Correlation and Beta: Listed Equity REITs and Stocks

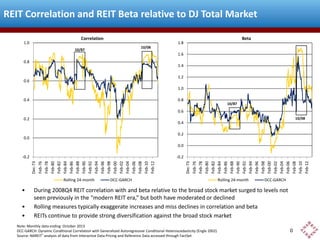

The correlation between listed U.S. equity REITs and U.S. stocks is 0.60 as of July 2017. The REIT-stock correlation had jumped as high as 0.82 during the recovery from the liquidity crisis, but fell rapidly from 2012 to 2015. Beta of listed U.S. equity REITs relative to the broad U.S. stock market is now just 0.71, below the levels that prevailed during the four years prior to the crisis. These figures are based on a DCC-GARCH model (dynamic conditional correlation with generalized autoregressive conditional heteroskedasticity, Engle 2002) using monthly total returns from the FTSE NAREIT All Equity REIT Index and the Russell 3000 Index. The data come from FactSet and the modeling uses Matlab code. This analysis is updated monthly. Questions? Contact me at bcase@nareit.com.

Recommended

Recommended

More Related Content

More from Brad Case, PhD, CFA, CAIA

More from Brad Case, PhD, CFA, CAIA (8)

Recently uploaded

Recently uploaded (20)

Correlation and Beta: Listed Equity REITs and Stocks

- 1. -0.2 0.0 0.2 0.4 0.6 0.8 1.0 Dec-73 Dec-75 Dec-77 Dec-79 Dec-81 Dec-83 Dec-85 Dec-87 Dec-89 Dec-91 Dec-93 Dec-95 Dec-97 Dec-99 Dec-01 Dec-03 Dec-05 Dec-07 Dec-09 Dec-11 Dec-13 Correlation Rolling 24-month DCC-GARCH 10/87 REIT Correlation and REIT Beta relative to DJ Total Market • During 2008Q4 REIT correlation with and beta relative to the broad stock market surged to levels not seen previously in the “modern REIT era,” but both have declined substantially since then • Rolling measures typically exaggerate increases and miss declines in correlation and beta • REITs continue to provide strong diversification against the broad stock market Note: Monthly data through December 2014 DCC-GARCH: Dynamic Conditional Correlation with Generalized Autoregressive Conditional Heteroscedasticity (Engle 2002) Source: NAREIT® analysis of data from Interactive Data Pricing and Reference Data accessed through FactSet -0.2 0.0 0.2 0.4 0.6 0.8 1.0 1.2 1.4 1.6 1.8 Dec-73 Dec-75 Dec-77 Dec-79 Dec-81 Dec-83 Dec-85 Dec-87 Dec-89 Dec-91 Dec-93 Dec-95 Dec-97 Dec-99 Dec-01 Dec-03 Dec-05 Dec-07 Dec-09 Dec-11 Dec-13 Beta Rolling 24-month DCC-GARCH 10/87 10/08 10/08 0