.5% -161.4% 1.1% 0.8% 0.5% 0.2%

+ Net new debt 17 15 2185 2320 2464 2617 2779

Debt 35227 35242 37427 39747 42212 44829 47608

Debt / tot net op capital 69.6% 67.0% 67.0% 67.0% 67.0% 67.0% 67.0%

FCFE w or w/o debt $643 $682 $1,776 $1,907 $2,048 $2,199 $2,360

% of sales 7.5% 7.3% 17.9% 18.1% 18.3% 18.5% 18.7%

Growth 6.0% 160.6% 7.4% 7.4% 7.4% 7.3%

/ No Shares 446.9 446.9 446.9 446.9 446.9 446.9 446.9

FCFE $1.44 $1.53 $3.97 $4.27 $4.58 $4.92 $5.28

Growth 6.0% 160.6% 7.4% 7.4% 7.4% 7.3%

* Discount factor 0.88 0.78 0.69 0.61 0.54 0.48 0.42

Discounted FCFE $1.27 $1.19 $2.75 $2.61 $2.48 $2.36 $2.24

Terminal value P/E

Net income $2,358 $2,566 $2,852 $3,050 $3,262 $3,488 $3,729

% of sales 27.5% 27.5% 28.8% 29.0% 29.2% 29.4% 29.6%

EPS $5.28 $5.74 $6.38 $6.83 $7.30 $7.80 $8.34

Growth 8.8% 11.2% 6.9% 6.9% 6.9% 6.9%

Terminal P/E 12.00

* Terminal EPS $8.34

Terminal value $100.13

* Discount factor 0.42

Discounted terminal value $42.46

Summary

First stage $2.47 Present value of first 2 year cash flow

Second stage $12.45 Present value of year 3-7 cash flow

Third stage $42.46 Present value of terminal value P/E

Value (P/E) $57.37 = value at beg of fiscal yr 2016

23. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 9, 2016

23

Appendix 6: Porter’s 5 Forces

Threat of New Entrants – Relatively Low

Despite regulations and the extensive capital required to enter the consumer financial services industry, a significant number

of new banks and credit card companies opened in the last decade. However, due to the level of risk and trust involved in this

industry, most of the new entrants either failed or merged with other firms. For these reasons, it is very difficult to enter the

financial industry and the threat of new entrants is very low.

Threat of Substitutes – High

DFS relies on its power to charge low interest rate on loans and to offer an attractive cash back and rewards program to its

clients. DFS would find it very difficult to either attract or retain new customers. This is true if stronger competitors decide to

make their rewards packages more attractive.

Supplier Power - Very high

One of DFS most important “fund suppliers” is its direct deposit customers. DFS has to offer a better yield than its

competitors in order to retain clients’ deposits. Therefore, supplier power is very high.

Buyer Power –High

Consumers of credit cards have a great degree of power over banks. There is no cost of switching between banks or other

credit card companies. Besides building or improving credit history; there are few benefits for consumers to not pay-off the

due amount before it starts accumulating interest.

Intensity of Competition – Very High

There are several national and international credit card companies. As the online market expands, DFS’s traditional

opponents are fighting even harder to obtain market share. Aggressive cash back offers and low to zero APR for an extended

amount of time generally force others to do the same, which hurts interest margins for all participants.

Appendix 6: SWOT Analysis

Strengths Weaknesses

High interest margin No prepaid cards

Low charge-off rate No wealthy customers

Prime cash-back and rewards program No international exposure

Opportunities Threats

International expansion Interest rate increase

Prepaid cards offer High unemployment

National expansion New regulations