Ladder Capital - Investor Presentation (November 2018)

ARES Analysis: Eat Cake and Have Too

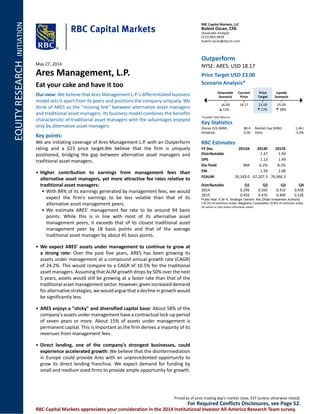

1. RBC Capital Markets, LLC

Bulent Ozcan, CFA

(Associate Analyst)

(212) 863-4818

bulent.ozcan@rbccm.com

Outperform

NYSE: ARES; USD 18.17

Price Target USD 23.00

Scenario Analysis*

Downside

Scenario

16.00

12%

Current

Price

18.17

Price

Target

23.00

27%

Upside

Scenario

25.00

38%

*Implied Total Returns

Key Statistics

Shares O/S (MM): 80.4

Dividend: 0.00

Market Cap (MM): 1,461

Yield: 0.0%

RBC Estimates

FY Dec 2013A 2014E 2015E

Distributable 1.47 1.94

DPS 1.13 1.49

Div Yield NM 6.2% 8.2%

ENI 1.59 2.06

FEAUM 59,163.0 67,207.3 76,966.3

Distributable Q1 Q2 Q3 Q4

2014 0.29E 0.35E 0.41E 0.43E

2015 0.45E 0.47E 0.49E 0.52E

Public float: 5.38 %. Strategic Owners: Abu Dhabi Investment Authority

(16.3% of common units); Alleghany Corporation (5.9% of common units)

All values in USD unless otherwise noted.

RBC Capital Markets appreciates your consideration in the 2014 Institutional Investor All-America Research Team survey.

May 27, 2014

Ares Management, L.P.

Eat your cake and have it too

Our view: We believe that Ares Management L.P.'s differentiated business

model sets it apart from its peers and positions the company uniquely. We

think of ARES as the "missing link" between alternative asset managers

and traditional asset managers. Its business model combines the benefits

characteristic of traditional asset managers with the advantages enjoyed

only by alternative asset managers

Key points:

We are initiating coverage of Ares Management L.P. with an Outperform

rating and a $23 price target.We believe that the firm is uniquely

positioned, bridging the gap between alternative asset managers and

traditional asset managers.

• Higher contribution to earnings from management fees than

alternative asset managers, yet more attractive fee rates relative to

traditional asset managers:

• With 84% of its earnings generated by management fees, we would

expect the firm's earnings to be less volatile than that of its

alternative asset management peers.

• We estimate ARES' management fee rate to be around 94 basis

points. While this is in line with most of its alternative asset

management peers, it exceeds that of its closest traditional asset

management peer by 18 basis points and that of the average

traditional asset manager by about 45 basis points.

• We expect ARES' assets under management to continue to grow at

a strong rate: Over the past five years, ARES has been growing its

assets under management at a compound annual growth rate (CAGR)

of 24.2%. This would compare to a CAGR of 10.5% for the traditional

asset managers. Assuming that AUM growth drops by 50% over the next

5 years, assets would still be growing at a faster rate than that of the

traditional asset management sector. However, given increased demand

for alternative strategies, we would argue that a decline in growth would

be significantly less.

• ARES enjoys a "sticky" and diversified capital base: About 58% of the

company's assets under management have a contractual lock-up period

of seven years or more. About 15% of assets under management is

permanent capital. This is important as the firm derives a majority of its

revenues from management fees.

• Direct lending, one of the company's strongest businesses, could

experience accelerated growth: We believe that the disintermediation

in Europe could provide Ares with an unprecedented opportunity to

grow its direct lending franchise. We expect demand for funding by

small and medium sized firms to provide ample opportunity for growth.

Priced as of prior trading day's market close, EST (unless otherwise noted).

For Required Conflicts Disclosures, see Page 52.

2. Target/Upside/Downside Scenarios

Exhibit 1: Ares Management, L.P.

8m

6m

4m

2m

5 12 19

M14

26

UPSIDE 25.00

TARGET 23.00

CURRENT 18.17

DOWNSIDE 16.00

May 2015

25

24

23

22

21

20

19

18

17

16

17 Days 02MAY14 - 26MAY14

ARES Rel. S&P 500 COMPOSITE MA 40 weeks

Source: Bloomberg and RBC Capital Markets estimates for Upside/Downside/Target

Target price/ base case

We arrive at our $23 price target using a price-to-earnings

multiple of 18.0x on next-twelve months (NTM) estimated fee-

based earnings of $0.87 per common unit. Moreover, we value

incentive income based on a price-to-earnings multiple of 9.0x

and NTM incentive income EPS of $0.76.

Our assumptions: Yield on incentive eligible assets of 4%

in Tradable Credit; multiple of invested capital of 1.5x in

private equity; yield on incentive eligible assets of 6% in Direct

Lending; yield on incentive eligible assets of 4% in Real Estate.

Upside scenario

Our upside scenario results in $0.87 in management fee

earnings per share and $0.90 in incentive income earnings per

share. We are applying a P/E multiple of 19x to management

fee earnings and 9.5x to incentive income earnings to arrive at

our $25 upside valuation.

Our assumptions: Yield on incentive eligible assets of 4.8% in

Tradable Credit; multiple of invested capital of 1.8x in private

equity; yield on incentive eligible assets of 7.2% in Direct

Lending; yield on incentive eligible assets of 4.8% in Real

Estate.

Downside scenario

Our downside scenario results in $0.87 in management fee

earnings per share and $0.49 in incentive income earnings per

share. We are applying a P/E multiple of 14x to management

fee earnings and 7x to incentive income earnings to arrive at

our $16 downside valuation.

Our assumptions: Yield on incentive eligible assets of 2.4% in

Tradable Credit; multiple of invested capital of 0.9x in private

equity; yield on incentive eligible assets of 3.6% in Direct

Lending; yield on incentive eligible assets of 2.4% in Real

Estate.

Investment summary

We think of ARES as the "missing link" between alternative

asset managers and traditional asset managers. We see upside

for the shares:

• Ares Management combines the best of two worlds: Large

contribution to earnings from management fees should

lead to steadier earnings emergence relative to other

alternative asset managers, more in line with traditional

asset managers. At the same time, effective fee rates are

twice that of the average traditional asset managers.

• With 84% of its earnings generated by management fees,

we would expect the firm's earnings to be less volatile than

that of its alternative asset management peers.

• We estimate ARES' management fee rate to be around 94

basis points. While this is in line with most of its alternative

asset management peers, it exceeds that of its closest

traditional asset management peer by 18 basis points and

that of the average traditional asset manager by about 45

basis points.

• ARES enjoys a "sticky" and diversified capital base: About

58% of the company's assets under management have a

contractual lock-up period of seven years or more. About

15% of assets under management is permanent capital.

• Direct lending, one of the company's strongest businesses,

could experience accelerated growth: We believe that

the disintermediation in Europe could provide Ares with

an unprecedented opportunity to grow its direct lending

franchise. We expect demand for funding by small and

medium sized firms to provide ample opportunity for

growth.

Risks:

• A decline in Ares Capital Corporation’s (ARCC) management

fees could adversely impact ARES' earnings. These make up

42% of ARES' total management fees as of 2013.

• Changes in interest rates could lead to an earnings shortfall.

The Tradable Credit Business seems most sensitive to

interest rate changes.

• Low liquidity and small float. We expect the average daily

volume to settle in the 300,000 to 400,000 range, on

average. Public float is only about 5.4%.

• Overhang due to ownership by strategic investors. While

we do not know whether Abu Dhabi Investment Authority

(ADIA) and Alleghany Corporation will sell their common

units, investors could be concerned as these entities own

22.25% of the common units.

• Poor performance by ARES’ funds and adverse capital

market & economic conditions could lead to a shortfall in

distributable earnings and impact the firm’s ability to raise

capital for future funds.

Ares Management, L.P.

May 27, 2014 Bulent Ozcan (212) 863-4818; bulent.ozcan@rbccm.com 2

3. Key questions

Our view

1. Can ARES deploy capital in private

equity given current valuations?

This is a legitimate concern, as EV/EBITDA deal multiples have been increasing since

2009. We believe that ARES will be able to deploy capital, but at a disciplined, slow

pace. Certainly, ARES is not facing the same headwinds as its publicly traded peers

that have a larger presence in the private equity sector. Its flagship fund (ACOF IV)

has about $4.7 billion of assets under management and about $0.95 billion of this

has been invested. It targets smaller deal sizes, committing equity in the $100

million to $400 million range. According to PitchBook, 4Q13 EV/EBITDA multiples for

deal sizes below $250 million have been around 6.5x, versus 9.8x for deal values

exceeding $250 million. We would expect ARES to deploy capital without lowering

its target return objectives. This means we do not expect ARES to raise a new

flagship fund until late 2016, at the earliest.

2. Given the company’s exposure to

credit, could increasing interest

rates impact the firm’s earnings?

We believe that there is a degree of interest rate sensitivity. About $19 billion of

assets under management is dedicated to long only credit strategies. These assets

include leveraged loan and high yield funds. Leveraged loans are priced off floating

rates, while high yield products tend to bear fixed interest rates.

However, we would expect potential outflows from high yield to be more than

offset by allocations to leveraged loan funds and alternative credit strategies. As

interest rates continue to rise, ARES could be a net beneficiary. This is because

higher interest rates could lead to higher earnings at Ares Capital Corporation

(ARCC), the firm’s business development company. About 42% of management fee

revenues are derived from ARCC.

3. ADIA and Alleghany are key

stakeholders owning over 22% of

common units. Could this be

viewed as an overhang?

We would expect Alleghany Corporation to continue to hold its investment in ARES

as the relationship is strategic in nature. As for the Abu Dhabi Investment Authority

(ADIA), we see the risk that it could sell down its holdings as ARES’ share prices

appreciates. We would characterize ADIA as a financial investor that could look for

other opportunities once it has achieved a targeted return on its investment in

ARES.

4. Could ARES’ shares become less

attractive if Congress changes tax

treatment of carried interest?

While carried interest has been an issue since 2007, it seems more likely that

Congress could move forward and change the tax treatment of carried interest. The

Senate Finance Committee released its eighth tax reform discussion paper on June

6, 2013, focusing on tax treatment of carried interest. The committee stated that tax

code reforms are needed to reduce or eliminate differences in overall tax burdens

across different types of entities, owners, and income. Higher taxes could lead to

lower payouts and dividend yields. However, any change in the tax law would come

with a multi-year transition period that would allow the firm to optimize its

corporate structure. Changing the corporate structure and reorganizing as a

corporation could increase institutional demand for ARES’ shares, potentially

offsetting the negative impact associated with higher taxes.

Ares Management, L.P.

May 27, 2014 Bulent Ozcan (212) 863-4818; bulent.ozcan@rbccm.com 3

4. Table of contents

Quick background on Ares Management, L.P. ......................................................................4

Investment thesis – Key positives.........................................................................................6

Highest contribution to earnings from management fees compared to peers should lead

to steady earnings emergence................................................................................................... 6

While a large portion of earnings are derived from recurring management fees,

resembling traditional asset managers, ARES’ effective fee rate is more attractive than

those of traditional asset managers........................................................................................... 7

Strong AUM growth ................................................................................................................... 8

Sticky and diversified capital base ............................................................................................. 9

Direct lending business could benefit from middle-market demand ...................................... 11

One of the youngest investment teams................................................................................... 12

Investment thesis – Key negatives...................................................................................... 14

ARES will not likely benefit from the current realization cycle given its low exposure to

private equity........................................................................................................................... 14

Private equity has not deployed large sums of capital ............................................................ 15

ARES does not have the same global footprint as some of its peers ....................................... 17

Having investment teams with deep knowledge about the market can help in finding

idiosyncratic investment opportunities. .................................................................................. 18

Interest rate sensitivity could be an issue in the short-term, when interest rates start

increasing – but the company could benefit from higher rates over the long-term ............... 19

Liquidity and float expected to be among the lowest in the alternative asset

management sector ................................................................................................................. 21

Overhang due to ownership by strategic investors ................................................................. 22

Potential tax rate changes could lower distributable earnings................................................ 23

Requirement to file K-1 is holding back investors.................................................................... 23

Analyzing companies within the sector is difficult given inconsistent accounting &

utilization of non-GAAP measures across the sector and the difficulty of projecting

realizations............................................................................................................................... 24

Valuation framework ......................................................................................................... 26

Risks and price target impediments ................................................................................... 27

Company description ......................................................................................................... 28

Milestones................................................................................................................................ 29

Business segments ................................................................................................................... 30

ARES publicly traded funds ...................................................................................................... 41

Management team............................................................................................................. 49

Ares Management, L.P.

May 27, 2014 Bulent Ozcan (212) 863-4818; bulent.ozcan@rbccm.com 4

5. Quick background on Ares Management, L.P.

Founded in 1997, Ares Management, L.P. (ARES) focuses mainly on alternative credit-based

strategies, which include direct lending, tradable credit, and real estate activities. The

company also operates a private equity franchise. Based out of Los Angeles, ARES has more

than 15 offices in the United States, Europe and Asia. ARES provides its services to sovereign

wealth funds, endowments, foundations, government and private pension funds, investment

companies, family offices, banks, insurance companies, private corporations and a limited

number of high net-worth clients. The company manages separate client-focused fixed

income portfolios and mutual funds. ARES provides a wide array of investment strategies,

serving over 500 institutional clients directly and utilizing its publicly traded and sub-advised

funds to offer its products to a retail investor base. As of December 31, 2013, ARES had

around 700 employees including approximately 315 investment professionals, 280

operations management professionals and with the balance in administrative support. ARES’

AUM stood at US$74 billion as of December 31, 2013.

Exhibit 2: Overview of Ares Management, L.P.

Source: Company reports

On May 1, 2013, the company announced that it had completed its initial public offering of

11,363,636 common units at a public offering price of $19. The following day, common units

started trading on the New York Stock Exchange under the ticker symbol “ARES”.

Underwriters have a 30 day option to purchase an additional 1.7 million shares.

Tradable Credit Direct Lending Private Equity Real Estate

A leading participant in the

tradable, non-investment

grade corporate credit markets

One of the largest self-

originating direct lenders to

the US and European middle

markets

One of the most consistent

performing PE managers in the

US with a growing

international presence

One of the largest real estate

private equity fund managers

and a growing direct lender

Assets Under Management $28 billion $27 billion $10 billion $9 billion

Long-only credit US direct lending US/European flexible capital Real estate debt

Alternative credit European direct lending China growth capital Real estate equity

Local Market Presence US & Europe US & Europe US, Europe & China US & Europe

Investment Funds 75+ active funds 25+ active funds 5 active funds 35+ active funds

Investment Personnel ~60 professionals ~125 professionals ~45 professionals ~80 professionals

Current Portfolio 600+ companies 400+ companies 25+ companies ~300 properties

15+ year investment track

records in both bank loans and

high yield bonds

Fund offering includes the

largest business development

company (Nasdaq: ARCC)

Aggregate gross IRR of 24% on

$7 billion invested since 2003

15+ year investment track

records in US and European

real estate private equity

Top quartile rankings in several

funds across long-only and

alternative credit strategies

ARCC generated a 14%

annualized total return for its

shareholders since 2004

Top quartile rankings in 2006

and 2008 funds

In 2013, PERE ranked AREA as a

top 15 real estate manager

based on equity raised from

January 2008 to April 2013

Proprietary research on over

1,000 companies in over 30

industries

Euro team named 2010, 2011

and 2012 Specialist Lender of

the Year

Preqin voted 2008 vintage fund

a Top 10 Best Performing

Buyout Fund among 2006 -

2010 vintages

Approved as a Fannie Mae

Delegated Underwriting and

Servicing Lender

Investment Strategies

Selected Distinctions

Ares Management, L.P.

May 27, 2014 Bulent Ozcan (212) 863-4818; bulent.ozcan@rbccm.com 5

6. Investment thesis – Key positives

Highest contribution to earnings from management fees

compared to peers should lead to steady earnings emergence

One of the challenges investors and analysts following the alternative asset management

sector are facing is the difficulty forecasting earnings and dividend distributions.

Distributable earnings can move around significantly, depending on the source of earnings.

While management fee revenues provide a good source of distributable earnings for ARES’

peers, net performance fees tend to contribute a sizeable amount to total revenues and

ultimately to earnings. Alternative asset managers tend to distinguish their dividends by the

source of earnings. The term “base dividends” is used to describe dividends that can be paid

out of earnings generated from management fees, i.e., from a stable source of earnings.

These are viewed as a minimum a company can pay out. These are then paired with top up

dividends, i.e., dividends that are a function of performance fees and usually determined in

the final quarter of the fiscal year. Performance fee related earnings tend to move around

significantly.

Exhibit 3 below depicts the relationship between management fees revenue and net

performance fees. Clearly, ARES stands out as having the highest contribution of

management fee revenues to the sum of management fee revenues and net performance

fees.

Exhibit 3: A large portion of ARES revenue is from management fees

84%

69%

56% 52% 47% 47%

36%

16%

31%

44% 48% 53% 53%

64%

ARES FIG OAK BX KKR CG APO

Management Fees Performance Fees

Source: Company reports; RBC Capital Markets

The implications are important. We believe that this could reduce future earnings volatility

and provide investors with more certainty around dividend payments. Put differently, we

would describe the variable component of earnings to be the least important contributor to

ARES’ earnings. This could command a higher multiple on distributable earnings as the risk of

an earnings shortfall could be the lowest relative to its alternative asset management peers.

We believe that the lower earnings volatility should appeal to investors who have avoided

this sector due to uncertainty around dividend distributions.

Ares Management, L.P.

May 27, 2014 Bulent Ozcan (212) 863-4818; bulent.ozcan@rbccm.com 6

7. While a large portion of earnings are derived from recurring

management fees, resembling traditional asset managers, ARES’

effective fee rate is more attractive than those of traditional

asset managers

One of the appeals of ARES is that while earnings volatility could be lower than that of its

alternative asset management peers, more in line with traditional asset managers, the

effective fee rates generated are significantly higher than those of any traditional asset

managers under our coverage. Exhibit 4 below depicts this.

Exhibit 4: ARES’ management fee rate exceeds that of traditional asset managers by a wide

margin

0.94%

1.08%

0.96%0.95%0.94%

0.80%

0.69%

0.76%

0.63%

0.58%

0.51%0.48%

0.44%

0.35%

0.22%

0.15%

0.1%

0.3%

0.5%

0.7%

0.9%

1.1%

1.3%

ARES

OAK

KKR

BX

FIG

CG

APO

APAM

BEN

WDR

IVZ

TROW

EV

LM

BLK

FII

Management Fee-Rates

Source: Company reports; RBC Capital Markets

We view this as an important point. While fee rates seem to have come under pressure for

some alternative asset managers, as institutional clients negotiate for better terms in

exchange for larger allocations, fee rates have not declined to the same degree as for

traditional asset managers. This makes sense. We believe clients are still willing to pay for

good performance and won’t switch to a second tier provider to save a few basis points on

management fees.

As demand for passive strategies among retail and institutional clients increased, the need to

reduce fees became necessary in order to attract capital from investors. After all, most

traditional asset managers have not been able to beat their benchmark after considering

fund expenses. Thus, investors are increasingly reluctant to pay high fees for active

management. Exhibit 5 below shows the percentage of funds outperforming their

benchmark.

Exhibit 5: Only in 2005 and 2009 did a majority of active managers beat their benchmark

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

# of funds beating benchmark 1449 1518 1404 1572 2022 1363 2040 1838 2917 2332 1720 2736 2457

# of funds with data 2933 3089 3253 3434 3637 3921 4234 4523 4811 5031 5354 5731 5800

% of funds beating benchmark 49.4% 49.1% 43.2% 45.8% 55.6% 34.8% 48.2% 40.6% 60.6% 46.4% 32.1% 47.7% 42.4%

Source: Morningstar; RBC Capital Markets

Ares Management, L.P.

May 27, 2014 Bulent Ozcan (212) 863-4818; bulent.ozcan@rbccm.com 7

8. This trend seems to be continuing. As follows, Exhibit 6 shows more recent data and depicts

once more the percentage of funds beating their benchmark after management,

administrative and 12b-1 fees over the past 12 months.

Exhibit 6: Looking at more recent data, we are not seeing a meaningful improvement

Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13 Jan-14 Feb-14 Mar-14

# of funds beating benchmark 2348 2236 2379 2481 2572 2433 2590 2460 2467 2498 2430 2504 2432

# of funds with data 5699 5713 5723 5733 5737 5754 5768 5777 5784 5807 5810 5813 5816

% of funds beating benchmark 41.2% 39.1% 41.6% 43.3% 44.8% 42.3% 44.9% 42.6% 42.7% 43.0% 41.8% 43.1% 41.8%

Source: Morningstar; RBC Capital Markets

While it is not an easy undertaking to determine whether alternative asset managers do

indeed generate alpha, alternative products seem to meet an increasing demand for

absolute return. Allocations to alternative asset managers have increased. At the same time,

passive strategies pose little risk to alternative asset managers. Thus, we would expect fee

rates not only to continue to exceed those of traditional asset managers, but the discrepancy

in effective fee rates between traditional asset managers and alternative asset managers to

expand.

Thus, the alternative asset management business model seems to be more isolated from fee

pressure. ARES could provide an appealing opportunity to gain exposure to the space,

especially for investors who had avoided the alternative asset management companies due

to the aforementioned earnings volatility.

Strong AUM growth

Similar to other alternative asset managers, ARES has grown its assets under management at

a considerable pace since it was founded in 1997. We believe that the firm could continue to

expand its asset base at a considerable pace over the coming year.

Over the past decade, management has grown assets under management at a compound

annual growth rate (CAGR) of 30.9%. Certainly, one could argue that this is an easy

comparison as the asset base, at $5 billion, was very low to begin with. Nonetheless, the

growth generated remains impressive even over a more recent period. Were we to analyze

growth over the past five years, we would still arrive at a CAGR of 24.2%. We believe that

ARES as well as its peers have benefited from increased demand for alternative asset

strategies – and we would expect this trend to continue.

We would position ARES as the missing link between traditional asset managers and

alternative asset managers. Think of Ares Management, L.P. as a money manager that

pursues alternative strategies, yet has an earnings pattern that resembles that of a

traditional asset management company.

Exhibit 7 below shows the annual growth rate in AUM for ARES and the assets under

management of US domiciled mutual funds, closed end funds, exchange traded funds, and

unit investment trust.

Ares Management, L.P.

May 27, 2014 Bulent Ozcan (212) 863-4818; bulent.ozcan@rbccm.com 8

9. Exhibit 7: Since 2003, annual AUM growth at ARES has significantly exceeded that of

traditional asset managers

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

ARES -CAGR (30.9%) US Traditional AM-CAGR (8.1%)

Source: Company reports; Investment Company Institute; RBC Capital Markets

While ARES grew its assets under management at a CAGR of 30.9% over the past decade, US

domiciled funds generated a CAGR of 8.1% during the same period. More importantly, assets

under management have grown every year since 2003.

As mentioned, the growth rate over the past five years has been slower than over the 10-

year period. Nonetheless, even assuming that ARES would be able to grow its AUM at half

the pace it has more recently, it could still generate an annual growth rate of over 12%. One

could even argue that going public could accelerate ARES’ growth rate due to brand

recognition. Institutional investors could also allocate more capital to ARES as complying

with strict SEC guidelines on internal control could provide these investors with additional

assurance.

Sticky and diversified capital base

Most alternative asset managers are in a fortunate position in that they do not have to worry

about losing assets and having to replenish these assets on a daily basis, but can manage

their business taking a longer-term perspective. Ares Management, L.P. is no exception to

this.

As of December 31, 2013, most of ARES’ funds have a contractual lock up period of seven

years or more. We view this as important as 84% of top line is derived from management fee

revenues. This means that there is more certainty around the sustainability of distributable

earnings and dividends.

Exhibit 8 below provides a break down of total assets under management by duration.

Ares Management, L.P.

May 27, 2014 Bulent Ozcan (212) 863-4818; bulent.ozcan@rbccm.com 9

10. Exhibit 8: Almost 58% of AUM have contractual lock-up periods of seven or more years

-

58%

15%

14%

29%

22%

5%

15%

42%

0%

20%

40%

60%

80%

100%

120%

Permanent

capital

10 years or

more

7 to 9 years 3 to 6 years Fewer than 3

years

Managed

accounts

Total

Source: Company reports; RBC Capital Markets

However, we would point out that the percentage of longer duration assets could increase as

ARES raises new funds. Assuming all funds were raised today, 56% of the new capital would

have a contractual lock-up period of 10 years or more and 11% of would have a contractual

lock-up period of 7 to 9 years. This would be on top of the 15% of assets under management

currently being deployed in permanent capital vehicles. Thus, about 82 percent of the capital

raised would be invested in with a duration of 7+ years under this scenario.

As for the limited partners (LPs), ie, investors allocating capital to ARES’ funds, we would

point out that there does not seem to be a concentration risk. According to management, no

single investor accounts for more than 4% of assets under management. The top 10 LPs

account for 19% of total assets under management.

About 52% of the $74 billion in assets under management was raised relying on over 500

direct institutional relationships. Pension funds represent the largest percentage of this,

making up 19% of total assets under management. ARES is currently working with

approximately 130 pension funds. Putting it differently, the average pension fund has about

$110 million of capital allocated to ARES’ funds.

ARES’ publicly traded entities contribute 31% to total assets under management. The

investor base seems diverse, as well. The publicly traded investment vehicles, including Ares

Capital Corporation (ARCC), Ares Commercial Real Estate Corporation (ACRE), Ares Dynamic

Credit Allocation Fund (ARDC), and Ares Multi-Strategy Credit Fund Inc. (ARMF), have over

350 institutional investors and over 200,000 retail investors as their investor base.

Ares Management, L.P.

May 27, 2014 Bulent Ozcan (212) 863-4818; bulent.ozcan@rbccm.com 10

11. Exhibit 9: ARES’ investor base seems diversified, with little concentration risk

Assets under management by channel Direct Institutional investor base

37%

19%

17%

8% 8%

5%

3% 3%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Pension

Sovereign

WealthFund

Bank

Investment

Manager

Insurance

Other

Ares

Endowment/F

oundation

Source: Company reports; RBC Capital Markets

Direct lending business could benefit from middle-market

demand

One of the investment themes that we have been frequently hearing about in the alternative

asset management sector is that banks in Europe could sell distressed assets, providing

private equity investors with an opportunity to deploy large sums of capital. We have not

seen this happen so far, despite tighter regulatory regimes in Europe. Our view is that even if

some of the assets were to come to market, the opportunity might not be that attractive, as

the industry is continuing to sit on a record amount of dry powder. We would expect fierce

bidding for the assets. On top of that, there is increased competition by strategic buyers for

these assets. The bottom line is that deploying capital could be less attractive if the assets

were purchased in a competitive auction process.

However, there are very attractive opportunities to be captured as banks are retreating and

obtaining loans is a more difficult endeavor for small- and mid-sized firms. Instead of buying

assets, private equity firms could fill the void by offering services that were previously

provided by banks. The tightening of regulations and the resulting withdrawal of banks from

certain sectors or at least a reduction in lending activity could lead to a supply/demand

imbalance in credit. We believe that ARES could capitalize on this opportunity with its direct

lending business.

Small- to medium-sized companies have historically relied on their banks to provide capital

and financing. One of the consequences of Basel III and Dodd-Frank regulation has been that

banks find it increasingly expensive to extend financing due to higher capital charges. While

large companies can access capital markets by issuing debt and equity to obtain capital, small

and medium sized firms cannot do so. This is creating an imbalance between companies

seeking financing and banks willing to provide capital. Banks are less likely to extend loans as

the capital charges have increased.

Direct lending in Europe is somewhat new and an area of growth, unlike in the US. According

to Deloitte, most of the European non-bank financing deals were closed in the UK, followed

by France and Germany. We would expect this trend to accelerate and alternative lenders to

Direct Institutional

52%

Public Entities

31%

Intermediary

17%

Ares Management, L.P.

May 27, 2014 Bulent Ozcan (212) 863-4818; bulent.ozcan@rbccm.com 11

12. become a vital source of capital and financing. Likewise, South Europe could become more

attractive to alternative lenders as the economy starts to recover.

An interesting statistic provided by Deloitte shows that 34% of the deals that closed in Q4/13

was related to leveraged buy-out and only 29% related to refinancing. We would expect

refinancing transactions to increase as banks retreat and mergers and acquisitions volume

increases.

Exhibit 10: Deloitte is seeing an increase in closed direct lending transactions (number of

deals completed)

23

18

31

35

56

0

10

20

30

40

50

60

4Q12 1Q13 2Q13 3Q13 4Q13

Source: Deloitte; RBC Capital Markets

Exhibit 10 above is based on Deloitte’s alternative lender deal tracker data and shows that

the transactions with alternative lenders more than doubled since Q4/12.

ARES conducts corporate lending and asset management activities across Europe through

Ares Management Limited. The business was launched in 2007 to directly originate middle-

market credit in Western Europe. As of December 31, 2013, ARES had 29 investment

professionals managing about $5.5 billion of total assets under management. Management

disclosed that about €200 billion of un-invested private equity capital was seeking financing

in Europe. Thus, as private equity firms start deploying capital, they will need to find a source

of financing to lever-up the portfolio companies. This could provide ARES with an

opportunity to put capital to work. Furthermore, we would expect demand for credit to

increase as the economy in Europe continues to recover. Small to medium sized businesses

need to invest in growth. This could benefit ARES’ direct lending business.

One of the youngest investment teams

A topic that frequently comes up when we talk to investors is succession planning. While the

key person risk seems to be an issue in many industries, we believe that it is a particularly

important topic in the alternative asset management space. These leaders are deemed to be

one of the main reasons why limited partners entrust money managers their capital. They

are thought to play a major role in capital raising and capital deployment. While the reality

might deviate from this perception, investors in the common shares perceive this to be true

and invest accordingly. The good news for ARES is that this issue should be less prevalent

than for some of its peers, as they have one of the youngest management teams in the

sector.

Ares Management, L.P.

May 27, 2014 Bulent Ozcan (212) 863-4818; bulent.ozcan@rbccm.com 12

13. Exhibit 11: Succession planning does not seem to be immediate concern

51 yrs 52 yrs

56 yrs

65 yrs 65 yrs

70 yrs

0

10

20

30

40

50

60

70

80

FIG ARES APO BX CG KKR

Age

Source: Company reports; RBC Capital Markets

ARES’ management team’s average age is 52 years, slightly above that of Fortress Investment

Group and well ahead of that of its peers. Certainly, any of the individuals running

Blackstone, Carlyle or KKR & Co. could be on the job for another decade. They most likely

have the energy, focus, and vision to continue doing their job at the highest level for years to

come. However, despite this, key person risk remains an important concern on investors’

minds and can affect stock performance. Consequently, we believe that succession planning

should not be an issue at ARES for years to come.

Ares Management, L.P.

May 27, 2014 Bulent Ozcan (212) 863-4818; bulent.ozcan@rbccm.com 13

14. Investment thesis – Key negatives

ARES will likely not benefit from the current realization cycle

given its low exposure to private equity

As we had mentioned earlier, a large portion of revenues at ARES are generated by

management fees. In contrast, net performance fees comprised only 16% of the revenues &

net performance fees in 2013 – the lowest among its peers. While this provides significant

downside protection, it also limits earnings growth in an improving economy.

Alternative asset managers have capitalized on the current market environment and are in

the process of selling down assets, thus, generating performance fees for holders of the

common units. We believe that investors in ARES’ common shares will not be in a position to

benefit from this “harvesting cycle/realization cycle” to the same degree as investors who

own shares of its peers. As Exhibit 12 shows, ARES’ peers have a larger presence in private

equity.

Exhibit 12: Just about 12% of fee generating AUM is invested in private equity at ARES

12%

22% 27% 31%

37%

53%

88%

78% 73% 69%

63%

47%

0%

20%

40%

60%

80%

100%

120%

ARES BX APO CG FIG KKR

Private Equity AUM Other AUM

Source: Company reports; RBC Capital Markets

As for ARES’ private equity investments, we believe that these investments are not as far

along the realization cycle relative to its peers. Exhibit 13 below depicts the percentage of

private equity investments valued using market or broker quotes. In a sense, it serves as a

proxy for the maturity of private equity portfolios.

Ares Management, L.P.

May 27, 2014 Bulent Ozcan (212) 863-4818; bulent.ozcan@rbccm.com 14

15. Exhibit 13: About 11% of private equity assets are valued based on public or broker quotes

11%

21%

35%

39%

42%

56%

0%

10%

20%

30%

40%

50%

60%

ARES KKR CG FIG BX APO

Source: Company reports; RBC Capital Markets

As shown in Exhibit 13 above, only about 11% of ARES’ private equity investments are valued

using broker or public quotes. This means that the firm would have to either find a strategic

buyer to sell the assets to or enlist the portfolio companies on an exchange before it could

start selling shares. This is a lengthy process. We believe that other alternative asset

managers such as Apollo Global Management and Blackstone are ahead on the realization

cycle, as they have a larger portion of assets that is readily available for sale.

Interestingly, ARES’ largest private equity fund by invested capital, ACOF III, has deployed

about $3.7 billion of capital and it has generated realizations of around $3.5 billion. Yet,

unrealized investments in ACOF III remain around $3.2 billion. We believe that the 11%

“public marks” mentioned above are mainly the result of ACOF III not having floated its

portfolio companies, yet.

Consequently, we would expect private equity realizations to take place at a gradual rate.

Furthermore, realizations would not have the same impact on distributable earnings

compared to peers given that private equity assets represent a small portion of total assets

under management. Therefore, investors trying to capitalize on the current harvesting cycle

could be better off investing in firms that have floated a large portion of their portfolio

companies and are selling down assets opportunistically.

Private equity has not deployed large sums of capital

We would describe ARES as a strong private equity investor. Indeed, similar to Apollo Global

Management, the company has its roots in credit investing. The credit perspective, in our

view, has led to an investment philosophy at ARES that focuses on the downside risk just as

much as on the opportunity set.

Exhibit 14 below shows the asset weighted net internal rate of returns as of December 31,

2013, for the various publicly traded alternative asset managers.

Ares Management, L.P.

May 27, 2014 Bulent Ozcan (212) 863-4818; bulent.ozcan@rbccm.com 15

16. Exhibit 14: ARES’ private equity funds have been performing well, especially ACOF III

26%

20%

18% 19%

15%

5%

0%

5%

10%

15%

20%

25%

30%

Apollo Global

Management

Ares

Management

Carlyle Group KKR & Co Blackstone Group Fortress

Investment Group

Source: Company reports; RBC Capital Markets

However, we believe that the amount of capital deployed could remain low over the coming

quarters and the firm might not see the need to raise a new flagship private equity fund until

2016 – or later.

Exhibit 15 below shows that ACOF IV, a 2012 fund, has deployed merely $945 million of

capital as of the end of the year.

Exhibit 15: ACOF IV has deployed only about 20% of committed capital

PE Fund

($ in MM) Vintage Maturity Fund Size

Inception to

Date Capital

Invested

Inception to

Date

Distributions

Net Asset

Value

MOIC

Estimate

Unrealized

Investments Gross IRR Net IRR

ACOF I 2003 In Liquidation $751 $847 $1,384 $1,501 3.4x $116 21.0% 14.0%

ACOF II 2006 Harvesting 2,100 2,069.0 3,244 4,153 3.6x 909 20.0% 15.0%

ACOF III 2008 Harvesting 3,500 3,715.0 3,468 6,627 2.7x 3,159 34.0% 25.0%

ACOF IV 2012 Investing 4,700 945.0 - 984 1.0x 984 n/a n/a

ACOF Asia 2011 Investing 220 170.0 10 207 1.3x 196 n/a n/a

Total 11,271$ $7,746 $8,106 $13,472 2.8x $5,364 28.0% 20.5%

Source: Company reports; RBC Capital Markets

While we like the company’s disciplined approach to investing, we would point out that the

firm could be having a difficult time sourcing deals that fit its return objective. One could

certainly infer this based on the capital deployed in ACOF IV over the past two years. We

believe that the size of ARES’ next fund will be determined by the opportunity set. We would

not expect ARES to increase the size of its next fund significantly, unless we go through a new

economic crisis that leads to new opportunities to invest capital. However, we believe that

the opportunity set to deploy capital could grow as ARES expands its global footprint.

However, this could take some time.

Ares Management, L.P.

May 27, 2014 Bulent Ozcan (212) 863-4818; bulent.ozcan@rbccm.com 16

17. ARES does not have the same global footprint as some of its

peers

We believe that having a global footprint provides distinct advantages. Having a presence in

multiple countries could provide an edge in raising and deploying capital. Limited partners

prefer relationships with general partners that have a permanent presence in their home

market. Furthermore, while alternative asset strategies make an increasing percentage of

assets in US portfolios, there is a large growth opportunity outside of the US.

Exhibit 16 below shows the expected allocation to various alternative asset classes and is

based on a survey conducted by McKinsey in 2013 titled “The Mainstreaming of Alternative

Investments”. We believe that the results would have been similar if the survey was

conducted today. As the authors point out, growth in alternative asset classes is expected to

be broad and strong. However, there are three items we would like to point out. First,

allocations to alternative asset classes are higher in North America, and we would expect

European investors to increase their allocation to alternative asset managers. Second,

allocation in real estate is expected to increase the most in Europe. Third, this survey does

not include Asia, a rapidly growing market. A report published by Julius Baer, a wealth

manager, predicted that the high-net-worth population (cash and assets over $1 million) will

more than double in Asia, up from 1.16 million in 2010 to 2.67 million by 2015.

Exhibit 16: If the US is an indication, European investors could increase allocation to

alternative asset classes

Real EstateHedge FundsPrivate Equity

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

2009 2010 2013E 2009 2010 2013E 2009 2010 2013E

North America European Union

Source: McKinsey & Company; RBC Capital Markets

Having a broad global presence allows the firm to identify attractive investment

opportunities by utilizing expertise about the local market. One could raise the question of

whether this is indeed true, given ARES’ strong private equity fund performance despite the

lack of a global footprint. We would argue that while ARES has generated excellent returns

investing mostly in the US, we believe that this was due to a few factors. First, ARES’ most

successful fund is a 2008 vintage. ARES Management LP, with its strength in credit, was able

to deploy capital in a profitable fashion. Note that its 2003 and 2006 funds have not enjoyed

the same level of success as ACOF III. Secondly, ARES’ flagship private equity funds are

smaller than those of its publicly traded peers. The ACOF IV fund has $4.7 billion of

commitments. As a comparison, Apollo Global Management raised over $17 billion from

third parties for its new flagship fund. Having a smaller fund can provide an advantage as one

can pursue smaller targets which tend to be available at lower entry multiples.

Ares Management, L.P.

May 27, 2014 Bulent Ozcan (212) 863-4818; bulent.ozcan@rbccm.com 17

18. Third, private equity investors with a credit-oriented investment philosophy seem to have

benefited to a larger degree from the recent financial crisis.

However, we believe that having a broad network to source deals across multiple regions will

become more important as entry multiples remain high in the US. We can see the challenges

of finding attractive opportunities with the firm’s fourth fund, ACOF IV, which has deployed

less than $1 billion since it was raised in 2012. Exhibit 17 below shows that ARES has the

least number of international offices.

Exhibit 17: ARES has only nine offices outside of the US

Ares

Management

L.P.

Apollo Global

Management

Blackstone

Group

Carlyle

Group

KKR & Co Fortress

Investment

Group

a a a a a a

x x x a a x

x x x a x x

x x x a x x

a x x x x x

a a a a a a

a x a a a x

x x x a x x

x x a x x x

a a a x x a

x x x a x x

a x x x x x

x x a x a x

x a x a x x

x x x x x a

x x x a x x

x x a a x x

x x a a a x

x a a a a x

x a a a a a

a a a a a a

x x a a a x

a x x a x x

a x a a x a

x x a a a x

x x a a a a

a x a a x a

x x x a x x

x x x a x x

310 277 840 700 265 276

x No

a Yes

Various cities, USA

Sao Paulo, BR

Lima, PE

Barcelona, ES

Frankfurt, DE

Munich, DE

Dublin, IE

Luxembourg, LU

London, UK

Paris, France

Amsterdam,NL

Dusseldorf, DE

Tokyo, JP

Mumbai, IN

Singapore, SG

Hong Kong, HK

Beijing, CN

Rome, IT

Milan, IT

Istanbul, TR

Dubai, AE

Madrid, ES

Stockholm, SE

Legend

Sydney, AU

Johannesburg, ZA

Lagos, NG

Investment Professionals

Chengdu, CN

Shanghai, CN

Seoul, KR

Source: Company reports; RBC Capital Markets

Having investment teams with deep knowledge about the market can help in finding

idiosyncratic investment opportunities.

Ares Management, L.P.

May 27, 2014 Bulent Ozcan (212) 863-4818; bulent.ozcan@rbccm.com 18

19. Interest rate sensitivity could be an issue in the short-term,

when interest rates start increasing – but the company could

benefit from higher rates over the long-term

Some investors might be concerned regarding the interest rate sensitivity of Ares

Management L.P. This would appear to make sense as 87% of assets under management are

either in tradable credit, direct lending or real estate. Based on the asset mix, an investor

might conclude that Ares Management L.P’s shares could be negatively impacted as interest

rates rise.

Exhibit 18: About 87% of assets could appear to be interest rate sensitive

Tradable Credit

38%

Direct Lending

36%

Private Equity

14%

Real Estate

12%

Source: Company reports; RBC Capital Markets

The impact of changes in interest rates would be most noticeable in the Tradable Credit

Group. This business comprises $28 billion of assets under management and includes long-

only strategies such as leveraged loans and high yield, as well as alternative strategies such

as multi-strategy credit and special situations. The disclosure provided in the S-1 filing shows

that the impact of a 10% decrease in total remaining fair value of the funds’ investments

could lead to a reduction of $117 million in performance fees and a $16 million decline in

investment income. The question then becomes what could lead to a 10% decline in fair

value. The company does not provide a breakdown of the AUM in tradable credit. While

leveraged loans would be generally priced off floating rates, high yield investments would

bear fixed rates. As for alternative strategies, we would expect the pricing primarily to be

based on floating rates. Nonetheless, it is difficult to determine what could lead to a 10%

decline in the remaining fair value given current disclosures. We would need more

information on whether the investments are priced off floating rates or fixed rates. At this

point, we cannot clearly determine the interest rate sensitivity of this segment.

As for the other parts of the business, we would argue that the impact of increasing interest

rates could be manageable.

ARES operates one of the largest business development companies, which tends to borrow

short-term and invest long-term - up to 10 years. This could negatively impact earnings due

to spread compression, but we would expect the spread compression to be manageable.

Ares Capital Corporation (ARCC) is ARES’ business development company. For managing the

assets, ARES receives performance fees on top of management fees. ARES calls the

performance fees out of Ares Capital Corporation “ARCC Part I fees” and characterizes them

Ares Management, L.P.

May 27, 2014 Bulent Ozcan (212) 863-4818; bulent.ozcan@rbccm.com 19

20. as management fees due to the recurring nature of these fees. These fees are meaningful

and contributed about 21% to total management fee revenues in 2013. The ARCC Part I fees

are based on ARCC’s pre-incentive fee net operating income. ARCC disclosed in its most

recent 10Q that only $100 million of the $3 billion of debt obligations is financed through a

revolving credit facility. As for the assets, about 9% of investments at fair value bore interest

at a fixed rate. The point is that there appears to be a small mismatch between assets and

liabilities. As interest rates increase from current levels, there would be a negative impact on

ARCC’s earnings. The interest rate sensitivity provided in the 10Q shows this. If the base rate

changed by +100 bps, net income would decline by $15.1 million. However, if the base

interest rate increased further (up 200 bps), ARCC’s earnings would actually increase.

Exhibit 19: ARCC’s net income would decline initially as base rate increases

($ in million)

Interest

Income

Interest

Expense Net Income

Up 300 basis points $104.9 $3.0 $101.9

Up 200 basis points 44.6 2.0 42.6

Up 100 basis points (14.1) 1.0 (15.1)

Down 100 basis points 6.4 (0.2) 6.6

Down 200 basis points 6.4 (0.2) 6.6

Down 300 basis points 6.4 (0.2) 6.6

Source: Company reports; RBC Capital Markets

An increase in interest rates absent economic growth and strong market conditions could

negatively impact the lending business, to be sure. Thus, we would be less concerned about

an increase in interest rates if this increase is accompanied by an economic recovery.

The same is true for the real estate business. Capitalization rates are low right now. As

interest rates increase, capitalization rates could increase, as well. This could potentially

depress real estate valuations, if net operating income for the properties does not increase.

This could happen if the occupancy rate increases or if rates can be taken, i.e., rents

increased. It is difficult to assess the impact of higher rates on the investments made by the

real estate without more information. However, we would view the impact of higher interest

rates on the real estate platform as low. The company disclosed that if the fair value of its

investments dropped by 10%, performance fees could decline by $5 million and investment

income could decline by $2 million.

One could argue that interest rate sensitivity might be lower than perceived. However, it is

difficult to determine whether the concerns are overblown based on information made

available to investors.

Ares Management, L.P.

May 27, 2014 Bulent Ozcan (212) 863-4818; bulent.ozcan@rbccm.com 20

21. Liquidity and float expected to be among the lowest in the

alternative asset management sector

While we have witnessed an increase in trading volume and liquidity in the sector since we

began coverage about a year ago, it should come as no surprise that the shares of alternative

asset managers remain fairly illiquid. This is certainly impacted by the structure of the firms.

There are a large number of mutual funds that do not allow ownership of limited

partnerships. There is still a reluctance to invest in back office operations to capture

opportunities offered by the alternative asset management sector. Furhthermore, a large

portion of the companies are owned by the founding partners and company insiders. Thus,

given the low liquidity, it can take a while to build a significant ownership in an alternative

asset manager. Exhibit 20 below shows the 30-day average trading volume for various

alternative asset managers.

Exhibit 20: 30-day average volume (in millions)

6.55

3.03

2.42

1.46 1.27

0.78

0.24 0.40

0.0

2.0

4.0

6.0

8.0

BX KKR FIG OZM APO CG OAK ARES

Source: FactSet; RBC Capital Markets; average volume excludes shares traded on the day of the IPO

We estimate that average daily volume for ARES will be around 400,000 shares. We have

excluded the volume on the first day of trading for the analysis, which was around 7.7 million

on May 2, 2014.

We would expect ARES to be one of the least liquid names in the sector. There are simply not

enough shares outstanding and management retains over 70% of the ownership of the

company. We would not expect them to sell their shares in the near term, even if they could.

ARES had to reduce the offering size given the ascribed valuation. We think that

management considers the current valuation as inexpensive, which could have driven the

decision to reduce the offering size. Thus, given current volumes, it would take about 10 days

to buy 5% of the shares outstanding. In comparison, investors could buy 5% of the

outstanding shares of Blackstone in less than half that time.

Ares Management, L.P.

May 27, 2014 Bulent Ozcan (212) 863-4818; bulent.ozcan@rbccm.com 21

22. Exhibit 21: Only about 80 million of ARES shares are currently outstanding (in millions)

578.0

404.8

453.9 472.6

149.0

64.1

127.7

80.4

0.0

200.0

400.0

600.0

800.0

BX KKR FIG OZM APO CG OAK ARES

Source: FactSet; RBC Capital Markets

Consequently, investors in ARES shares should expect stock price volatility as investors build

positions or rebalance their portfolios.

Overhang due to ownership by strategic investors

There are two strategic investors in Ares Management LP – the Abu Dhabi Investment

Authority (ADIA) and Alleghany Corporation (NYSE: Y). While we view Alleghany as a long

term investor that could retain its ownership in ARES, we would expect ADIA to reduce its

exposure to ARES in the coming years.

In July 2013, Alleghany invested $250 million for a 6.25% equity ownership in ARES. In

addition, the firm committed to invest up to $1 billion of capital in various ARES investment

strategies. Alleghany provides ARES with an opportunity to expand its presence in the

insurance industry. ARES’ management indicated that it would like to enhance its

distribution channels by targeting insurance companies. We believe that this is a mutually

beneficial relationship. Alleghany has gained access to investment expertise in credit. ARES,

on the other hand, now has a partner with in-depth experience in insurance - property and

casualty and reinsurance. Thus, we would expect Alleghany to retain its ownership in ARES.

As for ADIA, we would view them as a likely seller. This sovereign wealth funds, which usually

will not make a commitment of less than $50 million, started taking minority stakes in

alternative assets managers in 2007. ADIA bought 30 million non-voting shares in Apollo

Global Management (APO) in June 2007. The investment authority sold some of its

investment in Apollo in 2013. ADIA also had equity ownership in Carlyle Group (CG), which it

exited in September 2013.

We view ADIA as a willing seller, but would expect them to retain their ownership until

valuations improve. Initially, ADIA wanted to sell its shares with Ares Management LP going

public. The initial IPO range was between $21 and $23. However, at a $19 IPO pricing, ADIA

decided against selling its shares. Should the share price move closer to the initial IPO range,

ADIA could once more become interested in monetizing its holding. As a reminder, ADIA

owns 16.3% of ARES. Depending on the exit strategy, these shares could end up as public

float. However, there is a lock up period of one year. After one year, ADIA could sell 50% of

its ownership, with the remainder becoming available for sale after the second year.

Ares Management, L.P.

May 27, 2014 Bulent Ozcan (212) 863-4818; bulent.ozcan@rbccm.com 22

23. Potential tax rate changes could lower distributable earnings

The tax treatment of carried interest has been in the spotlight for some time now. With the

need to raise tax revenues and reduce the budget deficit, we would expect this debate to

continue. This is despite the fact that as the Private Equity Growth Capital Council pointed

out, changing the tax treatment of carried interest would only pay for 3.1 hours a year in

federal government operations.

Private equity firms generate income in two ways. They receive a management fee, which is

taxed as ordinary income, and carried interest. Private equity funds receive 20% of

partnerships profit when the return exceeds a certain hurdle rate, i.e., carried interest.

Currently, carried interest qualifies to be treated as long-term capital gains.

In 2007, the Congress held hearings on this topic. The Obama Administration’s 2008 Budget

Blueprint included a sentence that carried interest should be taxed as ordinary income. In

2010, the US House of Representatives passed HR 4213, the American Jobs and Closing Tax

Loopholes Act.

While it is difficult to predict whether the tax treatment of carried interest will change and

be a part of a tax reform bill, if passed, taxing carried interest as ordinary income could have

an adverse impact on capital distributions and dividend yields as it would significantly raise

the amount of taxes owed. HR 4213 could prevent ARES from completing certain types of

internal reorganization transactions or converting to a corporation on a tax-free basis. The

proposed legislation could also increase the ordinary income portion of any gain realized

from the sale of common units.

However, there could be a multi-year transition period before capital gains can be taxed as

ordinary income. Thus, the impact of any changes would not be immediate and there could

be sufficient time to revise any tax law changes under a new administration. Furthermore, it

is difficult to predict how the company’s shares would react to any changes in the tax law.

Currently, there is a reluctance to own shares of alternative asset managers as many

institutional investors do not want to be burdened with filing K-1s, cannot own them due to

fund mandates or due to the float not being sufficient.

Alternative asset managers could reconsider their corporate structure and reorganize as a

corporation, if carried interest is taxed as ordinary income. This, in turn, could increase

demand for their shares and liquidity, helping offset some of the negative effect of having to

pay ordinary income taxes.

Requirement to file K-1 is holding back investors

As mentioned above, certain institutional investors do not want to invest in alternative asset

managers due to the requirement to file K-1s. Limited partnerships are required to issue a

Schedule K-1 to unitholders. This would require institutional investors to build out their back

office.

Each unitholder has to report the partnership’s taxable income on a K-1. A certain portion of

the income from owning the common units could have tax consequences for tax-exempt

entities if it was deemed “Unrelated Business Taxable Income” (UBTI).

The bottom line is this: Owning shares of any alternative asset manager structured as a

limited partnership can lead to incremental administrative burdens.

However, institutional investors can avoid this by entering into a total return swap/buying a

note that provides a synthetic exposure to returns. Our understanding of a TRS/note is that a

Ares Management, L.P.

May 27, 2014 Bulent Ozcan (212) 863-4818; bulent.ozcan@rbccm.com 23

24. broker would structure this such that the counterparty would receive the cash flow

associated with the underlying assets – for a fee. The broker would take care of any filing

requirements/back-office duties. This would allow institutional investors to own the

economic benefits in companies such as ARES without having to outright own the shares.

This, of course, is a very high-level description of the structure and the details would be

beyond the scope of this note. Some institutional clients are prohibited from owning a

limited partnership due to fund mandates. Owning a TRS/note would alleviate increased

administrative costs associated with owning the underlying securities outright.

Exhibit 22: Investors can gain exposure to alternative asset managers through total return

swaps

9.1% 8.9%

6.9%

6.6%

5.3%

3.6%

2.6%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

KKR FIG OZM APO BX OAK CG

Source: FactSet; RBC Capital Markets

Exhibit 22 above shows the percentage of shares outstanding owned by brokers/dealers.

Investors unable to own the shares directly can gain exposure to alternative asset managers

by entering into a total return swap (TRS) or buying a note that provides them synthetic

exposure to an alternative asset manager.

Were alternative asset managers to change their corporate structure due to a loss of tax

advantages associated with being a limited partnership, we believe that more institutional

investors could be enticed to own their shares. As mentioned previously, some institutional

investors cannot own limited partnerships due to fund mandates. Owning the shares directly

would add to liquidity, there is likely a high probability that brokers providing exposure to

limited partnerships match buy and sell orders internally before routing any trades to the

exchanges.

Analyzing companies within the sector is difficult given

inconsistent accounting & utilization of non-GAAP measures

across the sector and the difficulty of projecting realizations

We believe that the reason why alternative asset managers trade at a discount to traditional

asset managers can be explained by the complexity of the industry, lack of visibility into

earnings (realization) and the difficulty of comparing companies within the sector.

For instance, while some alternative asset managers disclose the value of accrued

performance fees on their balance sheet, others do not. Furthermore, while most companies

disclose economic net income (a non-GAAP measure of earnings power), Fortress does not.

Ares Management, L.P.

May 27, 2014 Bulent Ozcan (212) 863-4818; bulent.ozcan@rbccm.com 24

25. The reason is that economic net income (ENI) adds volatility to earnings. Fortress argues that

over time, ENI and distributable earnings will converge. ENI shows marks on portfolios,

unrealized incentive fees and carried interest as earnings, which can fluctuate from quarter

to quarter. There are other examples of non-GAAP measures being used to demonstrate

value creation. Simple exercises such as comparing capital raising activity and capital

deployment are inherently difficult because not all companies disclose these measures for all

of their business units. Moreover, it is extremely difficult to project earnings as there is very

little visibility into realizations. This leads to many surprises and misses when the companies

report earnings.

Exhibit 23 below depicts this and shows the average deviation of reported earnings versus

the mean analyst expectation on a quarterly basis. We would expect larger “misses” for

annual projections. The data below goes back to Q1/08 or latest quarter data was available.

Exhibit 23: Average earnings surprises – actual reported earnings versus estimated earnings

(%)

-17%

-459%

-11%

30% 31% 64%

-500%

-400%

-300%

-200%

-100%

0%

100%

APO BX CG OAK OZM KKR

Source: FactSet; RBC Capital Markets

Clearly, projecting next quarter’s earnings is not an easy undertaking. Yet, we believe that

the lack of transparency could lead to opportunities. We would not expect the accounting to

change, nor would we expect the alternative asset managers to agree to use common non-

GAAP measures to make their performance more comparable. Consequently, the sector as a

whole trades at a discount given the issues described above. We could see a multiple

expansion as the industry matures, investors become more comfortable with the accounting,

and alternative asset managers provide additional information that would allow an easier

comparison across the sector.

Ares Management, L.P.

May 27, 2014 Bulent Ozcan (212) 863-4818; bulent.ozcan@rbccm.com 25

26. Valuation framework

We value Ares Management, L.P. using a “one plus a half methodology”, which is a deviation

from the valuation approach we have used for traditional asset managers. Under this

method, earnings derived from fee-based earnings (asset management fees) are valued

using a peer traditional asset management multiple, while earnings attributed to incentive

income (performance fees) are valued at a 50% discount.

Management fees earned by Ares Management L.P. are higher than those earned by

traditional long-only fund managers, justifying a premium to peer P/E multiples in our view.

We are applying a 15% premium to the peer multiple to value fee-based earnings. As for

incentive income, we apply a 50% discount to the management fee earnings multiple to

value the incentive income related earnings. We believe a discount is justified as

performance fees are more volatile than fee-based earnings and difficult to project.

Our price target for Ares Management L.P. is $23. We arrive at our price target using a price-

to-earnings multiple of 18.0x on next-twelve months (NTM) estimated fee-based earnings of

$0.87 per common unit. This is consistent with the approach we have taken for alternative

asset managers. We believe that a premium to the median traditional asset management

multiple is warranted, as alternative asset managers tend to charge higher management fee

rates. Furthermore, assets tend to be stickier due to the long lock-up periods for private

equity funds. We value earnings based on management fees at $15.71.

Moreover, we value incentive income based on a price-to-earnings multiple of 9.0x and NTM

incentive income EPS of $0.76. The multiple of 9.0x represents a 50% discount to the fee-

based earnings multiple. We value earnings based on incentive income at $6.86 per common

unit. The sum of the two valuations leads us to our price target of $23 for Ares Management,

L.P.

Exhibit 24: Price target based on one-plus-a-half-methodology

Valuation

NTM Management Fee Related EPS $0.87

P/E Multiple 18.0x

Per Share $15.71

NTM Performance Related Income EPS $0.76

P/E Multiple 9.0x

Per Share $6.86

Price Target $23

Source: Company reports; RBC Capital Markets estimates

Our $23 base case scenario valuation is based on these assumptions over the next 12

months: Yield on incentive eligible assets of 4% in Tradable Credit; multiple of invested

capital of 1.5x in private equity; yield on incentive eligible assets of 6% in Direct Lending;

yield on incentive eligible assets of 4% in Real Estate.

Ares Management, L.P.

May 27, 2014 Bulent Ozcan (212) 863-4818; bulent.ozcan@rbccm.com 26

27. Risks and price target impediments

Poor performance of ARES’ funds could lead to a shortfall in distributable earnings

Ares, like other alternative asset managers, derives a portion of its earnings from

performance fees. Distributable earnings could decline if performance deteriorates.

Adverse capital market and economic conditions could impact ARES’ economic net

income

Difficult economic conditions could adversely affect the company’s results. The market value

of securities and debt instruments held by the company could decline. Furthermore,

illiquidity in the markets could adversely impact the pace of realizations. Assets under

management could decline, lowering the base upon which ARES charges management fees.

Finally, adverse markets could lead to an increase in financing costs or reduce the availability

of financial instruments used to support private equity and real estate funds.

Weak investment performance could result in declining assets under management

and impact the firm’s ability to raise capital for future funds

Weaker than expected fund performance could impact the firm's ability to raise additional

capital for follow-on funds. This could lead to lower management fees if ARES cannot

replenish the capital it returns to its limited partners.

A decline in Ares Capital Corporation’s (ARCC) management fees could adversely

impact revenues and earnings

About 42% of ARES’ management fees are derived from managing the operations of ARCC. If

ARCC’s total assets or its net investment income were to decline, the amount ARES receives

due to the investment advisory agreement it has with ARCC would decline as well.

Changes in the tax code could negatively impact the company’s share

Changes to the US federal tax law could have a negative impact on the share price. Currently,

carried interest is treated as capital gain and not ordinary income. If carried interest income

were to be treated as ordinary fee income, the company’s share price could be negatively

impacted as this would affect dividends.

Key person risk

Retention of key senior managing directors is important. A departure of key personnel and

loss of their services could have an adverse impact on the company’s ability to raise and

retain capital. Departure of the company’s senior professionals could also lead to the

departure of highly qualified employees. Several funds have “key person” provisions, which