Downloaded 23 times

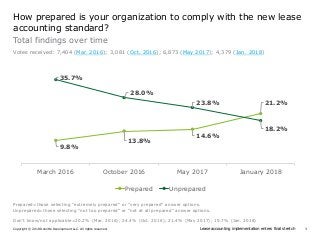

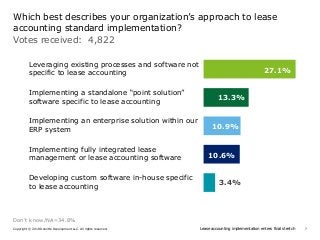

In a recent Deloitte Center for ControllershipTM poll of more than 3,850 professionals — many working in accounting (53 percent) and finance (21.5 percent) — about lease accounting implementation, just 21.2 percent of finance, accounting and other professionals say their companies are “extremely” or “very” prepared to comply with the Financial Accounting Standards Board’s (FASB) and International Accounting Standards Board’s (IASB) respective new lease accounting standards. https://www2.deloitte.com/us/en/pages/about-deloitte/articles/press-releases/few-highly-prepared-to-implement-lease-accounting-standards-as-deadline-nears.html?id=us:2sm:3ss:leases0318:awa:adv:031918:0118