PERBANYAKAN IN VITRO dan INDUKSI AKUMULASI ALKALOID pada TANAMAN JERUJU (Hydr...

project 1.2(1)

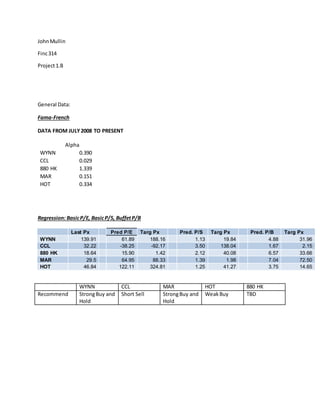

1. JohnMullin

Finc314

Project1.B

General Data:

Fama-French

DATA FROM JULY2008 TO PRESENT

Alpha

WYNN 0.390

CCL 0.029

880 HK 1.339

MAR 0.151

HOT 0.334

Regression: BasicP/E, BasicP/S, BuffetP/B

Last Px Pred P/E Targ Px Pred. P/S Targ Px Pred. P/B Targ Px

WYNN 139.91 61.89 188.16 1.13 19.84 4.88 31.96

CCL 32.22 -38.25 -92.17 3.50 138.04 1.67 2.15

880 HK 18.64 15.90 1.42 2.12 40.08 6.57 33.66

MAR 29.5 64.95 88.33 1.39 1.98 7.04 72.50

HOT 46.84 122.11 324.81 1.25 41.27 3.75 14.65

WYNN CCL MAR HOT 880 HK

Recommend StrongBuy and

Hold

Short Sell StrongBuy and

Hold

WeakBuy TBD

2. WYNN

WYNN has provenitself asa strong buy andholdstock since itsrecoveryfromthe 2008 marketcollapse,

thisstock moveswith the market. Since the recession the companyhasreboundedsteadily andhas

nearlytripledinvalue fromits1st

quarter2009 value.The upwardslopingtrendof the graphdepicts

findingsfromthe FamaFrenchregression thatWYNN hadpositive alphasince itsseverelosses fromthe

3. downturnof 2008. The P/Eregressionpredictssubstantial growthpotential fromWYNN pricingthe

securityat $50 above itscurrent value to$190. However,the P/SandP/B Buffetindicate otherwise.

These tworegressionsprice the securityatroughly%15its’ currentvalue implyingapossibledisconnect.

The book value pershare onWYNN isabout $20, $10 lessthanthe BuffetROEP/B regressiontarget

price yetthe stock is currentlytradingat $140. It is clearlyoverpricedwhensimplyconsideringthe gross

assetvalue of WYNN but froman earningsgrowthpotential standpointitisprettyattractive,given

stable or bettermarkets. WYNN’scurrentLongtermannual EPS growthrate isestimatedbetween45%

and 65% makingit the 2nd

fastestgrowingcompanyinitssector (CITE1). Itis obviousthatWYNN can

sustaingrowthinpoor to mildeconomicgrowthconditions,makingfuture prospectsof earnings

potential brightinastable andboom economy. Irecommend“BuyandHold” on WYNN,lossesonthe

stock have beenshorttermwashesandthe company’sassetswouldbe relativelyattractive fora

potential takeover. Beingthe owner/operatorof itscasinosprovidescashflow duringrecessions

withoutintensive reinvestmentandthe company shouldhave the bargainingpowerforahighvalue in

the eventof a buyout.

CCL

4. Thoughnot quite asstrong as thistime lastyear, CCL is a “BUY”, butonlyfor a limitedtime soaShort

Sell maybe the bestoption. Netincome forthe Cruise conglomerate ishighlyseasonalwithNOI

skyrocketingto4 timesoverduringthe 3rd

quarter of 2010 at $1.3 billion. Itisa companyyouwantto

keepaneye on though. CCL has lowassetturnoverforthe industryat 40% and profitshave been

decliningsince 2008. The companyisn’thighlyleveragedwhichisgood andhasmany subsidiarycruise

linesinniche marketsthatitcouldliquidate forcashinthe eventof an unlikelycrises. The regression

data on CCL isextremelyscatteredsojudgingfromahistorical dataperspectiveandgiventhe factthat

the cruise line isabove waterIwouldrecommend,BUYCCL in Septemberandsell itoff byor aroundthe

end1st quarter of 2011 or simplyshortitat thissame time. Aninvestorcouldprobablyrepeatthis

processannuallybutgiventhe lowalpha,.029, there are better“buyand hold”options.

5. MAR

MAR is one of the largestinternational hotelandluxuryreal estate conglomerates. BuffetP/B

regressionindicateanundervaluedstockasdoesthe P/Eregression. P/Sregressionpredictsand

overvaluedstockbutthatmay be attributable tolow unitprofitmarginsasa resultof a downeconomy.

MAR is currentlytradingaround$30 but has hoveredarounddouble thatforthe last10 yearswiththe

exceptionof 2007-2008. It has a decentalphaat .15 andis operatedbythe grandsonof the founder

whostartedthe companya centuryago and hasbeenmaintainingstabilityandmoderate expansion

throughthe recession. A companyof thissize has slowergrowthrates butismore stable. Pricesare

6. unlikelyskyrocketorplummetsoI wouldrecommend“weakbuyandhold”. The companycurrently

lookslike asleepinggiantandismost likelysellingata discount,greatfor highnetworthinvestors

lookingforreliablecompaniesinhibernation.

HOT

HOT is a companyyoungeryetcomparable toMAR withlessstabilityandlessmarketshare. Ithasan

alphatwice that of MAR but Price to Bookratio of half that of MAR so the returnsare offsetlessof a

7. confidence levelinthe company(ifprice tobookratioisany signof investorconfidence).Profitmargins

are far more volatile thanMARreachingnegligiblerates3timessince 1/2008 andthe weeklyPut/Call

ratiois out of control comparedto any of its top4 competitors. Regressionsrange fromgoodtobad as

the P/E regressionshowspotentialhighreturnsof anunderpricedstock,P/Bpricesitat close tomarket

but still asell andBuffetP/Bvaluesthe stockas vastlyoverratedand toorisky. I recommendthisstock

as a buy and holdwitha stoplimitsell fortworeasons. HOTis indirectcompletionwiththe much

larger,more powerful MARthatis likelytodonothingbutexpandorcomfortablysitonitslead. But,

HOT is investingheavily,upto20% of certainsubsidiariesinemergingmarketsof the Middle Eastand

China(CITE 2). Holdingthisstockcouldpayoff big inthe eventof a buyouta decade downthe line and

it’snot likelytoevaporate onamomentsnotice. “Avoidorsell forrisk-averse investors,Buy foryounger

investors”.

880 HK

8. (Graph isin$US) US $1 = HK $7.81)

Both P/SregressionsandBuffetP/Bprice 880.HK as undervaluedby HK$22 and HK$15 respectively.

Enormousprofitsare representedinthe alphaof the companywhichstandsat 1.339. 880 HK isthe

largestgrossingcasinointhe world,locatedinMacau, China. Evenwiththe potential forexcessive

returns,I wouldonlyrecommendabuytothe riskyportionof the emergingmarketssectorof a

portfolio. Lackof transparencyand the fact that the companyis still initsinfancyshouldkeepaverage

investorsgunshyon880 HK. “Buy and Holdwitha small percentage of the portfolio”andslowly

increase asthe companymaturesand produces“verified”income statements andbalance sheets.

Macau isa special economiczone withinChinawithpotential forcompanieswithhuge returnsbut

scrutinybeyondmathematicalanalysisshouldbe soughtbefore furtherinvestment. ThisisaJohn Daly

Buy.