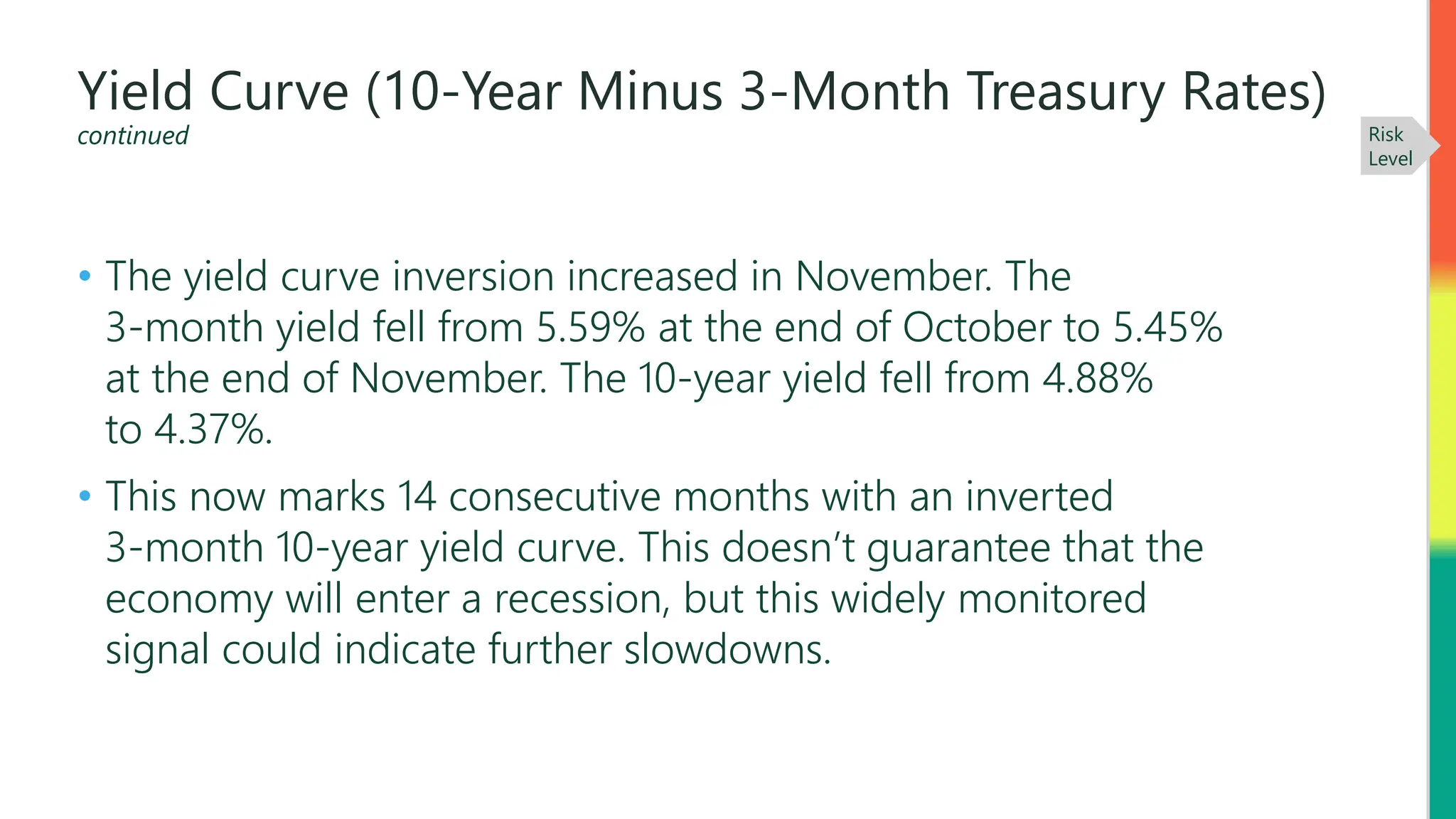

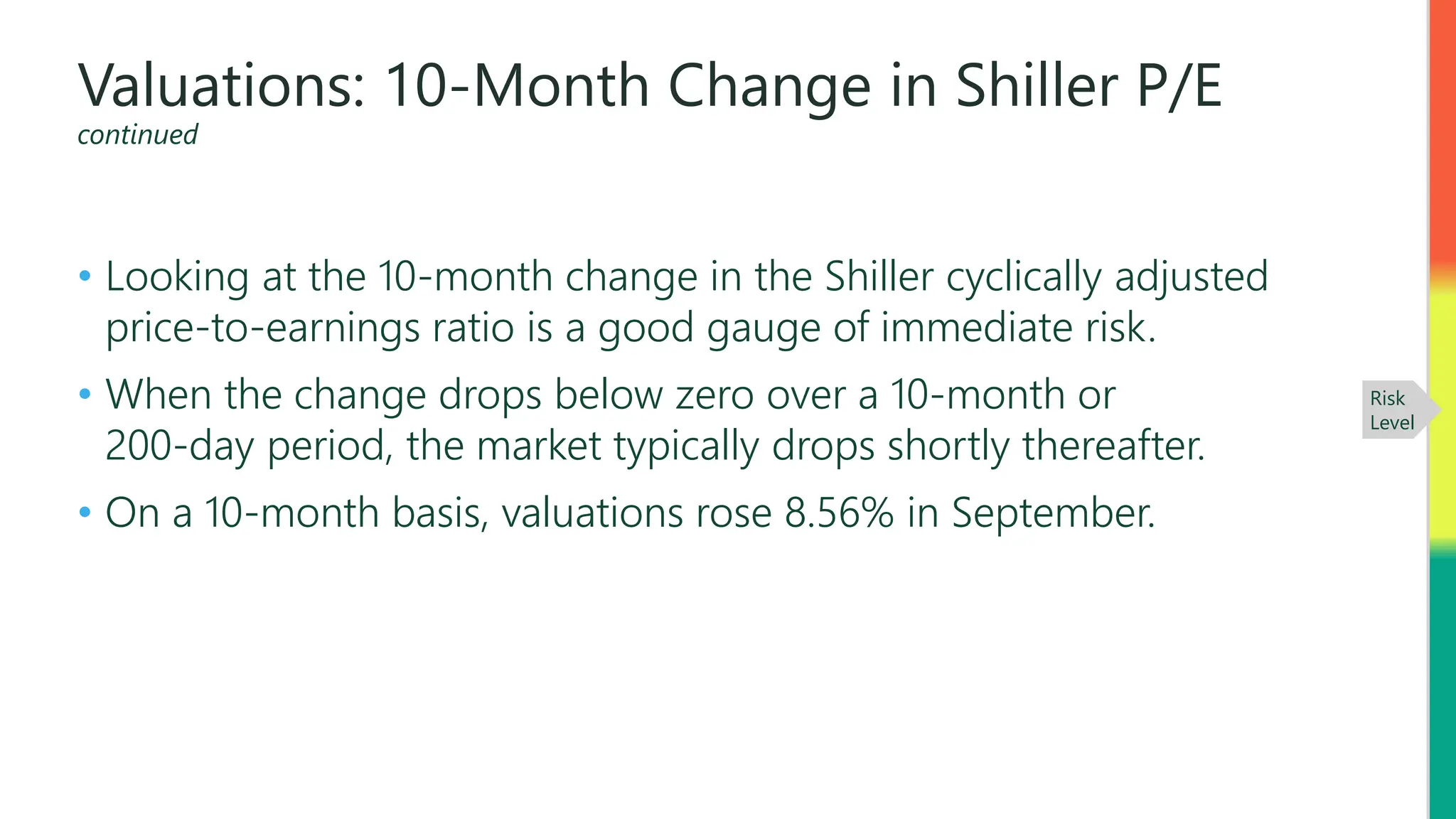

Download to read offline

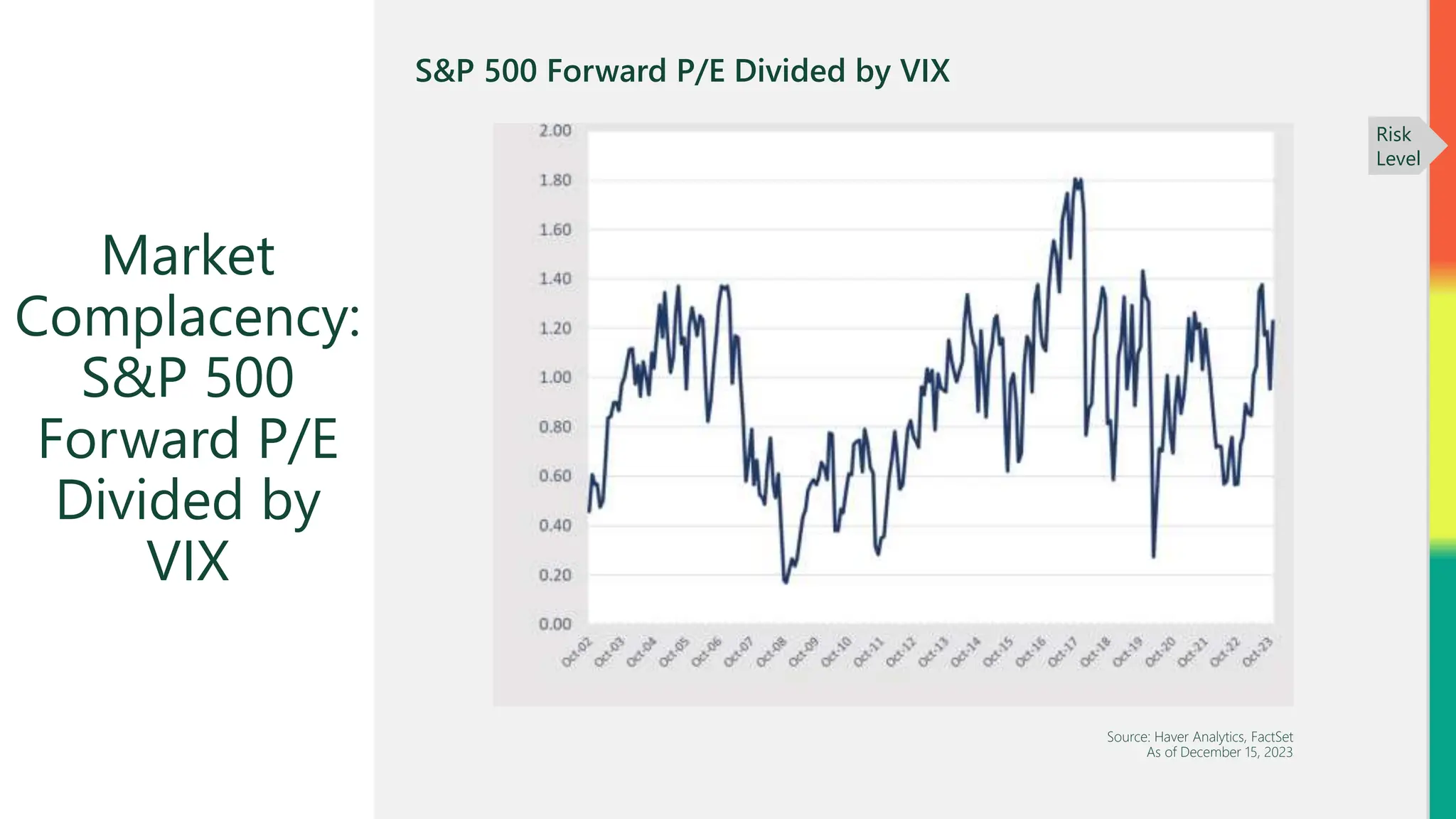

The December 2023 market risk update highlights ongoing recession risks, with historical correlations between recessions and market downturns. It notes a significant rise in margin debt and market complacency, indicating potential vulnerabilities as the economy continues to expand. The document emphasizes the importance of monitoring these indicators as we approach 2024 amidst an evolving economic landscape.

![Monthly Market Risk Update: October 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdateoctober2023-231018170735-6202cf20-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: November 2022 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdatenovember2022amrl-221117162851-44cfd6d3-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: January 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdatejanuary2024-240117184430-04ccf529-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: February 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdatefebruary2024-240214182605-2944667c-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: December 2022 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdatedecember2022amrl-221222150145-c91a7010-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: February 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdatefebruary2023amrl-230215153736-3cc82535-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: January 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdatejanuary2023rlam-230118150940-eac4e1d7-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: November 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdatenovember2023-231115143226-35f33125-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: October 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdateoct2024am-241016133219-d645282f-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: September 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdatesept2024am-240918134147-6b6cc9a3-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: May 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdatemay2023-230517141602-38346c0d-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: August 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdateaugust2024am-240821135054-bcf05ed7-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: March 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdatefebruary2024am-240320140945-833de20e-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: June 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdatejune2024am-pf2ka417-240618125718-421c825a-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: July 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdatejuly2023-230719123124-43dfed09-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: March 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdatemarch2023-230316184503-55129960-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: April 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdateapril2023-230419170710-4fe1603f-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: June 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdatejune2023-230614154355-e99841d6-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: July 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdatejuly2024am-240717142310-0da22cfe-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: October 2022 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdateoctober2022rlkfam-221019163337-f0504aff-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: April 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdateapril2024am-240424140359-342f2410-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: September 2022 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdateseptember2022-220915194606-6c06e262-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: September 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdateseptember2023-230912213959-e48e736b-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: May 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdatemay2024am-240522122148-e521348e-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: August 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdateaugust2023-230823125440-082a056b-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: January 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdatejanuary2024am-240110150920-3ad906d7-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: December 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdatedecember2023am-231213134840-5e762269-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: November 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdatenovember2023am-231108133417-ef934499-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: June 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdatejune2024am-240612135955-62fda29d-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: February 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdatefebruary2024am-240207153630-0724fa23-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: April 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdateapril2024am-240417130922-b8ca38a5-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: March 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdatemarch2024am-240313133142-2574fc7f-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: August 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdateaugust2024am-240815171155-2612b755-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: September 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdateseptember2023am-230906173934-b5fa365e-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: July 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdatejuly2024am-240712130225-147b17c8-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: October 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdateoctober2023am-231011151056-66e85714-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: September 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdateseptember2024am-240911134348-d9aeec3f-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: May 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdatemay2024am-240515130440-74d66100-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: August 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdateaugust2023am-230816184852-13dbaeea-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: October 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdateoctober2024am-241009015353-d2831b2a-thumbnail.jpg?width=640&height=640&fit=bounds)