+971565801893>>SAFE ORIGINAL ABORTION PILLS FOR SALE IN DUBAI,RAK CITY,ABUDHA...

NEPT Catalyst Research | June 18, 2012

1. Joseph Pantginis, Ph.D., (646) 358-1907

jpantginis@roth.com

Raluca Pancratov, Ph.D., (646) 358-1914

rpancratov@roth.com

Sales (800) 933-6830, Trading (800) 933-6820

COMPANY NOTE | EQUITY RESEARCH | May 22, 2012

Healthcare: Biotechnology

Neptune Technologies & Bioressources | NEPT - $2.91 - NASDAQ

| Buy

Company Update

Stock Data NEPT: Further Steps to Strengthen IP and

52-Week Low - High $2.02 - $4.66 Commercial Profile for NKO

Shares Out. (mil) 49.69

Mkt. Cap.(mil) $144.6 Neptune filed for Reexamination of an Australian patent granted to its

3-Mo. Avg. Vol. 108,092 competitor Aker. Neptune believes that the claims of Aker's patent are

12-Mo.Price Target $9.00 obvious, given previous opinions of the U.S. and European Patent Offices,

Cash (mil) $17.7 and its activities do not infringe Aker's IP Separately, Neptune obtained the

.

Tot. Debt (mil) $0.0 sustainability certification "Friend of the Sea" that can be extended to its krill

EPS $ oil distributors.

Yr Feb —2011— —2012E— —2013E— Event

Curr Curr Neptune requested re-examination of the AU2008231570 Australian patent

1Q 0.01A (0.03)A (0.02)E granted to competitor Aker Biomarine, as it believes the claims of this patent

2Q 0.01A (0.04)A (0.02)E

are obvious given prior publications and patents. According to Neptune, its

3Q 0.04A (0.01)A (0.01)E

activities do not infringe its competitor's patents, but the company believes that

4Q (0.04)A (0.01)E 0.02E

YEAR 0.01A (0.09)E (0.03)E

Aker's claims are invalid, based on previously issued European and U.S. patent

P/E NM NM NM office opinions. Separately, Neptune obtained a sustainability certification from

the international organization "Friends of the Sea", which will enable the

Revenue ($ millions) company and the distributors of NKO to label products as "eco-friendly".

Yr Feb —2011— —2012E— —2013E— Impact

Curr Curr

We view as positive Neptune's proactive efforts to maintain its strong IP

1Q 4.2A 4.3A 5.2E

position in Australia. We also believe Neptune benefits from key patents

2Q 4.1A 4.4A 5.3E

3Q 4.3A 5.1A 6.6E

issued in the U.S. covering krill-derived omega-3 phospholipids, active and

4Q 4.1A 5.2E 9.5E enforceable even while undergoing re-examination by the USPTO at Aker's

YEAR 16.7A 18.9E 26.5E request. With the sustainability certification and eco-friendly label, NKO may

see an expansion of its commercial profile, in our belief. Neptune's efforts in

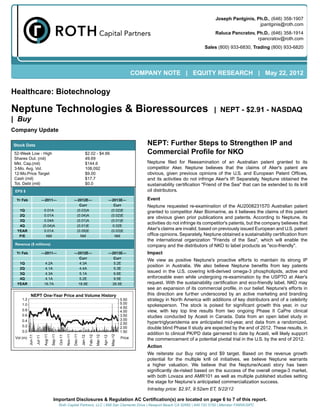

NEPT One-Year Price and Volume History this direction are further underscored by an active marketing and branding

1.2 5.50 strategy in North America with additions of key distributors and of a celebrity

1.0 5.00

4.50

spokesperson. The stock is poised for significant growth this year, in our

0.8 4.00 view, with key top line results from two ongoing Phase II CaPre clinical

0.6 3.50 studies conducted by Acasti in Canada. Data from an open label study in

0.4 3.00

2.50 hypertriglyceridemia are anticipated mid-year, and data from a randomized,

0.2 2.00 double blind Phase II study are expected by the end of 2012. These results, in

0.0 1.50

addition to clinical PK/PD data garnered to date by Acasti, will likely support

Aug-11

Sep-11

Nov-11

Dec-11

May-12

Jun-11

Feb-12

Mar-12

Oct-11

Jan-12

Apr-12

Jul-11

Vol (m) Price the commencement of a potential pivotal trial in the U.S. by the end of 2012.

Action

We reiterate our Buy rating and $9 target. Based on the revenue growth

potential for the multiple krill oil initiatives, we believe Neptune warrants

a higher valuation. We believe that the Neptune/Acasti story has been

significantly de-risked based on the success of the overall omega-3 market,

with both Lovaza and AMR101 as well as multiple published studies setting

the stage for Neptune’s anticipated commercialization success.

Intraday price: $2.97, 9:52am ET, 5/22/12

Important Disclosures & Regulation AC Certification(s) are located on page 6 to 7 of this report.

Roth Capital Partners, LLC | 888 San Clemente Drive | Newport Beach CA 92660 | 949 720 5700 | Member FINRA/SIPC

2. NEPTUNE TECHNOLOGIES & BIORESSOURCES Company Note - May 22, 2012

VALUATION

We reiterate our Buy rating and $9.00 price target. Our valuation of Neptune is based on a sum of the parts

analysis:

s Probability weighted clinical net present value (NPV) model of the pharmaceutical, CaPre, initial cardiovascular

opportunity with Neptune’s Acasti subsidiary.

s A discounted earnings valuation on Neptune’s core revenue and earnings on the sale of bulk krill oil (primarily

NKO currently).

Factors that could impede shares of Neptune from reaching our price target include negative data readouts

from ongoing clinical studies, any perceived delays in the CaPre regulatory path as well as Neptune's ability to

continue to fund its operations and monetize its expansion plans for NKO manufacturing.

RISKS

s Capacity expansion. Neptune is currently at or near full capacity in the manufacturing of NKO. The company

is now in the expansion phase for its Sherbrooke Canada facility with the goal of taking the current capacity of

130,000 kg per year to >400,000 kg per year in 2014 and approximately doubled over the next year. In line with

this capacity expansion is the expectation for increased revenue growth. Any potential delays in the timelines

in building out the expansion could have a deleterious effect on the company’s business model.

s Time behind the competition. The medical benefits of omega-3’s, specifically pharmaceutical grade

formulations (Lovaza, AMR101, CaPre) have been shown in multiple clinical trials. Drugs such as Lovaza

have laid important groundwork as the market prepares for additional and differentiated products. To this end,

AMR101 has the potential to significantly impact Lovaza’s market share, in our belief. Neptune/Acasti’s CaPre

is entering a large Phase II study in high triglyceride patients. Therefore the product is several years behind

AMR101 for potential commercialization.

s Market perception and education for differentiated profile of krill oil (NKO/CaPre). While potential CaPre

pharmaceutical sales should be driven by physician prescribing habits for patients with high triglycerides, we

believe patients still need to be educated about the differentiation of krill oil compared to the multitude of

omega-3 products available both off the shelf and through Lovaza and potentially AMR101 prescriptions. While

we do not believe this is a large risk for the company, Neptune/Acasti will need to be cognizant of addressing

the market properly.

s Financing and clinical trial risks. As with all drug development companies the need to continually fund drug

development exists. Should Neptune not be able to secure sufficient funding to grow its underlying business, it

could significantly impact the valuation of the shares. The company does have the potential to offset this risk by

having a revenue stream which is expected to grow from the sale of bulk krill oil to distributors and subsidiaries.

Additionally the pharmaceutical development pathway being pursued by Acasti and NeuroBioPharm are critical

to Neptune's success. Any failed or inconclusive clinical trials could significantly impact Neptune's shares.

COMPANY DESCRIPTION

Neptune Technologies & Bioressources Inc. researches, develops and commercializes proprietary bioactive

ingredients and products with the goal of superior added-value and clinically proven health benefits. The

Company extracts a range of bioactive ingredients such as novel proprietary omega-3 phospholipids from

abundant yet underexploited marine biomass including Krill, a cold deep water zooplankton. Neptune’s

first commercially available product is Neptune Krill Oil (NKO®), which represents marine based omega-3

phospholipids with potential in cardiovascular, cognitive and anti-inflammatory disorders. Neptune is pursuing

market opportunities in the nutraceutical market including dietary supplements and functional foods. The

Company is also pursuing opportunities in the pharmaceutical market through its pharmaceutical subsidiaries,

Acasti and NeuroBioPharm (including medical food, over-the-counter and prescription drug applications).

Page 2 of 7

6. NEPTUNE TECHNOLOGIES & BIORESSOURCES Company Note - May 22, 2012

Regulation Analyst Certification ("Reg AC"): The research analyst primarily responsible for the content of this report certifies

the following under Reg AC: I hereby certify that all views expressed in this report accurately reflect my personal views about

the subject company or companies and its or their securities. I also certify that no part of my compensation was, is or will be,

directly or indirectly, related to the specific recommendations or views expressed in this report.

Disclosures:

ROTH makes a market in shares of Neptune Technologies & Bioressources and as such, buys and sells from customers on

a principal basis.

On September 28, 2010, ROTH changed its rating system in order to replace the Hold rating with Neutral.

On May 26, 2011, ROTH changed its rating system in order to incorporate coverage that is Under Review.

Each box on the Rating and Price Target History chart above represents a date on which an analyst made a change to a

rating or price target, except for the first box, which may only represent the first note written during the past three years.

Distribution Ratings/IB Services shows the number of companies in each rating category from which Roth or an affiliate

received compensation for investment banking services in the past 12 month.

Distribution of IB Services Firmwide

IB Serv./Past 12 Mos.

as of 05/22/12

Rating Count Percent Count Percent

Buy [B] 185 70.34 59 31.89

Neutral [N] 61 23.19 6 9.84

Sell [S] 1 0.38 0 0

Under Review [UR] 16 6.08 8 50.00

Our rating system attempts to incorporate industry, company and/or overall market risk and volatility. Consequently, at any

given point in time, our investment rating on a stock and its implied price movement may not correspond to the stated 12-

month price target.

Ratings System Definitions - ROTH employs a rating system based on the following:

Buy: A rating, which at the time it is instituted and or reiterated, that indicates an expectation of a total return of at least

10% over the next 12 months.

Neutral: A rating, which at the time it is instituted and or reiterated, that indicates an expectation of a total return between

negative 10% and 10% over the next 12 months.

Sell: A rating, which at the time it is instituted and or reiterated, that indicates an expectation that the price will depreciate by

more than 10% over the next 12 months.

Under Review [UR]: A rating, which at the time it is instituted and or reiterated, indicates the temporary removal of the prior

rating, price target and estimates for the security. Prior rating, price target and estimates should no longer be relied upon for

UR-rated securities.

Not Covered [NC]: ROTH does not publish research or have an opinion about this security.

Page 6 of 7

7. NEPTUNE TECHNOLOGIES & BIORESSOURCES Company Note - May 22, 2012

ROTH Capital Partners, LLC expects to receive or intends to seek compensation for investment banking or other business

relationships with the covered companies mentioned in this report in the next three months. The material, information and facts

discussed in this report other than the information regarding ROTH Capital Partners, LLC and its affiliates, are from sources

believed to be reliable, but are in no way guaranteed to be complete or accurate. This report should not be used as a complete

analysis of the company, industry or security discussed in the report. Additional information is available upon request. This is

not, however, an offer or solicitation of the securities discussed. Any opinions or estimates in this report are subject to change

without notice. An investment in the stock may involve risks and uncertainties that could cause actual results to differ materially

from the forward-looking statements. Additionally, an investment in the stock may involve a high degree of risk and may not

be suitable for all investors. No part of this report may be reproduced in any form without the express written permission of

ROTH. Copyright 2012. Member: FINRA/SIPC.

Page 7 of 7