Gpca issue 22-ethylene market overview

•

0 likes•401 views

GCC Ethylene capacity overview

Recommended

More Related Content

What's hot

What's hot (10)

Viewers also liked

Similar to Gpca issue 22-ethylene market overview

Similar to Gpca issue 22-ethylene market overview (20)

More from Nora Ismagilova

More from Nora Ismagilova (11)

Gpca issue 22-ethylene market overview

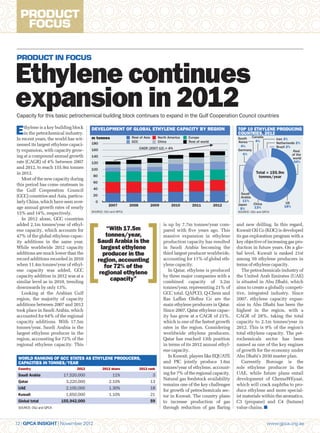

- 1. PRODUCT FOCUS PRODUCT IN FOCUS Ethylene continues expansion in 2012 Capacity for this basic petrochemical building block continues to expand in the Gulf Cooperation Council countries E thylene is a key building block in the petrochemical industry. In recent years, the world has wit- DEVELOPMENT OF GLOBAL ETHYLENE CAPACITY BY REGION m tonnes Rest of Asia North America Europe TOP 10 ETHYLENE PRODUCING COUNTRIES, 2012 South Canada Iran 3% GCC China Rest of world Korea 4% 180 Netherlands 2% nessed its largest ethylene capaci- 4% Brazil 2% CAGR (2007-12) = 4% ty expansion, with capacity grow- 160 Germany Rest 4% of the ing at a compound annual growth 140 world rate (CAGR) of 4% between 2007 120 34% and 2012, to reach 155.9m tonnes 100 in 2012. Total = 155.9m 80 tonnes/year Most of the new capacity during 60 this period has come onstream in the Gulf Cooperation Council 40 Saudi (GCC) countries and Asia, particu- 20 Arabia larly China, which have seen aver- 0 11% Japan China US 2007 2008 2009 2010 2011 2012 18% age annual growth rates of nearly 5% 13% SOURCE: OGJ and GPCA 15% and 14%, respectively. SOURCE: OGJ and GPCA In 2012 alone, GCC countries added 2.1m tonnes/year of ethyl- is up by 7.7m tonnes/year com- and new drilling. In this regard, ene capacity, which accounts for “With 17.5m pared with five years ago. This Kuwait Oil Co (KOC) is developed 47% of the global ethylene capac- tonnes/year, massive expansion in ethylene its gas exploration program with a ity additions in the same year. Saudi Arabia is the production capacity has resulted key objective of increasing gas pro- While worldwide 2012 capacity largest ethylene in Saudi Arabia becoming the duction in future years. On a glo- additions are much lower than the producer in the third largest producer worldwide, bal level, Kuwait is ranked 21st record additions recorded in 2010 region, accounting accounting for 11% of global eth- among 59 ethylene producers in when 11.4m tonnes/year of ethyl- for 72% of the ylene capacity. terms of ethylene capacity. ene capacity was added, GCC In Qatar, ethylene is produced The petrochemicals industry of capacity addition in 2012 was at a regional ethylene by three major companies with a the United Arab Emirates (UAE) similar level as in 2010, trending capacity” combined capacity of 3.2m is situated in Abu Dhabi, which downwards by only 13%. tonnes/year, representing 21% of aims to create a globally competi- Looking at the Arabian Gulf GCC total. QAPCO, Q-Chem and tive, integrated industry. Since region, the majority of capacity Ras Laffan Olefins Co are the 2007, ethylene capacity expan- additions between 2007 and 2012 main ethylene producers in Qatar. sion in Abu Dhabi has been the took place in Saudi Arabia, which Since 2007, Qatar ethylene capac- highest in the region, with a accounted for 64% of the regional ity has grow at a CAGR of 21%, CAGR of 28%, taking the total capacity additions. With 17.5m which is one of the fastest growth capacity to 2.1m tonnes/year in tonnes/year, Saudi Arabia is the rates in the region. Considering 2012. This is 9% of the region’s largest ethylene producer in the worldwide ethylene producers, total ethylene capacity. The pet- region, accounting for 72% of the Qatar has reached 13th position rochemicals sector has been regional ethylene capacity. This in terms of its 2012 annual ethyl- named as one of the key engines ene capacity. of growth for the economy under WORLD RANKING OF GCC STATES AS ETHYLENE PRODUCERS, In Kuwait, players like EQUATE Abu Dhabi’s 2030 master plan. CAPACITIES IN TONNES/YEAR and PIC jointly produce 1.6m Currently Borouge is the Country 2012 2012 share 2012 rank tonnes/year of ethylene, account- sole ethylene producer in the Saudi Arabia 17,520,000 11% 3 ing for 7% of the regional capacity. UAE, while future plans entail Natural gas feedstock availability development of ChemaWEyaat, Qatar 3,220,000 2.10% 13 remains one of the key challenges which will crack naphtha to pro- UAE 2,100,000 1.30% 18 for growth of petrochemicals sec- duce ethylene and more special- Kuwait 1,650,000 1.10% 21 tor in Kuwait. The country plans ist materials within the aromatics, Global total 155,942,000 59 to increase production of gas C3 (propane) and C4 (butane) SOURCE: OGJ and GPCA through reduction of gas flaring value chains. 12 | GPCA INSIGHT | November 2012 www.gpca.org.ae