1. 1

Accounting Entries Regarding Issue of Shares at Par

Par value does not indicate a stocks market value. Therefore, the cash proceeds

from issuing par value stock may be equal to, greater than or less than par value.

When the issuance of common stock faro cash is recorded, the par value of the

shares can be credited to common stock.

The portion of proceeds that is above or below the par value is recorded in a

separate paid in Capital a/c

Example 1

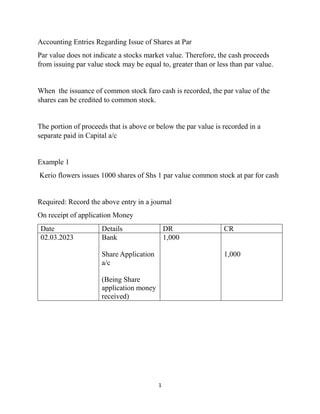

Kerio flowers issues 1000 shares of Shs 1 par value common stock at par for cash

Required: Record the above entry in a journal

On receipt of application Money

Date Details DR CR

02.03.2023 Bank

Share Application

a/c

(Being Share

application money

received)

1,000

1,000

2. 2

On Allotment of Shares

Date Details DR CR

02.03.2023 Share Application a/c

Share Capital A/c

(Being appropriation of application Money

towards Share capital)

1,000

1,000

Issue of Shares at a premium

Example 2

If Kerio flowers issues another 1000 shares of Shs 1 par value at Shs 5 for cash.

Required: Journalize the above transaction

Date Details DR CR

02.03.2023 Cash

Share Capital

Share Premium

(To record the issuance of shares at a

premium)

5,000

1,000

4,000

The total Paid in capital from these two transactions is Kes 6,000 and the legal

capital is 2,000. If Kerio flowers has retained earnings of Kes 500, the stockholders

equity will be Kes 6,500 and it will be presented as follows in the balance sheet.

3. 3

Equity

Share Capital 2,000

Premium A/c 4,000

Total Paid in Capital 6,000

Retained Earnings 500

Total Stakeholders Equity 6,500

Shares issued at a Discount

When Shares are issued at a price lower than their face value, they are said to have

been issued at a discount. For example, if a share of Kes 100 is issued at Kes 95,

then Kes 5 (Kes 100—95) is the amount of discount. It is a loss to the company.

It should be noted that the issue of share below the market price but above face

value is not termed as ‘Issue of Share at Discount’ Issue of Share at Discount is

always below the nominal value of shares.

It is debited to separate account called ‘Discount on Issue of Share’ Account.

Disclosure in Balance Sheet

It is deducted from securities premium reserve account from the liabilities side.

Conditions to Issue Share at Discount

Shares can be issued at discount subject to the following conditions:

1) The shares must belong to a class already issued.

2) Discount rate should not be more than 10%.

3) One year must have passed since the date at which the company was allowed

to commence business.

4. 4

4) The issue of such shares must take place within two months after the date of

court’s sanction or within such extended time as the court may allow.

Accounting Treatment for Shares issued at a Discount

Trendy Shoe Company invited applications for 12,000 equity shares of Kes. 100

each at a discount Kes. 4 per share (allowed at the time of allotment). The amount

was payable as follows: On Application Kes 30, on allotment Kes 36, on first and

final call Kes. 30.

The public applied for 10,000 shares and these were allotted. All money due was

with the exception the first and final call on 400 shares.

On Application

Date Details DR CR

02.03.23 Bank (10,000@30)

Share Application

(Being the receipt of application money

for issue of shares)

300,000

300,000

02.03.23 Share Application

Share Capital

(Being transfer from the share

allocation to the share capital)

300,000

300,000

02.03.23 Share Allotment a/c (10,000@36)

Share Discount a/c (10,000@4)

Share Capital a/c

(Being allotment of shares @36)

360,000

40,000

400,000

02.03.23 Bank (10,000@36)

Share Allotment

(Being the issue of Shares at a discount)

360,000

360,000

02.03.23 Equity First & Final call@30

Equity Share Capital

(Being the record of first and final call

of 10,000 shares)

300,000

300,000

02.03.23 Bank (9600@30) 288,000

5. 5

Calls in Arrears (400@30)

Equity first & Final Call A/c

(Being the payment of shares remaining

after the first and final call)

12,000

300,000