2. Costs

• In buying factor inputs (or factors of production), a

firm will incur costs.

• The cost of

– Labour (wages)

– Land (rent)

– Capital (interest)

– Enterprise (normal profit)

• Some of these costs are classified as:

– Fixed costs – costs that are not related directly to

production, eg land and fixed capital. Rent, rates, insurance

costs, admin costs are seen as fixed because they do not

change in relation to output

– Variable Costs – costs directly related to variations in output

eg wages and the cost of variable capital such as raw

materials primarily.

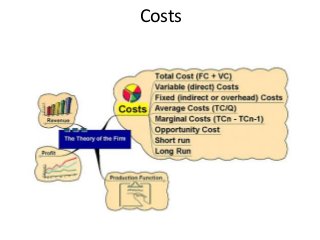

3. Costs

• Total Cost - the sum of all costs incurred in

production

• TC = FC + VC

• Average (Total) Cost – the cost per unit of output

• A(T)C = TC / Output

• A(T)C = AFC + AVC

• Marginal Cost – the cost of one more or one fewer

units of production

• MCn = TCn – TCn-1

4. Costs

• Short run – Diminishing marginal returns

results from adding successive quantities of

variable factors to a fixed factor

• Long run – Increases in capacity can lead to

economies or diseconomies of scale

6. Revenue

• Total revenue – the total amount received from

selling a given output

• TR = P x Q

• Average Revenue – the average amount received

from selling each unit

• AR = TR / Q

• AR is price

• Marginal revenue – the amount received from

selling one extra unit

of output

• MR = TRn – TR n-1

8. Profit

• The reward for enterprise

• Relating price to costs helps a firm to assess

profitability in production

• Profits help in the process of directing resources to

alternative uses in free markets.

• Profit measures the return to risk when committing

scarce resources to a market or industry. Entrepreneurs

take risks for which they require an adequate rate of

return. The higher the market risk and the longer they

expect to have to wait to earn a positive return, the

greater will be the minimum required return that an

entrepreneur is likely to demand.

9. Profit

• The standard assumption in economics is that

private sector businesses are profit-seeking /

profit maximisers. In reality pure profit

maximisation is a highly unlikely assumption to

hold and that a wide range of alternative

objectives are likely.

10. Normal profit

• Normal Profit – the minimum amount (transfer

earning or opportunity cost) required to keep a firm

in its current line of production.

• For instance normal profits need to reflect the

opportunity cost of using funds to finance a

business. £200,000 of savings invested into a

business could have earned a low-risk rate of return

by being saved in a bank account – that the rate of

interest would the minimum rate of return needed

or normal profit.

• Thus normal profit is the COST of enterprise and is

part of average cost just like rent, interest and wages.

11. Supernormal profit

• Supernormal (abnormal) profit occurs when profit

made is over and above normal profit

– Thus supernormal can be taxed away without altering

resource allocation.

– Supernormal profits are an incentive for other producers to

enter a market to try to acquire some of this profit.

– Thus supernormal profit only persists in the long run in

imperfectly competitive markets such as oligopoly and

monopoly where firms have the market power to

successfully block the entry of new firms.

– Thus supernormal profits may indicate the existence of

welfare losses

• Supernormal profit = TR – TC

12. Subnormal profit

• Sub-normal profit exists when profit below normal

profit

– Firms may not exit the market even if sub-normal

profits made if they are able to cover variable

costs

– Cost of exit may be high

– Sub-normal profit may be temporary (or perceived

as such!)

– Subnormal profit = TR < TC or price (average

revenue) < average cost

14. The function of profit in a market economy

• Finance for investment using retained especially when the alternatives

such as issuing new shares (equity) or bonds may not be attractive

depending on the state of the financial markets especially in the aftermath

of the credit crunch.

• Market entry: Rising profits send signals to other producers within a

market. When existing firms are earning supernormal profits, this signals

that profitable entry may be possible. In contestable markets, we may see a

rise in market supply and lower prices. In a monopoly, the dominant firm

may be able to protect their position through barriers to entry.

• Signals about the health of the economy as the profits made by businesses

throughout the economy provide important signals about the health of the

macroeconomy. Rising profits might reflect improvements in supply-side

performance (e.g. higher productivity or lower costs through innovation).

Strong profits are also the result of high levels of demand from domestic

and overseas markets. In contrast, a string of profit warnings from

businesses could be a lead indicator of a macroeconomic downturn.

15. Key revision points on profit

• By the time of the Unit 3 exam candidates should be able to:

– understand the links between market structure and profits

and the key role played by barriers to entry and exit

– understand how government intervention can affect profits

e.g. price regulation and policies that affect costs of

production

– be able to show how changes in AR/MR and changes in

MC/AVC/AC can affect the profit maximising equilibrium for a

business

– understand how macroeconomic variables affect profitability

e.g. the recession and changes in the exchange rate

– be able to explain and show how pricing strategies such as

price discrimination impact on revenues and profits