The Grocery Eye - Snack Attack

The crisps and savoury snacks category is seen as a popular and innovative category to shop; and with shelves stacked high with a vast array of tempting treats, we’re helpless to resist this ever innovating category. It also presents a very competitive category, owing to cost increases and price promotions both within and across bag formats. In recent years health has been a key driver of npd as products are seen as high in salt, fat and calories. While purchase judgements based on detailed nutritional information are unlikely, it is a category where brand plays a stronger role than other food categories. The Grocery Eye examined the shopping habits of 2,000 supermarket shoppers to identify perceptions towards purchasing food and drink, as well as non-food products. It assessed the crisps and savoury snacks category to understand topics such as perceptions towards category innovation, product attributes and ingredients, as well as drivers and barriers to purchase. Check out our infographic which provides a top level overview of some key research findings across the crisps and savoury snacks category including: - Purchase motivators – from price and flavour to the role of product type and brand. - Category innovation – the route to discovery and what tempts first time buyers. - Drivers and barriers to purchase – what are the most important factors. - Future considerations – the features which will be important over the next 2 years. For a detailed overview of consumer perceptions across the crisps and savoury snacks sector and The Grocery Eye please call or email Catherine Elms, Research Director on +44(0)1865 336 400 or Catherine.elms@spafuturethinking.com

Recommended

More Related Content

Viewers also liked

Viewers also liked (10)

More from Future Thinking

More from Future Thinking (11)

Recently uploaded

Recently uploaded (20)

The Grocery Eye - Snack Attack

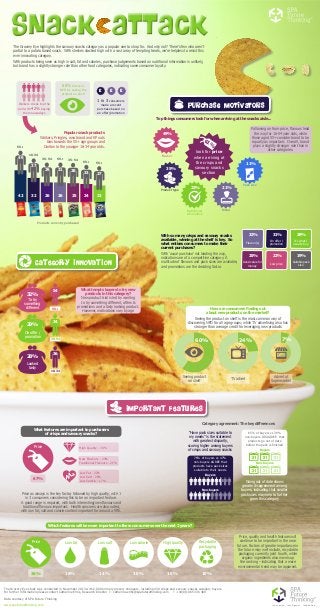

- 1. The Grocery Eye study was conducted in November 2013 with 2,000 primary grocery shoppers, including 430 crisps and savoury snacks category buyers. For further information please contact Catherine Elms, Research Director E: catherine.elms@spafuturethinking.com T: +44(0)1865 336 400 Data courtesy of SPA Future Thinking www.spafuturethinking.com innovation intelligence inspiration What tempts buyers to try new products in this category? New product trial is led by wanting to try something different, offers & promotions and a tasty looking product. However, motivations vary by age Snack attackSnack attack Popular snack products Walkers, Pringles, own brand and KP nuts bias towards the 55+ age groups and Doritos to the younger 16-34 year olds. Products currently purchased 42 32 26 26 25 24 22 49 55+ 37 16-34 29 35-54 31 55+ 28 35-54 33 55+ 27 55+ Purchase Motivators 60% discover NPD by seeing the product on shelf 1 in 3 consumers made a recent purchase based on an offer/promotion Walkers crisps top the poll with 42% buying them nowadays £ £ £ 22% Low price 31% On offer / promotion 32% Flavour(s) 29% It’s what I usually buy 25% Good value for money 19% Suitable pack size With so many crisps and savoury snacks available, winning at the shelf is key. So what entices consumers to make their current purchases? With ‘usual purchase’ not leading the way, indications are of a competitive category. A multitude of flavours and pack sizes are available, and promotions are the deciding factor. Top things consumers look for when arriving at the snacks aisle... Following on from price, flavours lead the way for 16-54 year olds, while those aged 55+ consider brand to be equally as important. Overall, brand plays a slightly stronger role than in other categories. look for price when arriving at the crisps and savoury snacks section 49% Flavour 61% 22% Nutritional information 21% Brand 35% Product type 11% Pack size The Grocery Eye highlights the savoury snacks category as a popular one to shop for. And why not? There’s few who aren’t partial to a potato based snack. With shelves stacked high with a vast array of tempting treats, we’re helpless to resist this ever innovating category. With products being seen as high in salt, fat and calories, purchase judgements based on nutritional information is unlikely, but brand has a slightly stronger role than other food categories, indicating some consumer loyalty. How are consumers finding out about new products on the market? Seeing the product on shelf is the most common way of discovering NPD for all age groups; while TV advertising also has stronger than average credit for leveraging new products 60% 24% 7% Seeing product on shelf TV advert Advert at Supermarket 32% To try something different 55+ 54 29% On offer / promotion 35-54 28% Looked tasty 16-34 34 36 IMPORTANT FEATURES What features are important to purchasers of crisps and savoury snacks? Price as always is the key factor, followed by high quality, with 1 in 3 consumers considering this to be an important feature. A good range is required, with both interesting/new flavours and traditional flavours important. Health concerns are also noted, with low fat, salt and calorie content important for around a fifth. Price 67% Low Fat - 22% Low Salt - 20% Low Calorie - 17% New Flavours - 24% Traditional Flavours - 21% High Quality - 34% CATEGORY INNOVATION Category agreement: The key differences Buyers 65% of buyers vs 39% non-buyers DISAGREE that products go out of date before the pack is finished Non-buyers 76% of buyers vs 47% non-buyers AGREE that products have pack sizes suitable to their needs Buyers Non-buyers “Have pack sizes suitable to my needs” is the statement with greatest disparity, scoring higher among buyers of crisps and savoury snacks Going out of date shows greater disagreement among buyers, indicating that smaller pack sizes may help to further grow this category Which features will be more important to these consumers over the next 2 years? Price 36% Low fat 16% Low salt 14% Low calorie 10% High quality 10% Recyclable packaging 10% Price, quality and health features will continue to be important in the near future. Factors of greater importance in the future may well include, recyclable packaging currently joint fourth, while organic ingredients also moves up the ranking – indicating that a more environmental trend may be apparent.