1. AUTOMOTIVE

The NPD Group’s Aftermarket Consumer Outlook Study

A Look into 2012

Use the eye dropper to capture type set

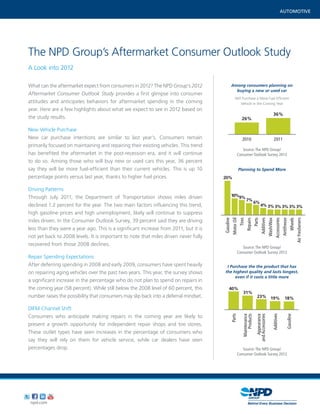

What can the aftermarket expect from consumers in 2012? The NPD Group’s 2012 Among consumers planning on

buying a new or used car

Use the eye dropper to capture type set

Aftermarket Consumer Outlook Study provides a first glimpse into consumer

Use the eye dropper to capture type set Will Purchase a More Fuel Efficient

attitudes and anticipates behaviorsFont for legend

for aftermarket spending in the coming Vehicle in the Coming36%

Year

26%

year. Here are a few highlights about what we expect to see in 2012 based on

Font for legend 36%

Font for legend

Font for chart values 36%

the study results. 26%

26%

Font for chart values

Font for chart values

Font for x-axis of chart 2010 2011

New Vehicle Purchase

New car purchase intentions Font for x-axis of chart year’s. Consumers remain

are similar to chart last

Font for x-axis title

2010 2011

Font for of 2010 2011

primarily focused on maintaining and repairing their existing vehicles. This trend

Font Fontpost-recession era, and it will continue

Fontfor title

Source: The NPD Group/

has benefited the aftermarket in for title —title

the for subhead Consumer Outlook Survey 2012

to do so. Among those whoFontfor title — or used cars this year, 36 percent

will buy new subhead

Font for title —subhead

say they will be more fuel-efficient than their current vehicles. This is up 10 20% Planning to Spend More

percentage points versus last year, thanks to higher fuel prices. 20%

20%

10%9%

Driving Patterns 7%

10%9% 6%

Through July 2011, the Department of Transportation shows miles driven 10%9% 4% 3% 3% 3% 3% 3%

7%

7% 6%

declined 1.2 percent for the year. The two main factors influencing this trend, 6% 4%

4% 3% 3% 3% 3% 3%

3% 3% 3% 3% 3%

Gasoline

MotorOil Oil

Tires Tires

Repairs

Parts Parts

Additives

Wash/Wax

Accessories

Antifreeze

Wheels

Air Fresheners

high gasoline prices and high unemployment, likely will continue to suppress

MotorMotor

Gasoline

Oil

Tires

Repairs

Parts

Additives

Wash/Wax

Accessories

Antifreeze

Wheels

Air Fresheners

miles driven. In the Consumer Outlook Survey, 39 percent said they are driving

Gasoline

Repairs

Additives

Wash/Wax

Accessories

Antifreeze

Wheels

Air Fresheners

less than they were a year ago. This is a significant increase from 2011, but it is

not yet back to 2008 levels. It is important to note that miles driven never fully

recovered from those 2008 declines.

Source: The NPD Group/

Consumer Outlook Survey 2012

Repair Spending Expectations

After deferring spending in 2008 and early 2009, consumers have spent heavily I Purchase the the product that has

on repairing aging vehicles over the past two years. This year, the survey shows the highest quality and lasts longest,

even if it costs a little more

a significant increase in the percentage who do not plan to spend on repairs in

the coming year (58 percent). While still below the 2008 level of 60 percent, this 40%

31%

number raises the possibility that consumers may slip back into a deferral mindset. 40%

40% 23% 19% 18%

31%

23% 19%

DIFM Channel Shift 18%

Consumers who anticipate making repairs in the coming year are likely to

Parts Parts

Maintenance

Products

Appearance

and Accessories

Additives

Gasoline

present a growth opportunity for independent repair shops and tire stores.

Maintenance

and Accessories

Products

Appearance

Additives

Gasoline

These outlet types have seen increases in the percentage of consumers who

say they will rely on them for vehicle service, while car dealers have seen

percentages drop. Source: The NPD Group/

Consumer Outlook Survey 2012

npd.com

2. AUTOMOTIVE

OFFICE SUPPLIES

Oil Change Interval Continues to Lengthen About The NPD Group, Inc.

Consumers are tracking their mileage or months between oil changes by window The NPD Group is the leading provider of

stickers (57 percent), car service vehicle indicator lights (10 percent), or on their reliable and comprehensive consumer

own (31 percent). Regardless of method, the average interval between oil and retail information for a wide range

changes keeps increasing gradually. In the Consumer Outlook Survey, consumers of industries. Today, more than 1,800

reported changing their oil on average every 4,058 miles or 5.1 months. manufacturers, retailers, and service

companies rely on NPD to help them

Spending Intentions for Key Categories

Consumers today are more certain about spending for 2012, whether drive critical business decisions at the

indicating they would spend more or less next year than they did this year. global, national, and local market levels.

This decisiveness stems from greater awareness of spending more on needed NPD helps our clients to identify new

parts, maintenance, and repair and greater determination to spend less on business opportunities and guide product

discretionary items. development, marketing, sales, merchan-

dising, and other functions. Information

Attribute Importance

is available for the following industry

Today’s consumer is looking for value in a difficult economy, but value is not

sectors: automotive, beauty, entertain-

being determined solely by low price. Quality was the only attribute measured in

ment, fashion, food, home and office,

the survey that saw an increase in importance. Forty-five percent of consumers

said a product “made with quality materials” was very important — a four sports, technology, wireless,

percent increase since 2009. It is not surprising then that more consumers toys, and video games. For more

indicated that in many key categories, they’d be willing to pay more for a information, visit npd.com.

quality product that lasts longer.

Industry Expertise

The NPD Group is the premium provider of consumer and retail information

for the North American automotive aftermarket, petroleum marketing, and

convenience retailing industries. NPD expertise and data provide industry leaders

with essential market information to assist in making more effective business

decisions. NPD is uniquely qualified to help marketers apply information to

address key marketplace issues from multiple perspectives, based on more than

20 years of experience in these industries.

NPD’s diverse portfolio of services includes consumer panel tracking and

national and Store Level retail point-of-sale (POS) tracking. Specifically, NPD

information supports benchmarking, competitive analysis, assortment and

product planning, and identification of new channel opportunities.

Learn more.

For more information about The NPD Group’s products and services for the automotive

aftermarket industry, please contact your NPD account representative, call

Charles Camaroto at 866-444-1411, or email contactnpd@npd.com.

1011

npd.com