Call Girls In Radisson Blu Hotel New Delhi Paschim Vihar ❤️8860477959 Escorts...

Activity based costing .pptx

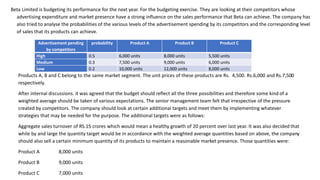

1. Beta Limited is budgeting its performance for the next year. For the budgeting exercise. They are looking at their competitors whose

advertising expenditure and market presence have a strong influence on the sales performance that Beta can achieve. The company has

also tried to analyse the probabilities of the various levels of the advertisement spending by its competitors and the corresponding level

of sales that its products can achieve.

Advertisement pending

by competitors

probability Product A Product B Product C

High 0.5 6,000 units 8,000 units 5,500 units

Medium 0.3 7,500 units 9,000 units 6,000 units

Low 0.2 10,000 units 12,000 units 8,000 units

Products A, B and C belong to the same market segment. The unit prices of these products are Rs. 4,500. Rs.6,000 and Rs.7,500

respectively.

After internal discussions. it was agreed that the budget should reflect all the three possibilities and therefore some kind of a

weighted average should be taken of various expectations. The senior management team felt that irrespective of the pressure

created by competitors. The company should look at certain additional targets and meet them by implementing whatever

strategies that may be needed for the purpose. The additional targets were as follows:

Aggregate sales turnover of RS.15 crores which would mean a healthy growth of 20 percent over last year. It was also decided that

while by and large the quantity target would be in accordance with the weighted average quantities based on above, the company

should also sell a certain minimum quantity of its products to maintain a reasonable market presence. Those quantities were:

Product A 8,000 units

Product B 9,000 units

Product C 7,000 units

2. The cost structure and other data relating to these products is as follows:

Product A Product B Product C

Material cost Rs.2,000 Rs.3,000 Rs.3,500

Other variable costs Rs.1,000 Rs.1,200 Rs.1,500

Hours utilized 50 Hours 60 Hours 70 Hours

the dealer commission per unit: Normal Rs.450 Rs.600 Rs.750

For quantities beyond the minimum

quantities mentioned above

Rs.600 Rs.800 Rs.1,000

The fixed overheads expenditure is Rs.2,00,00,000.

It is also envisaged that for meeting the sales target, a higher advertisement expenditure would be required than already included

in the fixed overheads. The additional advertisement expenditure irrespective of the quantity of additional sale over the minimum

quantities would be around Rs.14,00,000.

The capacity of the company is limited to 15,00,000 hours. It is envisaged that the same should be utilized in the best possible

manner. In the process, in case any shortfall/excess is noticed in the aggregate sales value within a margin of around 2%, the same

would be acceptable.

Based on the above data you are required to prepare a budget for Beta. Limited which would optimize the profit performance of

the company, clearly stating the following budgets:

i. Budgeted profit & loss account

ii. Sales quantity and value budget

iiL Material cost budget

iv. Overhead budget.

Please state your workings clearly in relation to arriving at the sales quantity budget in light of the various constraints stated

above.

3.

4. RG Company furnished the following data. Ascertain net income of the company under

1. Absorption Costing Method.

2. Marginal Costing Method.

Particulars Amount

(Rs.)

Direct Material cost per unit 3

Direct Labor cost per unit 5

Variable manufacturing OH cost per unit 2

Total fixed manufacturing OH per year 60,000

Number of units produced per year - 20,000 units

Closing stock - 5,000 units

Sales price per unit

-

Rs. 30

Variable selling expenses - Rs. 2 per unit

Fixed selling expenses - Rs. 40,000

5. Particulars Amount

(Rs.)

Amount

(Rs.)

Sales 4,50,000

Less Variable costs

Variable cost of goods sold

Opening inventory 0

Cost of goods produced( 20,000 units

@ Rs. 10 )

2,00,000

Cost of goods available for sale 2,00,000

Closing stock (5000 units @ Rs. 10) 50,000

Variable cost of goods sold 1,50,000

Variable selling expenses(15000 units

@ Rs. 2)

30,000

Total variable cost of good sold 1,80,000

Contribution 2,70,000

Less: Fixed costs

Manufacturing OH 60,000

Fixed selling expense 40,000 1,00,000

Net Income 1,70,000

Marginal Costing Income statement

Particulars Amount

(Rs.)

Amount

(Rs.)

Sales 4,50,000

Less Cost of goods sold

Variable cost of goods sold

Opening inventory 0

Cost of goods produced( 20,000 units

@ Rs. 13 )

2,60,000

Cost of goods available for sale 2,60,000

Closing stock (5000 units @ Rs. 13) 65,000

1,95,000 1,95,000

Gross Margin 2,55,000

Less Fixed costs 40,000

Variable selling expenses (15,000

@ 2)

30,000 70,000

Net Income 1,85,000

Income statement under Absorption Costing

Particulars Amount

(Rs)

Direct Materials 3

Direct Labor 5

Variable manufacturing cost 2

Per unit cost 10

Particulars Amount

(Rs)

Direct Materials 3

Direct Labor 5

Variable manufacturing cost 2

Fixed manufacturing cost

(60000/20000)

3

Per unit cost 13

Cost per unit under marginal costing Cost per unit under absorption costing

6.

7. Pacific, Inc. is a technology consulting firm focused on Web site development and integration of Internet

business applications. The president of the company expects to incur $775,000 of indirect costs this year,

and she expects her firm to work 5,000 direct labor hours. Pacific systems consultants provide direct labor

at a rate of $310 per hour. Clients are billed at 160% of direct labor cost. Last month, Pacific's consultants

spent 150 hours on Crockett's engagement.

Requirements

1. Compute Pacific's predetermined overhead allocation rate per direct labor hour.

2. Compute the total cost assigned to the Crockett engagement.

3. Compute the operating income from the Crockett engagement.

8. DK Ltd. manufactures and sells two products – D and K. The company has furnished the following data pertaining to cost

per unit of the products:

Particulars

D

(Rs.)

K

(Rs.)

Direct material 96 72

Direct labor (at the rate of Rs.20 per hour) 80 100

Variable production overheads at the rate of Rs.24 per hour 24 48

200 220

The fixed manufacturing overheads of the company are Rs.4,00,000 per month and the budgeted direct labor hours are

20,000 per month. The company has carried out an analysis of its production support activities and found that its fixed cost

varies in accordance with non-volume-related factors, which are given under:

Activity Cost driver

D

(No. of times)

K

(No. of times)

Total cost

(Rs.)

Setup Production run 30 20 52,000

Material handling Production run 20 30 1,20,500

Inspection Inspection 26 65 2,27,500

4,00,000

Budgeted production is 1,250 units of product D and 3,000 units of Product K. The company desires to earn a profit of

20% on total production costs.

Compute the selling prices of product K, using Activity based costing.

9. Particulars

D K Total

(Rs.) (Rs.) (Rs)

Set ups (30:20) 31,200 20,800 52,000

Materials handling (20:30) 48,200 72,300 1,20,500

Inspection (26:65) 65,000 1,62,500 2,27,500

Total 1,44,400 2,55,600 4,00,000

Budgeted units 1,250 units 3,000 units

Overheads per unit Rs.115.52 Rs.85.20

D K

Price of the products

Variable costs Rs.200.00 Rs.220.00

Fixed manufacturing costs Rs.115.52 Rs. 85.20

Rs.315.52 Rs.305.20

Profit mark-up (20%) Rs. 63.10 Rs. 61.04

Rs.378.62 Rs.366.24

10. Believing that its traditional cost system may be providing misleading information, Munnabhai Ltd. is considering to

implement Activity Based Costing (ABC) approach. It now employs a full cost system and has been applying its

manufacturing overhead on the basis of machine hours. The organization plans on using 50,000 direct labor hours and 30,000

machine hours in the coming year. The following data show the budgeted manufacturing overhead:

Activity Cost driver Budgeted

activity

Budgeted cost

(Rs.)

Material handling

Setup costs

Machine costs

Quality control

No of parts handled

No of setups

Machine hours

No of batches

60,00,000

750

30,000

500

7,20,000

3,15,000

5,40,000

2,25,000

Total overhead cost 18,00,000

Cost, sales, and production data for one of the organization’s finished products for the coming year are as follows:

Prime costs:

Direct material cost per unit Rs.4.40

Direct labor cost per unit (0.05 Direct labor

hours at the rate of Rs.15 per Direct labor hours) Re.0.75

Total prime cost Rs.5.15

Sales and production data:

Expected production and sales

Batch size

Setup

Total parts per finished unit

Machine hours required

20,000 units

5,000 units

2 per batch

5 parts

80 machine hours per batch

If the organization employs an ABC system, compute the cost per unit of the product for the coming year

11. Materials handling cost per part is Rs.0.12 (Rs. 7,20,00060,00,000),

cost per setup is Rs. 420 (Rs. 3,15,000 750),

machining cost per hour is Rs. 18 (Rs. 5,40,00030,000), and

quality cost per batch is Rs.450 (Rs.2,25,000 500).

Hence, total manufacturing overhead applied is Rs. 22,920 [(5 parts per unit x 20,000 units x Rs.0.12) + (4

batches x 2 setups per batch x Rs. 420)+ (4 batches x 80 machine hours per batch x Rs.18)+(4 batches x Rs.

450)]. The total unit cost is Rs. 6.296 or 6.30[Rs. 5.15 prime cost + (Rs.22,92020,000 units)overhead]

12.

13.

14.

15.

16.

17.

18. Triple Limited makes three types of gold watch – the Diva (D), the Classic (C) and the Poser (P). A traditional product costing system is used at present; although an

activity based costing (ABC) system is being considered. Details of the three products for a typical period are:

Direct labour costs $6 per hour and production overheads are absorbed on a machine hour basis. The overhead absorption rate for the period is $28

per machine hour.

Required:

(a) Calculate the cost per unit for each product using traditional methods, absorbing overheads on the basis of machine hours. (b) Calculate the cost per unit

for each product using ABC principles (work to two decimal places).

(c) Explain why costs per unit calculated under ABC are often very different to costs per unit calculated under more traditional methods. Use

the information from Triple Limited to illustrate.

(d) Discuss the implications of a switch to ABC on pricing and profitability.