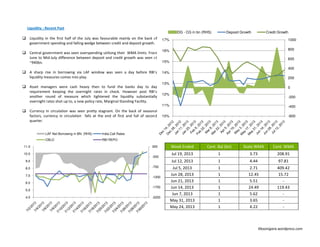

1. Liquidity in the first half of the July was favourable mainly on the back of

government spending and falling wedge between credit and deposit growth.

Central government was seen overspending utilising their WMA limits. From

June to Mid-July difference between deposit and credit growth was seen at

~940bn.

A sharp rise in borrowing via LAF window was seen a day before RBI’s

liquidity measures comes into play.

Asset managers were cash heavy then to fund the banks day to day

requirement keeping the overnight rates in check. However post RBI’s

another round of measure which tightened the liquidity substantially

overnight rates shot up to, a new policy rate, Marginal Standing Facility.

Currency in circulation was seen pretty stagnant. On the back of seasonal

factors, currency in circulation falls at the end of first and full of second

quarter.

Liquidity : Recent Past

-600

-400

-200

0

200

400

600

800

1000

10%

11%

12%

13%

14%

15%

16%

17%

DG - CG in bn (RHS) Deposit Growth Credit Growth

-2200

-1700

-1200

-700

-200

300

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

LAF Net Borrowing in BN. (RHS) India Call Rates

CBLO RBI REPO

Week Ended Cent. Bal (bn) State WMA Cent. WMA

Jul 19, 2013 1 3.73 208.91

Jul 12, 2013 1 4.44 97.81

Jul 5, 2013 1 2.71 409.42

Jun 28, 2013 1 12.45 15.72

Jun 21, 2013 1 5.51 -

Jun 14, 2013 1 24.49 119.43

Jun 7, 2013 1 5.62 -

May 31, 2013 1 3.65 -

May 24, 2013 1 4.22 -

Kbsonigara.wordpress.com

2. Rupee, post Fed’s intention of tapering bond buying earlier than

expected, depreciated by ~9.5%. Meanwhile it touched an all time

low of 61.17.

Volatility in currency markets increased. FIIs started pulling funds not

only from debt markets but from equity as well. Banks and large

domestic players were seen speculating on the currency as the cost of

fund was low enough to provide good arbitrage opportunity.

Thereafter RBI announced two set of measures. First on 16th when it

raised MSF by 200bps, capped LAF borrowing at 1% of total NDTL and

an OMO of 120bn. Second on 23rd when it reduced LAF limit to 0.5%

of individual NDTL and tweaked CRR requirement norms.

Falling incremental credit to deposit ratio is expected to add liquidity

into the system going ahead. RBI will be releasing dividend to

government which if released immediately via spending may help

liquidity ease further.

Liquidity : Recent Measures & Outlook

7.5

8.0

8.5

9.0

9.5

10.0

10.5

11.0

11.5

IN 3M CD (in %) IN 1Y CD (in %)

liquidity ease further.

Source : RBISource : RBI

Kbsonigara.wordpress.com

3. Short term rates in July rose substantially following RBI’s measure to

tighten liquidity in a bid to curb currency volatility.

Liquidity is mainly guided by factors like currency in circulation, difference

between deposit and credit growth and government spending.

Credit growth is expected to falter for the near future on the back of

economic uncertainty and fall in aggregate demand. Incremental credit

to deposit ratio is expected to follow a receding bias. Also to note, few

banks have raised short term interest rates. Few are believed to be

contemplating.

Currency in circulation is expected to reduce adding liquidity into the

system. Currency in circulation in June-Aug 2012 added ~166bn into the

system and in June – 19th July 2013 it supported liquidity by ~96bn.

Government is expected to receive substantial amount from the central

bank as dividend by second week of August. Since the dividend amount

Liquidity : Recent Measures & Outlook

Cash Inflows in Crs.

Date Instrument Payment Amount

1-Aug Tbills Redemption 11861

1-Aug SDLs Interest 104

2-Aug Gsec&SDLs Interest 8838

3-Aug SDLs Interest 244

5-Aug SDLs Interest 489

6-Aug SDLs Interest 520

7-Aug Gsec Interest 685

8-Aug SDLs Interest 687

8-Aug Tbills Redemption 25525

10-Aug Gsec&SDLs Interest 3127

12-Aug Gsec Interest 336

14-Aug SDLs Interest 1288

14-Aug T-bills Redemption 10531

bank as dividend by second week of August. Since the dividend amount

forms a part of non-monetary liabilities of RBI, it has no effect when the

same is transferred into government’s account. However liquidity will get

impacted if at all government continues to spend on a continuous basis.

Money market inflows and outflows on the right deciphers liquidity will be

on the easing bias given heavy inflow is expected into the system in next

couple of weeks.

Government, post 10th August is expected may turn more comfortable in

rejecting bids given cash balance will improve on the back of RBIs fund

transfer.

Overall liquidity, for now, seems will remain stable with an easing bias

given all major factors are on the supporting side. However continuous

volatility in the currency may compel RBI to suck liquidity either via a CRR

hike or an OMO.

14-Aug T-bills Redemption

16-Aug Gsec&SDLs Interest 8391

17-Aug SDLs Interest 2573

Total 75199

Cash Outflow in Crs.

Date Instrument Amount

1-Aug 7D CMB 3000

2-Aug G-sec Auction 15000

7-Aug T-bills Auction 12000

9-Aug G-sec Auction 15000

14-Aug T-bills Auction 12000

16-Aug G-sec Auction 16000

Total 73000

State may sell ~100bn on 13th Aug

Kbsonigara.wordpress.com