1. DETERMINANTS OF FINANCIAL RESPONSIBILITY:

A STUDY OF UNIVERSITY STUDENTS

*Olivia Hazel, Dr. Ali Ahmadi (Mentor), Department of Business--Marketing

Overview

Hypotheses

References

Responsibility -vs- Literacy

Acknowledgements

Financial Responsibility

The ability to make sound financial decisions

to capture the best interest of an individual.

Acquired through: living within means, budgeting, saving

more than spending, paying bills on time, & etcetera (readyratios.com)

Financial Literacy

Using knowledge on the topic of money management to

make smart financial decisions.

Acquired through educated understanding of: basic money

management concepts, investments, credit, etcetera (Hogarth, 2002)

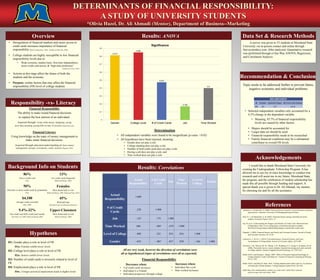

Data Set & Research MethodsResults: ANOVA

Abraham, A., & Marcolin, S. (2006). Financial literacy research: current literature and future

opportunities. Australia: University of Wollongong Research Online.

Beal, D. J., & Delpachitra, S. B. (2003). Financial literacy among Australian university

students. Economic Papers, 22(1), 15.

Fay, B. (n.d.). Understanding the Dangers and Benefits of Credit Cards. Retrieved from

CollegeXpress: http://www.collegexpress.com/articles-and-advice/student-

life/articles/living-campus/understanding-dangers-and-benefits-credit-cards/

Hogarth, J. (2002). Financial literacy and Family and Consumer Sciences. Journal of Family

and Consumer Sciences, 94, 14-28.

Letkeiwicz, J., & Fox, J. (2014). Conscientiousness, Financial Literacy, and Asset

Accumulation of Young Adults. Journal of Consumer Affairs, p274-300.

Norvilitis, J. M., Merwin, M. M., Osberg, T. M., Roehling, P. V., Young, P., & Kamas, M. M.

(2006). Personality factors, money attitudes, financial knowledge and credit card debt

in college students. Journal of Applied Social Psychology, 36, 1395-1413.

Robb, Cliff A. and Deanna L. Sharpe. 2009. "Effect of Personal Financial Knowledge on

College Students' Credit Card Behavior." Journal of Financial Counseling & Planning

20 (1): 2543.

Robb, Cliff A. and Mary B. Pinto. 2010. "College Students and Credit Card Use: An Analysis

of Financially At-Risk Students." College Student Journal 44 (4): 823-835.

Sallie Mae, How undergraduate students use credit cards: Sallie Mae's national

study of usage rates and trends, 2009

Background Info on Students

• Deregulation of financial markets and easier access to

credit cards increases importance of financial

responsibility (Beal & Delpachitra, 2003; Abraham & Marcolin, 2006).

• College students are highly susceptible to low financial

responsibility levels due to:

• Weak economy, student loans, first-time independence,

easier credit card access, & “high-time preference”

(Letkeiwicz & Fox, 2014)

• Actions at this stage affect the future of both the

students and the economy

• Purpose: isolate factors that may affect the financial

responsibility (FR) level of college students

A survey was given to 55 students at Morehead State

University via in-person contact and online through

Surveymonkey.com. After analyzed, Quantitative research

was performed through a One-Way ANOVA, Regression,

and Correlation Analysis.

I would like to thank Morehead State University for

creating the Undergraduate Fellowship Program. It has

allowed me to use my in-class knowledge to conduct true

research and will assist me in my future. Morehead State,

the program, and the celebration of student scholarship has

made this all possible through funding and support. A

special thank you is given to Dr. Ali Ahmadi, my mentor,

for choosing me and for all the assistance.

Recommendation & Conclusion

H1: Gender plays a role in level of FR

H1a: Females exhibit lower levels

H2: College level plays a role in level of FR

H2a: Seniors exhibit lower levels

H3: Number of credit cards is inversely related to level of

FR

H4: Employment plays a role in level of FR

H4a: A longer period of employment leads to higher levels

86%

Own a credit card

(Fay)

50%

Own four or more credit cards by graduation

(Fay)

$4,100

Average credit card debt

(Mae, 2009)

9.4%-32%

Pay credit card bills in full each month

(Norvilitis et al, 2006; Robb and Sharpe,2009)

13%

Use credit cards frequently

(Robb and Sharpe, 2009)

Females

More financially at risk

(Robb and Sharpe, 2009; Robb and Pinto, 2010)

45%

Work full-time

(National Center for Education Statistics)

Upper-Classmen

More financially at risk

(Robb and Sharpe, 2009)

0.813

0.849

0.473

0.169

0.4

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

Gender College Level # of Credit Cards Job Time Worked

Significance

Determination

• All independent variables were found to be insignificant (p-value >0.05)

• All hypotheses have been rejected, meaning:

• Gender does not play a role

• College standing does not play a role

• Number of held credit cards does not play a role

• Having a job does not play a role, and

• Time worked does not play a role

Actual

Responsibility

# of Credit

Cards

Job

Time

Worked

Level of

College

Gender

Actual

Responsibility

1.000

# of Credit

Cards

-.220 1.000

Job -.143 .174 1.000

Time Worked .086 -.005 -.679 1.000

Level of College -.088 .243 .018 .016 1.000

Gender -.033 -.007 .037 .078 -.166 1.000

All are very weak, however the direction of correlations were

all as hypothesized (signs of correlations were all as expected).

Financial Responsibility

Decreases when:

• # of credit cards increases

• Individual is a Female

• Individual progresses through college

Increases when:

• Individual has a job

• Time worked increases

Results: Correlations

REGRESSION

R R Square Adjusted R Square Std. Error of the Estimate

.251 .063 -.033 .66146

• Selected independent variables only accounted for a

6.3% change in the dependent variable

• Meaning, 93.7% of financial responsibility

levels are caused by other factors

• Majors should be accounted for

• Larger data set should be used

• Financial responsibility needs to be researched

• Family financial conditions may be a substantial

contributor to overall FR levels

Topic needs to be addressed further to prevent future,

negative economic and individual problems