Agenda

● Quick introto Bayesian Structural Time Series

● Review of 2 toolkits: Prophet & BSTS

● Inference with time series: causalImpact

3.

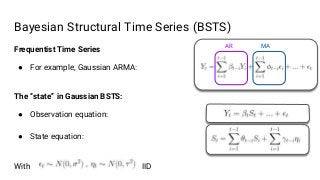

Bayesian Structural TimeSeries (BSTS)

Frequentist Time Series

● For example, Gaussian ARMA:

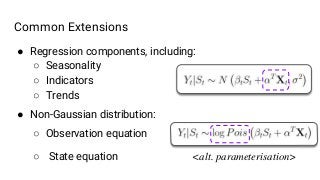

The “state” in Gaussian BSTS:

● Observation equation:

● State equation:

With IID

AR MA

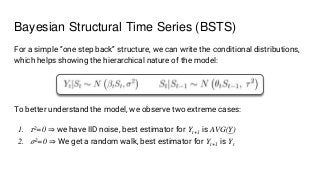

4.

To better understandthe model, we observe two extreme cases:

1. 𝜏2=0 ⇒ we have IID noise, best estimator for Yt+1 is AVG(Y)

2. 𝜎2=0 ⇒ We get a random walk, best estimator for Yt+1 is Yt

Bayesian Structural Time Series (BSTS)

For a simple “one step back” structure, we can write the conditional distributions,

which helps showing the hierarchical nature of the model:

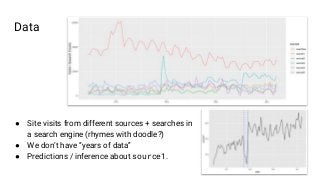

Data

● Site visitsfrom different sources + searches in

a search engine (rhymes with doodle?)

● We don’t have “years of data”

● Predictions / inference about source1.

7.

Toolkit 1: Prophet

●Wrapper around Stan

● Maintained by Facebook’s Core Data Science team

● Has R & Python bindings

● Strong/opinionated defaults

8.

Prophet mission statement

“Prophetis a procedure for forecasting time series

data based on an additive model where non-linear trends

are fit with yearly, weekly, and daily seasonality,

plus holiday effects. It works best with time series

that have strong seasonal effects and several seasons

of historical data. Prophet is robust to missing data

and shifts in the trend, and typically handles outliers

well.”

9.

What is Prophetdoing?

Fire a series of “heavy guns” at once:

● Piecewise trending (25 points!)

● Automatic seasonality (week, year)

With a small effort you can add:

● Preloaded holidays

● More cycles of seasonality

● One regressor at a time (no NA’s)

● Custom breakpoints

And the rest is IID noise...

Toolkit 2: bsts

●R package (only)

● Based on another R package - Boom (Bayesian Object

Oriented Modeling), maintained by the same author

● Long list of optional components for the time series:

seasonality, holidays, trends, AR structures, dynamic

regression, etc.

● Some versions break backwards compatibility

12.

BSTS mission statement

“Ourapproach combines three statistical methods into an

integrated system we call “Bayesian Structural Time Series”

or BSTS for short:

1) A “basic structural model” for trend and seasonality,

estimated using Kalman filters

2) Spike and slab regression for variable selection

3) Bayesian model averaging over the best performing models

for the final forecast.”[1]

13.

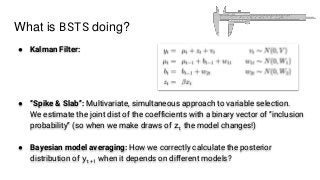

What is BSTSdoing?

● Kalman Filter:

● “Spike & Slab”: Multivariate, simultaneous approach to variable selection.

We estimate the joint dist of the coefficients with a binary vector of “inclusion

probability” (so when we make draws of zt the model changes!)

● Bayesian model averaging: How we correctly calculate the posterior

distribution of yt+1 when it depends on different models?

Summary

And for therest there’s Stan!

Prophet BSTS

Claim to

faim

Simple & powerful (fire & forget) Rich & complex (model selection)

Stability Stable (for now?) Changes from version to version

(breaks code)

Defaults Defaults for strong shrinkage,

long & “stationary” series

Allows for shorter & complex

situations and emphasizes causality

(or, aggressive fit?)

Dist Gaussian only Gaussian and (sometimes) Poisson

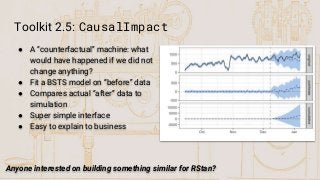

Toolkit 2.5: CausalImpact

●A “counterfactual” machine: what

would have happened if we did not

change anything?

● Fit a BSTS model on “before” data

● Compares actual “after” data to

simulation

● Super simple interface

● Easy to explain to business

Anyone interested on building something similar for RStan?

#13 Source:

[1] Scott SL, Varian HR. Bayesian Variable Selection for Nowcasting Economic Time Series. In: Economic Analysis of the Digital Economy. University of Chicago Press; 2015. https://www.nber.org/chapters/c12995.pdf

#14 [2] For more details on BMA see https://wwwlegacy.stat.washington.edu/www/research/online/hoeting1999.pdf

![BSTS mission statement

“Our approach combines three statistical methods into an

integrated system we call “Bayesian Structural Time Series”

or BSTS for short:

1) A “basic structural model” for trend and seasonality,

estimated using Kalman filters

2) Spike and slab regression for variable selection

3) Bayesian model averaging over the best performing models

for the final forecast.”[1]](https://image.slidesharecdn.com/bayesiandivination-210416125601/85/Bayesian-Divination-time-series-analysis-forecasting-with-Bayesian-Toolkits-2019-12-320.jpg?cb=1618577924)