A project report on technical analysis at share khan

Xishu Li Poster

1. Fleet Investment under Market, Regulatory and Technological Uncertainty

Xishu Li, Rob Zuidwijk, René de Koster, Rommert Dekker

Erasmus University Rotterdam

1 Introduction

Fleet investments face uncertainties in demand growth, environmental regulations that lack consistency, and new

technologies that are costly at an early stage of development.

There is often some leeway in the timing, type and amount of investment since one can "learn" and "update" knowledge over

the uncertainties as more information becomes available over time.

Besides exogenous uncertainties, the force of oligopolistic competition cannot be neglected.

Why are enormous investments common during recession in an oligopolistic market (Figure 1)?

Why is it always small firms that are facing bankruptcies (Figure 2)?

The leader firm has the incentive to invest earlier or favor large-scale investments during market depression in order to push the

follower firms to sell less and eventually cause them to go out of business. After reducing competition, the leader can

compensate the loss by earning monopoly-alike profits in the long run.

What factors influence the success of such investment strategies? How should the follower firms respond?

Figure 1 Demand and supply in the containership market Figure 2 Market consolidation

2 Research Questions

Dynamic investment problem where

1) exogenous uncertainties exist,

2) competitive interaction is considered,

3) each firm’s objective is to maximize the expected value of its

own long-term strategy, which is adapted to the evolution of the

state of the world.

What is the optimal fleet capacity investment strategy?

When should one buy new (green) ships and by how many?

Is it better to have many small investments or a few large

ones?

Does a simple description of the coupled dynamics and a

natural ordering of investment decisions exist?

3 Methodology

Markov decision process with a predetermined horizon

State space: market condition

Action space: invest, stay put or disinvest

Transition function:

competitive interaction ⇒ Stackelberg model

exogenous demand uncertainty ⇒ Brownian motion

Reward function: expected net present value

Find the optimal policy (e.g.,stay-put region St) which

prescribes the best action for each state.

Technological uncertainty can be incorporated in

investment cost functions.

Regulatory uncertainty: scenario analysis or model it as

a "surprise" event.

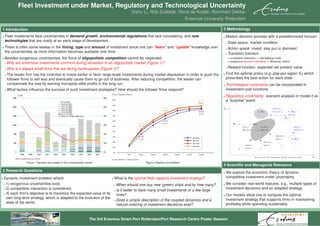

Kt−1,1

Sl,t(Sf,t)

Sf,t(K∗

l,t)

Disinvest 1

Stay put 2 Sf,t(Ka

l,t)

Sf,t(Kb

l,t)

K∗

l,t

Invest 1

Invest 2

Stay put 1

Invest 2

Invest 1

Stay put 2

Disinvest 1

Invest 2

Kl,t−1

Stay put

Stay put

Invest 1

Disinvest 2

Structure of a two-dimensional optimal investment policy

Kt−1,2

Kf,t−1

4 Scientific and Managerial Relevance

We explore the economic theory of dynamic

competitive investment under uncertainty.

We consider real-world features, e.g., multiple types of

investment decisions and an adapted strategy.

Our models allow one to compute the optimal

investment strategy that supports firms in maintaining

profitably while operating sustainably.

The 3rd Erasmus Smart Port Rotterdam/Port Research Centre Poster Session