Japan CRE Index 2013

•

1 like•610 views

The document summarizes the key findings of the Jones Lang LaSalle Japan CRE Index 2013, which compares survey responses from corporate real estate executives in Japan and globally. The index shows gaps in three areas - structure and resources, strategy, and driving force/governance. In particular, Japanese CRE teams have shorter planning horizons, less alignment with business strategy, and feel less equipped to meet increasing demands compared to global peers. The document outlines specific survey questions and responses that contribute to the scores in each area.

Recommended

Recommended

More Related Content

What's hot

What's hot (19)

Viewers also liked

Viewers also liked (17)

Similar to Japan CRE Index 2013

Similar to Japan CRE Index 2013 (20)

More from JLL

More from JLL (20)

Recently uploaded

Recently uploaded (20)

Japan CRE Index 2013

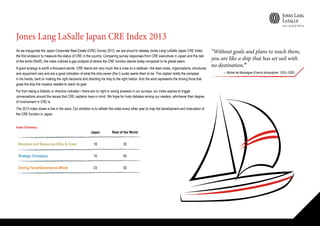

- 1. As we inaugurate the Japan Corporate Real Estate (CRE) Survey 2013, we are proud to release Jones Lang LaSalle Japan CRE Index, the first endeavor to measure the status of CRE in the country. Comparing survey responses from CRE executives in Japan and the rest of the world (RoW), the index outlines a gap analysis of where the CRE function stands today compared to its global peers. A good analogy is worth a thousand words. CRE teams are very much like a crew on a sailboat—the team sizes, organizations, structures and equipment vary and are a good indication of what the ship owner (the C-suite) wants them to be. The captain holds the compass in his hands, bent on making the right decisions and directing his ship to the right harbor. And the wind represents the driving force that gives the ship the impetus needed to reach its goal. Far from being a didactic or directive indicator—there are no right or wrong answers in our surveys, our index aspires to trigger conversations around the issues that CRE captains have in mind. We hope for lively debates among our readers, whichever their degree of involvement in CRE is. The 2013 index draws a line in the sand. Our ambition is to refresh the index every other year to map the development and maturation of the CRE function in Japan. Jones Lang LaSalle Japan CRE Index 2013 “Without goals and plans to reach them, you are like a ship that has set sail with no destination.” ― Michel de Montaigne (French philosopher, 1533–1592) Index Summary Japan Rest of the World Structure and Resources (Ship & Crew) 18 33 Strategy (Compass) 10 40 Driving Force/Governance (Wind) 23 52

- 2. Almost a third (32%) of CRE leaders reside in dedicated CRE departments, versus 39% globally. Although CRE services are delivered successfully in many companies without one, it is interesting to note that a correlation is observed between the existence of a dedicated department and the respondents’ confidence of being able to meet the demands from senior leadership. Today, the collaboration of CRE with other business functions (HR, IT and finance) has reached a shared- services level for 14% of the respondents in Japan, versus 37% in the RoW. Globally, there is a clear sense that increased collaboration is an opportunity to be in a better position to deliver on the workplace productivity agenda. Can you afford not to? Vouching for rigorous processes, internal procurement teams are increasingly actively involved in CRE decision making. This is already the case in 14% of responding companies in Japan, versus 37% elsewhere where procurement already has a stronghold. If the internal procurement teams are CRE-savvy enough and able to balance cost and value, they can add value to the process. Tip: recruit them to assist! By nature, CRE is a cost center. However, forward-looking companies also consider the value, and to some extent, the profit, which can be derived from this asset. Only 10% of respondents in Japan believe in that potential versus 17% in the RoW. Structure and Resources (Ship & Crew) Score: Japan 18/RoW 33 In other countries globally, more than half (58%) of CRE executives report to senior leadership; this is the case for 26% of them in Japan. The visibility acquired by CRE leaders on the aftermaths of the global financial crisis seems to be less of a reality in Japan. Would it make sense in Japan as well to have CRE more in evidence of the senior leadership’s radar? CRE is being asked to help increase productivity for the entire organization. Today, only 33% of CRE teams in Japan are facing high expectations to improve the productivity of people, workplaces, business and real estate assets, as compared with almost twice as many (61%) in the RoW. However, productivity improvement expectations are cascading down in Japanese companies and we believe that CRE teams should brace themselves for this demand earlier than expected. Overall, the entire spectrum of demands placed on CRE teams is broadening and intensifying, requiring action at both tactical and strategic levels. CRE is being challenged to impact and add value to a wider range of agenda items such as delivering a platform for growth in select markets, attracting and retaining talent, driving sustainability agenda, bringing more flexibility to the leasehold portfolio, creating on-demand space for the business, presenting scenarios and solutions to the business on demand and bringing innovation into the real estate function and portfolio. Faced with such amplified expectations, CRE leaders in Japan are not confident that they have what it takes to deliver. None of them feel they are “well equipped to meet all demands,” both strategic and tactical, whereas 28% of their global peers do. How equipped are you to meet these demands? Driving Force/Governance (Wind) Score: Japan 23/RoW 52 Strategy matters show Japan and the RoW at their greatest divergence. Only 4% of respondents in Japan report that CRE and business strategies are entirely aligned today, versus 54% elsewhere. We do not believe that this lack of alignment is sustainable, given the added expectations placed on CRE. Among the various processes used to select outsourced suppliers, sending an RFP to all suppliers is also a very occasional practice in Japan (4%) compared to the RoW (48%) where it is the preferred method. How long before CRE and/or procurement teams in Japan adopt this best practice? In terms of attitudes toward outsourcing, 17% in Japan still consider that outsourcing represents a strategic relationship, assessing longer-term value add with a partner (as opposed to considering outsourcing as a tactical transaction, mainly with the lowest cost supplier). This is lower than the 30% response rate elsewhere, but we believe that the sentiment is moving toward global trends. As a possible consequence, planning horizons applied to CRE strategy are considerably shorter in Japan, with only 18% of respondents in Japan benefiting from a timeline of three years and above, versus 48% elsewhere. This reveals that many Japan CRE leaders are reduced to line- of-sight navigation. Technology is the industry’s Achilles’ heel. CRE teams in Japan seem to be even less well equipped, with only 11 % of respondents feeling that they have everything they need to extract real estate metrics at facility and portfolio level, versus 23% in the RoW. Strategy (Compass) Score: Japan 10/RoW 40 “A ship is always safe at the shore, but that is not what it is built for.” ― Albert Einstein

- 3. Strategy Question Currently, to what extent is your CRE strategy aligned to your company’s broader business strategies/corporate goals? Answer Entirely aligned Question What best describes your organization’s policy regarding the selection of outsourced suppliers? Answer Request for Proposal (RFP) sent to all suppliers Question Which of the following statements best corresponds to your current attitudes toward outsourcing? Answer Outsourcing represents a strategic relationship where I assess longer-term value add with a partner Question What planning horizon do you apply to your CRE strategy? Answer Three years or longer Question How would you rate your current ability to extract real estate metrics (i.e., space held, costs and vacancy) on demand? Answer We have everything we need Driving Force/ Governance Question To what level of the organization does the global head of CRE currently report? Answer Senior leadership (i.e., C-Suite: CEO, CFO, CIO and COO) Question What productivity outcomes are your company expecting the CRE function to deliver? Answer High expectations to improve: • asset productivity (ROI and sustainability credentials); • workplace productivity (reinforce safety; reduce/avoid costs; reduce risk; and increase space utilization and flexibility); • business productivity (improve output quality, improve output quantity and increase speed to market); • people productivity (attract and retain staff; foster innovation; and enable collaboration). Question How are the demands of senior leadership on the CRE team changing in terms of the following areas? • delivering a platform for growth in select markets; • attracting and retaining talent; • transforming the quality of the portfolio/workplace (i.e., alternative workplace strategies and new workplace standards); • enhancing productivity of the real estate portfolio; • enabling remote and mobile working; • driving sustainability agenda; • bringing more flexibility to the leasehold portfolio; • creating on demand space for the business; • presenting scenarios and solutions to the business on demand; • bringing innovation into the real estate function and portfolio; • aligning CRE with business drivers and functional areas (HR, IT and finance). Answer Demand is increasing Question How equipped are you to meet these demands? Answer Well equipped to meet all demands Structure and Resources Question Within what department does the global head of CRE reside? Answer Dedicated CRE department Question Today, how would you describe the collaboration of CRE with each of the following business functions: HR, IT and finance? Answer A shared-services type of integration Question Is your internal procurement team actively involved in CRE? Answer Yes, on a permanent basis Question CRE is considered in my organization to be… Answer …more as a profit-center function Methodology The Jones Lang LaSalle Japan CRE Index is developed based on results from Jones Lang LaSalle’s Global Corporate Real Estate Survey 2013. The survey collected responses from 636 CRE executives across 39 countries, a large sample base representing a broad cross section of the corporate community, with a diverse range of sectors, locations and company sizes. For the purpose of this analysis, we analyzed the responses from the 31 Japanese companies located in Japan only. Thirteen specific questions and responses were chosen from the survey and grouped under three dimensions: structure and resources (illustrated as a ship and its crew); strategy (represented by a compass); and driving force/ governance (shown as the wind). These categories highlight some of the key components instrumental to the success of the CRE function and allow us to more clearly outline the major up-and-coming trends in our profession. For each question, the index only takes into account the benchmark answers that can be correlated to the highest degree of maturity of the CRE function, as observed globally. This is one way of pinpointing responses from Japanese companies, establishing their current position and mapping it against that of organizations in the RoW. It is by no means a recommendation or an indication of performance applicable indiscriminately to all companies. Equal weighting is used throughout the index. To determine an average percentage for each index dimension, the sum of its percentages is divided by the total number of questions. Similarly, an average percentage for the overall index is computed by averaging the percentages of the three dimensions. Jones Lang LaSalle was supported by the market survey experts of Kadence International in collecting, compiling and segmenting the research data. Visit www.jll.com/globalCREtrends to explore the global trends in more detail. See how CRE executives based in your region responded and compare your answers with the global survey results. Additional reports for specific countries and industry sectors will be posted to this site as they are released throughout the year.

- 4. www.joneslanglasalle.co.jp For more information, please contact: Research for this Index was conducted by Anne Thoraval and Henry Liao from Jones Lang LaSalle’s Corporate Research team in Asia Pacific. Toshiro Sato Head of Strategic Portfolio Services Jones Lang LaSalle, Japan toshiro.sato@ap.jll.com Risks Ahead: Global Corporate Real Estate Trends 2013 Jones Lang LaSalle’s second biennial global corporate real estate report provides powerful insights into the current condition and future direction of the corporate real estate industry. Based on the responses of more than 600 corporate real estate executives from 39 countries, we have identified five emerging global corporate real estate trends, each with its associated risks and specific actions that can be taken to manage those risks. Visit www.jll.com/globalCREtrends to explore the global trends in more detail. See how CRE executives based in your region responded and compare your answers with the global survey results. Additional reports for specific countries and industry sectors will be posted to this site as they are released throughout the year. Takahiro Takahashi Strategic Portfolio Services Jones Lang LaSalle, Japan takahiro.takahashi@ap.jll.com