International comparison of_productivity_jari_hyvärinen_pdf

1. International Comparison of Productivity 2013

Jari Hyvärinen

The developed countries are taking new steps to operate in economic

circumstances in which the labour force is decreasing and physical investments are

becoming less competitive. In these countries, the only way to improve economic

growth is to develop mechanisms that improve labour productivity and intangible

capital.

Labour productivity is calculated from terms of 1) value added, 2) value added

deflator, and 3) working hours. We use a methodology that establishes the

productivity level to the year 2007. Cross-sectional comparisons for 2007 are made

by using Eurostat SBS and LCS data (Hyvärinen, 2011). Comparisons for other years

are computed using productivity time series that are obtained from OECD STAN,

Rev. 4. Productivity growth is shown as a productivity time series for 1975–2011.

Comparing Finland to other industrialised countries, we find that productivity

growth in key industrial sectors in Finland has increased more rapidly than in the

OECD benchmark countries on the long run.

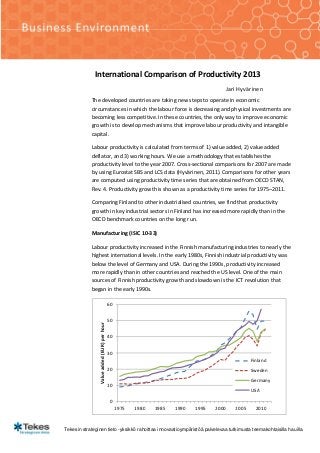

Manufacturing (ISIC 10-33)

Labour productivity increased in the Finnish manufacturing industries to nearly the

highest international levels. In the early 1980s, Finnish industrial productivity was

below the level of Germany and USA. During the 1990s, productivity increased

more rapidly than in other countries and reached the US level. One of the main

sources of Finnish productivity growth and slowdown is the ICT revolution that

began in the early 1990s.

60

50

Value added (EUR) per hour

40

30

Finland

20 Sweden

Germany

10

USA

0

1975 1980 1985 1990 1995 2000 2005 2010

Tekesin strateginen tieto -yksikkö rahoittaa innovaatioympäristöä palvelevaa tutkimusta teemakohtaisilla hauilla.

2. Wood and wood products (ISIC 16 )

The productivity level of the wood and wood product industries in Finland for

2007 was almost parallel with Sweden’s level. Afterwards, development in Finland

has been more moderate than in Sweden. In these comparisons, US productivity

appears to be surprisingly low. Further examination is required to determine why

the productivity level of the US wood industries was exceptionally low in 2007.

50

Finland

40 Sweden

Value added (EUR) per hour

Germany

30 USA

20

10

0

1975 1980 1985 1990 1995 2000 2005 2010

Pulp, paper and paper products (ISIC 17)

In the pulp and paper industries, we used the 2007 level, although there were

radical shifts in productivity levels compared with other studies.2 Finland has a

clear productivity advantage, but in the 2007 comparisons, the Swedish pulp and

paper industries were at the highest level. The pulp and paper industries are highly

capital-intensive industries. However, during the 2000s, the Finnish pulp and paper

industries underwent several stages of reorganisation that increased productivity

growth.

80

Finland

70

Sweden

60

Germany

50 USA

EUR

40

30

20

10

0

1975 1980 1985 1990 1995 2000 2005 2010

Tekes Strategic Intelligence Unit

3. Basic metals (ISIC 24)

In basic metals, the rapid growth and slump of basic metals exported from Finland

has affected rapid changes in value added even if working hours have remained

stable. In other countries, volatility has been less strong than in Finland. Main steel

producers are China, Japan, the US, India, Russia, South Korea and Germany. Their

share is 77 per cent of World production (ETLA 2012).

120

Finland

100

Sweden

80 Germany

USA

60

40

20

0

1975 1980 1985 1990 1995 2000 2005 2010

Fabricated metal products (ISIC 25)

One of the main producers in these industries is Germany, where also productivity

is strong. The main export countries from Finland are Russia, China, Sweden, the

US and Germany (ETLA 2012). The Finnish productivity has been an average while

in productivity rankings Finland is above Sweden and at the same level than the

US. The productivity has remained rather stable during the crisis.

60

Finland

50 Sweden

Germany

40

USA

30

20

10

0

1975 1980 1985 1990 1995 2000 2005 2010

Tekes Strategic Intelligence Unit

4. Electrical Equipment (ISIC 27)

Electric equipment includes electric motors, generators, transformers etc (271),

batteries and accumulators (272), wiring and wiring devices (273), electric lighting

equipment (274), domestic appliances (275) and other electrical equipment (279).

In the 2000s, the productivity growth has been strong in Finland, but productivity

has been at high level in Sweden since the 1970s. In Finland, exports of electrical

equipment has reached 50 per cent share in electrical machinery (ETLA 2012).

80

Finland

70

Sweden

60

Germany

50 USA

EUR

40

30

20

10

0

1975 1980 1985 1990 1995 2000 2005 2010

Machinery and equipment (ISIC 28)

In the US and Swedish machinery and equipment industries, the level of

productivity in 2007 was dramatically lower than in 2004 and in other productivity

comparisons (Kaitila et al.,2008). With regard to productivity growth, the fastest

improvement in productivity was observed in the Finnish industries during the

2000s. The Finnish machinery has succeeded well during the crisis.

50

Finland

40 Sweden

Germany

30 USA

EUR

20

10

0

1975 1980 1985 1990 1995 2000 2005 2010

Tekes Strategic Intelligence Unit

5. Computer, Electronic and Optical products (ISIC 26)

Electrical and optical equipment includes electronic components and boards (261),

computers and peripheral equipment (262), communication equipment (263),

consumer electronics (264), and various optical products (265-268). In these

industrial sectors, many price indices were unavailable or unreliable. Therefore,

we show only the aggregate productivity of computer, electronic and optical

products.

The most productive sector has been the ICT industry in Finland, Sweden and the

US, which has demonstrated record-breaking productivity growth since the ICT

revolution began in the 1990s. Technology improvements in mobility, wired and

wireless telecommunications, communication processes and data recording are

the ICT characteristics that have significantly improved productivity in Finland

(Maliranta, 2004; Maliranta – Rouvinen, 2004). One factor in the rapid increase of

Swedish and the US productivity has been the globalisation process where

assembly has off-shored to the developing countries such as to Asia. However,

value added flows to the home country where high-skill tasks such as headquarter,

R&D, marketing locate.

350

Finland

300

Sweden

250 Germany

USA

200

EUR

150

100

50

0

1975 1980 1985 1990 1995 2000 2005 2010

Sources:

ETLA (2012). Toimialakatsaus, Suhdanne 2012:2.

Hyvärinen, J. (2011). Productivity: An International Comparison, ETLA Discussion Papers

No. 1264.

Kaitila, V. – A. Nevalainen – M. Maliranta – R. Mankinen (2008). Tuottavuuden

mittaaminen – Suomi kansainvälisessä vertailussa, ETLA Discussion Papers No. 1123.

Maliranta, M. – P. Rouvinen (2004). Informational Mobility and Productivity – Finnish

Evidence, ETLA Discussion Papers No. 919.

OECD STAN Database 2013.

Tekes Strategic Intelligence Unit