Inflation Acceleration in 20016 Continues in 2017

•Download as PPTX, PDF•

1 like•126 views

Inflation Acceleration in 20016 Continues in 2017

Recommended

Recommended

More Related Content

More from John Rickmeier

More from John Rickmeier (19)

Recently uploaded

Recently uploaded (20)

Inflation Acceleration in 20016 Continues in 2017

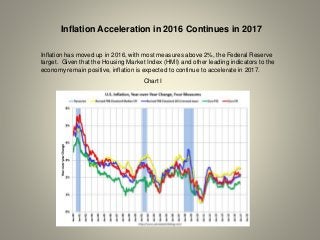

- 1. Inflation Acceleration in 2016 Continues in 2017 Inflation has moved up in 2016, with most measures above 2%, the Federal Reserve target. Given that the Housing Market Index (HMI) and other leading indicators to the economy remain positive, inflation is expected to continue to accelerate in 2017. Chart I

- 2. The chart above illustrates the year-over-year change for these four key measures of inflation. On a year-over-year basis, the median CPI rose 2.6% and the trimmed mean CPI rose 2.2% (both calculated by the Cleveland Fed based on data released in the Bureau of Labor Statistics (BLS) monthly report for December 2016). The BLS also reported for December 2016 that the CPI less food and energy rose 2.2%. Core PCE (December) increased 1.7% year-over-year. Given recent trends in inflation, a 2.5% or above forecast for core CPI inflation in 2017 seems reasonable (see Chart II). Inflationary expectations for the 30-year T-Bond yield (yield on 30-year T-Bond less yield on 30-Year Tips) of 2.07% could well increase to 2.5% or 3.0%, which lifts 30-year T-Bond yields from 3.1% to 3.5%, or even 4.0%, in 2017. Bond prices would then decline significantly on 30-year T-Bonds. Inflation-indexed 5, 10 and 30 year T-Bonds would appreciate due to a positive inflation adjustment. Chart II

- 3. How Does Higher Inflation Impact the S&P 500? The Major Bull Markets in S&P 500 Driven by a Positive Differential Between ROE less COE Analyzing the S&P 500 from 1990 to present (see Chart III), the ROE for the S&P 500 rose above its Cost of Equity (COE as calculated by IDCFP)* in June, 1993 and rose to a peak spread in March 2000. The S&P 500 rose from 452 to 1499, a 232% increase. The Housing Market Index (HMI) predicted the peak in ROE in 2000 and the decline in ROE below COE in 2001 and 2002 (see Chart IV). The next bull market in the S&P 500 began in September 2002, as the ROE again rose above COE. The S&P 500 increased from 815 in September 2002 to 1421 in March 2007, the quarter the ROE less COE spread peaked at 9.32% (see Chart III). Stocks rose 74% in this bull market. The decline in ROE from 17.3% in 2007 to a low of 1.4% in 2009 was again predicted by the HMI (see Chart IV). The current bull market was forecast by a positive ROE less COE spread in December 2009. ROE less COE spread rose from 2.73% on 12/31/09 to 9.78% on 12/31/2014. COE, meanwhile, declined from 8.07% on 12/31/09 to 4.31% on 12/31/2014. The S&P 500 rose from 1115 in December 2009 to 2059 in December 2014, an 85% bull market increase (see Chart III). However, the HMI continues to climb to new highs, indicating further economic gains and a recovery in ROE in 2017 (see Chart IV). ROE peaked at 14.8% in 2014 and receded to 13.1% estimated for the year ending December 2016. Since 2014, COE fell (due to lower interest rates) to 4.08% as of December 2016, from 4.31% in December 2014. The lower interest rates and COE allowed the S&P 500 to reach marginal new highs in 2016.

- 4. Higher inflation in 2017 and 2018 forecasts a 3.5% to 4.0% yield in 30-year T-Bonds, which, in turn, raises the COE to 5.5% to 6.0%. For the S&P 500 to maintain its current price to book value of 2.9 times, ROE must increase as fast as COE to 13.0% to 13.5%. The January 25, 2017 price for the S&P 500 of 2297 divided by the December 31, 2016 book value of 796 provides a price to book value of 2.88 times. Historic peaks in book value were normally 3 times book for the S&P 500 (see Chart V). Book value for the S&P 500 could rise to 870 in 2017 for a valuation of 2610 and, even, 1000 in 2018 for a valuation of 3000. A bear market forecast for the S&P 500 would require a peak and decline of 10 points in the price to Housing Market Index (see Chart IV). Chart III

- 5. Chart IV * COE as calculated by IDC uses general risk as demonstrated by the 30- Year T-Bond yield. A risk premium adjusts for another 50% of the 30- year T-bond and 20% of the 5-year standard deviation of the ROE to cover specific risk.

- 6. Chart V IDC Financial Publishing, Inc. normally only focuses on bank stock valuations, ROE, COE and price to book value. Given our unique “Cost of Equity” (COE), IDCFP tested the concept against the S&P 500.

- 7. John E Rickmeier, CFA President IDC Financial Publishing, Inc. 700 Walnut Ridge Drive, Suite 201 PO Box 140 Hartland WI 53029 800-525-5457 262-367-7231 262-367-6497 Fax jer@idcfp.com www.idcfp.com