Energy & Commodities, No.3, 14 March 2011

•

1 like•320 views

Energy & Commodities, No.3, March 2011. We need to accept the “slow fix”

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (7)

Similar to Energy & Commodities, No.3, 14 March 2011

Similar to Energy & Commodities, No.3, 14 March 2011 (19)

More from Swedbank

More from Swedbank (20)

Recently uploaded

Recently uploaded (20)

Energy & Commodities, No.3, 14 March 2011

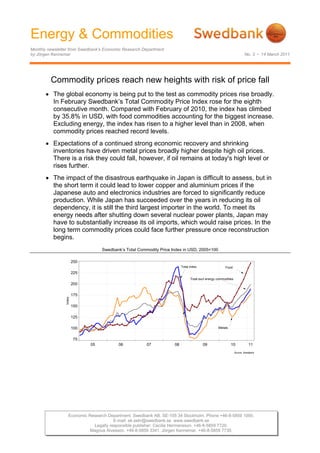

- 1. Energy & Commodities Monthly newsletter from Swedbank’s Economic Research Department by Jörgen Kennemar No. 3 • 14 March 2011 Commodity prices reach new heights with risk of price fall • The global economy is being put to the test as commodity prices rise broadly. In February Swedbank’s Total Commodity Price Index rose for the eighth consecutive month. Compared with February of 2010, the index has climbed by 35.8% in USD, with food commodities accounting for the biggest increase. Excluding energy, the index has risen to a higher level than in 2008, when commodity prices reached record levels. • Expectations of a continued strong economic recovery and shrinking inventories have driven metal prices broadly higher despite high oil prices. There is a risk they could fall, however, if oil remains at today's high level or rises further. • The impact of the disastrous earthquake in Japan is difficult to assess, but in the short term it could lead to lower copper and aluminium prices if the Japanese auto and electronics industries are forced to significantly reduce production. While Japan has succeeded over the years in reducing its oil dependency, it is still the third largest importer in the world. To meet its energy needs after shutting down several nuclear power plants, Japan may have to substantially increase its oil imports, which would raise prices. In the long term commodity prices could face further pressure once reconstruction begins. Swedbank’s Total Commodity Price Index in USD, 2005=100 250 Total index Food 225 Total excl energy commodities 200 175 Index 150 125 100 Metals 75 05 06 07 08 09 10 11 Source: Swedbank Economic Research Department. Swedbank AB. SE-105 34 Stockholm. Phone +46-8-5859 1000. E-mail: ek.sekr@swedbank.se www.swedbank.se Legally responsible publisher: Cecilia Hermansson. +46-8-5859 7720. Magnus Alvesson. +46-8-5859 3341. Jörgen Kennemar. +46-8-5859 7730.

- 2. Energy & Commodities Monthly newsletter from Swedbank’s Economic Research Department by Jörgen Kennemar No. 3 • 14 March 2011 Swedbank’s Total Commodity Price Index rose also risen substantially, but are still below the by an average of 4.4% in USD in February previous peak two and a half years ago. Other compared with the previous month. It was the agricultural products such as cotton have also eighth consecutive monthly increase, with the reached record highs this year, which is raising index reaching its highest level since commodity costs for the textile industry. September 2008. In euro, the price increase was slightly lower, at 2.2%. The krona’s The substantial price rise is being driven by appreciation against the dollar means that lower supplies of foods and other agricultural commodity prices gained a more modest 0.6% commodities due to poor harvests, though also in SEK between January and February. because of growing demand around the world. Excluding energy, the index is higher than two This has led to declining inventory levels. and a half years ago. That supply restrictions Demand is also affected by efforts by several are becoming more common is a sign of countries to build up their inventories to slow insufficient production capacity as the domestic inflation pressures and reduce the economy improves. The global financial crisis risk of social tensions. This is cutting into may have delayed new investments in supplies on the global market, causing prices commodity industries. Low interest rates and to rise. High oil prices also tend to raise food unconventional measures taken by central prices, since oil is an important input good in banks, like buying government debt to agricultural production. We think food prices stimulate the economy, have created greater could rise even more in the months ahead due liquidity in financial markets and may have to higher oil prices and shrinking inventories. added fuel to the commodity price rise in the Not until the second half of 2011 is it likely that last year. To ensure access to commodities prices could fall from today's high levels, and reduce price volatility, investments will be provided that production rises sharply and needed to expand future production capacity. It inventories recover. Experience from the food is also important that commodities are crisis in 2008 shows that high prices often lead consumed more efficiently, especially by to higher production. At the same time emerging economies, which account for a available acreage for food production is growing share of consumption. The current increasing. Further production disruptions such National People's Congress in Beijing is as bad weather, high oil prices and export planning several measures to reduce embargoes in several large net exporters commodity consumption and raise efficiency. increase the risk that food prices could While this may eventually reduce China's continue higher. vulnerability, in the short term it will not alleviate the problem that supply is rising more Oil price shock threatens the global slowly than demand. economy The global economic rebound and cold winter Food prices noted the largest price increase in pushed oil prices above USD 100 a barrel Swedbank’s Commodity Price Index in even before the political turbulence in North February, and since the start of the year have Africa began in late January. Global risen by nearly 11% on average in USD, more consumption rose by 3.3% in 2010 to 87.8 than crude and metals. After increasing by just billion barrels a day, or 1.7 billion barrels more over 50% since last summer, Swedbank’s than the last peak in 2008. Most of the Price Index for food commodities is higher than increase is coming from outside the OECD, led during the food crisis in 2008. This applies to by Asia excluding Japan. This trend has coffee, sugar, beverages and several grains strengthened in recent years as OECD such as barley and corn. Wheat prices have countries have reduced their consumption. The Economic Research Department. Swedbank AB. SE-105 34 Stockholm. Phone +46-8-5859 1000. E-mail: ek.sekr@swedbank.se www.swedbank.se Legally responsible publisher: Cecilia Hermansson. +46-8-5859 7720. Magnus Alvesson. +46-8-5859 3341. Jörgen Kennemar. +46-8-5859 7730.

- 3. Energy & Commodities Monthly newsletter from Swedbank’s Economic Research Department, continued No. 3 • 14 March 2011 growing dependency on oil in emerging days. Uncertainty about future oil supplies is economies will continue in the years ahead as growing at a time when the global economy is buying power rises and a larger middle class getting stronger. The International Energy takes shape. Agency (IEA) is predicting that global oil consumption will increase by 1.5 million barrels Oil production climbed by 2.5% in 2010 to 83.7 a day in 2011, which corresponds to Libya's billion barrels a day, with OPEC generating previous oil production volume. Oil futures nearly half the increase, while production suggest that high prices will persist in 2011, volume in OECD countries as a whole was with a price of around USD 115 dollar a barrel unchanged. Although demand grew faster than for delivery in December, before falling to USD supply, supplies remain good, as indicated by 110 for delivery in late 2012. The price picture the OECD’s inventories, which are above their could change quickly if the political situation historical average for the period 2005-2009. It stabilises, which could drop prices to USD 100, is noteworthy, however, that price of Northern which we think is more reasonable considering European oil (Brent crude) is significantly fundamentals in the oil market. Uncertainty is higher (USD 15 more at the time of writing) great, however, so we cannot rule out than North American (WTI crude), which is significantly higher oil prices if political priced in the US market. In addition to quality concerns in the region continue. differences – WTI contains less sulphur than Northern European oil – the big price Although the global economy is less difference is due to major regional imbalances, dependent on oil than during previous oil price with a lower supply of Brent crude in Europe shocks, a substantial rise in prices will and a growing surplus of WTI in the US. adversely affect growth. The rule of thumb is that if the price of oil rises by 10%, global Crude oil consumption, millions barrels/day growth will slow by 0.2% in the first year and 50.0 0.4% in the second. Our assumption of a year- 47.5 on-year increase of 25% in oil prices in 2011 45.0 means growth could slow even more, i.e., 42.5 Barrel/Day (millions) 40.0 upwards of one percentage point over a two- 37.5 year period, which would also affect 35.0 32.5 commodity demand. It is important, however, 30.0 to qualify how higher oil prices affect global 27.5 economy – whether through increased demand 25.0 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 or supply shortages, the latter of which would OECD Total Non-OECD Source: Reuters EcoWin probably have a greater negative impact. When the political conflict in the Middle East Oil futures for Brent crude spread to Libya in February, it caused growing 120 concerns about future oil supplies from OPEC, 110 which accounts for one third of global production, and oil prices rose to slightly over 100 USD 115 a barrel from USD 103 in early 90 February. Despite the Libyan oil production 80 represents only 2% of the global total, the 70 problem is uncertainty whether political developments in the region could jeopardize 60 jan feb mar apr maj jun jul aug sep okt nov dec jan feb mar supplies from major producers such as Saudi Spot price 10 Brent Crude Futures Dec 2011 Brent Crude Futures Dec 2012 11 Source: Reuters EcoWin Arabia, Iran and Iraq, which supply 40% of OPEC’s total production. Available production Tighter supply of metals capacity in OPEC countries of 4-6 million The price trend for metals is continuing, and in barrels a day can keep prices in check. Part of February prices rose by 4.2% in USD from the this capacity is replacing Libya's production, which has dropped substantially in recent previous month. Nickel accounted for the 3 (6)

- 4. Energy & Commodities Monthly newsletter from Swedbank’s Economic Research Department, continued No. 3 • 14 March 2011 largest increase (10.3%), followed by zinc medium-term goal of authorities there. In total, (32%) and copper (3.2%). Lead fell the most in steel production is expected to rise by 5% this price in the last month. Supply conditions for year. many metals have tightened as demand outpaces production. This is especially true of The powerful earthquake in Japan could have copper, tin and iron ore, where prices are at an impact on global metal prices, even though record highs and inventories are expected to the affected region accounts for only about 2% reach critically low levels in 2011, even if of the country's GDP. The Japanese auto and actual inventory data do not show it yet. The electronics industries will face serious increase in copper inventories since December production and delivery disruptions, which has not prevented prices from rising. should reduce aluminium and copper Expectations of further economic expansion in consumption. Another uncertainty affecting Asia, capacities shortages and lower ore Japanese industry is the risk of an energy quality in existing mines are also contributing shortage after several nuclear power to rising prices. International experts predict an generators have been shut down following the increase in copper consumption of around explosion in Fukushima and for safety reasons. 4.5% in 2011, while production is expected to Since the oil crisis in the 1970s, when oil gain just over 1%. Aluminium, nickel and zinc supplied two thirds of the country's electricity inventories are not as constrained, so price production, a large share has been replaced by increases for these metals are expected to be nuclear power. The earthquake and damage to lower. The chances of further increases in buildings and infrastructure could also limit the metal prices will decline if oil prices remain supply of steel on the global market if a larger high. share of the 100 million tons Japan produces were used domestically instead of exported. Inventory levels for metals, millions of tons Jörgen Kennemar 1.0 225000 0.9 200000 Nickel, right scal 0.8 175000 0.7 150000 Ton (metric) (millions) 0.6 Copper 125000 Ton (metric) 0.5 Zink 100000 0.4 75000 0.3 50000 0.2 25000 0.1 0 Lead 0.0 -25000 00 01 02 03 04 05 06 07 08 09 10 11 Source: LME, Reuters EcoWin Global steel production increased by as much as 15% in 2010, with China accounting for 44%, followed by Japan at 8%. Production volume of over 1.4 billion tons last year was a record high, which is driving iron ore prices higher. At the same time the supply of iron ore in the global market has been hurt by lower exports from India (the world's third largest exporter after Australia and Brazil), due to rising domestic demand and export restrictions. Spot prices of iron ore, which now serve as a guide for quarterly prices, consistently point higher in the next quarter. Estimates of a further increase in Chinese steel production would indicate high iron ore prices, despite that China’s expansion is expected to slow slightly in 2011, which is the 4 (6)

- 5. Energy & Commodities Monthly newsletter from Swedbank’s Economic Research Department by Jörgen Kennemar No. 3 • 14 March 2011 Swedbank Commodity Index - US$ - Swedbank Commodity Index - SKr - Basis 2000 = 1oo 14/03/11 Basis 2000 = 1oo 14/03/11 12.2010 1.2011 2.2011 12.2010 1.2011 2.2011 Total index 314.2 327.1 341.3 Total index 233.6 237.1 238.6 Per cent change month ago 5.8 4.1 4.4 Per cent change month ago 6.1 1.5 0.6 Per cent change year ago 25.0 25.5 35.8 Per cent change year ago 19.7 17.2 20.3 Total index exclusive energy 292.7 308.7 318.9 Total index exclusive energy 217.6 223.8 222.9 Per cent change month ago 3.1 5.5 3.3 Per cent change month ago 3.4 2.8 -0.4 Per cent change year ago 33.2 37.5 47.6 Per cent change year ago 27.6 28.4 30.7 Food, tropical beverages 286.2 302.5 317.6 Food, tropical beverages 212.8 219.3 222.0 Per cent change month ago 6.0 5.7 5.0 Per cent change month ago 6.3 3.1 1.2 Per cent change year ago 26.1 32.2 45.6 Per cent change year ago 20.8 23.5 29.0 Cereals 278.9 294.7 314.5 Cereals 207.4 213.7 219.8 Per cent change month ago 8.5 5.7 6.7 Per cent change month ago 8.8 3.0 2.9 Per cent change year ago 36.2 49.4 67.6 Per cent change year ago 30.5 39.5 48.4 Tropical beverages and tobacco 301.5 317.0 337.8 Tropical beverages and tobacco 224.2 229.8 236.1 Per cent change month ago 5.7 5.1 6.6 Per cent change month ago 6.0 2.5 2.7 Per cent change year ago 22.5 24.0 38.8 Per cent change year ago 17.4 15.8 23.0 Coffee 183.8 196.8 215.2 Coffee 136.7 142.7 150.4 Per cent change month ago 5.7 7.1 9.3 Per cent change month ago 6.0 4.4 5.4 Per cent change year ago 47.0 55.1 74.4 Per cent change year ago 40.9 44.9 54.5 Oilseeds and oil 258.0 276.4 276.1 Oilseeds and oil 191.8 200.4 193.0 Per cent change month ago 4.8 7.1 -0.1 Per cent change month ago 5.1 4.5 -3.7 Per cent change year ago 28.7 44.4 50.2 Per cent change year ago 23.3 34.9 33.0 Industrial raw materials 294.6 310.5 319.3 Industrial raw materials 219.0 225.1 223.2 Per cent change month ago 2.3 5.4 2.8 Per cent change month ago 2.6 2.8 -0.9 Per cent change year ago 35.4 39.0 48.2 Per cent change year ago 29.7 29.9 31.2 Agricultural raw materials 193.2 200.8 207.0 Agricultural raw materials 143.6 145.6 144.7 Per cent change month ago 1.3 3.9 3.1 Per cent change month ago 1.6 1.4 -0.6 Per cent change year ago 23.1 26.5 31.3 Per cent change year ago 18.0 18.2 16.3 Cotton 140.8 151.6 185.8 Cotton 104.7 109.9 129.9 Per cent change month ago 6.7 7.7 22.6 Per cent change month ago 7.0 5.0 18.1 Per cent change year ago 88.5 110.8 149.4 Per cent change year ago 80.6 97.0 120.9 Softwood 144.6 144.2 144.6 Softwood 107.5 104.5 101.1 Per cent change month ago -3.1 -0.3 0.3 Per cent change month ago -2.9 -2.8 -3.3 Per cent change year ago 3.4 4.0 6.0 Per cent change year ago -0.9 -2.8 -6.1 Woodpulp 949.8 949.0 949.1 Woodpulp 706.2 688.0 663.3 Per cent change month ago -0.7 -0.1 0.0 Per cent change month ago -0.5 -2.6 -3.6 Per cent change year ago 19.3 16.5 13.0 Per cent change year ago 14.3 8.9 0.0 Non-ferrous metals 275.6 288.3 300.3 Non-ferrous metals 204.9 209.0 209.9 Per cent change month ago 4.4 4.6 4.2 Per cent change month ago 4.7 2.0 0.4 Per cent change year ago 22.2 21.6 36.7 Per cent change year ago 17.0 13.6 21.1 Copper 9130.1 9563.7 9867.2 Copper 6788.0 6933.7 6896.3 Per cent change month ago 7.8 4.7 3.2 Per cent change month ago 8.1 2.1 -0.5 Per cent change year ago 31.1 29.5 44.4 Per cent change year ago 25.6 21.0 27.9 Aluminium 2347.4 2440.2 2507.8 Aluminium 1745.2 1769.1 1752.7 Per cent change month ago 0.6 4.0 2.8 Per cent change month ago 0.9 1.4 -0.9 Per cent change year ago 7.8 9.1 22.7 Per cent change year ago 3.2 1.9 8.7 Lead 2404.9 2600.2 2586.2 Lead 1788.0 1885.1 1807.5 Per cent change month ago 1.2 8.1 -0.5 Per cent change month ago 1.5 5.4 -4.1 Per cent change year ago 3.5 9.8 21.3 Per cent change year ago -0.9 2.6 7.5 Zinc 2272.7 2373.9 2464.7 Zinc 1689.7 1721.1 1722.6 Per cent change month ago -0.8 4.5 3.8 Per cent change month ago -0.5 1.9 0.1 Per cent change year ago -3.9 -2.5 14.4 Per cent change year ago -8.0 -8.9 1.3 Nickel 24055.5 25609.4 28250.1 Nickel 17884.7 18566.8 19744.4 Per cent change month ago 5.0 6.5 10.3 Per cent change month ago 5.3 3.8 6.3 Per cent change year ago 41.6 38.9 49.7 Per cent change year ago 35.6 29.8 32.6 Iron ore, steel scrap 607.0 653.3 660.0 Iron ore, steel scrap 451.3 473.6 461.3 Per cent change month ago 0.7 7.6 1.0 Per cent change month ago 1.0 5.0 -2.6 Per cent change year ago 73.4 86.6 87.8 Per cent change year ago 66.1 74.3 66.3 Energy raw materials 323.8 335.2 351.3 Energy raw materials 240.7 243.0 245.5 Per cent change month ago 6.8 3.5 4.8 Per cent change month ago 7.2 1.0 1.0 Per cent change year ago 21.9 21.2 31.6 Per cent change year ago 16.8 13.2 16.6 Coking coal 454.7 490.5 479.3 Coking coal 338.1 355.6 335.0 Per cent change month ago 11.8 7.9 -2.3 Per cent change month ago 12.1 5.2 -5.8 Per cent change year ago 48.5 34.2 37.8 Per cent change year ago 42.3 25.4 22.0 Crude oil 317.8 328.1 345.4 Crude oil 236.3 237.9 241.4 Per cent change month ago 6.5 3.2 5.3 Per cent change month ago 6.8 0.7 1.5 Per cent change year ago 20.5 20.4 31.2 Per cent change year ago 15.5 12.5 16.2 Source : SWEDBANK and HWWA-Institute for Economic Research Hamburg Source : SWEDBANK and HWWA-Institute for Economic Research Hamburg Swedbank Economic Research Department Swedbank’s monthly Energy & Commodities newsletter is published as a service to our customers. We believe that we have used reliable sources and methods in the preparation SE-105 34 Stockholm, Sweden of the analyses reported in this publication. However, we cannot guarantee the accuracy or Phone +46-8-5859 7740 completeness of the report and cannot be held responsible for any error or omission in the ek.sekr@swedbank.se underlying material or its use. Readers are encouraged to base any (investment) decisions www.swedbank.se on other material as well. Neither Swedbank nor its employees may be held responsible for Legally responsible publisher losses or damages, direct or indirect, owing to any errors or omissions in Swedbank’s Cecilia Hermansson, +46-88-5859 7720 monthly Energy & Commodities newsletter. Magnus Alvesson, +46-8-5859 3341 Jörgen Kennemar, +46-8-5859 7730 Economic Research Department. Swedbank AB. SE-105 34 Stockholm. Phone +46-8-5859 1000. E-mail: ek.sekr@swedbank.se www.swedbank.se Legally responsible publisher: Cecilia Hermansson. +46-8-5859 7720. Magnus Alvesson. +46-8-5859 3341. Jörgen Kennemar. +46-8-5859 7730.