Operational Risk Capital Calculation (Basel II)

•

0 likes•630 views

Brief overview of the three operational risk capital calculations allowed by Basel II and the US Fed. Also addresses the key challenges around data quality and validation.

Recommended

Recommended

More Related Content

Similar to Operational Risk Capital Calculation (Basel II)

Similar to Operational Risk Capital Calculation (Basel II) (20)

Recently uploaded

Recently uploaded (20)

Operational Risk Capital Calculation (Basel II)

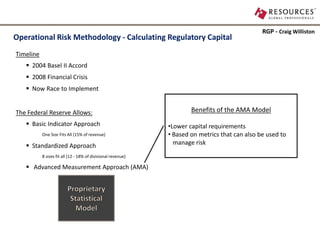

- 1. RGP - Craig Williston Operational Risk Methodology - Calculating Regulatory Capital Timeline 2004 Basel II Accord 2008 Financial Crisis Now Race to Implement The Federal Reserve Allows: Benefits of the AMA Model Basic Indicator Approach •Lower capital requirements One Size Fits All (15% of revenue) • Based on metrics that can also be used to Standardized Approach manage risk 8 sizes fit all (12 - 18% of divisional revenue) Advanced Measurement Approach (AMA)

- 2. RGP - Craig Williston Operational Risk Methodology - Calculating Regulatory Capital Process: Gather historical loss data (5+ years) Develop Key Risk Indicators (KRI) Run statistical studies to determine if the KRIs can help predict expected losses Typical Data Challenges: Additional Challenges: Finding the data Regressing the KRIs against the number of losses to assess their suitability as a predictor Reconciling loss data to books & records of losses Gaining agreement to feed the data (daily) Understanding the impact of new losses & KRIs Cleansing & enriching the data Building a process to assess model output quality in-flight Future State: Automated Feeds Automated model output quality checks Team responsible for explaining movements not just churning data manually