Manhattan Second Quarter 2010 Real Estate Market Report

•

1 like•329 views

Prudential Douglas Elliman Manhattan Second Quarter 2010 Real Estate Market Report

Recommended

Recommended

More Related Content

Recently uploaded

Recently uploaded (20)

Featured

Featured (20)

Manhattan Second Quarter 2010 Real Estate Market Report

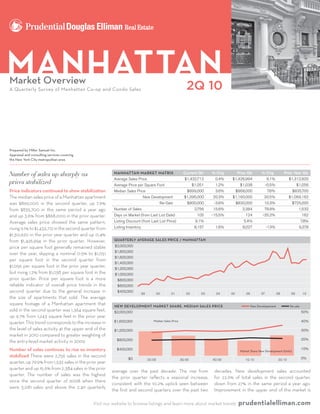

- 1. Manhattan Market Overview 2Q 10 A Quarterly Survey of Manhattan Co-op and Condo Sales Prepared by Miller Samuel Inc. Appraisal and consulting services covering the New York City metropolitan area Number of sales up sharply as Manhattan Market Matrix Current Qtr % Chg Prior Qtr % Chg Prior Year Qtr Average Sales Price $1,432,712 0.4% $1,426,994 9.1% $1,312,920 prices stabilized Average Price per Square Foot $1,051 1.2% $1,038 -0.5% $1,056 Price indicators continued to show stabilization Median Sales Price $899,000 3.6% $868,000 7.6% $835,700 The median sales price of a Manhattan apartment New Development $1,395,000 20.3% $1,160,000 30.5% $1,069,162 was $899,000 in the second quarter, up 7.6% Re-Sale $800,000 -3.6% $830,000 10.3% $725,000 from $835,700 in the same period a year ago Number of Sales 2,756 15.6% 2,384 79.9% 1,532 and up 3.6% from $868,000 in the prior quarter. Days on Market (from Last List Date) 105 -15.5% 124 -35.2% 162 Average sales price showed the same pattern, Listing Discount (from Last List Price) 9.1% 5.4% 7.8% rising 9.1% to $1,432,712 in the second quarter from Listing Inventory 8,157 1.6% 8,027 -13% 9,378 $1,312,920 in the prior year quarter and up 0.4% from $1,426,994 in the prior quarter. However, QUARTERLY�AVERAGE�SALES�PRICE�/�MANHATTAN QUARTERLY�AVERAGE�SALES�PRICE�/�MANHATTAN $2,000,000 price per square foot generally remained stable $2,000,000 $1,800,000 over the year, slipping a nominal 0.5% to $1,051 $1,800,000 $1,600,000 per square foot in the second quarter from $1,600,000 $1,400,000 $1,056 per square foot in the prior year quarter, $1,400,000 $1,200,000 but rising 1.2% from $1,038 per square foot in the $1,200,000 $1,000,000 prior quarter. Price per square foot is a more $1,000,000 $800,000 reliable indicator of overall price trends in the $800,000 $600,000 second quarter due to the general increase in $600,000 $400,000 99 00 01 02 03 04 05 06 07 08 09 10 the size of apartments that sold. The average $400,000 99 00 01 02 03 04 05 06 07 08 09 10 NEW�DEVELOPMENT�MARKET�SHARE��MEDIAN�SALES�PRICE New Developement Re-sale square footage of a Manhattan apartment that NEW�DEVELOPMENT�MARKET�SHARE��MEDIAN�SALES�PRICE New Developement Re-sale 50% $2,000,000 sold in the second quarter was 1,364 square feet, $2,000,000 50% up 9.7% from 1,243 square feet in the prior year $1,600,000 Median Sales Price 40% Median Sales Price 40% quarter. This trend corresponds to the increase in $1,600,000 $1,200,000 30% the level of sales activity at the upper end of the $1,200,000 30% market in 2010 compared to greater weighting of $800,000 20% $800,000 20% the entry-level market activity in 2009. $400,000 10% Market Share New Development (Units) Number of sales continues to rise as inventory $400,000 Market Share New Development (Units) 10% $0 0% stabilized There were 2,756 sales in the second 2Q 09 3Q 09 4Q 09 1Q 10 2Q 10 0% $0 2Q 09 3Q 09 4Q 09 1Q 10 2Q 10 quarter, up 79.9% from 1,532 sales in the prior year AVERAGE�PRICE�PER�SQ�FT�/�CO�OP Downtown East Side West Side Uptown quarter and up 15.6% from 2,384 sales in the prior AVERAGE�PRICE�PER�SQ�FT�/�CO�OP $1,200 decades. NewSide average over the past decade. The rise from Downtown East development sales accounted West Side Uptown quarter. The number of sales was the highest $1,200 the prior quarter reflects a seasonal increase, for 22.6% of total sales in the second quarter, $1,000 since the second quarter of 2008 when there consistent with the 10.2% uptick seen between down from 27% in the same period a year ago. $1,000 were 3,081 sales and above the 2,411 quarterly $800 the first and second quarters over the past two Improvement in the upper end of the market is $800 $600 $600 Visit our website $400 $400 to browse listings and learn more about market trends prudentialelliman.com $200

- 2. 2Q 10 MANhAttAN MArket overvIew Prudential douglas elliMan real estate evidenced by the increase in market share of 3-bedroom sales to 18% from 12% in the same Co-oP market 35% in the prior year quarter. The 3-bedroom 12% market share is consistent with the prior year period last year. Available listing inventory, which Price indicators stabilized as market share, but double the 5 year 6% average, excludes “shadow inventory” was 8,157 in the indicating improved demand at the upper end second quarter, 13% below the 9,378 listing total number of sales rose of the co-op housing market. Listing inventory of the prior year quarter, but up 1.6% from the Number of sales up sharply from prior year totaled 3,948 at the end of the quarter, 10.3% QUARTERLY�AVERAGE�SALES�PRICE�/�MANHATTAN prior quarter total of 8,027. “Shadow inventory”, quarter Co-op sales comprised 43.7% of below the 4,399 listings in the same period last $2,000,000 QUARTERLY�AVERAGE�SALES�PRICE�/�MANHATTAN apartments at or near completion but not formally apartment sales in the second quarter, below year, but 3.6% higher than the 3,809 listings in $1,800,000 $2,000,000 listed for sale, is estimated at approximately 6,500 the 47.9% 5-year average. Co-op sale market the prior quarter. New development co-op listing $1,600,000 $1,800,000 units. The total level of available inventory was in share averaged 54.5% and 57.8% over the past $1,400,000 inventory, in the cond-op form of ownership $1,600,000 sync with the 8,037 listing inventory average of 10$1,200,000 20 years respectively. There were years and comprised only 1.6% of total inventory, as new $1,400,000 the past five years. 1,203 co-op sales in the second quarter, 65.2% $1,000,000 $1,200,000 development favors condominiums. The co-op Days on market continues to fall, listing discount more than the 728 sales in the prior year quarter $800,000 $1,000,000 monthly absorption rate is 9.8 months, nearly rises The average days on market in the second and 8.3% more than the prior quarter total of $600,000 $800,000 one month faster than the 10.5 month average quarter was 105 days, down sharply from 162 days 1,111. The second quarter number of 02 $400,000 $600,000 99 00 01 sales was 03 over the 05 decade. 07 04 past 06 08 09 10 in the same period a year ago and down from 124 consistent $400,000 with the 1,157 quarterly average 99 00 01 02 03 04 05 06New Developement 08 07 Re-sale 10 09 NEW�DEVELOPMENT�MARKET�SHARE��MEDIAN�SALES�PRICE days in the prior quarter. The reduction in days number of sales over the past five years. Studio Price indicators show stabilization The median $2,000,000 NEW�DEVELOPMENT�MARKET�SHARE��MEDIAN�SALES�PRICE Re-sale 50% and 1-bedroom market share fell to 56% in the sales price for a Manhattan co-op was $697,501 in New Developement on market is consistent with the rise in the pace $2,000,000 50% of sales activity. Listing discount increased to second quarter, down from Price in the prior the second quarter, 7.5% higher than $649,000 in $1,600,000 Median Sales 61% 40% year quarter. The entry-level co-op market is $1,600,000 Median Sales Price the prior year quarter and 1.8% above $685,000 40% 9.1% from 7.8% in the prior year quarter and up $1,200,000 30% known as a key access point from the rental in the prior quarter. Average sales price for a from 5.4% in the prior quarter. The rise in listing $1,200,000 30% discount relative to the sharp decline seen in the market for first time buyers. This decrease in Manhattan co-op was $1,113,173 in the second $800,000 20% market share was offset by the 2-bedroom and $800,000 quarter, 4.2% higher than $1,068,726 in the prior 20% prior quarter suggests the prior quarter drop was $400,000 10% an anomaly. The listing discount is consistent with 3-bedroom increase to 42% market share from year quarter,Market Share New Development (Units) in the but 1.8% below $1,133,715 $400,000 10% $0 Market Share New Development (Units) 0% 2Q 09 3Q 09 4Q 09 1Q 10 2Q 10 the rise in “re-sale” inventory that was pulled from $0 0% the market in early 2009, which was priced for the 2Q 09 AVERAGE�PRICE�PER�SQ�FT�/�CO�OP 3Q 09 4Q 09 Downtown 1Q 10 East Side West Side 2Q 10 Uptown “pre-Lehman” market and re-listed in 2010. Since $1,200 AVERAGE�PRICE�PER�SQ�FT�/�CO�OP Downtown East Side West Side Uptown this additional inventory was generally priced $1,200 $1,000 above market levels, the buyer and seller had $1,000 $800 further to travel between list price and contract price to reach a “meeting of the minds”. $800 $600 The first half of 2010 was a significant $600 $400 improvement over 2009 Since the beginning $400 $200 of the year, sales activity has been significantly $0 $200 2Q 09 3Q 09 4Q 09 1Q 10 2Q 10 higher compared to the early quarters of 2009, $0 2Q 09 3Q 09 4Q 09 1Q 10 2Q 10 immediately following the Lehman Brothers LISTING�DISCOUNT�VS��DAYS�ON�MARKET�/�CO�OP bankruptcy–the credit crunch tipping point of 20% LISTING�DISCOUNT�VS��DAYS�ON�MARKET�/�CO�OP 200 September 15, 2008. The mortgage “net” cast 20% 200 16% 175 to borrowers remains smaller than it had been 16% 175 in recent years serving to temper the pace of 12% 150 recovery of the regional housing market. High 12% Days On Market 150 8% 125 unemployment levels, “shadow inventory” and Days On Market 8% 125 tight credit are challenges that continue to face 4% Listing Discount 100 the market, but general market conditions are 4% Listing Discount 100 0% 2Q 09 3Q 09 4Q 09 1Q 10 2Q 10 75 significantly improved over the same period a 0% 2Q 09 3Q 09 4Q 09 1Q 10 2Q 10 75 year ago. AVERAGE�PRICE�PER�SQ�FT�/�CONDO Downtown East Side West Side Uptown $2,500 AVERAGE�PRICE�PER�SQ�FT�/�CONDO Downtown East Side West Side Uptown $2,500 CO-Op Market Matrix Current Qtr %$2,000 Chg Prior Qtr % Chg Prior Year Qtr CO-Op apartMent Mix % of Total Median Price Average Sales Price $1,113,173 -1.8% $2,000 $1,133,715 4.2% $1,068,726 Studio 16% $380,000 $1,500 Average Price per Square Foot $943 3.9% $908 2.8% $917 Median Sales Price $697,501 $1,500 1.8% $685,000 7.5% $649,000 1 bedroom 40% $599,000 $1,000 Number of Sales 1,203 8.3% $1,000 1,111 65.2% 728 2 bedroom 30% $1,100,000 $500 Days on Market (from Last List Date) 92 -16.4% 110 -34.8% 141 3 bedroom 12% $2,200,000 Listing Discount (from Last List Price) 7.3% $500 3.8% 8.7% $0 2Q 09 3Q 09 4Q 09 1Q 10 2Q 10 Listing Inventory 3,948 3.6% 3,809 -10.3% 4,399 4+ bedroom 2% $4,400,000 $0 2Q 09 3Q 09 4Q 09 1Q 10 2Q 10 LISTING�DISCOUNT�VS��DAYS�ON�MARKET�/�CONDO 20% LISTING�DISCOUNT�VS��DAYS�ON�MARKET�/�CONDO 350 prudentialelliman.com Visit our 20% website to 16% browse listings and learn more about market trends 350 300 16% Days On Market 300 12% 250

- 3. $400,000 $600,000 99 00 01 02 03 04 05 06 07 08 09 10 $400,000 99 00 01 02 03 04 NEW�DEVELOPMENT�MARKET�SHARE��MEDIAN�SALES�PRICE 05 06New Developement 08 07 09 Re-sale 10 $2,000,000 Prudential douglas elliMan real estate MANhAttAN MArket overvIew NEW�DEVELOPMENT�MARKET�SHARE��MEDIAN�SALES�PRICE New Developement Re-sale 50% 2Q 10 $2,000,000 Median Sales Price 50% $1,600,000 40% CoNDo market $1,600,000 Median Sales Price 40% $1,200,000 30% Price indicators show mixed results The prior quarter. Price per square foot was $943 in $1,200,000 $800,000 30% 20% median sales price of a Manhattan condo the second quarter, 2.8% above $917 per square apartment was $1,100,000, 10.1% higher than the foot in the prior year quarter and 3.9% above the Price indicators mixed as number $800,000 20% 10% $400,000 Market Share New Development (Units) $999,000 median sales price in the prior year $908 price per square foot of the prior quarter. $400,000 $0 of sales jumped New Development 10 Market Share (Units) 10% 0% quarter and 3.3% higher than the $1,065,000 The East Side price per square 3Q 09 was the 4Q 09 2Q 09 foot 1Q 10 2Q Number of sales 10 surged as listing inventory median sales price of the prior quarter. Average highest of the four regions at $1,001 09 square 4Q 09 $0 2Q 09 3Q per 1Q 2Q 10 0% sales price followed a similar pattern, rising foot, essentially unchanged from $1,003 in the declined There were 1,553 sales in the second AVERAGE�PRICE�PER�SQ�FT�/�CO�OP Downtown East Side West Side Uptown $1,200 AVERAGE�PRICE�PER�SQ�FT�/�CO�OP quarter, 93.2% Side thanWest Side East more the 804 sales in the 9.5% to $1,680,236 in the second quarter, same period a year ago. Uptown jumped 24.9% Downtown Uptown from $1,534,031 in the same period a year ago to $653 per square foot from $523 per square prior year quarter and 22% more than the 1,273 $1,200 $1,000 and essentially unchanged from $1,690,399 foot, but was largely due to a shift in mix to larger sales in the prior quarter. The second quarter $1,000 $800 in the prior quarter. The rise in both of these apartments. Downtown averaged $910 per total was the highest since the second quarter $800 $600 indicators is consistent with the 14.1% increase square foot, 3.3% above the $881 per square foot 2008 total of 1,827. Condo sales accounted $600 $400 in the average square footage of apartments in the prior year quarter and the West Side was for 56.3% of all apartment sales in the second $400 sold over the past year. The second quarter 6.1% higher at $946 per square foot from $892 in quarter, just above the 52.1% five-year quarterly $200 average square footage of sold properties was the same period a year ago. $0 $200 2Q 09 3Q 09 average market share. There were 4,209 condo 4Q 09 1Q 10 2Q 10 1,482 square feet compared to 1,299 square feet $0 listings available 1Q 10 sale, excluding 10 for “shadow Days on market 09 2Q shortened as listing discount 3Q 09 LISTING�DISCOUNT�VS��DAYS�ON�MARKET�/�CO�OP 4Q 09 2Q in the prior year quarter, reflecting the shift in inventory”. The second quarter total was slips Co-op sales averaged 92 days on market, 20% 200 mix toward larger unit sales in 2010 from entry- LISTING�DISCOUNT�VS��DAYS�ON�MARKET�/�CO�OP down sharply from 141 days in the prior year 15.5% below the 4,979 listing total of the prior 20% level units in 2009. Because of the trend toward quarter and down from 110 days in the prior year quarter and essentially unchanged 175 from 200 16% larger unit sales, average price per square foot quarter. This is consistent with the rise in the 16% the prior quarter listing total of 4,218. This is 12% 175 150 showed a modest decline over the same period. number of sales and decline in available listing consistent with the five-year quarterly average of 150 Average price per square foot was $1,134 in the 12% inventory. Listing discount slipped to 7.3% from 4,207. Condos provided 51.6% of total available Days On Market 8% 125 second quarter, down 4% from $1,181 in the prior 8.7% in the prior year quarter, but was up from apartment listing inventory, also consistent125 with Days On Market 8% 4% Listing Discount 100 year quarter and down 1.7% from $1,154 in the 3.8% in the prior quarter. the 5-year 50.3% quarterly average. 4% Listing Discount 100 prior quarter. 0% 2Q 09 3Q 09 4Q 09 1Q 10 2Q 10 75 0% 2Q 09 3Q 09 4Q 09 1Q 10 2Q 10 75 Days on market fell sharply as listing discount AVERAGE�PRICE�PER�SQ�FT�/�CONDO Downtown East Side West Side Uptown rose The average days on market was 115 days, $2,500 AVERAGE�PRICE�PER�SQ�FT�/�CONDO Downtown East Side West Side Uptown more than 2 months faster than 181 days in the $2,500 $2,000 same period last year and nearly 3 weeks faster than the prior quarter average of 135 days. This $2,000 $1,500 is consistent with the rise in number of sales $1,500 $1,000 and decline in listing inventory over the same period. Listing discount expanded over the $1,000 $500 same period to 10.5% in the second quarter $500 $0 from 7% in the prior year quarter and 6.7% in 2Q 09 3Q 09 4Q 09 1Q 10 2Q 10 the prior quarter. The rise in listing discount $0 2Q 09 3Q 09 4Q 09 1Q 10 2Q 10 LISTING�DISCOUNT�VS��DAYS�ON�MARKET�/�CONDO reflects evidence that sellers are testing the 20% LISTING�DISCOUNT�VS��DAYS�ON�MARKET�/�CONDO 350 market by setting prices higher but are meeting 20% 16% 350 resistance from buyers and therefore have to 300 “travel further” to have a “meeting of the minds” 16% 300 12% Days On Market 250 over the contract sales price. 12% Days On Market 250 8% 200 8% Listing Discount 200 4% 150 4% Listing Discount 0% 150 100 2Q 09 3Q 09 4Q 09 1Q 10 2Q 10 0% 2Q 09 3Q 09 4Q 09 1Q 10 2Q 10 100 AVERAGE�PRICE�PER�SQ�FT�/�LUXURY AVERAGE�PRICE�PER�SQ�FT�/�LOFT COndO Market Matrix AVERAGE�PRICE�PER�SQ�FT�/�LUXURY Current Qtr $3,500 % ChgAVERAGE�PRICE�PER�SQ�FT�/�LOFT Prior Year Qtr $1,700 Prior Qtr % Chg COndO apartMent Mix % of Total Median Price Average Sales Price $3,000 $3,500 $1,680,236 -0.6% $1,500 $1,700 $1,690,399 9.5% $1,534,031 Studio 9% $444,000 Average Price per Square Foot $3,000 $1,134 -1.7% $1,300 $1,154 -4% $1,181 $2,500 $1,500 1 bedroom 31% $678,300 Median Sales Price $1,100,000 3.3% $1,065,000 10.1% $999,000 $2,000 $2,500 $1,100 $1,300 Number of Sales 1,553 22% 1,273 93.2% 804 2 bedroom 34% $1,350,000 $1,500 $2,000 $900 $1,100 Days on Market (from Last List Date) 115 -14.8% 135 -36.5% 181 $1,000 2Q 09 $700 $900 3 bedroom 22% $2,724,638 $1,500 Listing Discount (from Last List Price) 3Q 09 4Q 09 1Q 10 10.5% 2Q 10 2Q 096.7%3Q 09 4Q 09 1Q 10 7% 2Q 10 $1,000 2Q 09 Listing Inventory 4,209 -0.2% $700 4,2183Q 09 -15.5% 09 4,979 4+ bedroom 4% $5,850,000 3Q 09 4Q 09 1Q 10 2Q 10 2Q 09 4Q 1Q 10 2Q 10 Visit our website to browse listings and learn more about market trends prudentialelliman.com

- 4. 4% 40% 100 Listing Discount 30% 0% 2Q 09 3Q 09 4Q 09 1Q 10 2Q 10 75 2Q 10 MANhAttAN MArket overvIew 20% Prudential douglas elliMan real estate NEW�DEVELOPMENT�MARKET�SHARE��MEDIAN�SALES�P AVERAGE�PRICE�PER�SQ�FT�/�CONDO Downtown East Side West Side Uptown 10% $2,000,000 $2,500 Market Share New Development (Units) luxury market Median Sales Price $2,000 4Q 09 1Q 10 2Q 10 0% 1,502 listings in the prior quarter. Luxury listing listing discount and days on market declined $1,600,000 inventory trended in the opposite direction as The luxury market averaged 146 days on market, $1,500 Downtown East Side West Side Uptown the overall market in recent months, which had more than a month faster than the 182-day $1,200,000 Price indicators stabilized as listing $1,000 increased 1.6% from the prior quarter. average of the prior year quarter and the 193-day inventory dropped Price indicators showed mixed results The $800,000 prior quarter average. In 75% of the time over $500 Market share of higher end expanded as median sales price of a Manhattan luxury the past five years, the luxury market had longer $400,000 listing inventory 09 The luxury market began 4Q 09 $0 2Q fell 3Q 09 apartment was $4,093,365 in the second quarter, 1Q 10 2Q 10 marketing times than the overall market. The at the $3,000,000 threshold this quarter, 11.8% higher than the $3,660,608 in the prior year luxury market took 41 days longer to sell than the $0 LISTING�DISCOUNT�VS��DAYS�ON�MARKET�/�CONDO 1Q 09 2Q 09 3 representing the top 10% of all sales. Market quarter, but 10.7% below the $4,582,125 median overall market in the second quarter, higher than 20% 350 share of the high end market, which encompasses sales price of the prior quarter. Average sales the 10.6 additional days on market of the past the luxury market, 10 16% increased over2Q 10 past year price showed the same trend, rising 8.6% to the 300 five years. Listing discount was 6.4%, below the 4Q 09 1Q with 43% of all sales at or above $1,000,000, $5,169,161Market second quarter from $4,759,181 8.6% listing discount of the same period a year 12% Days On in the 250 compared to 38% in the same period a year ago. in the prior year quarter, but down 6.9% from ago, but higher than the 3.6% listing discount of The increased level of sales activity worked off $5,550,494 in the prior quarter. Average200 8% 200 price the prior quarter. excess inventory levels. There were 1,304175 4% Listing Discount listings per square foot was essentially unchanged at 150 Note: This sub-category is the analysis of the top ten percent of all over the $3,000,000 threshold in the second $1,843 in the second quarter compared to $1,848 co-op and condo sales. The data is also contained within the co-op and condo markets presented. 0% 2Q fewer than 1,844 listings150 the 09 quarter, 29.3%09 in 4Q in the prior year quarter and 2% 10 100 3Q 09 1Q 10 2Q below the $1,881 same period last Days On year and 13.2% fewer than the Market 125 result in the prior quarter. 100 AVERAGE�PRICE�PER�SQ�FT�/�LUXURY Luxury Market Matrix AVERAGE�PRICE�PER�SQ�FT�/�LOFT Current Qtr % Chg Prior Qtr % Chg Prior Year Qtr 4Q 09 $3,500 1Q 10 2Q 10 75 Average Sales Price $1,700 $5,169,161 -6.9% $5,550,494 8.6% $4,759,181 $3,000 Average Price per Square Foot $1,500 $1,843 -2% $1,881 -0.3% $1,848 Downtown East Side West Side Uptown Median Sales Price $4,093,365 -10.7% $4,582,125 11.8% $3,660,608 $2,500 $1,300 Number of Sales 276 17.4% 235 80.4% 153 $2,000 $1,100 Days on Market (from Last List Date) 146 -24.4% 193 -19.8% 182 $1,500 $900 Listing Discount (from Last List Price) 6.4% 3.6% 8.6% $1,000 2Q 09 3Q 09 4Q 09 1Q 10 2Q 10 $700 2Q 09 Listing Inventory 3Q 09 4Q 09 1Q 10 1,304 2Q 10 -13.2% 1,502 -29.3% 1,844 lofT market prior year quarter total of 737 listings and 1.4% but 2.1% above $1,121 in the prior quarter. below the 556 total of the prior quarter. This listing discount and days on market fell The trend corresponds to the surge in sales activity days on market for a loft apartment was 80 days Price indicators mixed as number 4Q 09 1Q 10 2Q 10 over the same period. in the second quarter, the fastest result posted of sales surged Price indicators were mixed, showing volatility in at least a decade and is consistent with the 350 Number of sales jumped as inventory declined The median sales price was $1,570,000 in the surge in sales and decline in listings. The second There were 262 loft sales in the second quarter, a 300 second quarter, 15.9% below $1,867,500 in the quarter results are approximately two months pronounced 263.9% increase from 72 sales in the Days On Market prior year quarter, but up 12.1% from $1,400,000 faster than the prior year quarter results of 138 250 prior year quarter and a 45.6% increase from 180 in the prior quarter. Average sales price was days and the prior quarter results of 146 days. 200 sales in the prior quarter. The second quarter $2,057,776 for the second quarter, 5.7% above Listing discount was 5.4% in the second quarter, represented a release of pent-up demand as the the $1,947,076 in the prior year quarter and 0.9% below 7.2% in the same period a year ago, but 150 number of sales exceeded the 193 sale quarterly above $2,040,263 in the prior quarter. Price per above 3.3% in the prior quarter. 4Q 09 100 average of the past 20 years. 10 1Q 10 2Q Listing inventory square foot was $1,145 in the second quarter, a Note: This sub-category is the analysis of all co-op and condo loft sales available. The data is also contained within the co-op and was 548 in the second quarter, 25.6% below the 4.3% decline from $1,197 in the prior year quarter, condo markets presented. AVERAGE�PRICE�PER�SQ�FT�/�LOFT LOft Market Matrix Current Qtr % Chg Prior Qtr % Chg Prior Year Qtr $1,700 Average Sales Price $2,057,776 0.9% $2,040,263 5.7% $1,947,076 $1,500 Average Price per Square Foot $1,145 2.1% $1,121 -4.3% $1,197 Median Sales Price $1,570,000 12.1% $1,400,000 -15.9% $1,867,500 $1,300 Number of Sales 262 45.6% 180 263.9% 72 $1,100 Days on Market (from Last List Date) 80 -45.2% 146 -42% 138 $900 Listing Discount (from Last List Price) 5.4% 3.3% 7.2% $700 2Q 09 3Q 09 4Q 09 1Q 10 2Q 10 Listing Inventory 548 -1.4% 556 -25.6% 737 ©2010 Prudential Douglas Elliman and Miller Samuel Inc. All worldwide rights reserved. easTsiDe 980 Madison Ave. 212.650.4800 • 575 Madison Ave. 212.891.7000 MiDTowN 425 East 58th St. 212.832.1666 Prudential douglas elliMan Miller saMuel inc. 205 East 42nd St. 212.692.6111 • 485 Madison Ave. 212.350.8500 wesTsiDe 1995 Broadway 212.362.9600 • 2142 Broadway real estate real estate aPPraisers 212.769.2004 • 2169 Frederick Douglass Blvd. 212.865.1100 DowNTowN 90 Hudson St. 212.965.6000 • 26 West 17 St. 575 Madison Avenue 21 west 38th Street New York, NY 10022 New York, NY 10018 212.645.4040 • 137 Waverly Pl. 212.206.2800 • 51 East 10 St. 212.995.5357 • 690 Washington St. 212.352.5252 BrooklyN 156 212.891.7000 212.768.8100 Montague St. 718.780.8100 • 189 Court St. 718.522.2929 • 299 Bedford Ave. 718.486.4400 • 154 Seventh Ave. 718.840.2000 prudentialelliman.com millersamuel.com 664 Fulton Street 718.780.8100 reNTal 485 Madison Ave. 212.350.8500 reloCaTioN 575 Madison Ave. 212.891.HOME For more information or electronic copies of this report please visit prudentialelliman.com/marketreports. Email report author Jonathan Miller ©2010. An Independently owned and operated member of the Prudential Real Estate Affiliates, Inc. is a service mark of Prudential Insurance Company of America Equal Housing Opportunity. All material presented herein is intended at jmiller@millersamuel.com with questions or comments. for information purposes only. While this information is believed to be correct, it is represented subject to errors, omissions, changes or withdrawal without notice. All property outlines and square footage in property listings are approximate.