![I n n o v a t i o n f o r R e a l – L i f e R e t i r e m e n t

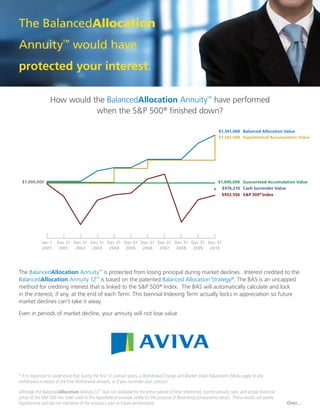

This hypothetical example is based on the following assumptions: a contract issued on January 1, 2001,

$1,000,000 single premium, a Balanced Allocation Strategy® allocation of 50% equity allocation (S&P 500®),

50% declared rate earning 1.0% interest and a Strategy Fee of 2.95%. Allocations are guaranteed for the

index term and can change on each index term renewal date. The values assume no withdrawals, loans or

distributions and do not reflect any surrender charges. The dark red line represents the value of the S&P

500® Index over the relevant time period and does not include any dividends.

You are in control.

What’s equally impressive about the BalancedAllocation Annuity™ is that with the patented ability to track

values daily, you would have had access to your Balanced Allocation Value, including appreciation, on any

day during this period.

It’s quite natural, as you have entered or are approaching retirement, that you begin to take a closer look

at your existing approach. Not everyone has a substantial amount of retirement assets that are exposed to

direct market risk. But, if you are like many Americans today, a very real and everyday concern is how you

would do in a market downturn.

“Standard & Poor’s”, “S&P 500”, “Standard & Poor’s 500” and “500” are trademarks of The McGraw-Hill Companies, Inc. and have been licensed for

use by Aviva Life and Annuity Company, West Des Moines, IA. These products are not sponsored, endorsed, sold or promoted by Standard & Poor’s and

Standard & Poor’s make no representation regarding the advisability of purchasing these products.

Annuities are not FDIC insured; are not obligations or deposits of, and are not guaranteed or underwritten by any bank, savings and loan or credit union

or its affiliates; are unrelated to and not a condition of the provision or term of any banking service or activity.

Guarantees provided by annuities are subject to the financial strength of the issuing insurance company; not guaranteed by any bank or the FDIC.

Market Indices do not include dividends paid on the underlying stocks, and therefore do not reflect the total return of the underlying stocks; neither a

market index nor any market-indexed annuity is comparable to a direct investment in the financial markets. Indexed annuities do not directly participate

in any stock or equity investments. Clients who purchase BalancedAllocation Annuities™ are not directly investing in the financial market.

The BalancedAllocation Annuity™ credits interest net earnings to the Accumulation Value at the end of each 2 year Term. The Accumulation Value

at any point in time is equal to the premium (plus any premium bonus, if applicable) plus interest earnings that have been credited less deductions

with respect to withdrawals. During a Term, the Balanced Allocation Value tracks appreciation to date (note that interest earnings are only credited

to the Accumulation Value at the end of a Term). The Balanced Allocation Value is used for determining the death benefit, terminal illness benefit and

confinement benefit. In addition, free partial withdrawals and Required Minimum Distributions include interest earnings to date. State law dictates the

Minimum Guaranteed Contract Value. If you surrender your annuity you will receive the greater of the Minimum Guaranteed Contract Value or the Cash

Surrender Value (Accumulation Value less applicable Withdrawal Charges, plus or minus Market Value Adjustments (where applicable)).

The BalancedAllocation Annuity 12™ [BAA12 (09/09) or state variation] and the BalancedAllocation Income Advantage® (BAAIR (09/09) or state

variation), an optional rider for which a charge is deducted, are issued by Aviva Life and Annuity Company, West Des Moines, IA. Product features,

limitations and availability vary by State; see the Product Disclosure for details.

18220 283881](data:image/gif;base64,R0lGODlhAQABAIAAAAAAAP///yH5BAEAAAAALAAAAAABAAEAAAIBRAA7)

Recommended

More Related Content

What's hot

What's hot (17)

Viewers also liked

Viewers also liked (20)

Similar to How the BalancedAllocation AnnuityTM Could Have Protected Your Retirement in a Declining Market

Similar to How the BalancedAllocation AnnuityTM Could Have Protected Your Retirement in a Declining Market (20)

How the BalancedAllocation AnnuityTM Could Have Protected Your Retirement in a Declining Market

- 1. The BalancedAllocation Annuity™ would have protected your interest. How would the BalancedAllocation Annuity™ have performed when the S&P 500® finished down? $1,341,068 Balanced Allocation Value $1,341,068 Hypothetical Accumulation Value $1,000,000 $1,000,000 Guaranteed Accumulation Value $976,210 Cash Surrender Value $952,556 S&P 500® Index Jan 1 Dec 31 Dec 31 Dec 31 Dec 31 Dec 31 Dec 31 Dec 31 Dec 31 Dec 31 Dec 31 2001 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 The BalancedAllocation Annuity™ is protected from losing principal during market declines. Interest credited to the BalancedAllocation Annuity 12™ is based on the patented Balanced Allocation Strategy®. The BAS is an uncapped method for crediting interest that is linked to the S&P 500® Index. The BAS will automatically calculate and lock in the interest, if any, at the end of each Term. This biennial Indexing Term actually locks in appreciation so future market declines can’t take it away. Even in periods of market decline, your annuity will not lose value. * It is important to understand that during the first 12 contract years, a Withdrawal Charge and Market Value Adjustment (MVA) apply to any withdrawal in excess of the Free Withdrawal amount, or if you surrender your contract. Although the BalancedAllocation Annuity 12™ was not available for the entire period of time referenced, current annuity rates and actual historical prices of the S&P 500 has been used in this hypothetical example solely for the purpose of illustrating comparative values. These results are purely hypothetical and are not indicative of the annuity’s past or future performance. Over...

- 2. I n n o v a t i o n f o r R e a l – L i f e R e t i r e m e n t This hypothetical example is based on the following assumptions: a contract issued on January 1, 2001, $1,000,000 single premium, a Balanced Allocation Strategy® allocation of 50% equity allocation (S&P 500®), 50% declared rate earning 1.0% interest and a Strategy Fee of 2.95%. Allocations are guaranteed for the index term and can change on each index term renewal date. The values assume no withdrawals, loans or distributions and do not reflect any surrender charges. The dark red line represents the value of the S&P 500® Index over the relevant time period and does not include any dividends. You are in control. What’s equally impressive about the BalancedAllocation Annuity™ is that with the patented ability to track values daily, you would have had access to your Balanced Allocation Value, including appreciation, on any day during this period. It’s quite natural, as you have entered or are approaching retirement, that you begin to take a closer look at your existing approach. Not everyone has a substantial amount of retirement assets that are exposed to direct market risk. But, if you are like many Americans today, a very real and everyday concern is how you would do in a market downturn. “Standard & Poor’s”, “S&P 500”, “Standard & Poor’s 500” and “500” are trademarks of The McGraw-Hill Companies, Inc. and have been licensed for use by Aviva Life and Annuity Company, West Des Moines, IA. These products are not sponsored, endorsed, sold or promoted by Standard & Poor’s and Standard & Poor’s make no representation regarding the advisability of purchasing these products. Annuities are not FDIC insured; are not obligations or deposits of, and are not guaranteed or underwritten by any bank, savings and loan or credit union or its affiliates; are unrelated to and not a condition of the provision or term of any banking service or activity. Guarantees provided by annuities are subject to the financial strength of the issuing insurance company; not guaranteed by any bank or the FDIC. Market Indices do not include dividends paid on the underlying stocks, and therefore do not reflect the total return of the underlying stocks; neither a market index nor any market-indexed annuity is comparable to a direct investment in the financial markets. Indexed annuities do not directly participate in any stock or equity investments. Clients who purchase BalancedAllocation Annuities™ are not directly investing in the financial market. The BalancedAllocation Annuity™ credits interest net earnings to the Accumulation Value at the end of each 2 year Term. The Accumulation Value at any point in time is equal to the premium (plus any premium bonus, if applicable) plus interest earnings that have been credited less deductions with respect to withdrawals. During a Term, the Balanced Allocation Value tracks appreciation to date (note that interest earnings are only credited to the Accumulation Value at the end of a Term). The Balanced Allocation Value is used for determining the death benefit, terminal illness benefit and confinement benefit. In addition, free partial withdrawals and Required Minimum Distributions include interest earnings to date. State law dictates the Minimum Guaranteed Contract Value. If you surrender your annuity you will receive the greater of the Minimum Guaranteed Contract Value or the Cash Surrender Value (Accumulation Value less applicable Withdrawal Charges, plus or minus Market Value Adjustments (where applicable)). The BalancedAllocation Annuity 12™ [BAA12 (09/09) or state variation] and the BalancedAllocation Income Advantage® (BAAIR (09/09) or state variation), an optional rider for which a charge is deducted, are issued by Aviva Life and Annuity Company, West Des Moines, IA. Product features, limitations and availability vary by State; see the Product Disclosure for details. 18220 283881