Are you confused about recent SEC guidance and proposed and final rules impacting public companies? So were we, so we put together this handy chart.

It covers the following recent SEC guidance and proposed and final rules:

- Amendments to "smaller reporting company" definition

- Non-GAAP financial measures

- Hedging policy disclosure

- Executive compensation clawback policy

- CEO pay ratio disclosure

- Pay-for-performance

- Bonus! An overview of the scaled disclosure requirements for "smaller reporting companies" under Reg. S-K and Reg. S-X

Feel free to share!

Petitioner Moot Memorial including Charges and Argument Advanced.docx

Handy chart of the day: Recent SEC guidance and rules

1. Summit Law Group, PLLC | 315 Fifth Avenue South, Suite 1000 | Seattle, Washington 98104-2682 | 206-676-7000 | www.summitlaw.com

Recent SEC Guidance and Proposed and Final Rules (July 2016)

The following is a list of selected guidance, proposed rules and final rules recently published or promulgated by the Securities

and Exchange Commission (the “SEC”). This list is intended only as a summary of certain key points, and should not be read as

an exhaustive list of all items from the guidance or rules that may be material. For more information, please click on the link in

the first column below, or contact your Summit team member.

Guidance/Rule

(including link)

Description of Guidance/Rule Phase-in

Period

Exemption

for SRC or

EGC?

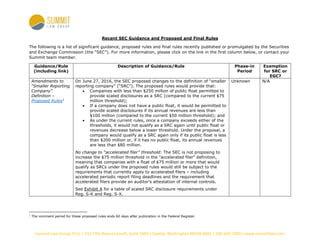

Amendments to

“Smaller Reporting

Company”

Definition –

Proposed Rules1

On June 27, 2016, the SEC proposed changes to the definition of “smaller

reporting company” (“SRC”). The proposed rules would provide that:

Companies with less than $250 million of public float permitted to

provide scaled disclosures as a SRC (compared to the current $75

million threshold);

If a company does not have a public float, it would be permitted to

provide scaled disclosures if its annual revenues are less than

$100 million (compared to the current $50 million threshold); and

As under the current rules, once a company exceeds either of the

thresholds, it would not qualify as a SRC again until public float or

revenues decrease below a lower threshold. Under the proposal, a

company would qualify as a SRC again only if its public float is less

than $200 million or, if it has no public float, its annual revenues

are less than $80 million.

No change to “accelerated filer” threshold: The SEC is not proposing to

increase the $75 million threshold in the "accelerated filer" definition,

meaning that companies with a float of $75 million or more that would

qualify as SRCs under the proposed rules would still be subject to the

requirements that currently apply to accelerated filers – including

accelerated periodic report filing deadlines and the requirement that

accelerated filers provide an auditor’s attestation of internal controls.

See Exhibit A attached hereto for a table of scaled SRC disclosure

requirements under Reg. S-K and Reg. S-X.

Unknown N/A

1

The comment period for these proposed rules ends 60 days after publication in the Federal Register.

2. Summit Law Group, PLLC | 315 Fifth Avenue South, Suite 1000 | Seattle, Washington 98104-2682 | 206-676-7000 | www.summitlaw.com

Guidance/Rule

(including link)

Description of Guidance/Rule Phase-in

Period

Exemption

for SRC or

EGC?

Non-GAAP

Financial Measures

– C&DIs Guidance

This guidance clarifies the rules for using non-GAAP financial measures

under Regulation G:

Certain presentations of non-GAAP financial measures are

expressly prohibited (e.g., substituting individually tailored

revenue recognition and measurement methods for GAAP

measures as a baseline for calculating non-GAAP earnings, and

non-GAAP measures that adjust for non-recurring charges but not

for non-recurring gains);

Confirms that certain adjustments, although not explicitly

prohibited, may result in a non-GAAP measure that is misleading

(e.g., presenting a performance measure that excludes normal,

recurring, cash operating expenses necessary to operate a

company’s business could be misleading, or presenting non-GAAP

measure inconsistently between periods);

GAAP financial measures should be given equal or greater

prominence with non-GAAP financial measures; whether a non-

GAAP measure is more prominent than the comparable GAAP

measure generally depends on the facts and circumstances in

which the disclosure is made, but the SEC indicated it would

consider the following examples of disclosure of non-GAAP

measures as more prominent:

Providing tabular disclosure of non-GAAP financial measures

without preceding it with an equally prominent tabular

disclosure of the comparable GAAP measures or including the

comparable GAAP measures in the same table;

Presenting a full income statement of non-GAAP measures or

presenting a full non-GAAP income statement when reconciling

non-GAAP measures to the most directly comparable GAAP

measures;

Excluding a quantitative reconciliation with respect to a

forward-looking non-GAAP measure in reliance on the

“unreasonable efforts” exception (see below) without disclosing

that fact and identifying the information that is unavailable and

None No

3. Summit Law Group, PLLC | 315 Fifth Avenue South, Suite 1000 | Seattle, Washington 98104-2682 | 206-676-7000 | www.summitlaw.com

Guidance/Rule

(including link)

Description of Guidance/Rule Phase-in

Period

Exemption

for SRC or

EGC?

its probable significance in a location of equal or greater

prominence;

Describing a non-GAAP measure as, for example, “record

performance” or “exceptional” without at least an equally

prominent descriptive characterization of the comparable GAAP

measure;

A non-GAAP measure that precedes the most directly

comparable GAAP measure (including in an earnings release

headline or caption);

Omitting comparable GAAP measures from an earnings release

headline or caption that includes non-GAAP measures;

Providing discussion and analysis of a non-GAAP measure

without a similar discussion and analysis of the comparable

GAAP measure in a location with equal or greater prominence;

and

Presenting a non-GAAP measure using a style of presentation

(e.g., bold, larger font) that emphasizes the non-GAAP

measure over the comparable GAAP measure.

Companies are required to provide a quantitative reconciliation of

forward-looking non-GAAP financial measures to the extent

available without “unreasonable efforts,” and if a comparable

GAAP financial measure is not available on a forward-looking

basis, a company must disclose that fact, provide the reconciling

information that is available, and identify the unavailable

information and disclose its probable significance; and

Non-GAAP liquidity measures (such as free cash flow), EBIT and

EBITDA may not be presented on a per-share basis.

4. Summit Law Group, PLLC | 315 Fifth Avenue South, Suite 1000 | Seattle, Washington 98104-2682 | 206-676-7000 | www.summitlaw.com

Guidance/Rule

(including link)

Description of Guidance/Rule Phase-in

Period

Exemption

for SRC or

EGC?

Hedging Policy

Disclosure -

Proposed Rules2

Proposed rules would require companies to disclose whether the company

permits any employee, officer or director of the company to purchase any

financial instruments or otherwise engage in transactions that are

designed to or have the effect of “hedging” or offsetting any decrease in

the market value of equity securities that such persons receive from the

company as compensation or that they otherwise hold, directly or

indirectly.

While no specific hedging policy is required, under the proposed rules, all

domestic public companies would be required to:

Specify the categories of hedging transactions it permits and

prohibits;

Describe the details and process involving any permitted hedging

transactions, including whether such transactions must be

preapproved and whether a holding period or stock ownership

guidelines apply before hedging will be permitted; and

Disclose any permissions or prohibitions that specially apply to any

of its employees or directors, but not to others.

Unknown No. This is

notable

because

currently

emerging

growth

companies

(“EGCs”)

and SRCs

are not

otherwise

required to

provide any

CD&A

hedging

policy

disclosure

under Item

402(b) of

Reg. S-K.

Executive

Compensation

Clawback Policy –

Proposed Rules3

Proposed rules would require national securities exchanges to establish

listing standards requiring listed companies to adopt, implement, enforce

and disclose a policy to recover “excess” incentive-based compensation

(i.e., compensation that is granted, earned or vested based wholly or in

part on attainment of a financial reporting measure) received by current

or former Section 16 executive officers during the prior three years to the

extent that such excess compensation was awarded as a result of

material noncompliance with financial reporting requirements that

Unknown No

2

The comment period for these proposed rules expired on April 20, 2015, and the SEC has not extended the comment period or released any new information

regarding when the final rules will be published.

3

The comment period for these proposed rules expired on September 14, 2015, and the SEC has not extended the comment period or released any new

information regarding when the final rules will be published.

5. Summit Law Group, PLLC | 315 Fifth Avenue South, Suite 1000 | Seattle, Washington 98104-2682 | 206-676-7000 | www.summitlaw.com

Guidance/Rule

(including link)

Description of Guidance/Rule Phase-in

Period

Exemption

for SRC or

EGC?

resulted in an accounting restatement. The proposed rules would require

public companies to:

Adopt a clawback policy within 60 days after the new exchange

rules become effective, which must be 90 days after the SEC’s

final rules are published;

Enforce the clawback policy by recovering the amount of incentive-

based compensation actually paid to current and former executive

officers during the three-year period preceding the year in which

the company is required to restate its financial statements in

excess of what would have been paid had the financial statements

been correct at the time the compensation was received,

irrespective of whether those executive officers engaged in any

misconduct; and

Disclose the clawback policy as an exhibit to its Form 10-K and

provide disclosures about the policy in its annual proxy or

information statement if and when the recovery policy is triggered.

Companies should review and update incentive plans, award agreements,

and employment agreements and consider modifications to the

compensation committee charter with respect to clawback policy

enforcement.

CEO Pay Ratio

Disclosure – Final

Rules

Final rules require companies to identify their “median” employee and

disclose the following information:

The median of the annual total compensation of all employees,

excluding the CEO;

The annual total compensation of the CEO; and

The ratio of these two totals. The ratio may be disclosed

numerically (e.g. 50 to 1) or narratively (e.g. “the CEO’s annual

total compensation is 50 times that of the median of the annual

total compensation of all employees), but not as a percentage or

fraction of the CEO’s compensation.

Identifying the median employee: Companies have significant flexibility in

identifying the median employee and can use reasonable estimates based

on the company’s facts and circumstances. However, the median

Disclosures

required for

compensatio

n paid for

the

company’s

first full

fiscal year

beginning on

or after

January 1,

2017 (so

generally

Yes – does

not apply to

SRCs or

EGCs. One-

year phase-

in grace

period after

loss of SRC

or EGC

status.

6. Summit Law Group, PLLC | 315 Fifth Avenue South, Suite 1000 | Seattle, Washington 98104-2682 | 206-676-7000 | www.summitlaw.com

Guidance/Rule

(including link)

Description of Guidance/Rule Phase-in

Period

Exemption

for SRC or

EGC?

employee must be determined from all “employees,” which includes all

U.S. and non-U.S. full-time, part-time, seasonal and temporary

employees and its consolidated subsidiaries. Independent contractors or

leased workers are excluded from the analysis but only to the extent that

they are employed by and their compensation is determined by an

unaffiliated third party. The date for determining the median employee

must be disclosed and must be within the last three months of the last

completed fiscal year. There are also limited exceptions for non-U.S.

employees relating to data privacy laws and when 5% or less of the total

workforce is non-U.S.-based.

Calculating annual total compensation: The total compensation of the

median employee must be calculated consistent with the requirements for

calculating total compensation for the CEO for purposes of the summary

compensation table under Item 402 of Reg. S-K. The company may use

reasonable estimates, as long as they are consistently applied and

disclosed. Any change in methodology, assumptions, adjustments or

estimates from the prior year must be disclosed if the effects are

significant.

the 2018

proxy,

practically

speaking)

Pay-for-

Performance –

Proposed Rules4

Proposed rules would require companies to disclose the relationship

between executive compensation actually paid and the company’s

financial performance in a table with the following information for the last

five years:

Executive compensation “actually paid” to the named executive

officers (the “NEOs”) (with separate disclosure for the principal

executive officer and the average for the other NEOs), calculated

based on total compensation as disclosed in the summary

compensation table (the “SCT”), including the vested value of

equity awards vesting during the year (rather than the value at

grant as reported in the SCT);

Annual Total Shareholder Return (TSR) of the company; and

Pay-for-

performance

table must

include the

required

information

for each of

the five

most

recently

completed

fiscal years,

Yes – does

not apply to

EGCs. SRCs

that are not

EGCs would

have

reduced

disclosure

obligations.

4

The comment period for these proposed rules expired on July 6, 2015, and the SEC has not extended the comment period or released any new information

regarding when the final rules will be published.

7. Summit Law Group, PLLC | 315 Fifth Avenue South, Suite 1000 | Seattle, Washington 98104-2682 | 206-676-7000 | www.summitlaw.com

Guidance/Rule

(including link)

Description of Guidance/Rule Phase-in

Period

Exemption

for SRC or

EGC?

Annual Peer Group TSR for the company’s peer group, using either

the peer group selected for the company’s stock performance

graph or as identified in the company’s CD&A disclosure.

Calculation of executive compensation “actually paid:” Under the

proposed rules, “executive compensation actually paid” would be

calculated as follows, but may be supplemented with additional measures

of compensation (such as “realized pay”) as long as such additional

disclosure is not misleading or presented more prominently than the

following required disclosure:

1. Total compensation as reported in the summary compensation

table;

2. Minus the change in the actuarial present value of all defined

benefit and pension plans;

3. Plus the actuarially determined service cost for services rendered

by the executive during the applicable year, in accordance with

FASB ASC Topic 715;

4. Minus the fair value of stock and option awards as of the grant

date; and

5. Plus the aggregate fair value of stock and option awards that

vested during the year as of the vesting date (as determined

under FASB ASC Topic 718), even if options have not been

exercised.

Reduced disclosure for SRCs: SRCs may disclose only three years of

compensation, rather than five, and only two years for the first year of

required disclosure under the proposed phase-in rules. Similarly, SRCs

are not required to disclose peer group TSR or pension-related

information.

which will

occur in

phases:

companies

initially

would only

report three

years of

data and

would

increase

disclosure

each year by

one year,

until five

years of

data is

presented.

8. Summit Law Group, PLLC | 315 Fifth Avenue South, Suite 1000 | Seattle, Washington 98104-2682 | 206-676-7000 | www.summitlaw.com

Exhibit A

Scaled SRC disclosure requirements under Reg. S-K and Reg. S-X

Regulation S-K

Item Scaled Disclosure Accommodation

101 − Description of Business May satisfy disclosure obligations by describing the development of its business during

the last three years rather than five years. Business development description

requirements are less detailed than disclosure requirements for non- smaller reporting

companies.

201 − Market Price of and

Dividends on the Registrant’s

Common Equity and Related

Stockholder Matters

Stock performance graph not required.

301 – Selected Financial Data Not required.

302 – Supplementary Financial

Information

Not required.

303 – Management’s Discussion and

Analysis of Financial Condition and

Results of Operations (MD&A)

Two-year MD&A comparison rather than three-year comparison.

Two year discussion of impact of inflation and changes in prices rather than three

years.

Tabular disclosure of contractual obligations not required.

305 – Quantitative and Qualitative

Disclosures About Market Risk

Not required.

9. Summit Law Group, PLLC | 315 Fifth Avenue South, Suite 1000 | Seattle, Washington 98104-2682 | 206-676-7000 | www.summitlaw.com

Regulation S-K

Item Scaled Disclosure Accommodation

402 – Executive Compensation Three named executive officers rather than five.

Two years of summary compensation table information rather than three. Not

required:

• Compensation discussion and analysis.

• Grants of plan-based awards table.

• Option exercises and stock vested table.

• Pension benefits table.

• Nonqualified deferred compensation table.

• Disclosure of compensation policies and practices related to risk

management.

• Pay ratio disclosure.

404 – Transactions With Related

Persons, Promoters and Certain

Control Persons5

Description of policies/procedures for the review, approval or ratification of related

party transactions not required.

407 – Corporate Governance Audit committee financial expert disclosure not required in first year.

Compensation committee interlocks and insider participation disclosure not

required.

Compensation committee report not required.

503 – Prospectus Summary, Risk

Factors and Ratio of Earnings to

Fixed Charges

No ratio of earnings to fixed charges disclosure required.

No risk factors required in Exchange Act filings.

601 – Exhibits Statements regarding computation of ratios not required.

5

The SEC identified Item 404 of Reg. S-K as the only instance in Reg. S-K in which the disclosure requirements applicable to SRCs could be more stringent.

Item 404 also contains the following expanded disclosure requirements applicable to SRCs: (1) rather than a flat $120,000 disclosure threshold, the threshold is

the lesser of $120,000 or 1% of total assets, (2) disclosures are required about parents and underwriting discounts and commissions where a related person is a

principal underwriter or a controlling person or member of a firm that was or is going to be a principal underwriter, and (3) an additional year of Item 404

disclosure is required in filings other than registration statements.

10. Summit Law Group, PLLC | 315 Fifth Avenue South, Suite 1000 | Seattle, Washington 98104-2682 | 206-676-7000 | www.summitlaw.com

Regulation S-X

Rule Scaled Disclosure

8-02 – Annual Financial Statements Two years of income statements rather than three years.

Two years of cash flow statements rather than three years.

Two years of changes in stockholders’ equity statements rather than three years.

8-03 – Interim Financial Statements Permits certain historical financial data in lieu of separate historical financial

statements of equity investees.

8-04 – Financial Statements of

Businesses Acquired or to Be

Acquired

Maximum of two years of acquiree financial statements rather than three years.

8-05 – Pro forma Financial

Information

Fewer circumstances under which pro forma financial statements are required.

8-06 – Real Estate Operations

Acquired or to Be Acquired

Maximum of two years of financial statements for acquisition of properties from related

parties rather than three years.

8-08 – Age of Financial Statements Less stringent age of financial statements requirements.