Recommended

Recommended

More Related Content

More from celenarouzie

More from celenarouzie (20)

W3 CodingNameInstructions Underline the main term in .docx

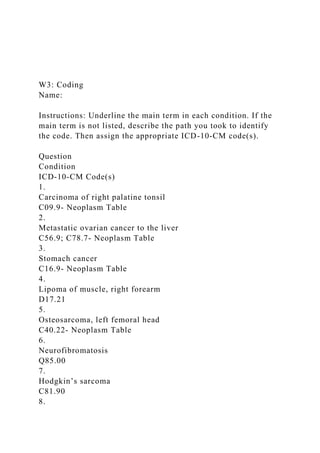

- 1. W3: Coding Name: Instructions: Underline the main term in each condition. If the main term is not listed, describe the path you took to identify the code. Then assign the appropriate ICD-10-CM code(s). Question Condition ICD-10-CM Code(s) 1. Carcinoma of right palatine tonsil C09.9- Neoplasm Table 2. Metastatic ovarian cancer to the liver C56.9; C78.7- Neoplasm Table 3. Stomach cancer C16.9- Neoplasm Table 4. Lipoma of muscle, right forearm D17.21 5. Osteosarcoma, left femoral head C40.22- Neoplasm Table 6. Neurofibromatosis Q85.00 7. Hodgkin’s sarcoma C81.90 8.

- 2. Chronic lymphocytic leukemia of B-cell type C91.10 9. Reticulosarcoma of intrathoracic lymph nodes C83.32 10. Adenocarcinoma of rectum and anus C21.8- Neoplasm Table 11. Allergic reaction to Benadryl T45.0x5A 12. Accidental food poisoning from lobster (food, shellfish) T61.78A 13. Accidentalpoisoning from ingesting toilet deodorizer T65.891A 14. Adverse effect of acetaminophen T39.1x5A 15. Suicide attempt, Ambien T42.6x2A 16. Accidental overdose of Prednisone T38.0x1A 17. Rash due to therapeutic use of penicillin T36.0X5A; L27.0 18. Underdosing of Synthroid in patient with enlarged thyroid T36.4X6D 19. Dizziness due to accidental overdose of Valerian tincture T42.6x1A; R42 20.

- 3. Suicide attempt due to carbon monoxide poisoning T58.92xA Copyright©2012. Cengage Learning. All Rights Reserved.Page 1 of 2 Accounting/Accounting/Assessment 10/Assessment 10.docx · Write a 3- to 5-page essay about the ethical and financial implications of insider trading. Note: Some of the assessments in this course build upon each other, so you are strongly encouraged to complete them in the order in which they are presented. Show More Investors depend on the information from financial statements in making investment decisions. However, if a company's financial information is used or shared before it is released to the public, this could cause substantial movement in the price of a company's stock. Some individuals do not see anything unethical about insider trading, yet it is a criminal offense, one for which even well-known and respected individuals have served, and are serving, time in prison. CPAs agree to a professional code of conduct upon licensure, but it is important to develop your own conclusions regarding the ethical implications of financial reporting, planning, and decision making within an organization. By successfully completing this assessment, you will demonstrate your proficiency in the following course competencies and assessment criteria: · Competency 2: Examine regulatory, ethical, and credibility issues in accounting

- 4. 1. Analyze how insider trading may affect general business management planning and decision making. 1. Analyze the ethical implications related to financial decisions concerning inside information. . Competency 5: Communicate in a manner that is professional and consistent with expectations for members of the business professions. 2. Communicate in a manner that is professional and consistent with expectations for members of the business professions. Competency Map Check Your ProgressUse this online tool to track your performance and progress through your course. · Toggle Drawer Resources Suggested Resources The following optional resources are provided to support you in completing the assessment or to provide a helpful context. For additional resources, refer to the Research Resources and Supplemental Resources in the left navigation menu of your courseroom. Library Resources The following e-books or articles from the Capella University Library are linked directly in this course: . Murthy, G. (2009). Financial accounting. Mumbai, India: Himalaya Publishing House. . Vataliya, K. S. (2009). Practical financial accounting: Advance methods, techniques and practices. Jaipur, India: Paradise Publishers. . Doran, D. T. (2012). Financial reporting standards: A decision-making perspective for non-accountants. New York, NY: Business Experts Press. Show More Course Library Guide A Capella University library guide has been created specifically for your use in this course. You are encouraged to refer to the resources in the MBA-FP6014 – Financial Accounting Library

- 5. Guide to help direct your research. Bookstore Resources The resources listed below are relevant to the topics and assessments in this course. These resources are available from the Capella University Bookstore. When searching the bookstore, be sure to look for the Course ID with the specific – FP (FlexPath) course designation. . Libby, R., Libby, P., & Hodge, F. (2017). Financial accounting (9th ed.). New York, NY: Irwin. · Assessment Instructions Based on your own experience and knowledge with financial reporting, planning, and decision making, develop conclusions and explain the ethical implications of financial decisions within an organization. You may need to do additional research on the implications of using insider information (for example, the case of Martha Stewart) to help you complete this assessment. Write an essay in which you respond to the following: . Why is insider trading considered unethical? Keep in mind that some individuals do not see anything unethical about it, even though it is a criminal offense. . Would allowing insider trading, even if it were ethical, hinder the operation of the stock market in raising capital for new and existing companies? Explain. You must use two or more scholarly sources in your essay to support your responses. Additional Requirements . Length: Your essay should be 3–5 typed, double-spaced pages, including a title page and references. . Written communication: Written communication should be free of errors that detract from the overall message. . Style and formatting: Use current APA style to format your essay and cite your references. You must use at least two references in your essay. . Font and font size: Times New Roman, 12 point. Ethical Issues: Ethics and Insider Trading Scoring Guide

- 6. View Scoring GuideUse the scoring guide to enhance your learning.How to use the scoring guide · [u10a1] Ethical Issues: Ethics and Insider Trading Write a 3- to 5-page essay about the ethical and financial implications of insider trading. · Assessment Submit Submit Assessment This button will take you to the next available assessment attempt tab, where you will be able to submit your assessment. · u10a1 Ethical Issues >> View/Complete · u10a1 Ethical Issues: Revision 1 >> View/Complete · u10a1 Ethical Issues: Revision 2 >> View/Complete Accounting/Accounting/Assessment 2/Assessment 2.docx Assessment 2 · For this assessment, complete the problem below. You may use Word or Excel to complete the assessments throughout this course, but you will find Excel to be most helpful for creating spreadsheets. Tutorials for using Excel are provided in the Supplemental Resources in the left navigation menu. If you use Excel, submit the assessment in one Excel document, using separate tabs for each spreadsheet. To complete this assessment, you may choose to use the Assessment 2 Problem Template linked in the Suggested

- 7. Resources under the Capella Resources heading. Transactions Audrey Jhingree opened an ice cream parlor in a university town. The parlor specializes in ice cream combinations named after popular professors in the business department of the university. You have been hired as a manager. Your duties include maintaining the store's financial records. The following transactions occurred in April 2012, the first month of operations: · a. Received cash of $40,000 total ($10,000 each) from four investors. Each investor received 100 shares of common stock. This took place on April 1. · b. Paid three months' rent for the store on April 1 at $2,000 per month (recorded as prepaid expenses). · c. Purchased ice cream and cones for $6,000 on account payable, due in 60 days. This took place on April 2. · d. Purchased supplies for $1,000 cash on April 2. · e. Received a two-year $11,000 loan at the bank. The note payable is dated April 2. · f. Used the money from (e) to purchase a computer for $3,000 (for record keeping and inventory tracking) and to purchase $8,000 of used furniture and fixtures for the store. · g. Placed a grand opening advertisement in the local paper for $600 cash. · h. Made sales in the first half of the month totaling $5,000: $4,250 was in cash and the rest was on accounts receivable. The cost of the ice cream sold was $2,000. · i. Made a $600 payment on accounts payable on April 18. · j. Incurred and paid employee wages of $2000 for the month of April. · k. Collected accounts receivable of $700 from customers. · l. Made a repair to one of the refrigerators for $300. · m. Made sales in the last half of the month for $6,000, all for cash. The cost of the ice cream sold was $2,400. Recording Transactions, Posting to T-Accounts, Preparing Financial Statements, and Commenting on What Financial

- 8. Statements Tell Potential Investors Using the information provided above, complete the following for Audrey Jhingree's ice cream parlor. To complete this problem, you may choose to use the Assessment 2 Problem Template, which is linked in the Suggested Resources under the Capella Resources heading. 1. Set up appropriate T-accounts for cash, accounts receivable, supplies, inventory, prepaid expenses, equipment, furniture and fixtures, accounts payable, notes payable, contributed capital, sales revenue, cost of goods sold (expense), advertising expense, wage expense, and repair expense. All accounts begin with zero balances. 1. Record in the T-accounts the effects of each transaction for Audrey's shop in April, referencing each transaction in the accounts with the transaction letter. Show the ending balances in the T-accounts. Note that transactions (h) and (m) require two types of entries, one for sales and one for cost of goods sold. Prepare trial balances for 4/30/12. 1. Prepare financial statements at the end of the month ended April 30, 2012. Hint: Do the income statement first, followed by the statement of stockholders' equity, and then the balance sheet. Properly label each statement: Does it cover a period of time or just a point in time? 1. Write a short memo to Audrey offering your opinion on the results of operations during the first month of business. 1. After three years in business, you are being evaluated for a promotion. One measure is how efficiently you have managed the assets of the business. Using the data in the following table, compute the total asset turnover ratio for 2014 and 2013 and evaluate the results. Also compute the return on invested capital (net income divided by total stockholders' equity). Do you think you should be promoted? Why or why not? Audrey's Ice Cream Parlor: Financial Data Account 2014 2013

- 9. 2012 Total assets $93,000 $78,000 $61,000 Total liabilities $23,000 $23,000 $16,500 Total contributed capital plus retained earnings $70,000 $55,000 $44,500 Total sales $100,000 $82,500 $57,250 Net income $15,000 $10,500 $4,500 Accounting/Accounting/Assessment 2/assessment_2_problem_template.xls T-Accounts SetupWorksheet 1 of 6. Template for requirement 1: Set up appropriate T-accounts for cash, accounts receivable, supplies, inventory, prepaid expenses, equipment, furniture and fixtures, accounts payable, notes payable, contributed capital, sales revenue, cost of goods sold (expense), advertising expense, wage expense, and repair expense. All accounts begin with zero balances.Learner:Audrey's Ice Cream ParlorCashAccounts ReceivableSuppliesPrepaid ExpensesEquipment- 0- 0- 0InventoryAccounts PayableNotes Payable- 0- 0- 0- 0Furniture & FixturesSales RevenueCost of Goods Sold- 0- 0Advertising ExpenseWage ExpenseRepair

- 10. ExpenseContribution CapitalEnd of worksheet T-AccountsWorksheet 2 of 6. Template for requirement 2: Using columns A through N, record in the T-accounts the effects of each transaction for Audrey's shop in April, referencing each transaction in the accounts with the transaction letter. Show the ending balances in the T-accounts. Note that transactions (h) and (m) require two types of entries, one for sales and one for cost of goods sold. In columns P through S, prepare trial balances for 4/30/12.Learner:Audrey's Ice Cream ParlorAudrey's Ice Cream ParlorTrial Balance30-Apr- 12CashAccounts ReceivableSuppliesDebitCredit(a)(b)(h)(k)(d)Cash(e)(d)Accoun ts Receivable(h)(f )- 0Supplies(k)(g)Inventory(m)(i)Prepaid Expenses(j)Equipment(l)Prepaid ExpensesEquipmentFurniture and Fixtures- 0- 0(b)(f)Accounts Payable- 0Notes PayableCommon StockSalesInventoryAccounts PayableNotes PayableCost of Goods Sold( c )(h)(i)(c )(e)Advertising(m)Wages- 0- 0- 0Repairs- 0Totals- 0=- 0Furniture & FixturesSales RevenueCost of Goods Sold(f)(h)(h)(m)(m)- 0- 0Advertising ExpenseWage ExpenseRepair Expense(g)(j)(l)Contribution Capital(a)End of worksheet Income StatementWorksheet 3 of 6. Template for requirement 3: Prepare the income statement at the end of the month ended April 30, 2012.Learner:Audrey's Ice Cream ParlorIncome StatementFor the Month Ended April 30, 2012SalesLess: Cost of Goods SoldGross Profit- 0Less: ExpensesAdvertisingWagesRepairs- 0Net Income$ - 00.00%End of worksheet Stockholders' EquityWorksheet 4 of 6. Template for requirement 3: Prepare the statement of stockholders' equity at the end of the month ended April 30, 2012.Learner:Audrey's Ice Cream ParlorStatement of Stockholders' EquityFor the Month Ended April 30, 2012Contributed Capital:Balance, April 01- 0Add: Issue of Common StockTotal Contributed Capital$ - 0Retained Earnings:Balance, April 01Add: Net

- 11. Income0.00%Retained Earnings, April 30$ - 0Total Shareholders' Equity$ - 0End of worksheet Balance SheetWorksheet 5 of 6. Template for requirement 3: Prepare the balance sheet at the end of the month ended April 30, 2012.Learner:Audrey's Ice Cream ParlorBalance SheetApril 30, 2012AssetsLiabilitiesCashAccounts PayableTotal Current Liabliites- 0Accounts ReceivableNotes PayableTotal Long-Term liabliites- 0SuppliesTotal Liabilities- 0InventoryPrepaid ExpensesTotal Current Assets- 0Stockholders' EquityEquipmentShareholders' EquityFurniture and FixturesTotal Equipment, Furniture and Fixtures- 0Total Assets$ - 0Total Liabilities and Owner's Equity$ - 0Current Ratio =0.00%End of worksheet Req 4 & 5Worksheet 6 of 6. Template for requirements 4 and 5: Write a short memo to Audrey offering your opinion on the results of operations during the first month of business. Then, using the financial data from the assessment, compute the total asset turnover ratio for 2014 and 2013 and evaluate the results. Also compute the return on invested capital (net income divided by total stockholders' equity). Evaluate whether you should be promoted based on how efficiently you have managed the assets of the business.Learner:(4) Memo to Audrey on the results of operations during the first month of business.Audrey's Ice Cream ParlorAccount201420132012Total assets$93,000$78,000$61,000Total liabilities$23,000$23,000$16,500Total contributed capital plus retained earnings$70,000$55,000$44,500Total sales$100,000$82,500$57,250(5) Compute the total asset turnover ratio and the return on invested capital and evaluate the results. Based on this measure, do you think you should be promoted? Why or why not?Net income$15,000$10,500$4,50020142013Average Assets8550069500Average Capital6250049750 Accounting/Accounting/Assessment 3/cf_assessment_3_problem_1_template.xls

- 12. Journal EntriesTemplate for adjusting entries in a journal: Column A is the letter (a through h) for the transaction, column B is for the type of adjustment, column B is for debits (DR), and column D is for credits (CR).Learner:Huntington CompanyAdjusting Entries31-Dec-11DRCRa.Unearned Rent RevenueRent Revenue(4 months of 6 months of $9,000)b.Interest ExpenseInterest Payable($30,000 × .12 × 3/12)c.Depreciation ExpenseAccumulated Depreciation - Truck(amount of $5,000 is given)d.Unearned Service RevenueService Revenue($4,800/12 × 2 months)e.Insurance ExpensePrepaid Insurance($12,000/12 × 2 months)f.Accrued Service RevenueService Revenues(amount of $6,000 is given)g.Wages ExpenseAccrued Wages Payable(amount of $17,500 is given)h.Property Tax ExpenseAccrued Taxes Payable(amount of $16,000 is given)End of worksheet Accounting/Accounting/Assessment 3/cf_assessment_3_problem_2_template.xls Effects of AdjustingTemplate for indicating the effect of each adjusting entry (a through h from Problem 1) on the balance sheet and income statement. Compute the assets, liabilities, stockholders' equity, revenues, expenses, and net income for all transactions. Huntington Company, year ended December 31, 2012.Learner:TRANSACTIONBALANCE SHEETINCOME STATEMENTAssetsLiabilitiesStockholders' EquityRevenuesExpensesNet IncomeaNENEbNENE900cNEdNE-800800800NE800e-2,000NE- 2,000NE2,000-2,000fgNENE-17,500hNE16,000NE- 16,000CRCRDRCRDRDR-2,00015,200-1,2008002,900- 34,700Change in Assets & Liabilities17,200Revenue − Expense =-2,100Change In:DRCRAssetsLiabilitiesEquity28,600Must Equal28,600-End of worksheet Accounting/Accounting/Assessment 3/Note.docx Assessment 3 · Note: Some of the assessments in this course build upon each

- 13. other, so you are strongly encouraged to complete them in the order in which they are presented. For this assessment, complete Problems 1 and 2. You may use Word or Excel to complete the assessments throughout this course, but you will find Excel to be most helpful for creating spreadsheets. Tutorials for using Excel are provided in the Supplemental Resources in the left navigation menu. If you use Excel, submit the assessment in one Excel document, using separate tabs for each spreadsheet. Templates for both problems are linked in the Suggested Resources under the Capella Resources heading. Problem 1: Adjusting the Books Using Adjusting Entries Huntington Company's annual accounting year ends on December 31. It is December 31, 2012, and all of the 2012 entries except the following adjusting entries have been made: · a. On September 1, 2012, Huntington collected six months of rent worth $9,000 on storage space. At that date, cash was debited and unearned rent revenue was credited for $9,000. · b. On October 1, 2012, the company borrowed $30,000 from a local bank and signed a 12 percent note for that amount. The principal and interest are payable on the maturity date, September 30, 2012. · c. Depreciation of $5,000 must be recognized on a service truck purchased on July 1, 2012, at a cost of $30,000. · d. Cash of $4,800 was collected on November 1, 2012, for services to be rendered evenly over the next year beginning on November 1. Unearned service revenue was credited when the cash was received. · e. On November 1, 2012, Huntington paid a one-year premium for fire insurance of a total of $12,000 for one year of coverage starting on that date. Cash was credited and prepaid insurance was debited for this amount. · f. The company earned service revenue of $6,000 on a special job that was completed December 24, 2012. Collection will be made during January 2012. No entry has been recorded. · g. At December 31, 2012, wages earned by employees totaled

- 14. $17,500. The employees will be paid on the next payroll date, January 15, 2012. · h. On December 31, 2012, the company estimated it owed $16,000 for 2012 property taxes on land. The tax will be paid when the bill is received in January 2012. Using the information above, prepare the adjusting entry required for each transaction at December 31, 2012. To complete this problem, you may choose to use the Assessment 3, Problem 1 Template, which is linked in the Suggested Resources under the Capella Resources heading. Problem 2: Analyzing the Effects of Adjusting Entries on the Accounting Model To complete this problem, you will need to refer to Problem 1. Indicate in a table format the effect of each adjusting entry in Problem 1 (a through h) and the amount of the effect. Use + for increase, − for decrease, and NE for no effect. This problem is built around the following formulas and concepts: · Assets = Liabilities + Stockholders' Equity. · Revenues − Expenses = Net Income. · Net Income accounts are closed to Retained Earnings, a part of Shareholders' Equity. Accounting/Accounting/Assessment 4/Assessment 4.docx Assessment 4 · Note: Some of the assessments in this course build upon each other, so you are strongly encouraged to complete them in the order in which they are presented. For this assessment, you may use Word or Excel to complete the assessments throughout this course, but you will find Excel to be most helpful for creating spreadsheets. Tutorials for using Excel are provided in the Supplemental Resources in the left navigation menu. If you use Excel, submit the assessment in one Excel document, using separate tabs for each spreadsheet. To complete this problem, you may choose to use the

- 15. Assessment 4, Comprehensive Problem Template, which is linked in the Suggested Resources under the Capella Resources heading. Comprehensive Problem Patricia Allison began an engineering consulting business on January 1, 2011, organized as a corporation (PA Engineering, Inc.) under the laws of Delaware. The annual reporting period ends December 31, 2011. The trial balance on January 1, 2012, is provided in the following table: PA Engineering Trial Balance, January 1, 2012 Account Titles Debit Credit Cash $10,000 Accounts Receivable Office Supplies $20,000 Land Computers $80,000 Accumulated Depreciation (on computers) Miscellaneous Other Assets $5,000 Accounts Payable

- 16. Salaries and Wages Payable Interest Payable Income Taxes Payable Long-Term Notes Payable Contributed Capital (100,000 shares) $115,000 Retained Earnings Service Revenue Depreciation Expense Supplies Expense Wages Expense Interest Expense Income Tax Expense

- 17. Remaining Expenses (not detailed to simplify) Totals $115,000 $115,000 Transactions during 2012 are as follows: · a. Borrowed $20,000 cash on a five-year, 10 percent note payable, dated July 1, 2012. · b. Purchased land for a future building site; paid cash, $10,000. · c. Earned $200,000 in revenues for 2012, including $60,000 on credit and the rest in cash. · d. Sold 4,000 additional shares of capital stock for cash at $1.15 market value per share on January 3, 2012. · e. Incurred $120,000 in remaining expenses for 2012, including $20,000 on credit and the rest paid in cash. · f. Collected accounts receivable, $40,000. · g. Purchased other assets for $8,000 cash. · h. Paid accounts payable, $18,000. · i. Purchased office supplies on account for future use, $25,000. · j. Signed a three-year, $33,000 service contract to start February 1, 2013. · k. Declared and paid cash dividends, $10,000. Data for adjusting entries: · l. Supplies counted on December 31, 2012, $18,000. · m. Depreciation for the year on the equipment, $21,000. · n. Interest accrued on notes payable (to be computed). · o. Wages earned by employees since the December 24 payroll but not yet paid, $15,000. · p. Income tax expense, $10,000, payable in 2013. Complete the following for this problem: 1. Set up T-accounts for the accounts on the trial balance and enter beginning balances.

- 18. 1. Prepare journal entries for transactions (a) through (k) and post them to the T-accounts. 1. Journal and post the adjusting entries (l) through (p). 1. Prepare an income statement (including earnings per share), statement of stockholders' equity, balance sheet, and statement of cash flows. 1. Journal closing entries. 1. Compute the following ratios for 2012 and explain what the results suggest about the company. 22. Current ratio. (Industry average is 2.2 to 1.0.) 22. Total asset turnover. (Industry average is 3 times a year.) 22. Net profit margin. (Industry average is 5.00%.) Accounting/Accounting/Assessment 4/cf_assessment_4_comp_problem_template.xls T-Accounts BegWorksheet 1 of 9. Template for requirement 1: Set up T-accounts for the accounts on the trial balance and enter beginning balances.Learner:PA Engineering, Inc.CashAccounts ReceivablePrepaid Office SuppliesB. BalB. Bal- 0- 0- 0- 0- 0- 0- 0- 0- 0Prepaid ExpensesComputersMiscellaneous Other AssetsB. BalB. Bal5,000.00Land5,000.00Accounts PayableNotes PayableInterest Payable- 0- 0- 0Supplies ExpenseIncome Tax PayableSalaries and Wages PayableWages ExpenseContributed CapitalAccumulated Depreciation115,000.00B. Bal115,000.00Depreciation ExpenseDividends DeclaredService RevenueRemaining ExpensesInterest ExpenseIncome Tax ExpenseRetained EarningsEnd of worksheet Journal EntriesWorksheet 2 of 9. Template for requirements 2 and 3, journal entries: Prepare journal entries for transactions (a) through (k) in columns A through D. Journal the adjusting entries (l) through (p) in columns G through I.Learner:PA Engineering, Inc.Transactions during 2012DRCRAdjusting entriesDRCRDebit is always first and credit is indenteda.Cashl.Supplies expenseNote PayablePrepaid Office

- 19. SuppliesBorrowed cash(20000+25000- 18000)b.Landm.Depreciation expenseCashAccumulated depreciationPurchased landc.Cashn.Interest expenseAccounts ReceviableAccrued Interest payableService Revenue($20,000 x .1 x (6/12))Earned revenues for 2012o.Wages expensed.CashSalaries and Wages payableContributed Capital(4,000 shares @1.15 - market value)p.Income tax expensee.Remaining ExpensesIncome tax payableCashAccounts PayableDebits must equal Credits- 0- 0Incurred remaining expensesf.CashAccounts ReceivableCollected on Accounts Receivableg.Other AssetsCashPurchased other assetsh.Accounts PayableCashPaid accounts payablei.Prepaid Office SuppliesAccounts PayablePurchased office suppliesj.No entry contract onlyk.Dividends DeclaredCashDeclared and paid cash dividendsDebits must equal Credits- 0- 0End of worksheet T-AccountsWorksheet 3 of 9. Template for requirements 2 and 3, T-accounts: Post transactions (a) through (k) and adjusting entries (l) through (p) to the T-accounts.Learner:PA Engineering, Inc.CashAccounts ReceivablePrepaid Office SuppliesB. Bal(b)( c)60,000.0040,000.00(f)B. Bal(l)(a)(e)(i)(c )(g)60,000.0040,000.00- 0- 0(d)(h)20,000.00- 0(f)(k)- 0- 0- 0Prepaid ExpensesComputersMiscellaneous Other AssetsB. Bal80,000.00B. Bal5,000.00Land(g)(b)10,000.005,000.00Accounts Payable(h)(e)Notes PayableInterest Payable25,000.00(i)(a)1,000.00(n)- 025,000.0025,000.00Supplies ExpenseIncome Tax PayableSalaries and Wages Payable(l)10,000.00(p)(o)Wages ExpenseContributed CapitalAccumulated Depreicaiton(o)B. Bal(m)(d)- 0Depreciation ExpenseDividends DeclaredService Revenue(m)(k)( c)Remaining ExpensesInterest ExpenseIncome Tax Expense(e)(n)(p)Retained EarningsEnd of worksheet Income StatementWorksheet 4 of 9. Template for requirement 4: Prepare an income statement (including earnings per share).Learner:PA Engineering, Inc.Income StatementFor the Year Ended December 31, 2012Service RevenueLess:

- 20. ExpensesDepreciation expenseSupplies expenseWages expenseInterest expenseRemaining expenseTotal expense- 0Net Income before taxes- 0Less: Income TaxesNet Income$ - 0End of worksheet Stockholders' EquityWorksheet 5 of 9. Template for requirement 4: Prepare a statement of stockholders' equity.Learner:PA Engineering, Inc.Statement of Stockholder's EquityFor the Year Ended December 31, 2012Contributed Capital: December 31, 2011, 100,000 sharesAdd: January 3, 2012 issue of 4,000 sharesTotal Contributed Capital at December 31, 2012- 0Retained Earnings:Balance December 31, 2011Add: Net IncomeLess DividendsBalance December 31, 2012- 0Total Stockholder's Equity$ - 0End of worksheet Balance SheetWorksheet 6 of 9. Template for requirement 4: Prepare a balance sheet.Learner:PA Engineering, Inc.Balance SheetAt December 31, 2012AssetsLiabilitiesCurrent AssetsCurrent LiabilitiesCashAccounts PayableAccounts ReceivableSalaries and Wages PayablePrepaid Office SuppliesInterest PayableIncome Tax PayableTotal Current Assets- 0Total Current Liabilities- 0Long-Term Notes PayableLong-Term AssetsLandComputersContributed CapitalLess: Accumulated Depreciation (enter as -)Retained EarningsMiscellaneous Other Assets- 0Total Long-Term Assets- 0Total Liabilities and Owners' Equity$ - 0Total Assets$ - 0End of worksheet Cash FlowsWorksheet 7 of 9. Template for requirement 4: Prepare a statement of cash flows.Learner:PA Engineering, Inc.Statement of Cash FlowsFor the Year Ending December 2012Cash flows from operating activitiesCash collected from customersCash paid to suppliersCash paid for remaining expensesNet cash flows from operating activities0Cash flows from investing activitiesCash paid for landCash paid for other assetsNet cash flows from investing activities0Cash flows from financing activitiesCash received from issuing stock to ownersCash received from note payableCash paid for dividendsNet cash flows from financing activities0Net increase

- 21. in cash during the month0Cash and cash equivalents, January 1Cash and cash equivalents, December 310Ending Cash balance should agree to Balance Sheet balance of $68,600. If agrees to Balance Sheet, next cell will be zero.$ - 0End of worksheet Closing EntriesWorksheet 8 of 9. Template for requirement 5: Journal closing entries.Learner:PA Engineering, Inc.Closing EntriesDRCRService RevenueIncome SummaryIncome SummaryDepreciation ExpenseSupplies ExpenseWages ExpenseInterest ExpenseIncome Tax ExpenseRemaining ExpenseIncome SummaryRetained EarningsRetained EarningsDividends DeclaredDebits must equal credits- 0- 0End of worksheet RatiosWorksheet 9 of 9. Template for requirement 6: Compute the current ratio, asset turnover, and net profit margin for 2012 and explain what the results suggest about PA Engineering, Inc.Learner:RatiosCurrent Ratio = Current Assets ÷ Current LiabilitiesCurrent Assets=- 0Current LiabilitiesCurrent ratio results compared to industry average (2.2 to 1.0):Asset Turnover = Sales ÷ AssetsSales=- 0AssetsAsset turnover results compared to industry average (3 times per year):Net Profit Margin = Net Income ÷ SalesNet Income=0%SalesNet profit margin results compared to industry average (%5.00):End of worksheet Accounting/Accounting/Assessment 5/Assessment 5.docx Assessment 5 · Preparation For this problem, you will need to select a publicly traded company. Once you have selected a publicly traded company, obtain Form 10-K for the company for the most current fiscal year. Use the EDGAR database from the U.S. Securities and Exchange Commission (SEC) or the investor (or investor relations) page on the company's site. Follow these steps to find Form 10-K for your selected company

- 22. using the SEC's EDGAR database: 1. Go to the Company Search Page by clicking the link in the Required Resources, under Internet Resources. 2. Type the company's official name in the Company Name box to search for the company's filings. 3. Select the 10-K form from the list of search results. Analysis of a Company's Financial Statements Assume you have been hired by a client to evaluate the financial health of the company you have selected. The client wants advice on whether or not the company is a viable option for their current portfolio. Create your analysis and recommendation for the client using the company's financial statements and your prior knowledge of accounting, supplemented by textbooks or other references of your choosing, to answer the following questions and computations: 4. What were the company's assets, liabilities, and owners' equity amounts at the end of fiscal year? 5. If the company were liquidated at the end of the fiscal year, are the shareholders guaranteed to receive the total shown in your answer for owners' equity (question 1)? Clearly explain why or why not. 6. What were the company's noncurrent liabilities for the fiscal year? 7. What was the company's current ratio for the fiscal year? 8. For the fiscal year, did the company have a cash inflow or outflow from investing activities? How much? 9. For the fiscal year, how much was the company's cash flow from operations? Why is this not the same amount as the company's operating income? Explain in general terms. 10. What is the company's revenue recognition policy? (Hint: Look in the notes to the financial statements.) 11. Calculate general, administrative, and selling expenses as a percentage of sales for the past three fiscal years. By what percentage did these expenses increase or decrease? This is calculated as Percentage Change = (Current Year % − Prior Year %) / Prior Year %.

- 23. 12. Compute the company's total asset turnover for the fiscal year and explain its meaning. Show all of your work. 13. How much is in the prepaid expenses and other current assets account at the end of fiscal year? Where did you find this information? 14. What did the company report for deferred rent and other liabilities at the end of fiscal year? Where did you find this information? 15. What is the difference between prepaid rent and deferred rent? 16. What are accrued liabilities? Describe in general terms. 17. What would generate the interest income that is reported on the income statement? 18. What are the company's earnings per share (basic only) for the three years reported? 19. Compute the company's net profit margin for the three years reported. What does the trend suggest to you? 20. How much cash and cash equivalents does the company report at the end of the fiscal year? 21. What was the change in accounts receivable and how did it affect net cash provided by operating activities for the current year? 22. Compute the company's gross profit percentage for the most recent two years. Has it risen or fallen? Explain the meaning of the change. Deliverable to the Client: Analysis Summary and Investment Recommendation Prepare a business memo addressed to the client summarizing your analysis and providing a recommendation on investing: . Write 2–4 pages in a professional format appropriate for the information you are presenting. . Make sure you have answered all of the provided questions and computations in your analysis. If a question or computation does not apply, there should be a statement within your memo stating that the aspect does not apply and why. For example: "Based on the review of the XYZ Company, there were no

- 24. prepaid expenses." . Include support for your investment recommendation by citing the company's financial statements and other references of your choosing, Accounting/Accounting/Assessment 6/Assessment 6.docx · When a company owns inventory, it has to decide how to consistently value the inventory sold and on hand. Four inventory valuation methods are available to help the organization effectively value its inventory. These valuation methods are based on the systematic cash flow of adding and removing inventory, and each has its advantages and disadvantages. When selecting an inventory method, management should select the method that best reflects their operations. Once an inventory valuation method is selected, it must be applied consistently from year to year. Show Less The four inventory valuation methods are described below: · Average cost: An average cost is calculated based the total costs for the inventory on hand. · First in, first out (FIFO): This method assumes that inventory is used in the order it is received. · Last in, first out (LIFO): This method assumes that the newest inventory is always used first. · Specific identification: Under this method, the costs and selling price are specified for one particular item. This method is appropriate when each item has a unique identifying characteristic. When a company purchases a long-term asset such as equipment, the cost of the long-term asset is capitalized. This means the asset will benefit more than one accounting period, so the original cost of the asset is allocated to the accounting

- 25. periods it benefits. This allocation results in an expense that is recorded over several periods known as depreciation expense. Depreciation is used in accounting to estimate the cost of the fixed asset that is allocated to each period. There are a variety of depreciation methods available to estimate depreciation expense. · Toggle Drawer Questions to Consider To deepen your understanding, you are encouraged to consider the questions below and discuss them with a fellow learner, a work associate, an interested friend, or a member of the business community. Show Less · What are the acceptable inventory valuation methods under the U.S. Generally Accepted Accounting Principles (GAAP)? · How does each affect the valuation of inventory? · How does each affect cost of goods sold? · What elements might organizational leaders consider when selecting which inventory valuation method to adopt? · Toggle Drawer Resources Suggested Resources The following optional resources are provided to support you in completing the assessment or to provide a helpful context. For additional resources, refer to the Research Resources and Supplemental Resources in the left navigation menu of your courseroom. Capella Resources Click the links provided to view the following resources: · Assessment 6, Problem 1 Template. Show More Library Resources The following e-books or articles from the Capella University Library are linked directly in this course: · Murthy, G. (2009). Financial accounting. Mumbai, India: Himalaya Publishing House.

- 26. · Vataliya, K. S. (2009). Practical financial accounting: Advance methods, techniques and practices. Jaipur, India: Paradise Publishers. · Doran, D. T. (2012). Financial reporting standards: A decision-making perspective for non-accountants. New York, NY: Business Experts Press. Course Library Guide A Capella University library guide has been created specifically for your use in this course. You are encouraged to refer to the resources in the MBA-FP6014 – Financial Accounting Library Guide to help direct your research. Bookstore Resources The resources listed below are relevant to the topics and assessments in this course. These resources are available from the Capella University Bookstore. When searching the bookstore, be sure to look for the Course ID with the specific – FP (FlexPath) course designation. · Libby, R., Libby, P., & Hodge, F. (2017). Financial accounting (9th ed.). New York, NY: Irwin. · Assessment Instructions Note: Some of the assessments in this course build upon each other, so you are strongly encouraged to complete them in the order in which they are presented. For this assessment, complete Problems 1 and 2. You may use Word or Excel to complete the assessments throughout this course, but you will find Excel to be most helpful for creating spreadsheets. Tutorials for using Excel are provided in the Supplemental Resources in the left navigation menu. If you use Excel, submit the assessment in one Excel document, using separate tabs for each spreadsheet. To complete the first problem, you may choose to use the Assessment 6, Problem 1 Template linked in the Suggested Resources under the Capella Resources heading. Problem 1: The Effects of Different Cost Flow Assumptions for Inventory At the end of January 2011, the records of Sheldon and Blair

- 27. showed the following for a particular item that sold at $20 per unit: Problem 1, Table 1: Records of Sheldon and Blair Transactions Units Total Amount Inventory, January 1, 2011 500 @ $6.00 $3,000 Purchase, January 12 600 @ $7.00 $4,200 Purchase, January 26 200 @ $7.10 $1,420 Sale (400 units sold for $20 each) Sale (300 units sold for $20 each) Based on the information provided in the table above, complete the following. An optional template, Assessment 6, Problem 1 Template, is provided in the Suggested Resources under the Capella Resources heading. 4. Assuming the use of a periodic inventory system, prepare a summarized income statement through gross profit for the month of January under each method of inventory listed below. Show the inventory computations for each method in detail. 1. a. Average cost. (Round the average cost per unit to the nearest cent.) 1. b. First in, first out (FIFO). 1. c. Last in, first out (LIFO). 1. d. Specific identification. (Assume that the first sale was selected from the beginning inventory and the second sale was selected from the January 12 purchase.)

- 28. 4. Of FIFO and LIFO, which method would result in the higher pretax income? Which would result in the higher EPS? 4. Of FIFO and LIFO, which method would result in the lower income tax expense? Explain, assuming a 35 percent average tax rate. 4. Of FIFO and LIFO, which method would produce the more favorable cash flow? Explain. Problem 2: The Effects of Differing Depreciation Methods Total Workout, Inc. purchased three ï¬ï¿½tness machines from Ace Used Equipment at the beginning of the year. All three were used machines that had to be overhauled and installed before they were put into use. The costs of the machines and their renovation and installation are shown in Table 1 below: Problem 2, Table 1: Equipment Costs Account Machine A Machine B Machine C Amount paid for asset $21,000 $30,750 $8,000 Installation cost $500 $1,000 $200 Renovation costs prior to use $2,000 $1,000 $1,500 By the end of the first year, each machine had been operating 4,800 hours. Depreciation estimates are shown in Table 2 below: Problem 2, Table 2: Equipment Depreciation Machine Life

- 29. Residual Value Depreciation Method A 5 years $1,000 Straight-line B 60,000 hours $2,000 Units-of-production C 4 years $1,500 Double-declining balance Using the data provided above, complete the following: 4. Compute the cost of each machine. 4. Give the entry to record depreciation expense at the end of the first year, using all three depreciation methods listed in Table 2. Inventory Analysis and Depreciation Methods Scoring Guide View Scoring GuideUse the scoring guide to enhance your learning.How to use the scoring guide 1. [u06a1] Inventory Analysis And Depreciation Methods Complete a problem involving inventory analysis and a problem involving the use of depreciation methods. 1. Assessment Submit Submit Assessment This button will take you to the next available assessment attempt tab, where you will be able to submit your assessment. 1. u06a1 Inventory Analysis and Depreciation Methods >> View/Complete 1. u06a1 Inventory Analysis and Depreciation Methods: Revision 1 >> View/Complete

- 30. 1. u06a1 Inventory Analysis and Depreciation Methods: Revision 2 >> View/Complete Accounting/Accounting/Assessment 6/cf_assessment_6_problem_1_template.xls Solution Template for a summarized income statement through gross profit for the month ended January 31, 2011, under four inventory valuation methods: (a) weighted average, (b) FIFO, (c) LIFO, and (d) specific identification. For Sheldon and Blair.Learner:Sheldon and BlairPartial Income StatementFor the Month Ended January 31, 2011(a) Weighted Average(b) FIFO(c) LIFO(d) Specific IdentificationSales revenue1$14,000$14,000$14,000$14,000Cost of goods sold2$3,000$200$2,300($1,120)Gross profit$11,000$13,800$11,700$15,120Sheldon and BlairComputations1Sales revenue:700 units @ $20 =$14,0002Cost of goods sold:UnitsWeighted AverageFIFOLIFOSpecific IdentificationBeginning inventory500$3,000$3,000$3,000$3,000Purchases (net)30$0$0$0$0Goods available for

- 31. sale500$3,000$3,000$3,000$3,000Ending inventory4$0$2,800$700$4,120Cost of goods sold500$3,000$200$2,300($1,120)3Purchases (net)Purchase, January 12$0Purchase, January 26$0Totals0$04Ending inventory(a) Weighted-average cost:UnitsAmountBeginning inventory500@$6$3,000Purchases30$0500$3,000Average cost:$8,620 ÷ 1,300 units =6.00Ending inventory:600 units × $6.63 =$0(b) FIFO:units @ $7.10units @ $7.00$2,800600$2,800(c) LIFO:units @ $6.00units @ $7.00$700600$700(d) Specific identification:units @ $6.00units @ $7.00units @ $7.10$1,420600$4,120Of FIFO and LIFO, which method would result in the higher pretax income? Which would result in the higher EPS?Of FIFO and LIFO, which method would result in the lower income tax expense? Explain, assuming a 35 percent average tax rate.FIFO = Gross profit × .35LIFO = Gross profit × .35Of FIFO and LIFO, which method would produce the more favorable cash flow? Explain.End of worksheet Accounting/Accounting/Assessment 7/Assessment 7.docx · Complete two problems. Problem 1 focuses on working capital and quick ratio, and Problem 2 is a comprehensive problem in which you will bring together various financial analysis measures and interpret their meaning in order to draw conclusions about hypothetical companies.

- 32. Note: Some of the assessments in this course build upon each other, so you are strongly encouraged to complete them in the order in which they are presented. Show Less By successfully completing this assessment, you will demonstrate your proficiency in the following course competencies and assessment criteria: · Competency 1: Apply theories, models, and practices of accounting in the construction and analysis of financial statements. 1. Perform appropriate computations using data from company financial statements. 1. Compute working capital using appropriate financial data. 1. Compute the quick ratio using appropriate financial data. . Competency 4: Integrate accounting analyses into general business management planning and decision making. 2. Interpret the implications of the working capital results. 2. Report recommendations and solutions for each company. Competency Map Check Your ProgressUse this online tool to track your performance and progress through your course. · Toggle Drawer Questions to Consider As you complete the assessment, you may find it helpful to consider the questions below. You are encouraged to discuss

- 33. them with a fellow learner, a work associate, an interested friend, or a member of the business community, in order to deepen your understanding of the topics. Show More . What is meant by liquidity? . What metrics can be used to assess improvement or deterioration in liquidity? . How is liquidity influenced by debt? . How do different types of debt affect liquidity? . How does equity affect liquidity? . How do different types of assets affect liquidity? · Toggle Drawer Resources Suggested Resources The following optional resources are provided to support you in completing the assessment or to provide a helpful context. For additional resources, refer to the Research Resources and Supplemental Resources in the left navigation menu of your courseroom. Library Resources The following e-books or articles from the Capella University Library are linked directly in this course: . Murthy, G. (2009). Financial accounting. Mumbai, India: Himalaya Publishing House. . Vataliya, K. S. (2009). Practical financial accounting:

- 34. Advance methods, techniques and practices. Jaipur, India: Paradise Publishers. . Doran, D. T. (2012). Financial reporting standards: A decision-making perspective for non-accountants. New York, NY: Business Experts Press. Show Less Course Library Guide A Capella University library guide has been created specifically for your use in this course. You are encouraged to refer to the resources in the MBA-FP6014 – Financial Accounting Library Guide to help direct your research. Bookstore Resources The resources listed below are relevant to the topics and assessments in this course. These resources are available from the Capella University Bookstore. When searching the bookstore, be sure to look for the Course ID with the specific – FP (FlexPath) course designation. . Libby, R., Libby, P., & Hodge, F. (2017). Financial accounting (9th ed.). New York, NY: Irwin. · Assessment Instructions Note: Some of the assessments in this course build upon each other, so you are strongly encouraged to complete them in the order in which they are presented. For this assessment, complete Problems 1 and 2. You may use Word or Excel to complete the assessments throughout this

- 35. course, but you will find Excel to be most helpful for creating spreadsheets. Tutorials for using Excel are provided in the Supplemental Resources in the left navigation menu. If you use Excel, submit the assessment in one Excel document, using separate tabs for each spreadsheet. Problem 1: Working Capital, Current Ratio, Quick Assets, Acid- Test Ratio The Sanchez Corporation is preparing its 2012 balance sheet. The company records show the following selected amounts at the end of the accounting period, December 31, 2012: Problem 1: Sanchez Corporation Selected Amounts Account Dollar Amount Total assets $600,000 Total noncurrent assets $350,000 Liabilities Dollar Amount Notes payable (8%, due in 6 years) $40,000 Accounts payable $60,000 Income taxes currently payable

- 36. $15,000 Liability for withholding taxes $4,000 Rent revenue collected in advance by up to four months $8,000 Bonds payable (due in 15 years). $100,000 Wages payable $6,000 Property taxes payable $3,000 Note payable (10%, due in 6 months) $22,000 Interest payable $1,200 Common stock $200,000 Use the information provided in the table to compute and answer the following for the Sanchez Corporation: · Compute (a) working capital and (b) the quick ratio—quick assets are $120,000. · Why is working capital important to management? · How do financial analysts use the quick ratio? · Would your computations be different if the company reported $250,000 worth of contingent liabilities in the notes to the

- 37. statements? Explain. Include in your explanation a definition of contingent liabilities and an example of a contingent liability. Problem 2: Comprehensive Problem Bring together various financial analysis measures and interpret their meaning in order to draw conclusions about hypothetical companies. Note that each situation provided is to be considered independently of the others. Situation A: The following tables represent selected data from recent financial statements of Lincoln and Samuelson, Inc. (dollars in thousands): Problem 2, Table 1: Lincoln and Samuelson, Inc. Selected Items from Balance Sheets Assets (in thousands) December 31, 2012 December 31, 2011 Current assets: Cash and cash equivalents $4,000 $3,400 Accounts receivable (net of allowances of $32 and $28, respectively) $6,500 $5,700

- 38. Problem 2, Table 2: Lincoln and Samuelson, Inc. Selected Income Statement Data Account 2012 2011 2010 Net sales (in millions) $6,020 $5,425 $5,000 Net income (in millions) $300 $285 $220 The selected income statement data is for the year ended December 31. The company also reported bad debt expense of $62,000 in 2012; $55,000 in 2011; and $49,500 in 2010. Using the data provided, complete the following for Lincoln and Samuelson, Inc.: · Compute the dollar amount of uncollectible accounts receivable that the company wrote off as uncollectible in 2012. Show all of your work. · Assuming all sales were on credit, what amount of cash did the company collect on accounts receivable in 2012? Show all of your work.

- 39. · Compute the company's net profit margin for the three years presented. What does the trend suggest to you about the company? Situation B: The Israel Manners Entertainment Group uses the allowance approach to estimate bad debt expense, as is required of all companies with significant sales on accounts receivable. At the end of 2012, the Manners Group reported a balance in accounts receivable of $4,350,000 and estimated that $44,000 of its accounts receivable would likely be uncollectible. The allowance for doubtful accounts has a $1,500 debit balance at year-end, prior to the adjustment needed to raise it to the $44,000 desired amount. Use this information to answer the following questions for the Manners Group: · How is it possible that the allowance for doubtful accounts has developed a debit balance instead of a credit balance? · What amount of bad debt expense should be recorded for 2012? · What amount will be reported on the 2012 balance sheet as the net realizable amount of accounts receivable? Situation C: At the end of 2012, the unadjusted trial balance of Donovan, Inc. included $6,000,000 in accounts receivable, a credit balance of $50,000 in the allowance for doubtful accounts, and sales revenue (all on credit) of $200,000,000. Based on

- 40. knowledge that the current economy is in distress, Donovan increased its bad debt rate estimate to 0.4 percent on credit sales. Use this information to answer the following questions for Donovan, Inc.: · What amount of bad debt expense should be recorded for 2012? · What amount will be reported on the 2012 balance sheet for the net realizable amount of accounts receivable, after being reduced by the balance in the allowance for uncollectible accounts? Situation D: BrightStar Company reported the following inventory records for June 2012: Problem 2, Table 3: BrightStar Company Inventory Records Date Activity # of Units Cost/Unit June 1 Beginning balance 200 $40 June 5 Purchase 600

- 41. $42 June 8 Sale @ $100 per unit 500 June 17 Purchase 400 $45 June 23 Sale @ $100 per unit 500 Selling, administrative, and depreciation expenses for the month were $20,000. BrightStar's tax rate is 35 percent. Use this information and the table above to complete the following for BrightStar Company: · Calculate the cost of ending inventory and the cost of goods sold under each of the following methods: . a. First in, first out (FIFO). . b. Last in, first out (LIFO). . c. Weighted average. · Using your answers from question 1 above, answer the following: . a. What is the gross profit percentage under the FIFO method?

- 42. . b. What is net income under the LIFO method? . c. Which method would you recommend to BrightStar for tax purposes? Explain your recommendation. . d. If BrightStar also used the method that you recommended for tax purposes on its balance sheet, would BrightStar's current ratio suffer, compared to the use of FIFO? · BrightStar uses the lower of FIFO cost or market method to value its inventory for reporting purposes at the end of the month. If inventory had a market replacement value of $44 per unit, what would BrightStar report in its balance sheet for inventory? Why? Situation E: BlackBurn Company purchased the following on January 1, 2012: · Office Equipment at a cost of $100,000 with an estimated useful life to the company of five years and a residual value of $10,000. The company uses the double-declining-balance method of depreciation for the equipment. · Factory equipment at an invoice price of $780,000 plus shipping costs of $20,000. The equipment has an estimated useful life of 100,000 hours and no residual value. The company uses the units-of-production method of depreciation for the equipment. · A patent at a cost of $450,000 with an estimated useful life of 15 years. The company uses the straight-line method of

- 43. amortization for intangible assets with no residual value. Use the information above to complete the following for BlackBurn Company: · Prepare a partial depreciation schedule for 2012, 2013, and 2014 for the following assets. Round your answers to the nearest dollar. . a. Office equipment. . b. Factory equipment. The company used the equipment for 8,000 hours in 2012; 9,000 hours in 2013; and 8,500 hours in 2014. · On January 1, 2014, BlackBurn altered its corporate strategy dramatically. The company sold the factory equipment for $700,000 in cash. Record the entry related to the sale of the factory equipment. · On January 1, 2014, when the company changed its corporate strategy, its patent had estimated future cash flows of $300,000 and a fair value of $250,000. What would the company report on the income statement (account and amount) regarding the patent on January 2, 2014? Explain your answer. (Hint: You may need to research this question using Internet sources.) Accounting/Accounting/Assessment 8/Assessment 8.docx · Using the transactions listed below for Audrey's Ice Cream Parlor, prepare a statement of cash flows for the month of April

- 44. 2012. Classify the transactions into appropriate categories (operating activities, investing activities, and financing activities). To complete this assessment, use the Statement of Cash Flows Template to complete and submit the following information: · a. Received cash of $40,000 total ($10,000 each) from four investors. Each investor received 100 shares of common stock. This took place on April 1. · b. Paid three months' rent for the store on April 1 at $2,000 per month (recorded as prepaid expenses). · c. Purchased ice cream and cones for $6,000 on account payable, due in 60 days. This took place on April 2. · d. Purchased supplies for $1,000 cash on April 2. · e. Received a two-year $11,000 loan at the bank. The note payable is dated April 2. · f. Used the money from (e) to purchase a computer for $3,000 (for record keeping and inventory tracking) and to purchase $8,000 of used furniture and fixtures for the store. · g. Placed a grand opening advertisement in the local paper for $600 cash. · h. Made sales in the first half of the month totaling $5,000: $4,250 was in cash and the rest was on accounts receivable. The cost of the ice cream sold was $2,000. · i. Made a $600 payment on accounts payable on April 18. · j. Incurred and paid employee wages of $2000 for the month

- 45. of April. · k. Collected accounts receivable of $700 from customers. · l. Made a repair to one of the refrigerators for $300. · m. Made sales in the last half of the month for $6,000, all for cash. The cost of the ice cream sold was $2,400. Accounting/Accounting/Assessment 8/cf_statement_cash_flows_template.xls Statement of Cash FlowsTemplate for statement of cash flows for Audrey's Ice Cream Parlor for the month ended April 30, 2012. Classify the transactions into appropriate categories (operating activities, investing activities, and financing activities). See the transactions provided in the assessment.Learner:Audrey's Ice Cream ParlorStatement of Cash FlowsFor the Month Ended April 30, 2012Cash from Operations:Collections from Customers (Items K, H, and M)Cash paid for Inventory (Item I)Cash paid for Rent (Item B)Cash paid for Supplies (Item D)Cash paid for Advertising (Item G)Cash paid for Wages (Item J)Cash paid for Repairs (Item L)Cash provided by Operations$ - 0Investing Cash Flow:Cash from borrowing from bank (Item E)Cash paid for Equipment and Furniture (Item F)Net Investing Cash Flow$ - 0Financing Cash Flow:Issuance of Stock (Item A)Overall Increase in Cash$ - 0Add: Cash at April 1Yields: Cash at April

- 46. 30$ - 0End of Worksheet Accounting/Accounting/Assessment 9/Assessment 9.docx · Preparation For this problem, you will need to select two publicly traded companies. For comparison purposes, the two companies should be competitors within the same industry. Once you have selected two publicly traded companies, obtain Form 10-K for each company for the most current fiscal year. Use the EDGAR database from the U.S. Securities and Exchange Commission (SEC) or the investor (or investor relations) page on the company's site. Follow these steps to find Form 10-K for each selected company using the SEC's EDGAR database: 1. Go to the Company Search Page by clicking the link in the Required Resources, under Internet Resources. 2. Type the company's official name in the Company Name box to search for the company's filings. 3. Select the 10-K form from the list of search results. Analysis of the Financial Statements and Comparison of the Results Your supervisor has given you an important task to complete for one of the firm's top clients. The client has identified two companies within the same industry to add to his current portfolio. He does not want to add both since these are

- 47. competing companies. Your task is to complete an analysis on these companies, compare the results, and provide a recommendation to the client. Complete your analysis for the client using the financial statements and your prior knowledge of accounting, supplemented by textbooks or other references of your choosing, to answer the following questions and computations: 4. What method does the company use to determine the cost of inventory for the fiscal year? 5. Compute the inventory turnover ratio for the fiscal year. Also compute it for the previous two fiscal years. What conclusions can you make? 6. What method of depreciation does the company use? Does the company use the same method for all fixed assets, or are different classes of assets depreciated differently? 7. What is the amount of accumulated depreciation and amortization at the end of the most recent reporting year? 8. For depreciation purposes, what is the estimated useful life of furniture and fixtures? 9. What was the original cost of leasehold improvements owned by the company at the end of the most recent reporting year? 10. What amount of depreciation and amortization was reported as expense for the most recent reporting year? 11. How many shares of common stock are authorized at the end of the current year? How many shares are issued and

- 48. outstanding at the end of the current year? 12. Is there more than one class of common stock? If so, what is the name of each class of common stock? 13. Is there any preferred stock? If so, what is the dividend rate on the preferred stock, as a percentage of the par value of the preferred stock? 14. Did the company pay dividends on the common stock during the most recent reporting year? If so, what was the total amount of dividends paid and how much were they per share? 15. Does the company have any treasury stock? If so how much? 16. Has the company issued a stock dividend or a stock split over the past three reporting years? If so, what percentage and in what year or years? 17. Does the company's common stock have par value? If it does, what is the par value? 18. Did the common stockholders buy back a significant amount of shares in the current year? You can see this in the Statement of Stockholders' Equity as a reduction in shares. 19. Does the company have any marketable securities at the end of the year? How many dollars of marketable securities? How are they classified? Short-term, long-term, or both? 20. How much cash did the company use to purchase marketable securities during the current year, if any? Where did you look to find this information? 21. Is the total amount of cash flows from operations the exact

- 49. same amount regardless of whether the direct or the indirect method is used? Explain. 22. How about the Financing and Investing Cash Flow sections? Are they the exact same regardless of whether the direct or the indirect method is used? 23. Which method, the direct or indirect method, was used to report cash flows from operating activities? How can you be sure about this? Include in your answer the first three items in the Cash From Operations section. 24. What is the major use of cash in the Cash From Investing Activities section? 25. What is the major source of cash in the Cash From Investing Activities section? 26. Are there any sources of cash in the Cash From Financing Activities section? What are they? 27. Has the company paid cash dividends during the last three years? How do you know? Deliverable to the Client: Summary and Investment Recommendation Prepare a business memo addressed to the client summarizing your analysis and comparison of both companies and providing a recommendation on investing in one of the companies. . Write 2–4 pages in a professional format appropriate for the information you are presenting. . Make sure you have answered all of the provided questions

- 50. and computations in your analysis. If a question or computation does not apply, there should be a statement within your memo stating that the aspect does not apply and why. For example: "Based on the review of the XYZ Company, there were no dividends paid for the year ending 20XX." . Include support for your conclusions and investment recommendation. Cite your own analysis and comparison of the companies, the companies' financial statements, and other references of your choosing. MBS pass-throughYield to maturity2.750%Initial principal of MBS600000MBSWAC4.750%total payments733938WAM (initial)28value to investor628975Seasoning3average time to payment of principal73.39Servicing fee25duration64.06Fee for credit enhancement85average time to receipt of paymentsPSA rate250.00Pass through coupon rate3.650%Yield to maturity2.750%MBS pass throughmonth of MBSmonths to maturityprincipal balancescheduled paymentinterestscheduled principalCPRSMMexcess principaltotal principaltotal paymenttotal feespass through interestpass through principaltotalt*principalt*payment/(1+y)t 0333600000133259812132462375.00871.022.0%0.17%1008187 8.844254550.001825.001878.843703.8418793695233159598932 412367.56872.992.5%0.21%12592131.754499548.281819.29213

- 72. 0.000.0015.0%1.35%-0-0.00-0-0.00-0.00-0.00-0.00-0-03600-00- 0.000.0015.0%1.35%-0-0.00-0-0.00-0.00-0.00-0.00-0-0 IO and PO pass-throughsYield to maturity2.750%Initial principal of MBS600000IOPOWAC4.75%total payments133938600000WAM (initial)28value to investor117510511465Seasoning3average time to payment of principal73.39Servicing fee25duration54.2566.32Fee for credit enhancement85average time to receipt of payments60.25PSA rate250Pass through coupon rate3.65%Yield to maturity2.75%IO pass-throughPO pass-throughmonth of MBSmonths to maturityprincipal balancescheduled paymentinterestscheduled principalCPRSMMexcess principaltotal principaltotal paymenttotal feespass through interestpass through principalinterest paymentst*paymentt*payment/(1+y)t principal paymentst*paymentt*payment/(1+y)t 0333600000133259812132462375.00871.022.0%0.17%1008187 8.844254550.001825.001878.841825.001825.001820.831879187 91875233159598932412367.56872.992.5%0.21%12592131.7544 99548.281819.292131.751819.293638.573621.95213242634244 333059360632342359.12874.603.0%0.25%15092383.254742546 .321812.802383.251812.805438.405401.1923837150710143295 9097332262349.69875.843.5%0.30%17572633.004983544.1418 05.552633.001805.557222.217156.382633105321043653285880 9232162339.27876.704.0%0.34%20042880.705220541.731797.5