Collaborative Robot Market by Product Type, Distribution Channel, End User 20...

Final Draft

1. North Dakota State University Student Research

This report is published for educational purposes only by students competing in the CFA Institute Research Challenge.

Graco Inc. (New York: GGG)

Recommendation: HOLD

Price Target: $67.49 High Margins

Current Price: $76.22 Market Cap: 4.53 Bil.

Sector: Industrials

Industry: Machinery

Sub-Industry: Industrial Machinery

Graco: Strong Barriers and Enterprising

Growth

We are issuing a HOLD rating on Graco with a price target of $67.49 per share based on

our discounted cash flow valuation. While our target price is below the current trading

price, a strong business model and competitive advantage make Graco an attractive

company, and since Graco trades at a high P/E compared to similar firms price seems to

be above intrinsic value but this is less likely to weaken key performance measures.

Manufacturing Premium Priced, Highly Engineered Products for

Niche Markets

Graco’s business model of targeting specialized flow control markets has yielded high

ROIC and profit margins for the firm. Focusing on these specialized markets has allowed

the firm to gain economies of scale in difficult to enter markets and charge high prices to

consumers with no feasible substitute to Graco’s highly specialized products.

Breaking the Tradeoff between Profit Margin and Asset

Turnover

Graco’s high-priced, specialized products have yielded high profit margins for the firm,

but they have also maintained uncharacteristically high asset turnover largely due to

good communication and longstanding relations with end users. This has been a

significant driver for Graco’s ROE and ROA.

Significant Barriers to Entry Matched With Cyclical Growth

Graco benefits from high barriers to entry in the markets they serve, and is diversified

across several end markets in the industrials sector. This allows investors in Graco

exposure to cyclical growth while still having relatively secure long term profit because

Graco does not operate in easily contestable markets.

Business Description

Graco manufactures equipment to pump, meter, mix, and dispense fluids and coatings,

specifically for difficult-to-handle materials with high viscosities, abrasive or corrosive

properties and multiple component materials that require precise ratio control. They serve

niche markets where they provide customers value by providing products that reduce use

of labor, materials and energy, improve quality, and achieve environmental compliance.

Drivers of growth in the Industrial Equipment segment include factory movements and

upgrades, integration of equipment with factory data and control systems, reducing

energy consumption, and material changes driving demand. In the Contractor Equipment

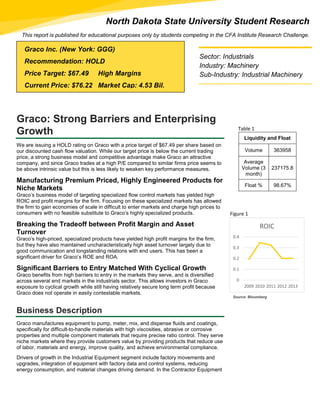

Liquidity and Float

Volume 363958

Average

Volume (3

month)

237175.8

Float % 98.67%

0

0.1

0.2

0.3

0.4

2009 2010 2011 2012 2013

ROIC

Table 1

Figure 1

Source: Bloomberg

2. 2

segment growth drivers include conversion of end users outside of North America from

manual application methods to spraying equipment, application of texture and cement

materials, entry level product and channel expansion, and expanding pavement

maintenance product line and channel. In the Lubrication segment growth drivers include

filling product lines for a single source solution and targeting competition in the industrial

lubrication market. Overall the firm has four strategies for long-term growth; investing in

new products, expending geographically, targeting new markets, and making

acquisitions.

Graco sells a low quantity of products at a high margin and thus has a high proportion of

fixed costs to variable costs. Manufacturing and engineering excellence are highly valued

at Graco so there are high costs for developing new technology and meeting specific end

user needs. To manage high fixed costs and high costs from specialization Graco

centralizes their manufacturing operations geographically, allowing for leveraging of

overhead, and leverages their product technologies for new applications and markets.

Industry Overview and Competitive Positioning

Macroeconomic Analysis

Graco operates in the industrials sector and is well diversified across end markets with

the largest percent of their revenue in 2012 coming from residential and non-residential

construction (40%), the second largest from automotive (15%), the third largest from

Industrial & machinery (13%), and the rest coming from end markets individually

representing less than 10% of revenue (Table 2). With the industrials sector being fairly

cyclical Graco is exposed to quite a bit of systematic risk, their three, five, and ten year

betas are all above one. Also with Graco’s products being the high price premium option

in nearly all their markets they are more exposed to economic downturns than the typical

industrial manufacturing firm. Overall Graco has a lot of systematic exposure, exposure

to the construction market, and to the automotive market.

Based on consensus of analyst’s forecasts we can expect growth in GDP around the

2.85% range in the US in the first half of 2015, slower growth in the Eurozone between

0.74% and 1%, and growth in the 7% range in China. Slow growth in Europe and slower

growth in China are both headwinds for Graco as well as the continued strengthening of

the dollar. But with around half of their revenue generated domestically Graco is set to

benefit from continued economic growth in the US and further recovery in the US housing

market.

Group of Peer Companies

We’ve developed a group of peer companies for Graco listed in appendix B. This group

was selected from Graco’s Bloomberg peers group and screened based on correlation of

revenue, earnings, and market capitalization, and similarities in business operations and

geographical operations.

Five Forces Analysis

Threat of New Entrants

Low: Graco benefits from barriers to entry from a high scale threshold in their markets,

high switching costs, and specialized assets.

Economies of Scale: In 2012 Graco had a total of 40,972 different SKU’s, 91% of

which sold an average between 0-1 units per day and made up nearly half of

their 2012 annual revenue (Table 3). These low units sold per day products are

typically highly specialized industrial equipment produced to meet specific

customer needs. Because these products are highly specialized and need to be

Revenue by End Market

Residential & Non-

Residential

Construction

40%

Automotive 15%

Industrial & Machinery 13%

Other 8%

Mining, Oil & Gas 6%

Public Works 5%

Vehicle Services 4%

Wood 4%

White Goods 3%

Chemical 2%

Table 2

Table 3

Average Number of

Units Sold Per Day # of SKU's

2012 Sales ($

in millions)

0 to 1 37176 (91%) $452 (49%)

2 to 5 2430 (6%) $173 (19%)

6 to 10 307 (1%) $84 (9%)

11 to 15 211 (1%) $40 (4%)

Greater than 15 548 (1%) $170 (19%)

Legacy Graco Total 40,972 $919

Plus: Gema Acquisition $93

Graco 2012 Sales $1,012

*Souce Graco Investor Presentation

3. 3

made of quality materials they are produced at a high marginal cost, and couldn’t

be produced by a competing firm because no other firm is manufacturing

products like this on the scale Graco does.

High Switching Costs: Customers in markets for specialized industrial equipment

could find less specialized substitute products that would be available to them at

a much lower price, but added costs from additional usage of labor, materials,

and energy, or from not being in compliance with environmental standards

makes switching costs in these markets very high.

Specialized Assets: Difficult-to-handle materials require equipment made of

quality materials that need more engineering expertise to produce than typical

industrial equipment. So to operate in these markets firms need very specialized

assets that could not be easily converted to other uses if the firm where to need

to make a strategic move out of the market.

Degree of Rivalry between Firms

Low: Graco experiences a weak degree of rivalry in its markets due to these markets

being concentrated, their leadership position in most of its markets, and having

differentiated products.

According to the 2002 economic census the Pump and pumping equipment

manufacturing industry had a concentration ratio of 21.7% among the four largest

firms and an HHI of 321.6 between the 50 largest firms. Within this industry

Graco targets niche markets where there are typically very few firms competing,

and Graco typically holds a leadership position in most of these markets.

Because Graco is able to serve small markets efficiently this severely dampens

rivalry between them and competing firms. Very few other companies can or do

serve these markets, and for firms that can serve them it is difficult to keep up

with Graco’s technology advances (Graco’s R&D expenditure as a percent of

sales in 2013 of 4.66% far exceeded the average of comparable firms of 2.03%).

Threat of Substitutes

Low: The threat of substitutes for Graco’s products is weak because of their

specialization.

A pump, meter, mixer, or dispenser of a viscous, abrasive, or corrosive material

could not feasibly be replaced by one manufactured for a normal liquid.

Graco’s customers on in the market for specialized industrial equipment because

they deal in products where performance and precision are critically important

and they need reliable equipment, they deal in materials that cannot be handled

by less sophisticated equipment, or need to follow precise regulatory guidelines.

Under these circumstances it is not economically feasible to substitute a Graco

product with a less specialized one.

Bargaining Power of Suppliers

Low to Moderate: Graco’s suppliers have low to moderate bargaining power mostly

driven by moderate switching costs in manufacturing equipment.

Graco gets its raw materials such as steel and aluminum from through multiple

sources so there is little concentration and commodities like these are typically

sold at low margin.

As of 2013 Graco has no unionized workers. They do have a significant amount

of their manufacturing in Minnesota so labor costs are not as low as they could

be but Graco does benefit from a loyal workforce.

There are significant switching costs for the manufacturing equipment used by

Graco, which is the main source of supplier bargaining power facing the firm.

Figure 2

4. 4

Bargaining Power of Customers

Low: Graco’s buyers have little bargaining power because of high switching costs and

fragmented buyers.

These traits are a product of the niche markets Graco operates in and the firm’s

diversification among end markets.

Only construction and automotive end markets take up a significant portion of

Graco’s revenue, and no products sold in any of these markets are critically

important to Graco; therefore no single buyer has much power.

Competitive Advantage

In summary we can see Graco has a distinct competitive advantage derived from their

business strategy of targeting niche markets where they can provide highly engineered

and specialized products. Graco has significant cost advantages over competitors

because of the efficient scale they are able to produce these specialized products at.

Because of their specialization most customers have no feasible substitute to Graco

products. For an example of the lack of viable substitutes in Graco’s markets we’ll look at

Graco’s recently acquired abrasive blasting product line EcoQuip. EcoQuip is significantly

different from other forms of blasting because it is a dry blaster that ejects 92% less

airborne dust during use. Customers have been quoted to use this product because it

could clean delicate materials that other equipment could not, it could be used for interior

blasting because of the well-contained dust, and one customer whose business was

forced to blast at night because of dust complaints was able to now blast during the day

which is obviously much more convenient. Although this is a very specific example it

conveys the unique value-added that is present in most Graco products and cannot be

replaced by less specialized substitutes.

Management & Governance

Management Experience, Compensation, and Capital Allocation

Graco’s management team has provided continued progress for the company’s

operations and investor returns. Senior management has a lengthy track record of both

company loyalty and strong performance within their respective positions with the current

team having an average of 15.6 years of experience with Graco. Executive compensation

aligns with Graco’s continued long term growth strategies as it focuses largely on stock

oriented compensation which increased 192% from 2009 to 2013. With the retirement of

Jim Graner as CFO, there is the possibility of short term turmoil in senior management.

However, with a search committee already in place and the recognition of the change to

come from management, the expected transition from Jim Graner to a new CFO appears

it will go smoothly.

Recently Graco made a deal to acquire ITW’s finishing business for $650 million. Graco

has a great track record of making quality acquisitions as part of their long term growth

strategy, but with ITW they clearly overlooked some of the regulatory risk involved with

the transaction and were forced to sell it in October 2014. Another major decision made

by Graco that differs from their competitors is in regards to their spending on research

and development. Graco currently spends twice as much on R&D as compared to their

competitors and never reduced their spending during the recession of 2008 when

comparable firms did, giving them a competitive advantage when the economy turned

around.

Quality of the Board of Directors

Graco’s board of directors is composed of the nine members and chaired by Lee Mitau.

The board is structured as a unitary board with Graco’s CEO, Patrick McHale serving on

0.000

0.100

0.200

0.300

0.400

0.500

0.600

2009 2010 2011 2012 2013

ROE

Figure 3

Source: Bloomberg

5. 5

the board. Currently Graco has 3 standing committees which are the audit, governance,

and management organization and compensation committee.

Independence: Except Graco’s CEO, Pat McHale, the other eight members are

independent.

Experience: Each board member has previous management experience; Graco’s board

members have on average 14.4 years on their board compared to Nordson’s 6.9 years.

In addition, half of Graco’s audit committee have been designated financial experts.

Resources: Graco’s board has the authority to hire external auditors through their

auditing committee without management’s approval.

Accurate Information of financial and operating position: The board establishes the

financial statement reporting procedures.

Overall, Graco complies with the standard requirements and good practices of corporate

governance.

Financial Analysis

ROE Decomposition

Historically Graco has maintained a high return on equity driven by superior operating

efficiency, asset use efficiency, and appropriate use of leverage, but has seen a decline

recently largely due to the ITW Liquid Finishing businesses sitting on their books. Graco’s

high profit margins are a product of the barriers to entry they have built in their markets.

The firm has seen steady growth in their profit margin since the 2008-2009 financial

crisis. In 2013 their profit margin was 19.1%, above pre-recession levels and well above

their long run average of 11.4%. As was stated above since 2012 there has been roughly

$420 million in short term assets on Graco’s balance sheet due to the FTC’s order for the

firm to hold the business separate until a final order had been made on the acquisition.

Earnings from the liquid finishing business came to Graco in the form of dividend

payments, so the assets were a major draw on asset turnover and brought it to a historic

low of 0.92 and 0.83 in 2012 and 2013 respectively. Historically Graco has had an

average asset turnover of 1.55 since 1988 and has done an outstanding job of

generating revenue on a slim asset base. Even at this recent deflated level Graco’s asset

turnover is about on par with comparable firms while still having a significantly higher

profit margin. This demonstrates one of Graco’s most impressive traits, how they

seemingly reject the typical tradeoff between a high profit margins and high asset

turnover.

Our outlook for Graco’s continued maximization of ROE is largely contingent on the

capital redeployment from the recent divestiture of the liquid finishing business assets.

Net proceeds from the sale are expected to be roughly $570 million. Management has

stated their priorities for the proceeds to be reducing their net debt position to nearly zero

(about $300 million in debt offset by a nearly equal amount of cash), redeploying capital

in acquisitions (will have about $800 million in capital capacity after closing), and to

continue buying back shares to current goal of less than 60 million shares outstanding.

Putting that cash to work will have an obvious benefit to shareholders, but more

importantly the firm will have to find investment opportunities that will sustain their high

margins and long run profitability.

Financial Statement Analysis

Looking more closely at asset use efficiency we can see Graco compares the best to its

peers in total asset turnover, net fixed asset turnover, and accounts receivable turnover

(Table 4). They compare worst to their peers in the inventory turnover category. Its

0.000

0.050

0.100

0.150

0.200

0.250

0.000

0.500

1.000

1.500

2.000

2.500

3.000

20092010201120122013

Decomposition A

Asset Turnover

Equity Multiplier

Profit Margin

Figure 4

0.000

0.500

1.000

1.500

2.000

2.500

3.000

0.000

0.100

0.200

0.300

0.400

0.500

0.600

0.700

0.800

2009 2010 2011 2012 2013

Decomposition B

Tax Burden

ROTA

Compound Leverage Factor

Table 4

Figure 5

Source: Bloomberg

TTM

Average of

comparable

firms (TTM)

Economic Value Added 104.06 55.35

Return on Common Equtiy 35.48% 18.71%

Return on Assets 16.04% 7.92%

Asset Turnover 0.86 0.801

Net Fixed Asset Turnover 7.68 7.54

Accounts Receivable Turnover 5.80 5.55

Inventory Turnover 3.82 4.539

Annualized Days Sales Outstanding 64.55 70.404

Source: Bloomberg

6. 6

trailing twelve month inventory turnover is lower than its 10 year average implying Graco

may have developed a habit of holding excess inventories. However, their turnover in net

fixed assets and accounts receivable are higher than comparable firms, and their

annualized days sales outstanding is significantly lower indicating Graco uses fixed

assets efficiently and collects on receivables quickly.

Graco has strong liquidity ratios (Table 5), showing they are in a very good position to

service short-term debt obligations. Graco’s current assets have been inflated over the

past three years from the Liquid Finishing business acquisition being held separately

from the firm as a short term investment. These assets are mostly offset by long-term

debt. Management has stated that they expect their cash reserves to be reduced to

roughly $300 million when the sale of the liquid finishing business has been completed,

and even at this level of cash Graco will still have a favorable amount of liquidity

compared to its peers.

Graco currently has a debt to equity ratio of 0.8 in the trailing twelve months and a

substantially higher interest coverage ratio and Altman’s Z score than comparable firms.

Historically the firm has done a very good job of using leverage appropriately to maximize

shareholder’s return while still being conservative with their capital structuring decisions

and never putting the firm in serious risk of bankruptcy.

Overall looking at the financials for Graco we can see a history of superior performance

driven by high margins that they have sustained over time (Table 6), uncommonly high

asset turnover matched with this profitability, and good capital structure decisions by

management that enhance return to shareholders while maintaining solvency and

liquidity. Looking forward we expect margins to stay high relative to peers, and continue

rising consistently with their historical rate. Graco’s asset use efficiency will be contingent

on how they can redeploy cash from the liquid finishing business divestiture.

Management targets a revenue growth rate around 9%, coming from 6% organic growth

and 3% revenue growth added on through acquisitions. The outlook to make their

organic growth goal seems favorable based on macroeconomic conditions and conditions

in key end markets. We expect the firm will be able to maintain this superior performance.

Quality of Earnings

To analyze the quality of Graco’s earnings we looked at the company’s accruals ratio

using the cash flows method and compared it to both historic figures for Graco and their

peer group. Historically Graco has a good record of low accruals ratios. There have only

been a few spikes caused by anomalies in the financing of the business, and the ratio

has consistently reverted to normal levels after. Graco’s accrual ratios have been lower

than peers on average during three of the past four years. In 2012 the firm acquiring the

Liquid Finishing Business and having to hold it separately caused their accruals ratio to

spike to 147.12%. Grouping those short term assets in with cash would drop the ratio to

51.1%, and in 2013 the ratio reverted back down to -0.17% (Table 7). Based on our

analysis of Graco’s accrual ratios we feel we can be confident in the quality of earnings

reported.

We also looked at their history of restatements of earnings, late filings over the past five

years, dividend cuts over the past five years and auditor changes in the past three years.

A history of restatements and other forms of accounting irregularities generally signal bad

quality of earnings. Graco has no restatements in the past two years, no late filings in the

past five years, no dividend cuts in the past five years, and no auditor changes in the past

three years. A good record based on these measures further improves our confidence in

the quality of Graco’s earnings.

TTM

Average of

comparable

firms (TTM)

Gross Margin 54.79% 38.63%

Operating Margin 26.08% 15.43%

Pretax Margin 27.28% 14.71%

Profit Margin 19.68% 8.69%

TTM

Average of

comparable

firms (TTM)

Current Ratio 5.28 2.291

Quick Ratio 4.16 1.449

Cash Ratio 2.82 0.628

Debt/Equity 0.80 0.56

Debt/Capital 0.44 0.34

LT Debt/Equity 0.64 0.49

LT Debt/Capital 0.44 0.31

Interest Coverage Ratio 17.28 11.85

Altman's Z 6.46 4.64

Table 5

Table 7

Peer Average

Accruals

Ratio

Graco's

Accruals

Ratio

2010 11.20% 6.45%

2011 14.51% 2.50%

2012 26.62% 147.12%

2013 20.24% -0.17%

Accruals Ratios

Table 6

7. 7

Valuation

Discounted Cash Flow Model

Through the discounted cash flow valuation method we have determined the intrinsic

value of Graco to be $67.49 per share. The discounted cash flow model is our primary

form of valuation and the sole determinant of our price target. Our forecasting method

starts with a forecasting revenue, then forecasting nearly every expense between

revenue and free cash flow to the firm as a percent of sales.

Revenue Forecast

We first estimated 2014 Q4 earnings based on our Autoregressive Integrated Moving

Average (ARIMA) model constructed using Graco’s quarterly revenue and a four quarter

lag in both the autoregressive and moving average parts of the model. Then from 2015 to

2019 our forecast is based on expansion period growth rates and a revenue shock we’ve

incorporated into the forecast to Account for the cyclical nature of Graco’s revenue. The

organic growth rates outlined in the table to the table to the right are driven by favorable

conditions in the construction, automotive, and industrials market which are poised to

benefit from a strong domestic economy, and the firm successfully continuing to develop

new products and make acquisitions that add the target 3% growth to revenue. The

revenue shock represents the economic reality of a recession happening at some point in

the near future and risk from poor economic forecasts in the Eurozone and China. Overall

this estimate yields a CAGR of 6.65% (Table 8) in revenue which is consistent with long

term averages for the firm, and we believe reflects mid-cycle growth.

Margins and Expenses Forecast

We’re forecasting a gross margin of 54.63% in 2014 ramping up to 55.83% by 2019,

which is consistent with Graco’s long term downward trend in cost of goods sold. We’re

forecasting an operating margin of 27.92% in 2014 ramping up to 31.92% in 2019, based

on research and development expenses maintaining a 5% of sales level and non-R&D

operating expenses continuing their long-term downward trend. Effective tax rate was

forecasted as 30% through 2017 then increasing to 32% in 2018 and 2019 to factor in the

uncertainty of Graco’s R&D tax credit continually being renewed every year. Capital

expenditures and changes in net working capital where forecasted as 2.5% and 2% of

sales respectively.

WACC

We’ve calculated Graco’s cost of debt to be 2.37% based on the weighted average

interest rate on Graco’s outstanding bonds, revolving credit, and notes payable to banks.

We calculated Graco’s cost of equity to be 14.12% based on the Fama-French three-

factor model, adjusting the market beta for its mean reverting property (Table 9). Graco’s

SMB and HML coefficients where both positive and statistically significant, causing our

WACC to be higher than one calculated using the CAPM. Since small cap and value

oriented firms have a history of outperforming the market, and Graco’s returns are

positively correlated to this outperformance we believe it’s appropriate to use this higher

discount rate.

Terminal Value

Terminal Value was calculated using the H-Model under the assumptions that it will take

Graco 15 years to reach its maturity period, and that cash flows will grow at 3% in the

mature growth period.

5-year CAGR From

Forecast 6.65%

Average Annual

Growth Rate Since IPO 6.61%

15-year Average

Annual Growth Rate 7.34%

10-year Average

Annual Growth Rate 8.76%

Source: Bloomberg

Wd 0.144558

Cd 0.023686

Tax Rate 0.278616

We 0.855442

Ce 0.141191

= 12.325%

WACC

Table 8

Figure 6

Table 9

8. 8

Multiples Valuation

Through a relative valuation method based on the median EV/EBITDA and P/E multiples

of comparable firms we believe Graco has a fair value of $66 per share with a feasible

range from $50 to $80 based on the highest and lowest reasonably comparable multiples

(Table 10). Because of Graco's large and diversified product line it’s a more challenging

firm to make an accurate peer group for to use for valuation. Firms we’ve chosen to

compare to Graco all operate in specialized industrial manufacturing, but vary in the end

markets they serve and therefore the risks and growth prospects of these markets. With

this in mind we believe the most comparable firm to Graco is Nordson Corp based on the

products they manufacture, their size, and geographic exposure.

Peer Comparison

Compared to Peers Graco’s EV/EBITDA (TTM) of 13.52 is higher than the median of

peers, 11.61, and Nordson, their most comparable firm, with an EV/EBITDA of 12.5.

Judging valuation by P/E ratio Graco is also trading at a comparably higher ratio than the

median of peers, Nordson, and the S&P 500.

The Market is valuing Graco at higher multiples than comparable firms.

We believe this is driven more by Graco’s higher historic ROE and ROIC than its

peer group, than by inflated forecasts of growth

Implied earnings growth rates in EBITDA and EPS by multiples are 9.59% and

9.71% respectively. These rates are fairly consistent with historic growth for

Graco, and our forecast of earnings growth.

Higher valuation than comparable firms is not favorable, but because of Graco’s

record of high ROE and ROIC that will likely be sustained this valuation seems

justified.

Multiples History

Graco’s average annual EV/EBITDA ratio over the past 10 years is 12.5, with the lowest

annual average of 7.3 occurring in 2009 and the highest of 15.8 occurring in 2013. Based

on Figure 7 Graco has traded at an average annual P/E ratio of 22.3 over the past 10

years, with the lowest average annual P/E in that period being 10.8 in 2008 and the

highest being 36.6 in 2010.

Graco’s current valuation multiples are near mid-cycle levels.

Market valuations of Graco are near historic average multiples, making it unlikely

the firm is currently overpriced.

This also implies investors may benefit from waiting for a more favorable market

valuation of Graco.

Estimated Forward Multiples

Based on our forecast of earnings Graco is currently trading at a forward EV/EBITDA

multiple of 10.6 and a forward P/E of 17.52, higher than the forward P/E of the S&P 500

of 17.2.

Benjamin Graham Valuation Methods

Our analysis included use of the modified Graham Formula, not as an indicator of

intrinsic value but as a sanity check for our discounted cash flow model and multiples

valuation. Graham proposed two formulas for valuation; the original formula in the 1962

edition of Security Analysis, and a Revised Formula in 1972. By the original formula

Graco’s value per share is $88.42, and by the revised formula its value is $156.99. By

these methods it seems our valuation of Graco is reasonable given value investing

criteria. The Piotroski F score seen in Appendix O yielded a 6 out of 9 which indicates

overall strength in various key areas. We also used the Benjamin Graham Enterprise

Figure 7

Low Median High

EV/EBITDA

(TTM) 45.81$ 64.32$ 76.22$

P/E (TTM) 23.90$ 65.54$ 76.22$

Multiples of Comparable Firms Valuation

Table 10

EPS 3.65

no-growth P/E 8.5

7-10 year earnings

growth rate 7.862

Value 88.42$

Benjamin Graham Formula

Table 11

9. 9

criteria which met 4 of the 5 criteria, another positive indicator of relative company

strength.

Investment Summary

Hold Recommendation

We give Graco a HOLD recommendation with a price target of $67.49 (Table 12) per

share based on our discounted cash flow valuation. By our judgment a buy

recommendation for a stock would require a return a potential return/loss of 15% to have

an appropriate amount of margin of safety to recommend a buy or sell. Since our price

target yields a potential loss of 11.45% for Graco it is inside our margin of safety and

warrants a hold recommendation.

Graco generates superior return on equity and capital due to its ability to operate

efficiently in niche markets.

Graco’s market position has allowed the firm to generate higher returns

historically than comparable firms. With few risks to their business model we

expect this will continue into the future

Feasible long-term growth strategy to generate sustainable growth in cash flows.

Graco’s four pronged approach to long-term growth includes new product

development, expanding geographically, entering new markets and making

acquisitions. These are solid fundamental approaches for growing the firm and,

given Graco’s market position, are very feasible.

Positioned to gain from cyclical growth in the short-term, with barriers to entry as

a long-term safety net.

Given the end markets Graco serves it is poised to gain from further recovery in

the domestic economy, while having less long-term risk given their strong

barriers to entry that not many other cyclical firms have.

Graco has many traits that make it a good business and attractive investment to

shareholders. By our methods of valuation these traits seem to be fairly reflected in its

current price, justifying our expectation of market performance and a hold

recommendation.

Recent Developments

1/2/2015: Graco announces four acquisitions in the Industrial segment including

High Pressure Equipment Company for $160 million, and three additional

purchases totaling $25 million. The company expects the deals to add $0.13 to

$0.15 to FY 2015 EPS.

10/8/2014: Graco to sell Liquid Finishing business assets for $590 million.

10/1/2014: Graco acquires U.K.-based Alco Valves Group for £72 million.

Earnings Forecast

We are forecasting EPS of $4.35 in 2015, growing to $4.84 by 2019 at a CAGR of 5.2%

over our forecast period. This forecast is driven by revenue growth assumptions which

we’ve outlined in the valuation section, gross and operating margins increasing at a rate

consistent with historic trends, the reduction of dividends after the sale of the Liquid

Finishing Business, and average annual growth historically. Our forecast is significantly

lower than 5 and 10 year average annual growth in earnings of 26.26% and 18.57%

respectively. We believe our forecast is more consistent with mid-cycle growth in

DCF 67.49$

Multiples of

Comparable Firms 66.00$

Graham Valuation 88.42$

Piotrosky's F-Score 6 of 9

Valuation Summary

Table 12

10. 10

earnings. Our forecast of 5.2% growth is lower than the average of analysts’ estimates of

9.3%.

Valuation Summary

Our primary form of valuation, which we used to calculate our price target of $67.49, was

a discounted cash flow model. We also the relative valuation method of multiples of

comparable firms to obtain a fair value estimate of $66, with a reasonable range between

$50 and $80 per share. Finally we incorporated Graham valuation methods as a way to

check if our valuation assumptions met value investing criteria.

Investment Risks

Risks to Operations

Graco’s business model is reliant on high margins derived from premium prices, because

of this they are highly sensitive to consumer demand. In this case, any lag in

technological advancement or mismatch of new product development and end user

needs poses a threat to Graco’s operations through decreasing margins and thus

operating efficiencies.

Risks to Growth Strategy

International growth has proven a key area of improvement for Graco in their growth

strategy; lower than expected market penetration into the region coupled with slowing

trends in the region stemming from areas like the Chinese mining market will prove

troublesome for Graco in the short to midterm. Also, recent and future acquisitions also

pose sizeable risk, as oil prices (Figure 8) have dropped to below 5 year lows and

Graco’s most recent acquisitions have targeted products in oil related markets, including

exploration.

Systematic Risk

A large systematic investment risk posed to Graco involves significant currency

fluctuations and a continued appreciation of the US dollar versus other foreign currencies

(Figure 9). While a large portion of revenues (57%) are derived in the Americas segment,

international revenues have significant impact on total revenues and net income.

Because management has stated that they do not intend to hedge against currency risk

in relation to income, this does provide some risk to our thesis.

Statistical Measures of Risk

For statistical risk measures we used value at risk and standard deviation as

indicators of risk. Our methodology included yearly data spanning back to the IPO of

the firm and different time periods to give a broad picture of statistical risk and

calculations for value at risk can be seen to the right As can be seen in Table 13

statistical risk over time has exceeded benchmarks like the S&P 500 (8.15% since

IPO); however, there is also a significant decrease in risk when considering a more

recent timeframe, which fits with the frame of Graco’s continued development of

operating efficiencies and relatively stable market share in niche markets.

Statistical Risk Measures

Standard

Deviation

Value at

Risk (5%

CI)

IPO 24.82% -20.070%

10

Year 24.86% -26.53%

5

Year 16.24% 1.24%

0

20

40

60

80

100

120

M-14 J-14 S-14 D-14 A-15

WTI Oil Prices

Figure 8

Figure 9

Table 13

12. 12

Appendices

Appendix A

Date

Announced Target Name Seller Name

Announced

Total Value

(mil.) Payment Type Deal Status

1/2/2015 High Pressure Equipment Co 160 Cash Pending

1/2/2015

GeoBlaster Equipment Sales

& Services Inc N/A Cash Completed

1/2/2015

Multimaq-Pistolas e

Equipamentos Para Pintura

Ltd N/A Cash Completed

1/2/2015

White Knight Fluid Handling

Inc N/A Cash Pending

10/8/2014 Liquid Finishing business Graco Inc 590 Cash Pending

10/1/2014 Alco Valves Ltd 116.55 Cash Completed

1/2/2014

Ecoquip Ltd,QED

Environmental Systems Inc N/A Undisclosed Completed

4/14/2011 Finishing Business Illinois Tool Works Inc 650 Cash Completed

10/2/2008

LubeSci Assets,Airlessco

Painting Assets

Lubrication Scientifics

Inc,Durotech Inc 20 Cash Completed

12/3/2007 Cohesant Technologies Inc 35 Cash Completed

7/11/2006 Lubriquip Inc IDEX Corp N/A Undisclosed Completed

9/23/2005 PBL Industries N/A Cash Completed

2/4/2005 Gusmer Corp PMC Global Inc 45 Cash Completed

2/4/2005 Gusmer Europe SL PMC Global Inc 20 Cash Completed

12/21/2004 Liquid Control Corp Inc N/A Cash Completed

3/31/2003 Sharpe Manufacturing Co N/A Undisclosed Completed

3/20/2001

Panatech Research &

Development Corp

Harbour Group

Investments LP N/A Undisclosed Completed

4/28/1999 Bollhoff Verfahrenstechnik N/A Undisclosed Completed

Sources:

Bloomberg,

Graco.com

13. 13

Appendix B

Graco Peer Group

Ticker Company Name Description

GGG Graco

Graco is a manufacturer of specialized materials applicators for a wide

variety of niche markets

IEX Idex Corp

Idex manufactures specialized pumps and pumping equipment for a variety of

markets in the industrials sector and others

FELE Franklin Electric Co.

Franklin designs and manufactures motors for specialized pumping

equipment as well as a variety of other industrial equipment including fans,

heating equipment, pool equipment, and other areas

SPW SPX Corp.

Provides technical components and complete systems for a variety of

markets, but specifically target data transfer and communications networks

ITT ITT Corp.

ITT is a manufacturer of diversified industrial products geared towards end

markets, which includes pumps and applicators as well as brake pads and

connectors

CR Crane Co.

Crane manufactures industrial products for a variety of product lines and

market segments including pumps, as well as vending machines, hydrocarbon

processing

XYL Xylem Inc.

Xylem designs and manufactures equipment and provides services for water

and wasterwater processes, from distribution to dispensing, and includes

pumping equipment along with valves, heat exchangers and others

NDSN Nordon Corp.

Nordson designs and manufactures complete systems that apply adhesives

and other abrasive products for industrial and consumer application

FLS Flowserve Corp.

Flowserve designs, manufactures, and distributes flow management

equipment

including pumps, valves and mechanical seals in various industries

PNR Pentair PLC

Pentair distributes and services products for customers in various segments

including water and other fluids, thermal management, and equipment

protection

CFX Colfax Corp.

Colfax manufactures a variety of fluid handling equipment which includes

pumps, fluid handling systems, and valves serving several markets but

specifically the rotary positive displacement pump segment

14. 14

Appendix C

Beta t-score p-value

3-year 1.312 9.708 0

5-year 1.472 19.986 0

10-year 1.303 25.592 0

Beta Time Series

15. 15

Appendix D

Source from Graco. Com and Bloomberg

Officers Position Affiliate and Description

Chairman

Lee R. Mitau Retired Executive Vice

President and General

Counsel, U.S. Bancorp

Chairman of the Board of Director at Graco Inc. and HB Fuller

Company

Board Member

William Grant Van

Dyke

Retired Chairman,

Donaldson Company

Inc.

Member of the Board of Directors at Graco and Polaris Industries Inc.

Martha A. M.

Morfit

President/CEO at River

Rock Partners Inc. and

CEO at Airborne

Health Inc.

Member of the Board of Directors at Shock Doctor Inc.,

Lululemon Athletica Inc., Life Time Fitness Inc., Intrawest Ulc.,

and Graco Inc.

William J. Carrol CEO at Hybra-Drive

Systems LLC.

Member of the Board of Directors at Graco Inc.

J. Kevin Gilligan Chairman/CEO at

Capella Education

Company

Chairman of the Board of Directors at Capella Education

Company

Member of the Board of Directors at United Subcontractors Inc.,

Capella University, and Graco Inc.

Jack W. Eugster Retired Chairman,

President/CEO at

Musicland Stores

Corporation

Chairman of the Board of Directors at Carleton College

Member of the Board of Directors at Trans-Alarm Inc., Life

Time Fitness Inc. Black Hills Coporation, and Graco Inc.

R. William Van

Sant

Senior Operating

Partner at Tenex

Capital Management

Chairman of the Board of Director at Quintec SA

Vice Chairman of the Board of Directors at HB Fuller

Member of the Board of Directors at Rush Corporation, Graco

Inc., and Amcast Industrial Corporation

Patrick J. McHale President/CEO at

Graco Inc

Member of the Board of Directors at North Memorial Health

Care and Graco Inc.

Eric P. Etchart Senior Vice President

of Business

Development at

Manitowoc Company

Inc.

Member of the Board of Directors at Graco Inc.

16. 16

Appendix E

Graco Inc Income Statement (GGG US) - Standardized

In Millions of USD except Per Share FY 2009 FY 2010 FY 2011 FY 2012 FY 2013

12 Months Ending 2009-12-25 2010-12-31 2011-12-30 2012-12-28 2013-12-27

Revenue 579.2 744.1 895.3 1,012.5 1,104.0

- Cost of Revenue 286.4 340.6 395.1 461.9 496.6

Gross Profit 292.8 403.4 500.2 550.5 607.5

+ Other Operating Revenue 0.0 0.0 0.0 0.0 0.0

- Operating Expenses 218.3 250.3 280.7 325.9 327.7

R&D Expenses 37.5 37.7 41.6 48.9 51.4

SG&A Expenses 180.8 212.6 239.1 276.9 276.3

Operating Income 74.5 153.1 219.5 224.7 279.8

- Interest Expense 4.9 4.2 9.1 19.3 18.1

- Foreign Exchange Losses (Gains) 0.0 0.0 0.0 0.0 0.0

- Net Non-Operating Losses (Gains) 0.9 0.4 0.7 -11.9 -27.2

Pretax Income 68.7 148.5 209.7 217.3 288.8

- Income Tax Expense 19.7 45.7 67.4 68.2 78.0

Income Before XO Items 49.0 102.8 142.3 149.1 210.8

- Extraordinary Loss Net of Tax 0.0 0.0 0.0 0.0 0.0

- Minority Interests 0.0 0.0 0.0 0.0 0.0

Net Income 49.0 102.8 142.3 149.1 210.8

- Total Cash Preferred Dividends 0.0 0.0 0.0 0.0 0.0

- Other Adjustments 0.0 0.0 0.0 0.0 0.0

Net Inc Avail to Common Shareholders 49.0 102.8 142.3 149.1 210.8

Basic EPS 0.82 1.71 2.36 2.47 3.44

Diluted EPS 0.81 1.69 2.32 2.42 3.36

Source: Bloomberg

17. 17

Graco Inc Balance Sheet Forecast (GGG US) - Standardized

In Millions of USD except Per Share FY 2009 FY 2010 FY 2011 FY 2012 FY 2013

Assets

+ Cash & Equivalents 5 10 303 458 442

+ Accounts & Notes Receivable 100.8 124.6 150.9 172.1 183.3

+ Inventories 58.7 91.6 105.3 121.5 133.8

+ Other Current Assets 24.1 26.6 23.6 25.4 33.5

Total Current Assets 189.0 252.4 583.0 777.0 792.6

+ Net Fixed Assets 139.1 134.2 138.2 151.5 151.7

+ Other Long-Term Assets 148.4 143.9 153.1 393.2 382.9

Total Long-Term Assets 287.4 278.1 291.3 544.7 534.6

Total Assets 476.4 530.5 874.3 1,321.7 1,327.2

Liabilities & Shareholders' Equity

+ Accounts Payable 18.0 19.7 27.4 28.9 34.3

+ Short-Term Borrowings 12.0 8.2 8.7 8.1 9.6

+ Other Short-Term Liabilities 73.8 91.9 95.2 114.6 125.0

Total Current Liabilities 103.8 119.8 131.3 151.7 168.9

+ Long-Term Borrowings 86.3 70.3 300.0 556.5 408.4

+ Other Long-Term Liabilities 76.7 76.4 120.3 159.5 115.6

Total Long-Term Liabilities 163.0 146.6 420.3 715.9 524.0

Total Liabilities 266.8 266.4 551.6 867.6 692.9

+ Total Preferred Equity 0.0 0.0 0.0 0.0 0.0

+ Minority Interest 0.0 0.0 0.0 0.0 0.0

+ Share Capital & APIC 250.3 272.1 301.8 348.6 408.1

+ Retained Earnings & Other Equity -40.6 -8.0 21.0 105.6 226.3

Total Equity 209.7 264.1 322.7 454.1 634.4

Total Liabilities & Equity 476.4 530.5 874.3 1,321.7 1,327.2

Source: Bloomberg

18. 18

Graco Inc Statement of Cash Flows Forecast (GGG US) - Standardized

In Millions of USD except Per Share FY 2009 FY 2010 FY 2011 FY 2012 FY 2013

Cash From Operating Activities

+ Net Income 49.0 102.8 142.3 149.1 210.8

+ Depreciation & Amortization 35.1 34.0 32.5 38.8 37.3

+ Other Non-Cash Adjustments 8.6 -0.1 16.8 -6.9 7.0

+ Changes in Non-Cash Capital 53.8 -35.6 -29.6 8.7 -12.1

Cash From Operations 146.5 101.1 162.0 189.7 243.1

Cash From Investing Activities

+ Disposal of Fixed Assets 0.8 0.3 0.4 0.0 1.6

+ Capital Expenditures -11.5 -16.6 -23.9 -18.2 -23.3

+ Increase in Investments 0.0 0.0 0.0 0.0 0.0

+ Decrease in Investments 0.0 0.0 0.0 0.0 0.0

+ Other Investing Activities -2.1 -2.4 -4.6 -676.3 -9.5

Cash From Investing Activities -12.8 -18.8 -28.0 -694.5 -31.2

Cash from Financing Activities

+ Dividends Paid -45.4 -48.1 -50.6 -54.3 -61.1

+ Change in Short-Term Borrowings -6.4 -3.2 0.5 -0.6 1.3

+ Increase in Long-Term Borrowings 78.0 140.5 402.2 649.3 419.9

+ Decrease In Long-Term Borrowings -171.7 -156.5 -172.4 -394.8 -568.1

+ Increase in Capital Stocks 6.9 14.8 24.4 34.4 50.0

+ Decrease in Capital Stocks -0.2 -24.2 -43.3 -1.4 -67.8

+ Other Financing Activities -1.6 -1.4 -1.3 0.1 2.7

Cash from Financing Activities -140.4 -78.2 159.5 232.8 -223.2

Net Changes in Cash -6.7 4.2 293.6 -272.0 -11.4

Source: Bloomberg

19. 19

Appendix F

Graco Inc Income Statement Forecast (GGG US) - Standardized

In Millions of USD except Per Share FY 2014E FY 2015E FY 2016E FY 2017E FY 2018E FY 2019E

12 Months Ending

Revenue 1,219.0 1,346.0 1,501.4 1,351.2 1,507.4 1,681.7

- Cost of Revenue 550.4 601.1 645.5 692.8 743.6 798.0

Gross Profit 668.6 744.9 855.9 658.4 763.8 883.7

+ Other Operating Revenue 0.0 0.0 0.0 0.0 0.0 0.0

- Operating Expenses 324.0 348.3 368.0 388.4 409.7 432.0

R&D Expenses 60.7 66.6 71.9 77.6 83.7 90.3

SG&A Expenses 263.4 281.7 296.1 310.8 326.0 341.6

Operating Income 344.6 396.6 487.9 270.1 354.1 451.7

- Interest Expense 17.5 17.5 17.5 17.5 17.5 17.5

- Foreign Exchange Losses (Gains) 0.0 0.0 0.0 0.0 0.0 0.0

- Net Non-Operating Losses (Gains) 0.0 0.0 0.0 0.0 0.0 0.0

Pretax Income 327.1 379.1 470.4 252.6 336.6 434.2

- Income Tax Expense 98.1 113.7 141.1 75.8 107.7 138.9

Income Before XO Items 229.0 265.3 329.3 176.8 228.9 295.2

- Extraordinary Loss Net of Tax 0.0 0.0 0.0 0.0 0.0 0.0

- Minority Interests 0.0 0.0 0.0 0.0 0.0 0.0

Net Income 229.0 265.3 329.3 176.8 228.9 295.2

- Total Cash Preferred Dividends 0.0 0.0 0.0 0.0 0.0 0.0

- Other Adjustments 0.0 0.0 0.0 0.0 0.0 0.0

Net Inc Avail to Common Shareholders 229.0 265.3 329.3 176.8 228.9 295.2

Basic EPS 3.75 4.35 5.40 2.90 3.75 4.84

Diluted EPS 3.72 4.31 5.35 2.87 3.72 4.80

25. 25

2014 2015 2016 2017 2018 2019 Terminal

226.05 228.92 234.00 192.83 190.91 194.74 2722.21

PV of FCF 3989.66

WACC 0.12325

Total Debt 418 Price 67.49$

Cash and Equiv. 442

Equity Value 4013.66

Shares Outst. 59.469

Present Value of Forecasted Cash Flows

26. 26

Appendix I

Parameter Standard

Estimate Error

Intercept 1 0.54413 0.45226 1.2 0.2306

Mkt_RF 1 1.03763 0.10104 10.27 <.0001

SMB 1 0.55122 0.13975 3.94 0.0001

HML 1 0.81645 0.14256 5.73 <.0001

Adjusted Market Beta 1.0094075

Data Source: Bloomberg, Kenneth R. French Data Library

Estimated market beta adjusted based on mean reverting property. .75+.25*raw beta

Parameter Estimates

Variable DF t Value Pr > |t|

27. 27

Appendix J

Yield Outstanding Amount (in Millions)

Series A 0.01912 75

Series B 0.03104 75

Series C 0.02511 75

Series D 0.03517 75

Average Interest rate (12/27/2013)

Unsecured revolving credit facility 0.0142 108.37

Notes payable to banks 0.0081 9.584

Yield Amount Weight

0.01912 75 0.17945 0.00343

0.03104 75 0.17945 0.00557

0.02511 75 0.17945 0.00451

0.03517 75 0.17945 0.00631

0.0142 108.37 0.25929 0.00368

0.0081 9.584 0.02293 0.00019

417.954

Weighted Average Yield 2.369%

current yield of bonds

Average Interest Rate on other forms of debt

Cost of Debt Calculation

28. 28

Appendix K

ERP Weight

ERP(US) 0.08298 0.539

ERP(EURO) 0.11207 0.256

ERP(CHINA) 0.08805 0.205

Weighted

Average Equity

Risk Premium 0.09147

E(RF) 0.01775

E(SMB) 0.02187

E(HML) 0.02334

Fama French Assumptions

29. 29

Appendix L

free cash flow in period 5 194.74

short-term growth rate 6.647%

long-term (mature) growth rate 3.0%

Years until Mature growth 15

WACC 0.12325

Terminal Value 2722.21

H-Model

32. 32

Appendix O

Benjamin Graham Enterprise Investor screening

Current ratio at least 1.5 Y

No negative earnings in last 5 years Y

Dividends currently being paid Y

Current earnings higher than 5 years ago Y

Stock price less than 120% of assets N

Positiv

e Net

Income

Positive

Operating

Cash Flow

Increasing

ROA

Quality

of

Earnings

Long

Term

Debt

vs.

Assets

Current

Ratio

Shares Out

Same or

Decreasing

Increasing

Gross

Margin

Increasing

Asset

Turnover

Piotroski

F-Score

1 1 1 1 1 0 0 1 0 6

33. 33

Appendix P

The model used to forecast Graco’s revenue is an Autoregressive Integrated Moving

Average Model (ARIMA) with 4th lag on autoregressive part and moving average

part. We decided to use ARIMA instead of Autoregressive Moving Average Model

(ARMA) because we found that Graco’s revenue is integrated of order 1 by a

statistical test called augmented Dickey-Fuller test. This test checks whether or not

data is stationary. Based on the ARIMA model, we forecasted Graco’s revenue for

five quarters and found that 2015 third quarter to be 324.93 million.

0

50

100

150

200

250

300

350

400

0 5 10 15 20 25 30 35 40 45 50

RevenueinMillions

Quearters

Revenue in Millions

Actual Forcasted

34. 34

Dependent Variable:

D(GRACO_REV)

Method: Least Squares

Date: 01/09/15 Time:

16:32

Sample (adjusted):

1991Q2 2014Q3

Included observations: 94

after adjustments

Convergence achieved

after 13 iterations

MA Backcast: 1990Q2

1991Q1

Variable Coefficie

nt

Std. Error t-

Statistic

Prob.

C 33.68234 278.7472 0.12083

5

0.904

1

AR(4) 0.996173 0.031665 31.4596

6

0

MA(4) -0.69509 0.073149 -

9.50237

0

R-squared 0.55046

9

Mean

dependent

var

2.501181

Adjusted R-squared 0.54058

9

S.D.

dependent

var

14.81445

S.E. of regression 10.0412

2

Akaike info

criterion

7.482668

Sum squared resid 9175.17 Schwarz

criterion

7.563837

Log likelihood -348.685 Hannan-

Quinn criter.

7.515455

F-statistic 55.7165

2

Durbin-

Watson stat

1.519079

Prob(F-statistic) 0

Inverted AR Roots 1 .00+1.00i -

.00-

1.00

i

-1

Inverted MA Roots 0.91 .00-.91i

.00+.9

1i

-0.91

35. 35

Appendix Q

In our technical analysis, we used a weekly chart to analyze price movements for

Graco. Since the week of March 13th 2009 Graco’s stock price has been in a strong

upward trend. Currently, price looks like it is in the range bound territory which is

confirmed by the flattening move of both 20 and 50 period simple moving averages.

Also, there is strong support around $66 per share which is verified by two bouncing

back movements and an upper resistance at $80 per share. Additionally, the relative

strength index lies between the 70 and 20 zone; therefore, there is a room for

potential upside movement.

36. 36

Disclosures:

Ownership and material conflicts of interest:

The author(s), or a member of their household, of this report does not hold a financial interest in the

securities of this company.

The author(s), or a member of their household, of this report does not know of the existence of any

conflicts of interest that might bias the content or publication of this report.

Receipt of compensation:

Compensation of the author(s) of this report is not based on investment banking revenue.

Position as an officer or director:

The author(s), or a member of their household, does not serve as an officer, director or advisory board

member of the subject company.

Market making:

The author(s) does not act as a market maker in the subject company’s securities.

Disclaimer:

The information set forth herein has been obtained or derived from sources generally available to the

public and believed by the author(s) to be reliable, but the author(s) does not make any representation or

warranty, express or implied, as to its accuracy or completeness. The information is not intended to be used

as the basis of any investment decisions by any person or entity. This information does not constitute

investment advice, nor is it an offer or a solicitation of an offer to buy or sell any security. This report should

not be considered to be a recommendation by any individual affiliated with North Dakota State University,

CFA Society of Minnesota, CFA Institute or the CFA Institute Research Challenge with regard to this

company’s stock.

CFA Institute Research Challenge