1. India : Macro update

Core Combined CPI

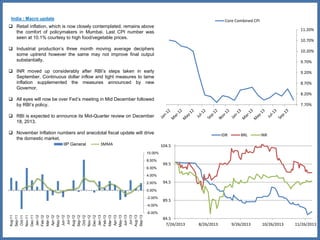

Retail inflation, which is now closely contemplated, remains above

the comfort of policymakers in Mumbai. Last CPI number was

seen at 10.1% courtesy to high food/vegetable prices.

11.20%

10.70%

Industrial production’s three month moving average deciphers

some uptrend however the same may not improve final output

substantially.

10.20%

9.70%

INR moved up considerably after RBI’s steps taken in early

September. Continuous dollar inflow and tight measures to tame

inflation supplemented the measures announced by new

Governor.

9.20%

8.70%

8.20%

All eyes will now be over Fed’s meeting in Mid December followed

by RBI’s policy.

7.70%

RBI is expected to announce its Mid-Quarter review on December

18, 2013.

November Inflation numbers and anecdotal fiscal update will drive

the domestic market.

IIP General

3MMA

IDR

BRL

INR

104.5

10.00%

8.00%

99.5

6.00%

4.00%

2.00%

94.5

0.00%

-2.00%

89.5

-4.00%

Aug-11

Sep-11

Oct-11

Nov-11

Dec-11

Jan-12

Feb-12

Mar-12

Apr-12

May-12

Jun-12

Jul-12

Aug-12

Sep-12

Oct-12

Nov-12

Dec-12

Jan-13

Feb-13

Mar-13

Apr-13

May-13

Jun-13

Jul-13

Aug-13

Sep-13

-6.00%

84.5

7/26/2013

8/26/2013

9/26/2013

10/26/2013

11/26/2013

2. India : Fiscal Deficit

2012

Fiscal worries continue to mount as anecdotal data adds not respite.

Apr-Oct Fiscal deficit for current year was seen at ~84.4% of BE

compared to ~72% in previous year.

2013

50%

45%

Cum. Total Receipts w.r.t. BE

40%

As budget estimate was drawn considering a GDP growth of 6%+,

substantial fall in the same is only escalating fiscal fears.

35%

30%

On the revenue side government is seen working hard however there

is no considerable movement to counter incremental expenses.

25%

20%

Recent media reports suggest that government is contemplating to cut

its plan expenditure by ~800bn. Last year plan expenditure was

reduced by ~900bn. As per latest release(Apr-Oct) government had

spend ~48% of plan expenditure. Among plan expenditure rural

ministry will take a heavy hit if government go with planned austerity.

Government finally may resort to faulty accounting practices to limit

the deficit figure at 4.8%. Remember FM have been promising

domestic and foreign investors to keep the macroeconomic situation

in control.

15%

10%

5%

0%

Apr

May

June

July

2012

Aug

2013

Sep

Oct

90%

In addition to shifting current year’s expenditure to next year

government is also taking its own time to refund tax. Chidambaram

quite ago said that this year refunds have totaled Rs 57,000 crore till

mid-December against last year’s Rs 70,000 crore..

80%

Cum. Fiscal Deficit w.r.t. BE

70%

60%

Department/Ministry

BE FY14

Spending w.r.t. BE (AprOct)

Finance

507116

47%

Defence

253345

60%

30%

Food

91091

87%

20%

Fertilizers

66183

75%

Petroluem

65145

84%

50%

40%

10%

0%

Source : CGA

Apr

May

June

July

Aug

Sep

Oct

3. Indian Debt Market

Yield on 7.16%GS2023 rose by ~35bps in the previous month on the

back of high inflation and announcement of a new benchmark.

Participants expected RBI to come out with new paper in the next

calendar year.

G-sec

Change in bps

Yield (RHS)

50

Conventionally RBI boosts reserve money in the second half of the

fiscal by buying Gsec however this time RBI refrained from announcing

back to back OMOs and preferred to buy dollars subsequently

supporting liquidity.

45

Spread at the long end of the corporate bond curve narrowed primarily

due to new gilt benchmark. Low supply with decent demand from

regular buyers(PF, Insurers & Retirement funds) supplemented spread

narrowing.

9.4

30

PDs and Asset managers were top sellers in the Gsec market. PDs

preferred remaining light as sentiment continues to remain weak.

Dynamic/Income reduced exposure to duration heavy gilt by the reason

of low OMO hopes and lack of liquid papers.

9.2

40

9.0

35

8.8

25

8.6

20

15

8.4

10

8.2

5

Upcoming Inflation number and fiscal talks will drive bond yields. We

believe 50% of rate hike is already priced in at current juncture. RBI’s

action and guidance will remain key for the market.

0

Net Buy/Sell in Crs. (1-29Nov)

Entities

Gsec

T-bills

8.0

1Y

3Y

5Y

10Y

14Y

24Y

30Y

Corporate Bond Spread (Bps) as on Nov'13 end

SDLs

Total

Foreign Banks

-10664

-1152

-988

-12804

Public Sector Banks

19792

2818

2960

25570

Private Sector Banks

3701

-174

456

3983

Mutual Funds

-7183

7793

-1567

7836

2457

1635

11928

-13641

-11742

-2496

-27879

AAA

Month

Ago

AA+

Month

Ago

AA

Month

Ago

AA-

Month

Ago

1

84

86

96

99

110

111

127

127

3

97

91

109

106

121

119

137

135

5

77

76

88

90

101

104

118

120

10

30

65

43

79

56

95

74

111

-957

Others

Tenor

Primary Dealers