Difference between a public and a private company under Companies Act, 2013

•Download as DOCX, PDF•

17 likes•11,142 views

Difference between a Public Limited Company and a Private Limited Company as per the provisions contained in the Companies Act, 2013 and relevant rules and regulations prescribed thereunder.

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Difference between a public and a private company under Companies Act, 2013

Similar to Difference between a public and a private company under Companies Act, 2013 (20)

Recently uploaded

Recently uploaded (20)

Difference between a public and a private company under Companies Act, 2013

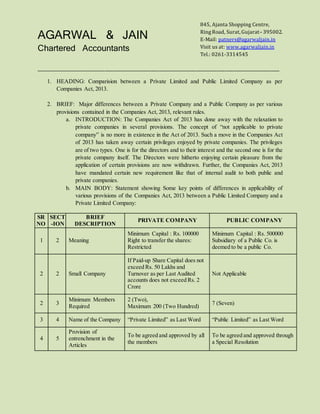

- 1. AGARWAL & JAIN Chartered Accountants _____________________________________________________________________________________ 1. HEADING: Comparision between a Private Limited and Public Limited Company as per Companies Act, 2013. 2. BRIEF: Major differences between a Private Company and a Public Company as per various provisions contained in the Companies Act, 2013, relevant rules. a. INTRODUCTION: The Companies Act of 2013 has done away with the relaxation to private companies in several provisions. The concept of “not applicable to private company” is no more in existence in the Act of 2013. Such a move in the Companies Act of 2013 has taken away certain privileges enjoyed by private companies. The privileges are of two types. One is for the directors and to their interest and the second one is for the private company itself. The Directors were hitherto enjoying certain pleasure from the application of certain provisions are now withdrawn. Further, the Companies Act, 2013 have mandated certain new requirement like that of internal audit to both public and private companies. b. MAIN BODY: Statement showing Some key points of differences in applicability of various provisions of the Companies Act, 2013 between a Public Limited Company and a Private Limited Company: SR NO SECT -ION BRIEF DESCRIPTION PRIVATE COMPANY PUBLIC COMPANY 1 2 Meaning Minimum Capital : Rs. 100000 Right to transfer the shares: Restricted Minimum Capital : Rs. 500000 Subsidiary of a Public Co. is deemed to be a public Co. 2 2 Small Company If Paid-up Share Capital does not exceed Rs. 50 Lakhs and Turnover as per Last Audited accounts does not exceed Rs. 2 Crore Not Applicable 2 3 Minimum Members Required 2 (Two), Maximum 200 (Two Hundred) 7 (Seven) 3 4 Name of the Company “Private Limited” as Last Word “Public Limited” as Last Word 4 5 Provision of entrenchment in the Articles To be agreed and approved by all the members To be agreed and approved through a Special Resolution 845, Ajanta Shopping Centre, RingRoad, Surat, Gujarat–395002. E-Mail: patners@agarwaljain.in Visit us at: www.agarwaljain.in Tel.: 0261-3314545

- 2. 5 23 Issue of Securities By way of Right Issue or Bonus Issue Through Private Placement To Public through Prospectus (“Public Offer”) By way of Right Issue or Bonus Issue Through Private Placement 6 29 Public Offer to be in Dematerialised Form Not Applicable In case of public offer of securities, the securities have to be in Dematerialised Form 7 40 Securities in Public Offer to be listed in Stock exchanges Not Applicable Securities offered in Public Offer,to be listed in Recognised Stock Exchanges 8 67 Purchase / Loan for Purchase of Own Shares Not allowed to Purchase its own Shares Not allowed to Purchase its own Shares; No Financial assistance to be given to purchase its own shares 9 73 Acceptance of Deposits Not allowed to accept deposit Allowed if Paid up share capital is Rs. 100 Crore or more or Turnover of Rs. 500 Crore or more 10 103 Quorum of Meetings Two members personally present Five in case of Members upto 1000; Fifteen in case of Members more than 1000, upto 5000; Thirty in case of Members exceed 5000. 11 138 Internal Audit Applicable in case of : 1. Turnover >= Rs. 200 Crore in preceding financial year, OR 2. Loans from bank or NBFCs >= Rs. 100 Crore in preceding financial year Applicable in case of : 1. Paid Up Capital >= Rs. 50 Crore in the preceding financial year, OR 2. Turnover >= Rs. 200 Crore in preceding financial year, OR 3. Loans from bank or NBFCs >= Rs. 100 Crore in preceding financial year, OR 4. Public Deposit >= Rs. 25 Crore in preceding financial year 12 134 (3)(p) Annual Evaluation in the Board’s Report Not Applicable If Paid up share capital is Rs. 25 Crore or more, the details of annual evaluation in the Board’s Report 13 139 (2) Rotation of Auditor Applicable in case of Paid up Capital is Rs. 20 Crore or more Applicable in case of Paid up Capital is Rs. 10 Crore or more 14 149 No. of Directors and Independent Directors 2 (Two); Not required to appoint independent director 3 (Three); and In case of Listed Companies, at least One-Third as independent directors

- 3. 15 152 Retirement by rotation - Appointment of Director Not Applicable At least two-third of total no. of directors be liable to retire by rotation and eligible of being re- appointed in AGM 16 190 Contract of Employment with Managing Director / Whole Time Director Not Required (Optional) Compulsorily Required 17 197 Restriction on Managerial Remuneration No restriction on amount of managerial remuneration Managerial Remuneration is: Restricted to 11% of Net profit (subject to conditions); OR at least Rs. 30 lakh p.a. depending upon paid up capital c. Conclusion: From the above discussion, it is evident that many provisions as applicable to Public Limited Companies are now made applicable to Private Limited Companies as well under the Companies Act, 2013. For MSMEs, earlier the Private Companies were preferable mode of entity for running business operations. However,with the new Companies Act,2013, some major advantages enjoyed by Private Companies have been withdrawn. With the introduction of Limited Liability Partnership, a new form of entity is introduced through which the benefits of legal entity can be reaped without being tied up with the much legal formalities as enumerated in the case of Private / Public Limited Companies. 3. Details of the Author: a. NAME: FCA Sachin D Jain b. ADDRESS: 845, 8th Floor, Ajanta Shopping Centre, Ring Road, Surat, Gujarat – 395002 c. PHOTOGRAPH:Attached herewith. 4. Consent for exclusive publication: This article is exclusive sent to taxguru.in for its publication on its website.