Downloaded 58 times

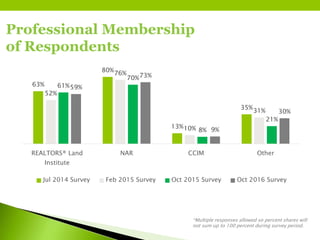

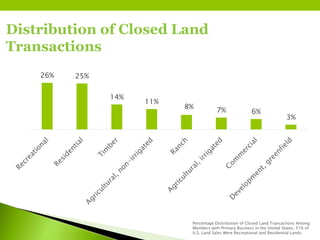

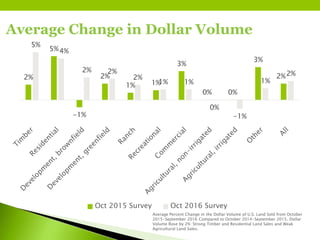

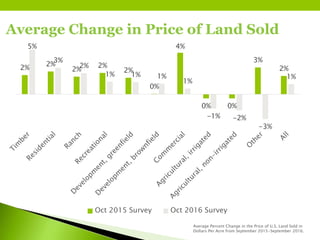

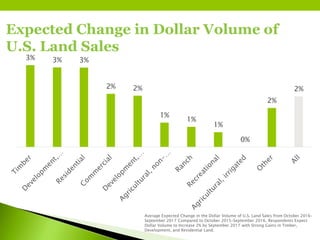

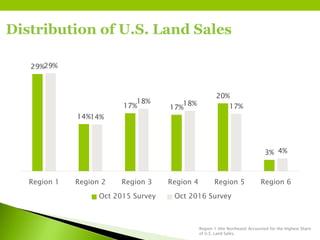

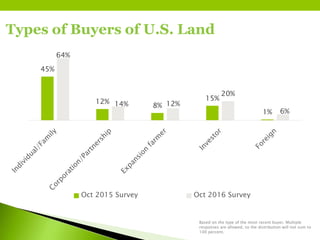

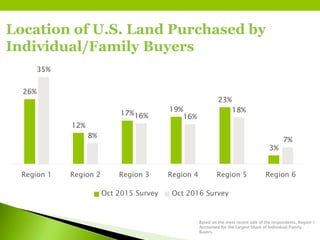

The 2017 Land Market Survey by the Realtors® Land Institute gathered insights from 614 land real estate professionals regarding transactions from October 2015 to September 2016 and projections for the following year. Key findings include a 2% increase in dollar volume of land sales, with residential and recreational lands making up 50% of transactions, and an expectation for continued growth in land sales and prices in 2017. The report serves as a benchmarking resource for industry professionals, highlighting regional trends and buyer/seller dynamics in U.S. land markets.